DCI - Donaldson: An Interesting Segment At The Right Value But A 'Hold' Here

2023-12-05 07:52:51 ET

Summary

- Donaldson is a multinational filtration company with well-diversified sales mix and strong overall safety.

- The company has above-average profitability and strong fundamentals in its peer comparison.

- Donaldson is focused on long-term trends in technology and offers potential double-digit growth and EPS growth forecast.

Dear readers/followers,

In this article, I'll be looking at Donaldson ( DCI ). While I've been looking at this business before, I haven't been covering it in an official capacity until now. I like covering the industrial sector, and I like covering companies with specific and interesting verticals. In this case, we're talking about a filtration company.

We'll be looking at what Donaldson can offer investors in terms of long-term and short-term upside. It's a tricky macro to invest in companies like this, because of their relatively limited yield (less than 2% in those cases), and their relatively low growth. However, on the flip side, these companies tend to have very good levels of overall safety.

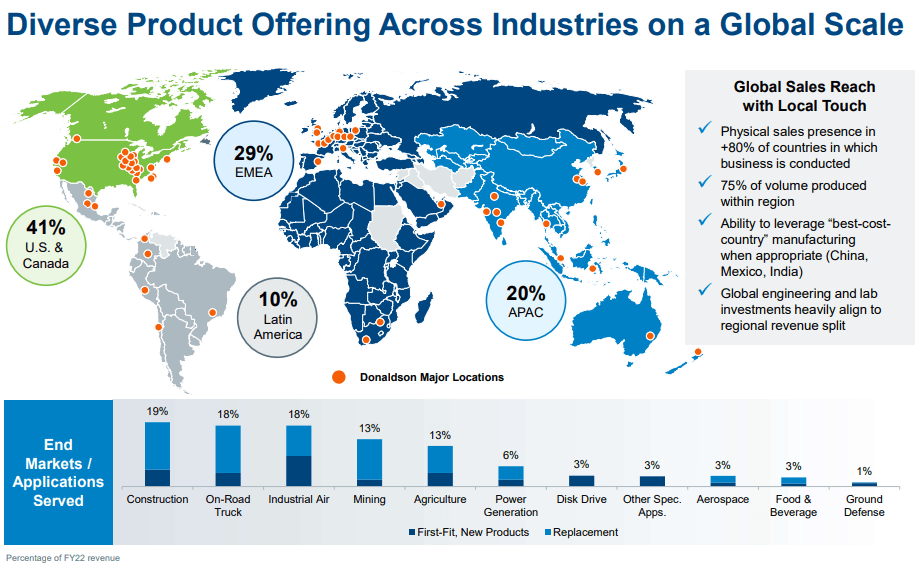

This is a multinational company, meaning it operates not only in the US but has significant operations in nations like Belgium, Mexico, China, The UK, the Czech Republic, Malaysia, Thailand, the US, South Africa, and many other nations.

Unlike many other companies, this one has a very well-diversified sales mix with around 40-50% of company net revenues coming from geographies other than North America.

Let's look at what Donaldson can offer to investors, and whether we can consider the company a "BUY" here.

Donaldson - A decent upside at the right valuation, but more growth than income

So, Donaldson is a company active in the R&D, manufacturing, and selling of filtration solutions, specifically air filtration. The company is one of the most significant companies worldwide when it comes to this.

I say this because the company, in terms of profitability and fundamentals in its peer comparison, is one of the best businesses out there. It doesn't really matter if you look at Gross margins, net margins, operating margins or various return metrics, this company is in the 80th-90th percentile in the industrial product segment.

When it comes to pure fundamentals, the company has an overall average debt to equity, but good leverage to EBITDA multiples, and an interest coverage multiple of 24.15x, making it well above the overall average here.

I report these things to make it clear to you that this company is in fact a qualitative business , when by quality you're speaking of these sorts of fundamental KPIs.

The company, if we want to look at it from a business model perspective, has an above-average quality business model when looking at the double-digit net margin the company is able to squeeze from its sales revenue.

