DCI - Donaldson Company: Attractively Valued With Good Growth Prospects

2023-12-03 23:05:27 ET

Summary

- Donaldson Company's revenue growth is expected to benefit from easier year-over-year comparisons, good execution, and market share gains.

- The company's gross margin should continue to see gains from pricing action, cost deflation, and increased plant productivity.

- Despite recent sales declines in certain segments, DCI's revenue outlook is positive, with expectations of sequential and year-over-year improvement in sales in the coming quarters.

Investment Thesis

Donaldson Company, Inc. ( DCI ) stock has traded flattish since my previous coverage in September. The company has reported mixed Q1FY24 results since then with its flattish sales missing estimates while EPS coming better than estimates. I continue to see good growth potential for the company. In the coming quarters, Donaldson's revenue growth is well-positioned to benefit from easier year-over-year comparisons, good end-market demand and market share gains in the Industrial segment, aftermarket inventory destocking completing in the Mobile Solutions segment, and recovery in the Disk Drive market in the Life Sciences segment. Apart from organic growth, the company has a healthy balance sheet and is well-placed to do bolt-on M&As.

On the margin front, the company should continue to see gains from pricing actions, cost deflation, operating leverage, and increased plant productivity. The company's Life Sciences segment is currently posting negative operating margins as it is investing in scaling its recent acquisitions but management expects sequential improvement as the year progresses. This should also help overall operating margins in the coming quarters. The valuation is attractive when compared to its 5-year historical averages. This, combined with good growth prospects makes DCI stock a buy.

Revenue Analysis and Outlook

Post-pandemic, DCI's sales growth benefited from strong, broad-based end-market demand and higher pricing. However, in recent quarters, the company's sales growth was negatively impacted by the improvement in global supply chain conditions which drove its OEM customers to normalize their inventory, leading to decreased aftermarket sales. In addition, the weakness in the disk drive market also negatively impacted the sales growth.

