GPMT - Don't Get Scrooged

2023-12-21 07:00:00 ET

Summary

- Scrooge-like behavior is associated with being a miser who only cares about money and neglects others' feelings.

- The article emphasizes the importance of making the most of one's financial resources early on and avoiding investments with high risks.

- In this article, I will provide readers with a list of three REITs to avoid at all costs.

I'm sure you know the term Scrooge.

You may have never read Charles Dickens' A Christmas Carol or seen any of the movie adaptations. But the name "Scrooge" is nonetheless embedded in our culture.

When people get labeled that way, it's not a compliment.

It means they're misers.

That they only care about money.

That they'd easily throw others' feelings (and perhaps their bodies) under a bus if it meant saving a coin.

It's a shame considering the redemptive story that Dickens takes Ebenezer Scrooge on. The book ends like this (as copied from SparkNotes ):

"Scrooge… became as good a friend, as good a master, and as good a man, as the old city knew, or any other good old city, town, or borough, in the good old world… and it was always said of him, that he knew how to keep Christmas well, if any man alive possessed the knowledge. May that be truly said of us, and all of us! And so, as Tiny Tim observed, God Bless Us, Every One!

Admittedly, the bulk of the book has him acting inexcusably. So I guess we can chalk this up as a fiction-based caution that actions always have consequences.

With that in mind, let's not create a legacy of mistakes. Let's commit to making the most of what we have as early on as possible.

In a financial sense, that includes avoiding the sucker yields. They might pay off in the moment, but they only lead to eventual grief.

"The fire's gone cold, Mr. Scrooge"

In case you really have never read or watched A Christmas Carol , here's one early-on exchange. It's between Ebenezer Scrooge himself and his overworked, underappreciated clerk, Bob Cratchit.

I lifted it from the 1984 adaption starring George C. Scott, as captured on IMDB :

[ Bob goes to the fireplace and reaches for some coal ]

Ebenezer Scrooge: Mr. *Cratchit*!

Bob Cratchit: The fire's gone cold, Mr. Scrooge.

Ebenezer Scrooge: [ calmly covers his eyes with both hands ] Come over here, Mr. Cratchit.

[ Bob stands in front of Scrooge, who tugs on his right sleeve ]

Ebenezer Scrooge: What is this?

Bob Cratchit: A shirt.

Ebenezer Scrooge: [ points to his waistcoat ] And this?

Bob Cratchit: A waistcoat.

Ebenezer Scrooge: [ tugs on his coat ] And this?

Bob Cratchit: A coat.

Ebenezer Scrooge: These are garments, Mr. Cratchit. Garments were invented by the human race as protection against the cold. Once purchased, they may be used indefinitely for the purpose for which they are intended. *Coal*... burns. Coal is momentary, and coal is costly. There will be no more coal burned in this office today. Is that quite clear, Mr. Cratchit?

Bob Cratchit: Yes, sir.

Ebenezer Scrooge: Now, please get back to work before I am forced to conclude that your services are no longer required.

Bob Cratchit: Yes, sir.

And you complain about your boss!

Scrooge also asks two charity workers if there are any debtors prisons and workhouses left. And when they say yes, he responds with sardonic relief, saying that that's what they're there for: to handle the poor. His finances are best spent elsewhere.

Or, to capture his message a bit better, they're best not spent elsewhere, sitting in his bank account.

Because that's what misers do. They make money, and they hoard it, never to be enjoyed in more than thought.

"But, Mr. Scrooge, It's Christmas!"

Now, my regular readers know I'm not a proponent of spending money on just anything.

This time of year, with a wife, five kids, two sons-in-law, a grandchild, a mom, and a brother, you'd better believe money gets spent. Vacations can be a time to treat yourself, too. And you know what? Sometimes it's okay just to splurge.

There are also necessities like food, shelter, and safety. Plus heating.

With all due respect to the old Scrooge, putting some coal on the fire so it doesn't go out in the cold of winter is well worth the expense.

But for the most part, pre-retirement, you really do want to focus more on making money than giving it away. It's how you prepare for an enjoyable retirement - another concept Scrooge didn't realize for decades.

The whole point of saving up is to get to the point where you can spend it carefree.

Of course, in order to save up, you have to make money. And then you have to keep it. And, ideally, you want to make more money off the money you've already made.

That's why I like real estate investment trusts, or REITs, so much. As a category, they offer not only long-term share price appreciation but also consistent dividends.

I can take those dividends pre-retirement and put them right back into buying up more dividend-paying stock. And after retirement, they can give me even more income to rely on.

When you buy the right ones.

There are exceptions. And those exceptions can drain you every bit as much as Scrooge drained the poor people who borrowed from him.

There's no such thing as a debtors' prison anymore. But you might find yourself wishing for one if you invest in a REIT with a sucker yield.