{kind=link}

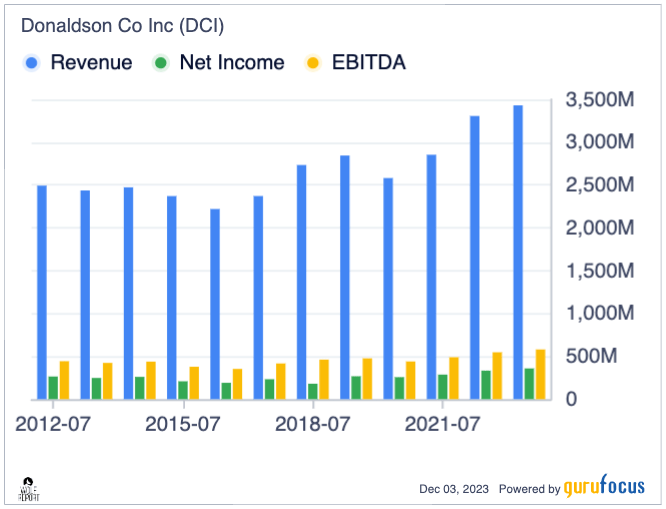

While the company's ROIC isn't as high as it was around 10 years ago, it's still well above where many other industrials manage in this macro. And while the company's revenues and net earnings are far from perfect as such, they're still very good.

{kind=link}

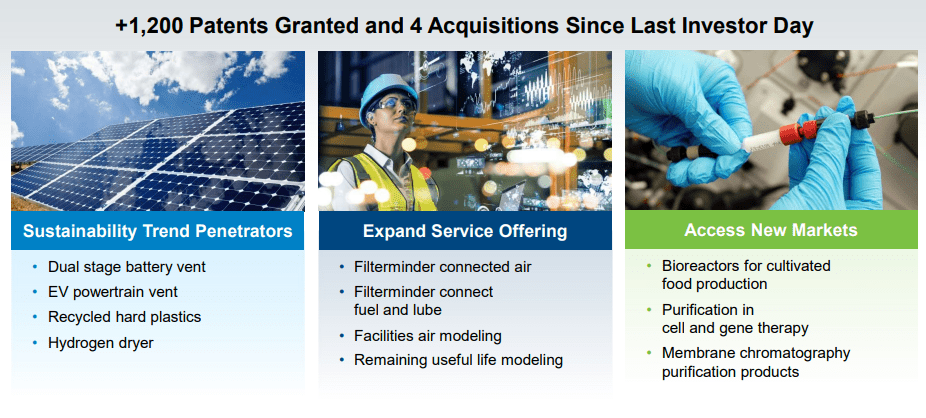

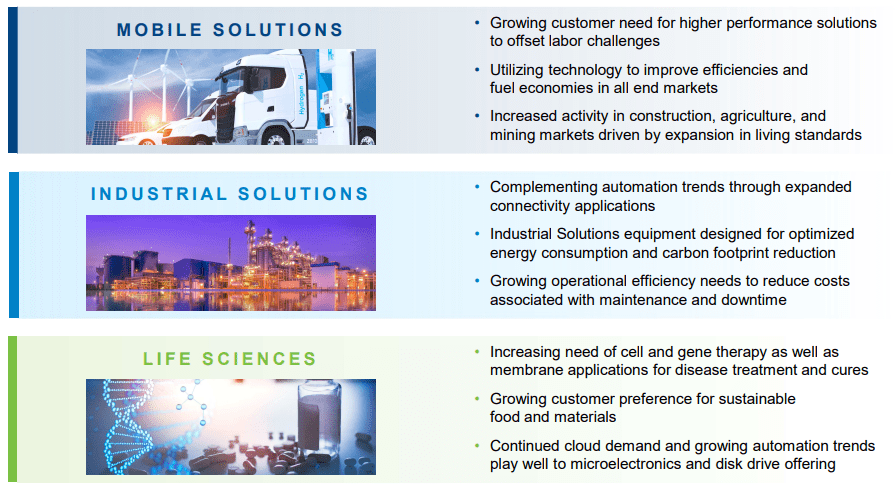

Essentially, this company is a global leader in solving complex problems in filtration. It's also, due to its operations, part of the transition to alternative energy/EV as well as a focus on the life science market. The company is over 100 years old, employs over 14,000 people, with representation at over 140+ locations with over 2,700 active patents around the world. The company also boasts a near-$8B market cap and has managed a 13% long-term CAGR for the company dividend, which is of course very solid.

