PTY - Don't Panic! Growing Your Income In A Volatile Market

2023-11-14 07:35:00 ET

Summary

- We've seen more uncertainty and increased volatility in the market recently. Investors need to be prepared for sell-offs.

- It's important to keep a clear head and not rush decisions in times of market volatility.

- Focus on your strategy, including portfolio yield, allocation to fixed income, individual diversification, and reinvestment resources.

Co-authored with Beyond Saving.

Since August, we have started seeing the market sell off. Then the market indexes started rebounding before the official start of a bear market. However, with recession risk high, investors will need to be prepared for days when everything sells off.

When prices are down, it is more important than ever to keep a clear head. There is a saying that has its roots in the U.S. Military: "Slow is smooth, smooth is fast."

Have you ever tried to rush but ended up clumsily fumbling around? – dropping things, making mistakes, and ultimately taking far more time to complete the task?

Then you watch your favorite professional sport on TV, and you will see professional athletes complete complicated moves in the blink of an eye – they make it look effortless and almost relaxed. The reason that they can reach this level of expertise is through relentless practice, doing the same thing over and over again at a very slow speed until it is instinctive. They might be moving fast, but they are never rushing. Being smooth and making deliberate controlled movements is far more important than speed alone. Slow is smooth, smooth is fast.

Know When To Stop

The market can move quickly. As a result, we are often tempted to be reactionary. When you wake up in the morning and see the whole market bleeding red, investors have one of two instincts: BUY! or SELL! The reality is that the best response is often to turn off your computer, grab a cup of coffee, and go about your day. It is important that you learn to recognize the warning signs that you should stop and step back before making a decision.

Investing is a marathon, not a sprint. You will be invested in the market for many decades, and over those decades, you will see some very large swings.

If you ever find yourself rushing to buy or sell – Stop .

If you are disturbed when your spouse comes into the room and tries to talk to you because you are trying to figure out what you should do – Stop .

If you are worrying about whether or not making a buy or sell is a good idea – Stop .

If you find yourself getting overly emotional – Stop .

If the idea of your Internet going out causes panic – Stop .

Your decisions should be made methodically. You should be able to pinpoint why you are buying a particular stock and why you are selling a particular stock. Understand the particular investment and how it fits into your overall strategy. Make your decisions in a principled manner based on your overall strategy.

Whenever you feel rushed and are making decisions without considering your strategy, stop and walk away; come back when you are able to think through your decisions in a principled manner.

Maybe you only need to step away for a coffee break, or maybe you need to leave for the whole day or even a week. Your portfolio will be there when you get back. You are not a day trader. You don't need to be clinging to every small swing the market makes. There is not a single day in the market where you have to be glued to your computer. There is not a single day in the market where you have to make a decision. You should never feel like you are racing.

One of the best parts of the Income Method is that it is a strategy that doesn't require constant care and attention. You can set up your portfolio, then walk away and live your life, checking on your portfolio when it is convenient for you. Let your life dictate when you check on your portfolio; don't let the market dictate your life. There is nothing about the strategy that demands an immediate reaction to anything. Just because the market is moving quickly does not mean you need to join the herd running off the cliff.

Know Your Strategy

Once you have taken the time to control your emotions, you are ready to implement your strategy in a principled manner. Of course, to do that, you have to know what your strategy is. By breaking your strategy into its fundamental parts, you can then logically work through any investment decision. This is how elite professionals in any field develop their abilities. They focus on each individual step, making sure they get it as close to perfection as possible, before adding speed.

Going back to the fundamentals, the Income Method strategy is:

- Construct a portfolio of income-producing investments with an average current yield of 8-10%.

- Include an allocation of 40% to fixed-income investments like preferred equity, bonds, and fixed-income closed-end funds, or CEFs.

- Diversify your individual holdings, targeting 2-3% or less in any one investment.

- As needed, withdraw up to 75% of the income your portfolio produces. Reinvest the remaining 25%+.

- Focus your investment decisions on increasing your income and income quality.

When you wake up to a market that is all red or all green, and you become tempted to dive in because everyone around you is trading, run through your checklist.

1. Is Your Portfolio Yielding 8-10%?

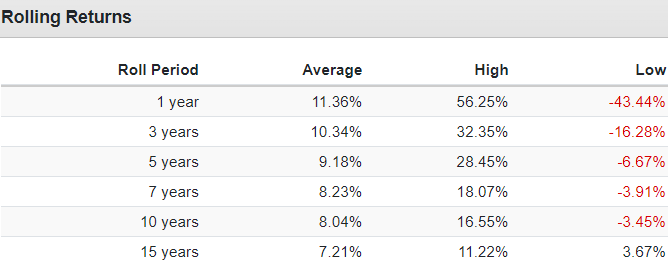

I use an 8-10% yield as my target because, in my experience, that is a target range that can be achieved in most economic conditions without taking on too much risk. It isn't a coincidence that the 8-10% target correlates strongly with what we can expect the long-term total return of the S&P 500 (SP500) to achieve. Here are the average rolling returns for SPY since 1993: Source .