Don't Let These Sucker Yields Steal Your Presents

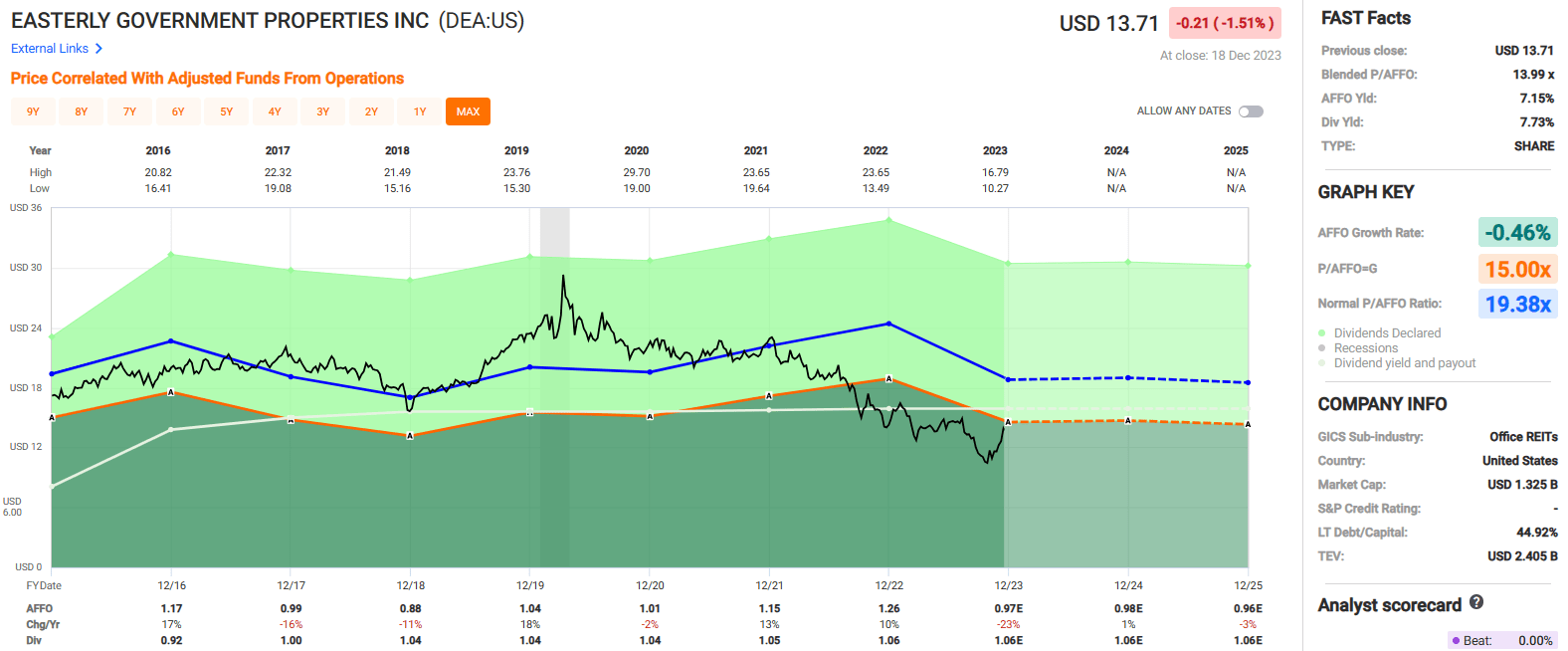

Easterly Government Properties, Inc. ( DEA )

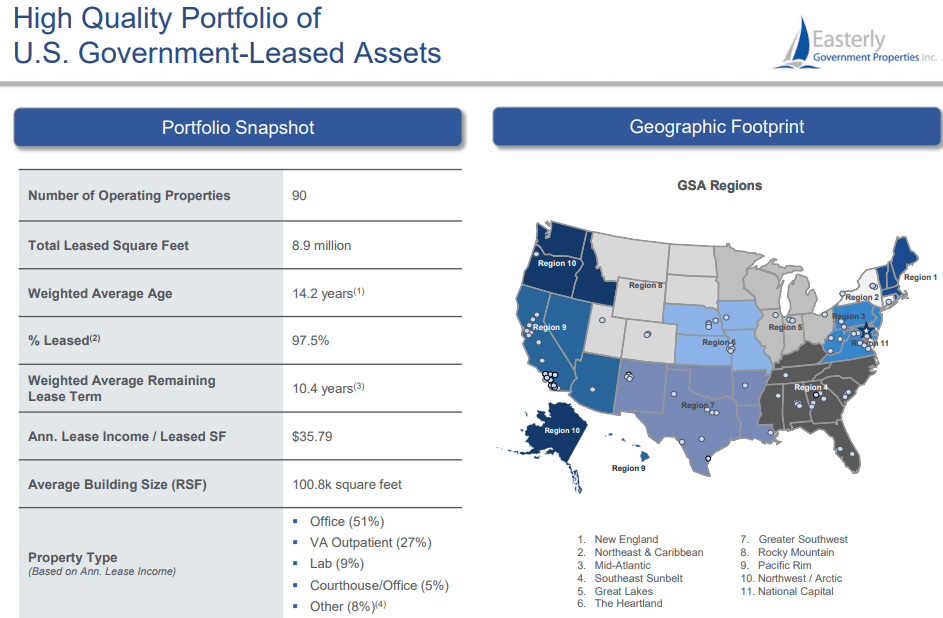

Easterly Government Properties is a REIT in the office sector that specializes in the development and acquisition of Class A properties that are leased to U.S. Government agencies that carry out critical and essential tasks.

DEA generates almost all of its rental revenue by leasing its commercial properties to government agencies through the General Services Administration ("GSA"), and 99% of its lease income is backed by the full faith and credit of the U.S. Government.