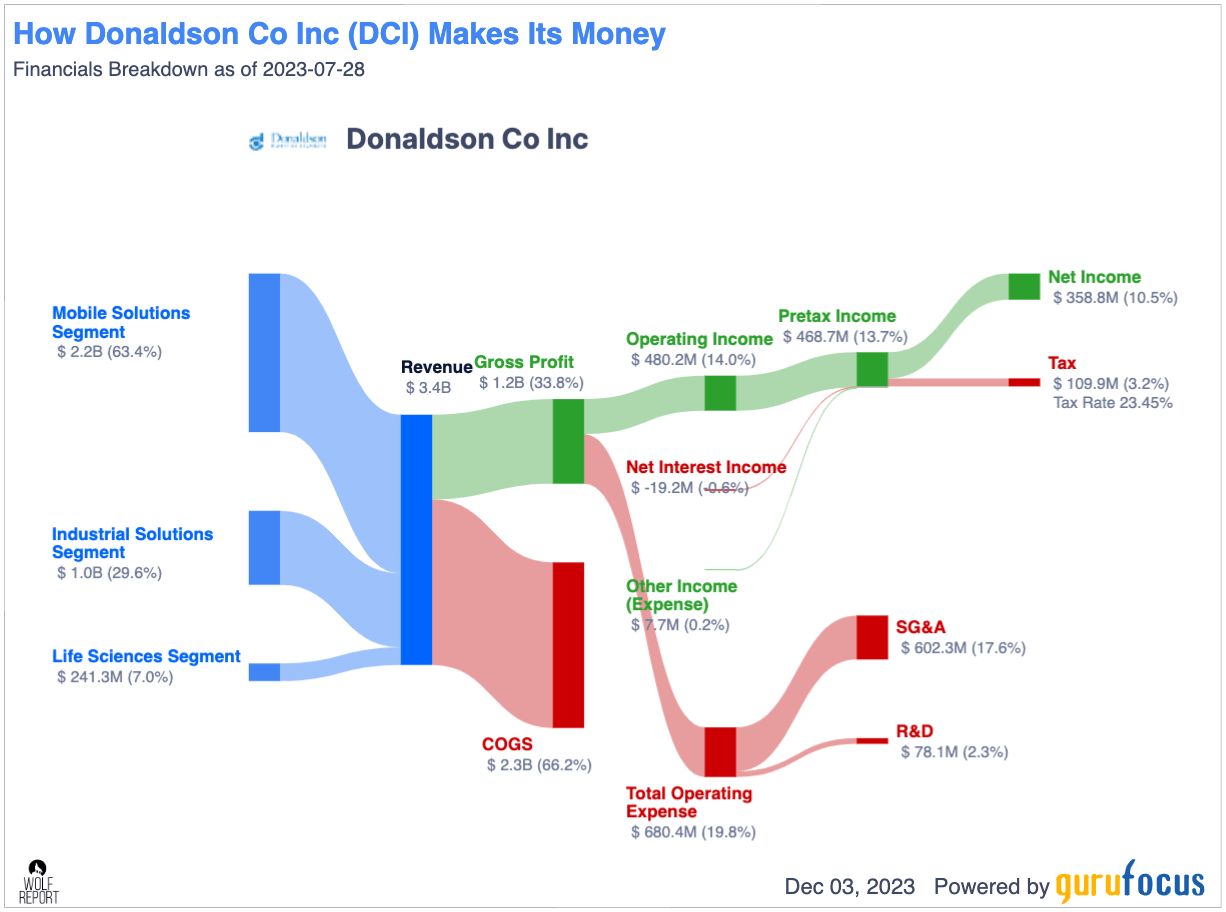

In terms of mix, over 64% of the company's sales are from mobile solutions, with only 8% from the budding life science segment - and most of the company's revenue is replacement revenue , meaning recurring customers. The company's earnings, as you can see above, are not perfectly in a positive overall trajectory, but coupled with the aforementioned geographical diversification, there's a lot to be said for the safety of the company. If we couple this with the company's attractive and conservative end markets, then we can see why this is an attractive business.

{kind=link}

The company is recently through an extensive reorganization started in 2015, when Donaldson acquired new assets to strengthen its engine filtration sensor offering and expand its international presence. This has culminated in a 2020-2022 16% EPS CAGR on an adjusted basis, where the company has significantly increased its serviceable addressable market area and has generated 2022 returns of $2.68 as of the latest investor presentation, and $3.04 on an adjusted basis for the 2023A, given that the company recently presented 1Q24.