{kind=link}

Note that SPDR® S&P 500 ETF Trust (SPY) has had some huge 1-year swings. Up 56%+ in a single year, and down 43%+. Yet, as the length of time included in the rolling period increases, both the high and low swings trend toward the middle. History tells us that 8-10% is a reasonable long-term target for stock market returns, even as you experience much more dramatic swings over short periods.

By targeting 8-10% yields, I am essentially saying I want substantially all of my returns from the market to come in the form of dividends. Growth of the big number in my portfolio will primarily be driven by my choice to reinvest dividends.

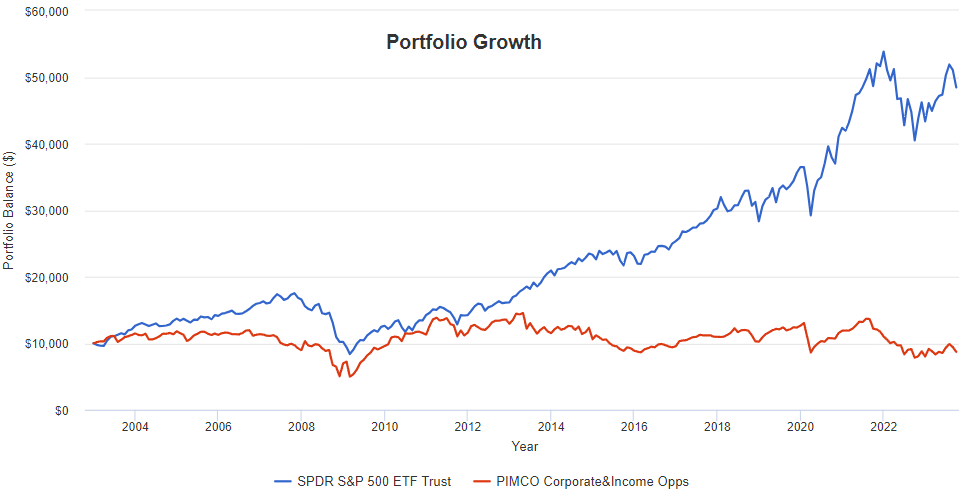

Consider one of my favorite CEFs, PIMCO Corporate & Income Opportunity Fund ( PTY ); since 2003, its price has been very flat compared to SPY. Source .

{kind=link}

Yet, when we include the dividends, PTY has dramatically outperformed:

{kind=link}

The reason is that substantially all of PTY's return over the past 20+ years has come from dividends. Many investors freak out when PTY's price moves 20%+ – I don't, because I understand that somewhere around 90%-110% of my total return from PTY is going to come from dividends. Why would I worry about the price swings when that will account for less than 10% of my total return over the long run?

With an investment like PTY, I have a choice with each dividend to take it out and spend it however I wish or reinvest a portion of it. Obviously, the more I reinvest, the more shares of PTY I will own, and the more that big number will grow. I get to choose with each dividend payment what is important to me – having income I can spend or growing my investments. I like having control of that decision.

This is why I choose a strategy where most of my gains come as dividends, maximizing my current income and putting the power to decide when and how aggressively to reinvest in my hands.

So, when considering a trade, start with your bottom line. What is your yield goal, and is your portfolio meeting it? If your portfolio is yielding less than your target, consider options for increasing it. If your portfolio is yielding more than your target, consider options that might decrease it. Why would you want to consider decreasing your portfolio yield? If your portfolio is yielding more than your target, odds are that many dividend-paying stocks are on sale. When yields are high throughout the market, it is a great opportunity to look to diversify into stocks that typically wouldn't fit your target. When you have an opportunity to diversify without sacrificing your ultimate goal, you should often take it.

2. Do You Have a Healthy Allocation to Fixed Income?

If you have been a regular reader of my work, you know that I like to have a healthy allocation to fixed income. Which for me, is primarily through preferred equity and bonds. The reason for this is simple: I prioritize income in my portfolio, and one feature of fixed income is that the income it produces is predictable. When the investment is first offered, you know how much it is supposed to pay and when. Whereas with common equity, management can cut the dividend whenever they want for whatever reasons they want. During times of economic stress, there is an increased risk of management teams deciding to retain more cash and reduce dividends. During such periods, fixed-income investments provide great reliable income. The deterioration that has to happen before a preferred dividend is suspended or a bond goes into default is much greater.

When the whole market is red, check your fixed-income allocation. Do you want more? If you do, it might be a great time to look at your options. While the income is fixed, the price is not. Often, you will see preferred equity or bonds sell off in sympathy with the common shares, even when the risk has not materially increased.

These investments are great options when fear is running the market, as they are ones that you can hold comfortably if the fear spreads and becomes an all-out panic.

3. How Is Your Individual Diversification?

By maintaining relatively small position sizes, you reduce both the financial and psychological impact of one particular holding collapsing. When there is a lot of red in the market, be aware of which positions you have that you are underweight on and which you are overweight. All things being equal, you should favor buying more shares in positions that you have less than 1% exposure to, while inclined to avoid adding more to those that make up 3%+ of your portfolio.