While principally all of its tenants are government agencies, not all of its properties are office buildings. Based on annualized lease income office properties makes up 51% of its portfolio, VA outpatient centers makes up 27%, Labs makes up 9%, and Courthouses makes up 5% of DEA's portfolio.

DEA owns or has an ownership interest in 90 operating properties in the U.S. covering roughly 8.9 million SF that are leased to 40 different government agencies. These include the U.S Food and Drug Administration ("FDA"), the Drug Enforcement Administration ("DEA"), and the Federal Bureau of Investigation ("FBI"). At the end of the third quarter, DEA's portfolio was 97.5% leased, with a weighted average lease term ("WALT") of 10.4 years.

{kind=link}

On October 31st DEA released its third quarter operating results and reported total revenues during the quarter of $72.0 million, compared to $75.0 million for the same period in 2022.

Funds from operations ("FFO") in 3Q-23 came in at approximately $30.0 million, or $0.28 per share, compared to FFO of $32.4 million, or $0.32 per share during 3Q-22.

Core FFO was reported at $30.2 million, or $0.29 per share, compared to Core FFO of $32.7 million, or $0.32 per share in the third quarter of 2022.

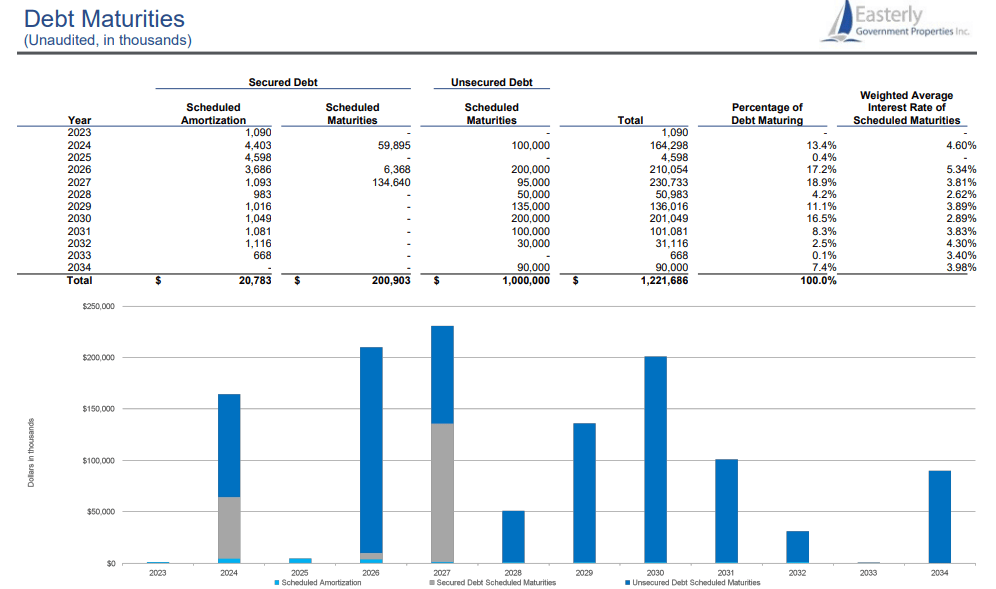

At the end of the third quarter, DEA's debt metrics were as follows:

- Net Debt to Total Enterprise Value: 49.4%

- Adjusted Net Debt to Pro Forma EBITDA: 6.7x

- Cash Fixed Charge Coverage Ratio: 3.3x

- % of Fixed Rate Debt: 100%

- W.A. interest rate: 4.0%

- W.A. Term to Maturity: 5 years.

{kind=link}

DEA filed its initial public offering in early 2015 and since that time they have not cut their dividend, but they have not grown it much, either.

In 2017, DEA increased their dividend by a respectable 8.70% and increased it by 4.00% the following year.

Since that time, though, DEA has either made no increase to its dividend or has increased its dividend by less than 1%. In total, over the last 6 years, DEA has had an annual average dividend growth rate of 2.43%.

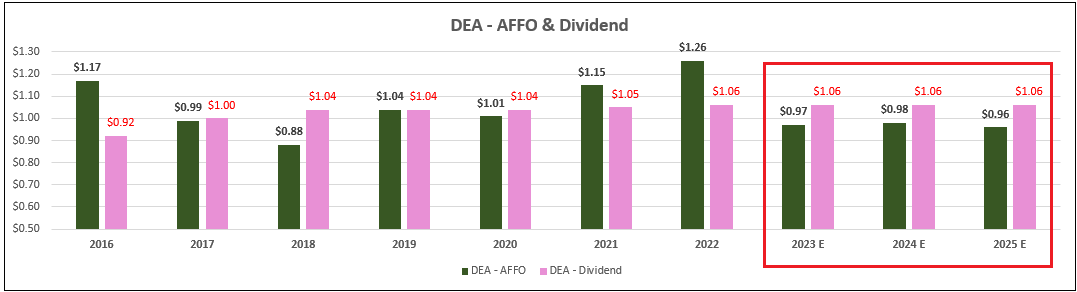

What worries me about DEA's future dividend is the high adjusted funds from operations ("AFFO") payout ratio that analysts are projecting over the next several years.