The degree of expansion the company has seen since the last investor day can be expressed through 4 acquisitions as well as a large number of new patents.

{kind=link}

The life science segment is expected to generate significant growth on a forward basis. The company's target is for this segment to be a 33% split in in the future (Source: Donaldson IR). Its new segment split, with mobile/industrial/life science is as follows, with the following growth expectations.

{kind=link}

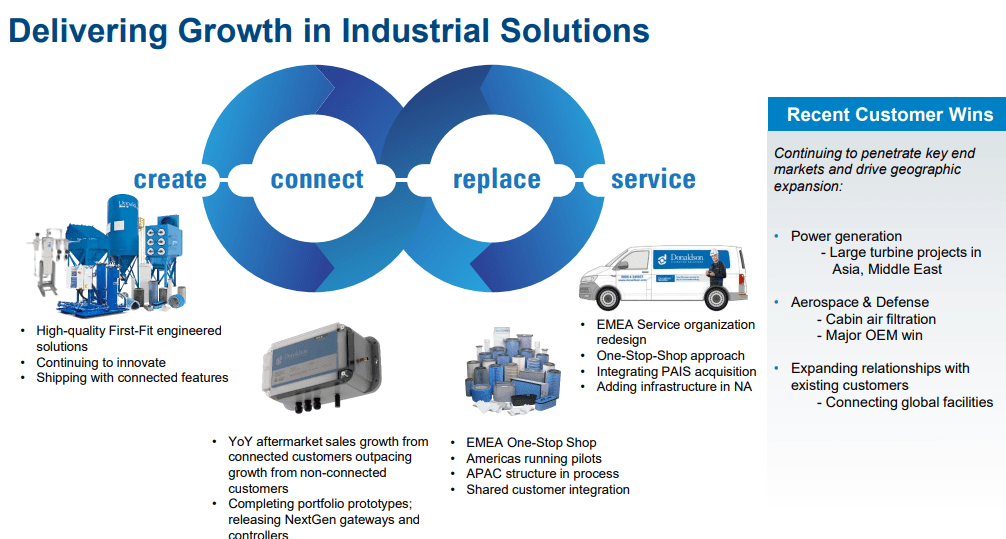

1Q24 is the latest set of results we have to consider here. The results for this quarter were good - delivering a decade-high record in gross margin with robust sales growth in industrial solutions while managing to execute on strategic priorities and efficiencies. The company's dividends aren't much worth mentioning - less than 2%, but a total of $84 in combined dividends and share buybacks were executed.

Sales were actually down year-over-year, despite a 3% pricing benefit and flat EPS. However, gross margins were up 1.7%, and FCF conversion was up to 125%. The company also reaffirmed the positive fiscal guidance forecast, now expecting 3-7% with an EPS growth enabling a high-end EPS range of $3.3, as well as delivering increasing operating margins with a higher end rate of 15.3% possible here.

Segment-specific trends were mixed here. Sales in mobile solutions were down 3%, whereas industrial solutions were up - with growth from specific sub-segments.

{kind=link}

Life sciences meanwhile, reported declining results, mostly driven by ongoing softness in the disk drive market with weakness in both APAC and NA, but strength in EU/LATAM. However, despite recent M&As and overall investments, the company's fundamentals remain very solid. The company is still at less than 1x net debt/EBITDA, with a total debt amount of $434M on a net basis.

Investing in Donaldson means you're investing in the long-term trends in technology, including current sustainability trends. It's an investment into generally favorable megatrends. The company is focusing on higher-margin investment opportunities driving profitable growth and good shareholder value - and the company considers itself well-positioned to either achieve or exceed its long-term financial targets.

Overall, Donaldson is a favorable investment. Long-term investors have been able to generate a total RoR of almost 490% in 20 years, averaging 9%. The problem is that this is based, a lot of it, on a premium to 22-23x P/E - and at times, the company trades well below this for extended periods of time.

Despite a lack of credit rating, due to strong fundamentals, I view the company as investable at an undervaluation to the company's premium.

There are other risks worth considering as well.