Some investors like to rebalance to keep all positions roughly equal. This can be a good strategy, but for those who are reinvesting a large portion of dividends, a similar result can be achieved by focusing your buys on the positions that are smallest. We discuss reallocation strategies in more depth here .

However, keep in mind that you shouldn't buy a position only because you are underweight. Continue to consider your overall outlook on the investment and the risk of the investment. If you are underweight because you are less confident than you are in other investments or because it fell more than others and you want to wait for more information before committing more, by all means, keep the position size small.

4. Check Your Reinvestment Resources

I recommend planning on withdrawing no more than 75% of the income your portfolio produces. The reason for this is two-fold. First, it provides income that you can reinvest on a routine basis, which will help grow the balance of your portfolio and your income. Second, it will provide you with a cushion in the event there are dividend cuts. When you are retired, income from your portfolio will make up a substantial portion of your income. Having a cushion built into your plan ensures that your personal budget is not negatively impacted by what happens in the market.

When the market is red, check your dividend tracker to see how much income you have coming in and when. I know some people like to have a little bit of a reserve built up for the purpose of investing. Personally, I prefer to remain 100% invested most of the time. I reinvest each month as my income comes in.

Note that I am discussing dollars already earmarked for reinvestment, not an emergency fund that you should have in place for your personal budget. No matter how tempting the market gets, you should never tap your personal emergency budget for investing . Keep your personal budget separate. The market can always go down more, prices will fall more than you believe is possible and what appears to be the safest "no-brainer" investment of all time, might turn out to be the biggest disaster of all time. Investing inherently carries numerous risks and nobody is going to identify all of them. That is why we diversify.

Now, maybe you have some extra-curriculars built into your budget that you are okay reducing when the market is low. I'll leave whether you want to adjust your lifestyle to market conditions up to you. It is always a tradeoff. The more you reinvest today, the more money you will have in the future. If you can withdraw only 50% of your income and reinvest 50%, your future income will grow faster than withdrawing 75%. Only you and your spouse can do the cost-benefit analysis of reducing your personal budget for future gains or enjoying as much as you can today.

From an investment perspective, be aware of how much you have coming in, and plan the amount you are willing to reinvest. When the market is red, avoid the urge to "back up the truck" and invest every penny you have; instead, consider how much you will have to invest over the next month and plan out a series of small buys. Prices that are down today could easily fall more tomorrow. By averaging in with numerous small buys, you ensure you are getting a good average price, while also giving yourself an opportunity to gain more information to reinforce your decision to buy a particular investment or to change your mind.

We discussed methods for buying into new positions here , and these strategies also apply to adding to or exiting established positions.

5. Focus on Your Income

As the name suggests, "The Income Method" is an investment strategy that is centered on the income that a portfolio is producing. The goal of the Income Method is to produce a stream of recurring income that grows over time.

So, many investment decisions aren't as difficult as they initially appear. When considering a buy, sell, or swap, ask yourself: "What does this mean for my income?" Will the trade:

- Increase the amount of your income

- Increase the safety of your income

- Grow your income in the future

- Bring you closer to your overall portfolio goals like target yield, target asset diversification (common equity vs fixed income), and/or individual holding diversification.

The ideal transaction is one that achieves all four of these, but every stock transaction should achieve at least two of these. It is likely that sometimes you are giving a little on the amount of your income, in order to increase the safety or maybe to have a holding that has better prospects for dividend growth. Whether that decision makes sense should be viewed through your overall goals. The more goals a transaction is achieving, the more you should be willing to do it. If a buy or sell isn't achieving any of your goals, don't do it.

Often, we are considering a buy between several potential investments. Go through your goals and compare which potential investments fit these goals the best. It might not be the stock that is the "cheapest" in the market right now.

Conclusion

Slow is smooth, smooth is fast. The bottom line is that you shouldn't base your investment decisions on a knee-jerk reaction to market price movements. Don't let yourself be drawn into the hectic rat race. Slow down, step back, and think about your overall portfolio goals. Take the time to go through the fundamentals of your strategy and how a particular investment fits into your overall portfolio. Initially, you might find this process takes time. Yet the more you do it, the more instinctive it will become, and you will find that you can do it quickly.

Do not panic, do not hurry. A dropping market is not a threat; it is an opportunity to invest capital at higher yields and grow our income even faster. Avoid the desire to dive in headfirst, running the risk of becoming overallocated to stocks that are very cheap. When you are overwhelmed by the opportunities in the market or feeling stressed when everything is red, revisit the fundamentals of your strategy. What are you trying to achieve? What guidelines are you staying within to protect your portfolio? How do the buys/sells you are considering impact your goals?

Today, I've discussed how to do this within the framework of the Income Method, but the overall principles can be applied to any investment style. Your investment decisions should never be random, and they should never be driven by your emotions. Slow down, think through your decisions, and make decisions that bring you closer to your overall goals. When you do that, you will be surprised at how quickly you can achieve your goals. Whether the market is red or green, you can keep your income growing one dividend at a time!

For further details see:

Don't Panic! Growing Your Income In A Volatile Market