Analysts expect AFFO per share to fall from $1.26 in 2022 to $0.97 in the current year. This projection represents an expected decline in AFFO of roughly -23% and puts the AFFO payout ratio over 100%.

{kind=link}

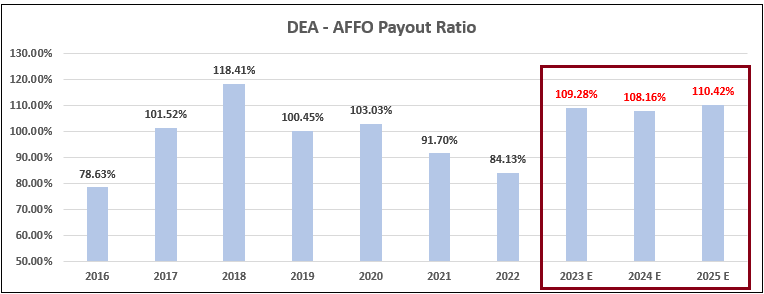

If analysts' expectations are on the mark, it would put DEA's AFFO payout ratio at 109.28% in 2023, and then at 108.16% and 110.42% in the years 2024 and 2025, respectively.

An AFFO payout ratio over 100% implies the company is paying out more in dividends than the free cash flow it generates and typically is a good indication that the company may cut its dividend.

{kind=link}

Since 2016, DEA has had an average AFFO growth rate of negative -0.46%. As previously mentioned, analysts expect AFFO per share to fall by -23% in 2023, increase by 1% in 2024, and then fall by -3% in 2025.

We see possible trouble on the horizon, as their AFFO is expected to fall below their current dividend payment, and the company's AFFO payout ratio is expected to exceed 100% for the next 3 years.

Currently, DEA pays a 7.73% dividend yield and trades at a P/AFFO of 13.99x, compared with its average AFFO multiple of 19.38x. We think it is highly likely that the current dividend is a suckers yield and rate DEA a sell.

We rate Easterly Government Properties a Sell / Avoid.

{kind=link}

Global Net Lease, Inc. ( GNL )

Global Net Lease is an internally managed REIT that specializes in acquiring commercial properties both domestically and internationally through sale-leaseback ("SLB") transactions.

Their SLBs typically involve mission critical properties leased to a single tenant on a net basis across the United States and Europe.

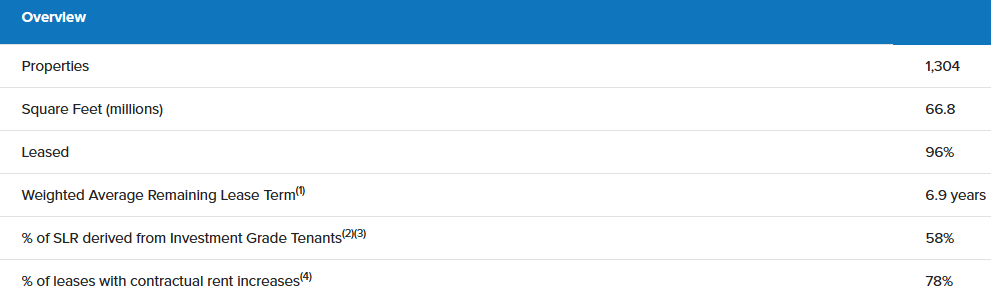

GNL's portfolio consists of more than 1,300 commercial properties covering approximately 66.8 million SF across 11 countries. At the end of the third quarter, GNL's portfolio was 96% leased with 815 tenants and a WALT of 6.9 years.

As a percentage of their straight line rent ("SLR"), GNL generated 81% from the United States and Canada, while the remaining 19% was derived from Europe. Additionally, GNL received approximately 58% of its SLR from investment-grade tenants.

{kind=link}

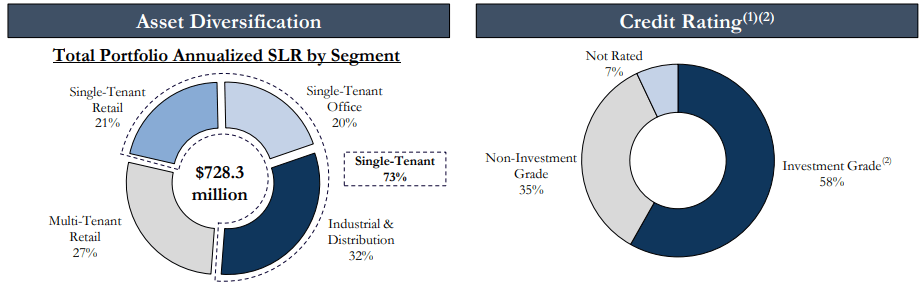

Global Net Lease owns multiple property types, including necessity retail, mission critical offices, and industrial properties.

As a percentage of SLR, industrial and distribution properties makes up 32% of GNL's portfolio, followed by multi-tenant retail at 27%. Single-tenant retail make up 21% and single-tenant office makes up approximately 20% of GNL's portfolio.

As previously mentioned, GNL receives approximately 58% of its SLR from IG tenants, 35% from non-investment grade tenants, and 7% from tenants that are not credit-rated.

{kind=link}

GNL released its third-quarter operating results in November and reported total revenue during the quarter of $118.2 million, compared with $92.6 million in the third quarter of 2022.