Risk & Upside

Donaldson is a play on long-term trends, but these trends do sometimes come with volatility - and this company certainly comes with share price volatility. Its lows go to a P/E of 11x, up all the way up to a P/E of almost 30x. The risk of sub-par performance is, at least historically, likely if you invest close to the company's premium unless the company's growth trajectories are held.

Beyond that, any company that goes through the sort of strategic reprioritization and new operations that Donaldson is comes with a potential degree of operational risks.

Upside-wise, the arguments for the company are solid. Based on its results and growth expectations, even just at conservative estimates, there is a double-digit growth potential and EPS growth forecast here (Source: S&P Global). If those potentials are realized, then you could see significant rates of return at the right share price here.

Let me show you what I mean by this upside.

Valuation

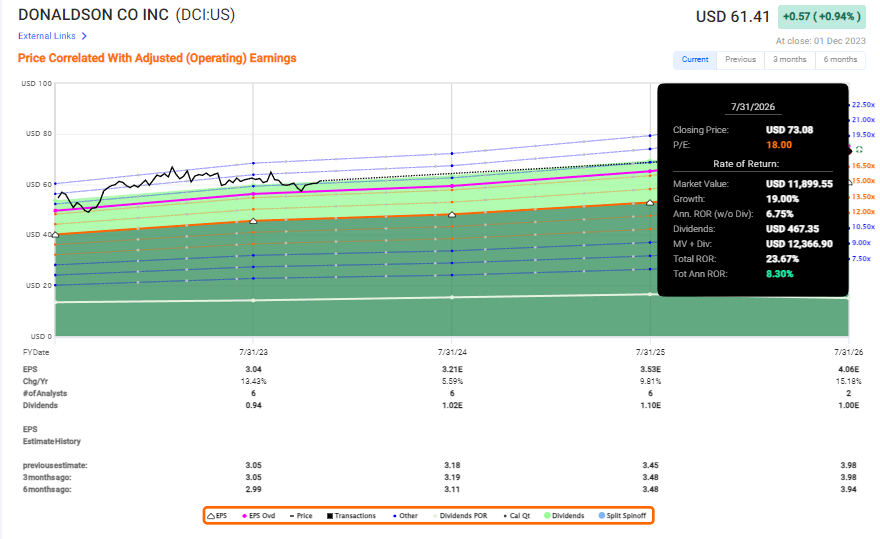

There are two ways to view Donaldson here. Either you estimate the company at 15-18x P/E, at which point the upside is clearly sub-par. Even at a 10.7% EPS growth rate, the annualized RoR due to the low yield and this company's trading history implies an RoR of less than 25% in 3 years until 2026E in accordance with this.

{kind=link}

You should also know that analysts do not view Donaldson all that favorably. By that, I mean that the company's current $61/share price, despite the company not being all that expensive compared to its historical premium, only 1 out of 5 analysts are currently at a "BUY" (Source: S&P Global).

This implies that there is some doubt about the company's appeal at this price. However, if you choose to forecast the company at around 22x P/E, that upside goes from 8% annually to 18%, or a total upside of 55.56% in 3 years. So, under those estimates and scenarios, this company does have an upside. And that 22x P/E, that's confirmed not only for a 5-year average but for the 20-year average as well.

So in the end, it's all about what value you want to assign to Donaldson both on a current and forward basis. Myself, I would go along with the other analysts here. I'd say that I'm not looking to assign premiums to almost any company - and a somewhat cyclical industrial like Donaldson, despite some resilience in its segments, is not one of them.

I'll forecast Donaldson to have an upside to an 18x P/E, which implies that we'd need a share price of around $55/share to really get a solid upside going here. At $55/share, we're looking at 13-16% annually depending on how much the company does end up growing here.

That also means that currently, Donaldson stock is a "HOLD" with the following theses applicable here.

Thesis

- Donaldson is a fundamentally attractive industrial company in the business of filtration - an attractive long-term industry with good upside both for the alternative energy move that's ongoing at this time.

- The company does not have a great yield, nor a significant outperformance on record if you choose to invest at over 18-19x P/E - but if you target an attractive entry point here, you're able to get a 15%+ annualized upside.

- I would put this company at a PT, at most, of $55/share and no higher. Given the current company share price, I'd be happy waiting here for a better entry point, and I believe investors are better off doing the same, depending on their situation.

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

Donaldson: An Interesting Segment At The Right Value, But A 'Hold' Here