Core FFO was reported at $31.5 million, or $0.24 per share, compared to Core FFO of $48.3 million, or $0.47 per share for the comparable period in 2022.

AFFO was reported at $46.9 million, or $0.36 per share, compared to AFFO of $41.3 million, or $0.40 per share in the third quarter of 2022.

Additionally, GNL reported a net debt to adjusted EBITDA of 7.6x, a net debt to gross asset value ratio of 56.7%, and an interest coverage ratio of 2.5x.

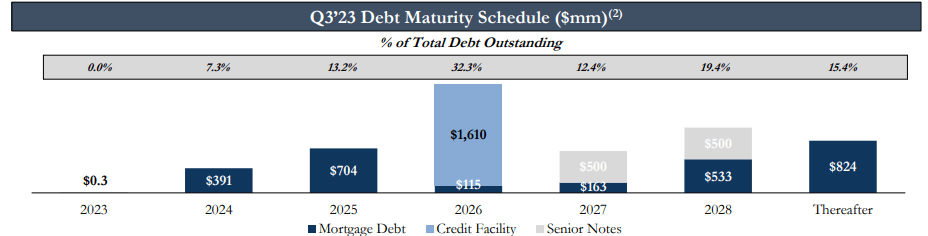

Their debt is 82% fixed rate with a weighted average interest rate of 4.7% and at the end of the third quarter, GNL had $319.4 million of liquidity and only 7.3% of their debt matures in 2024.

{kind=link}

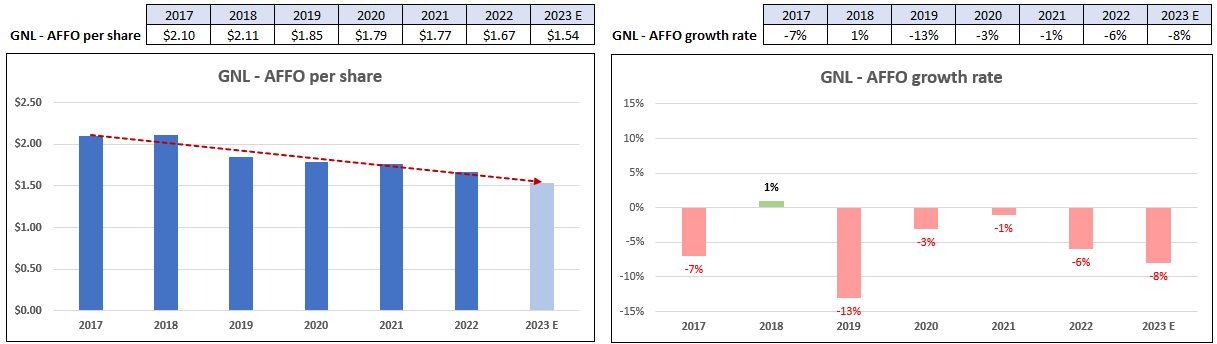

Over its recent history, GNL has displayed poor execution, with AFFO per share falling in each year between 2017 and 2022, with the exception of 2018, when GNL achieved 1% AFFO growth. To make matters worse, analysts expect AFFO to fall by -8% in 2023.

{kind=link}

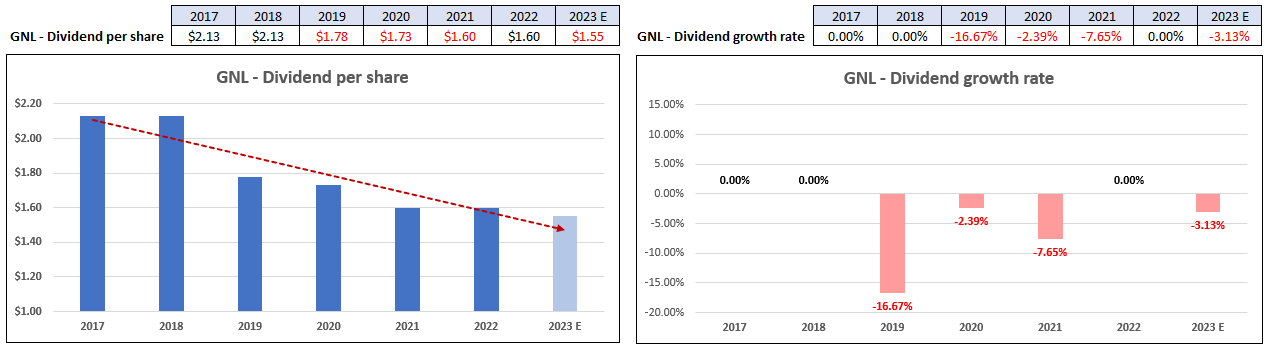

GNL's poor execution shows up in their dividend history as well, with multiple cuts made since 2017.

GNL maintained its dividend of $2.13 per share in 2017 and 2018 and then cut the dividend by 16.67% the following year to $1.78 per share.

GNL went on to cut the dividend by -2.39% in 2020, and by -7.65% in 2021.

They maintained the dividend in 2022, but analysts expect the dividend to be cut by another -3.13% in 2023.

We've already seen the beginning of GNL's latest dividend cuts, as their last quarterly dividend was declared for $0.354, compared to the previous quarter's dividend of $0.40 per share.

{kind=link}

One might think that GNL has a reasonable AFFO payout ratio after all the dividend cuts, but in spite of the cuts, their 2022 year-end AFFO payout ratio came in at 95.81%.

GNL's AFFO payout ratio was over 100% in 2017 & 2018. The payout ratio improved to 95.95% in 2019, but that was due to the almost 17% dividend cut they made that year.

After two more dividend cuts, GNL got its AFFO payout ratio down to 90.40% in 2021, but the following year their AFFO payout ratio crept back up to 95.81%

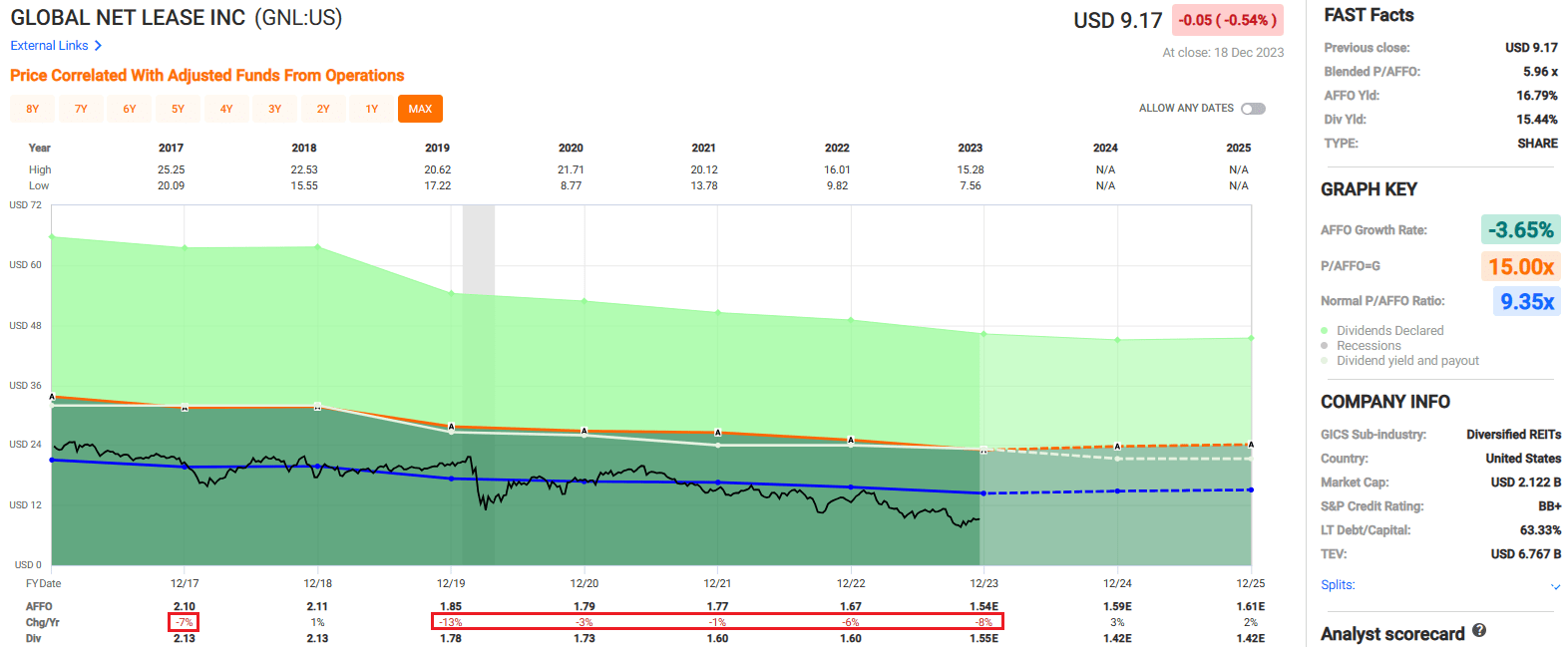

FAST Graphs (compiled by iREIT®)

GNL's latest dividend rate of $0.354 annualized comes to $1.42 per share. While analysts expect the 2023 dividend to be covered by AFFO earnings, we believe GNL's AFFO will continue to deteriorate given the company's past history of poor execution.

Since 2017, GNL has had a negative AFFO growth rate of -3.65% and a negative dividend growth rate of -4.45%.

Currently, GNL shares pay a 15.44% dividend yield, but we are cautious on management's execution and would not be surprised to see AFFO continue to fall which would inevitably lead to another dividend cut. GNL is trading at a P/AFFO of 5.96x, compared to its average AFFO multiple of 9.35x.

We rate Global Net Lease a Hold / Avoid.

{kind=link}

Granite Point Mortgage Trust Inc. ( GPMT )

GPMT is a mortgage REIT ("mREIT") that originates, invests in, and manages a portfolio of debt instruments which primarily consist of senior floating-rate loans that are secured by commercial real estate within the U.S.

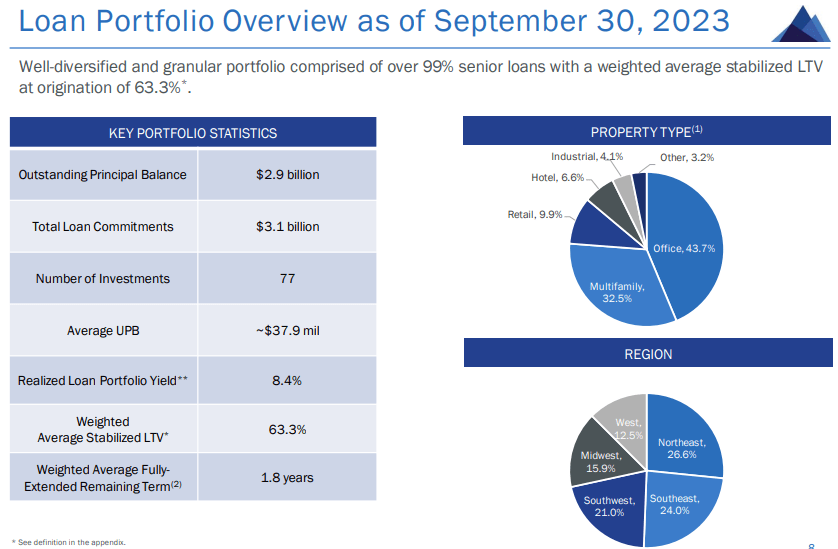

Their portfolio is comprised of 77 debt investments, with an outstanding principal balance of $2.9 billion, total loan commitments of $3.1 billion, and a weighted average origination loan-to-value ("LTV") of 63.3%.

More than 99% of GPMT's portfolio consists of senior loans and approximately 98% of their portfolio consists of floating rate loans. The loans in their portfolio are collateralized by multiple property types including multifamily, office, hospitality, and industrial real estate.

Office and multifamily are GPMT's largest property types and combined make up 76.2% of their portfolio. Office is their largest property type at 43.7%, followed by multifamily at 32.5%.

In addition to their two main property types, GPMT's portfolio includes 9.9% retail, 6.6% hotel, and 4.1% industrial.

{kind=link}

Granite Point Mortgage Trust has done a dismal job of returning value to their shareholders.

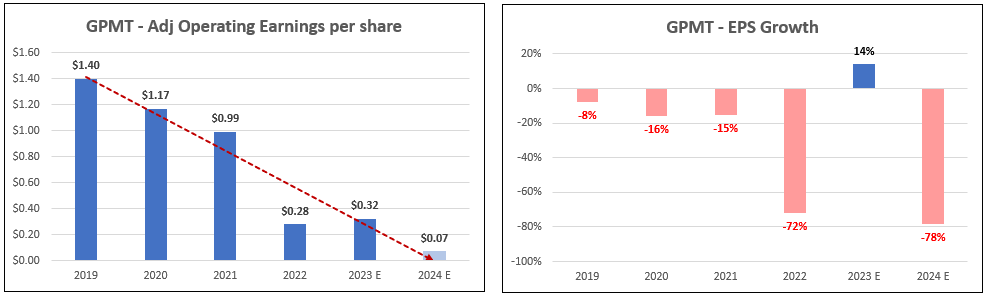

Their adjusted operating earnings per share ("EPS") fell from $1.40 in 2019 to just $0.28 by 2022. Analysts expect EPS to increase by 14% in 2023 but then fall by -78% in 2024.

From 2019 to 2022, GPMT has had negative EPS growth each year. The only positive EPS growth is estimated to occur in 2023, but that is expected to be followed by a significant decline in EPS in 2024.

{kind=link}

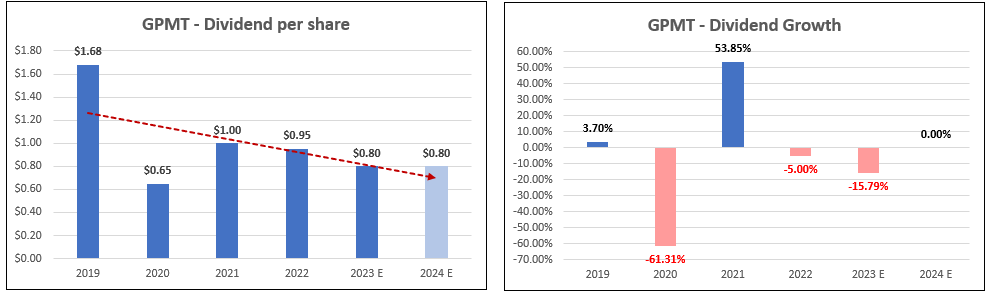

GPMT's dividend history doesn't look any better, with the dividend being cut by more than 60% in 2020.

The following year they increased the dividend from $0.65 to $1.00, representing an increase of 53.85%, only to cut the dividend again by 5.00% the very next year.

Analysts expect a more severe dividend cut of -15.79% in 2023, with expectations of no dividend growth in 2024.

We can already see the 2023 dividend cut, as GPMT reduced their quarterly dividend from $0.25 to $0.20 per share in the fourth quarter of 2022. Throughout 2023, GPMT has maintained its quarterly dividend of $0.20 per share.

{kind=link}

Meanwhile, GPMT has habitually paid out more in dividends than what they generate in adjusted operating earnings.

In 2019, GPMT had a dividend payout ratio of 120.00%. The payout ratio improved the following year to just 55.56%, but that was due to the -61.31% dividend cut they made in 2020 rather than earnings growth.

After GPMT increased its dividend by a substantial amount in 2021, its dividend payout ratio went back over 100% and was up to 339.29% by the end of 2022.

Analysts expect the 2023 year-end dividend payout ratio to come in around 250%, which is still absurdly high and likely cannot be sustained over the long term.

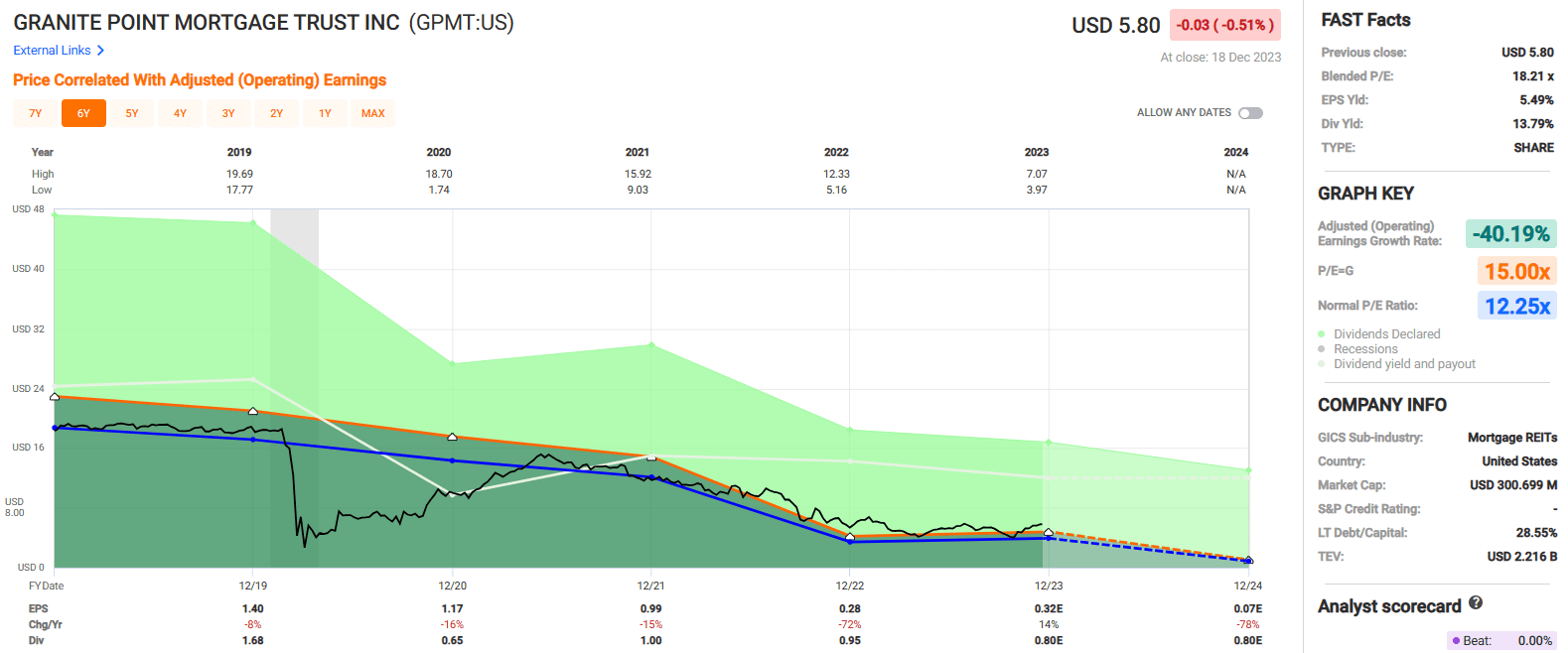

FAST Graphs (compiled by iREIT®)

Since 2019 GPMT has had a negative adjusted operating earnings growth rate of -40.19% and cut its dividend from $1.68 per share in 2019 to just $0.80 per share in 2023.

With deteriorating earnings and a dividend payout ratio exceeding 200%, this mortgage REIT is very likely to cut its dividend again.

To make matters worse, the stock is trading at a premium to its normal P/E ratio. Currently, GPMT pays a 13.79% dividend yield and trades at a P/E ratio of 18.21x, compared to its normal P/E ratio of 12.25x.

We believe that investors should avoid Granite Point Mortgage Trust.

{kind=link}

Avoid Dividend Cuts To Avoid Being Scrooged

Investors should avoid dividend cuts at all costs.

If you don't believe me, just take a look at Gladstone Commercial ( GOOD ) after the 20% dividend cut in January 2023.

{kind=link}

Of course, we warned readers in advance, literally days before the dividend cut.

Then earlier this week, Ready Capital ( RC ) said it was slicing its dividend for the second consecutive quarter, to $0.30 per share.

{kind=link}

Once again, I warned folks to steer clear of this sucker yield,

"In my opinion Ready Capital is a REIT to avoid. They pay a tempting 16.91% dividend yield, but this looks like a "suckers yield" to me. Ready Capital has shown a history of cutting their dividend which leads me to believe the company is at a risk of another cut given analysts' expectations of declining earnings."

I could provide many more examples of "sucker yields" that we warned you in advance; however, if you own them, the damage is already done.

My warning to you, my valued followers, please run from DEA, GNL and GMPT as far away as you can.

Run, run, as fast as you can, you can't catch me I'm the gingerbread man.

{kind=link}

For further details see:

Don't Get Scrooged