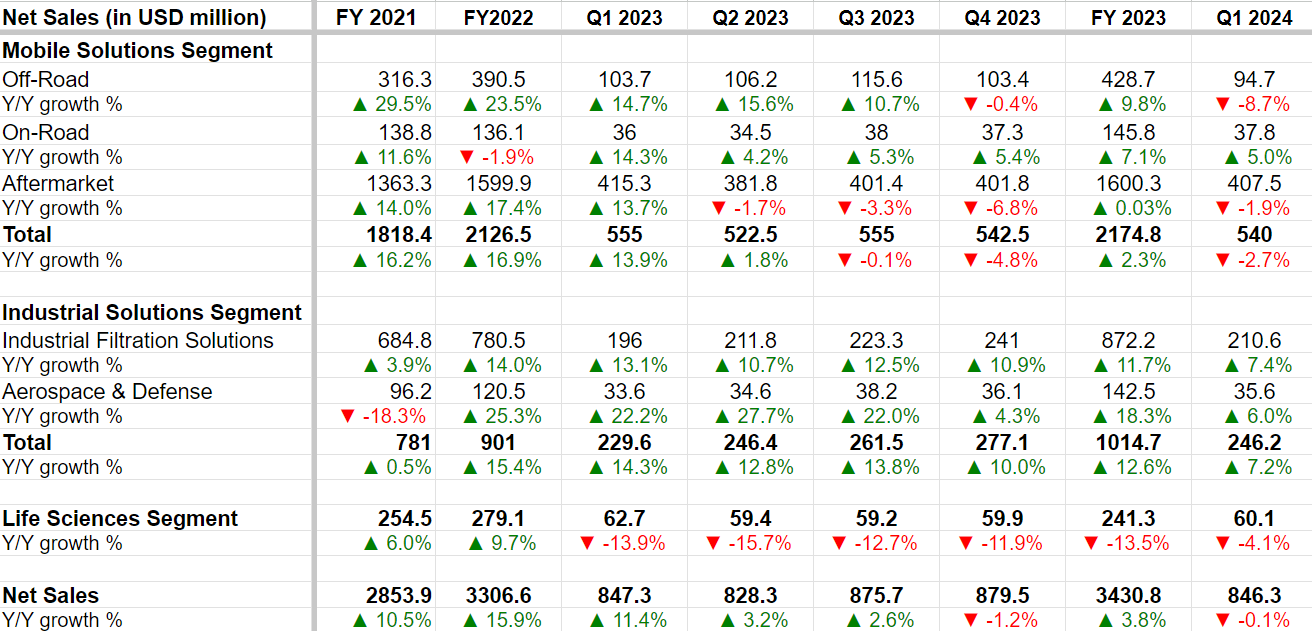

In the first quarter of 2024, the company's Mobile Solutions segment sales declined 2.7% Y/Y due to a volume decline in its Off-Road and Aftermarket businesses, partially offset by a pricing benefit of 3%. Weakening global end-market conditions, particularly in China and the agriculture markets in the Americas and India, led to an 8.7% Y/Y decline in Off-Road sales. Aftermarket sales decreased 1.9% Y/Y as the OEM customer destocking continued in response to normalizing global supply chain conditions. However, On-Road sales grew 5% Y/Y attributed to increased on-highway equipment production, especially in China.

In the Industrial Solutions segment, sales increased by 7.2% Y/Y driven by strong demand in most of its geographic regions and a 2% contribution from pricing. Strong dust collection and power generation sales drove a 7.4% Y/Y sales growth for the Industrial Filtration Solutions ((IFS)) business. Aerospace and Defense sales grew 6% Y/Y thanks to the continued strength in Defense business.

The Life Sciences segment continues to face headwinds from ongoing softness in Disk Drive market demand, which caused its sales to decline 4.1% Y/Y in the first quarter.

On a consolidated basis, net sales of $846.3 million were essentially flat Y/Y as lower volumes in the Mobile Solutions and Life Sciences segments were offset by volume growth in the Industrial Solutions segment and a 3% contribution from pricing.

DCI's Historical Revenue Growth (Company Data, GS Analytics Research)

{kind=link}

Looking forward, the company's revenue outlook is positive.

If we look at the company's quarterly sales growth trajectory in the last fiscal year, Q1 FY23 sales were up 11.4% Y/Y, and then they saw a leg down with 3.2% Y/Y growth, 2.6% Y/Y growth and 1.2% Y/Y decline in Q2, Q3, and Q4 of FY23 respectively. So, the revenue comparisons are becoming meaningfully easier from the current quarter onwards.

Segmentwise, the Mobile Solutions segment's aftermarket business, which accounts for ~75% of the segment's sales and was under pressure from inventory destocking, has now started seeing a stabilization in order patterns. This bodes well for the segment's sales which should see sequential as well as Y/Y improvement in the coming quarters.

The company's Industrial segment should continue to do well driven by end market strength as well as market share gains. In my last article , I explained how the company's connected offering with real-time information and data analytics about the state of the filters installed at the customer's location as well as an e-commerce application for replacement parts is helping it win market share. On its latest earnings call , management noted that aftermarket sales growth from connected customers in FY23 is outpacing that of non-connected industrial customers validating the customer-centric approach of this model which is helping them win share. The company launched its connected model in India, Thailand, and China last year and is still in the early phase of realizing the benefits of this model. I am expecting continued strength in the end markets and market share gains from connected solutions offering to drive growth in this segment.

In the Life Sciences segment, the weakness in the disk drive market has impacted the company's sales over the last few quarters. However, this market is likely near the bottom. Talking about this market on the Q1 earnings call, the Company's CEO Tod E. Carpenter said :

We are seeing early signs of a slow demand recovery and expect a sequential improvement in disk drive sales through fiscal 2024 as data center and cloud computing demand recovers."

So, a recovery in this market should help the segment's growth in the coming quarters. Life Science segment sales should also benefit from the company's focus on growing its bioprocessing and filtration offering for the alternative protein market where management is investing significant resources.

Overall, I expect a good acceleration in Y/Y revenue growth helped by easing comps, good execution and market share gains, and recovery in aftermarket and disk drive businesses. The company also has a healthy balance sheet with a net debt-to-EBITDA ratio of 0.7x at the end of the last quarter. So, I expect the company to remain active in the M&A area as well, and any bolt-on acquisition can add to overall growth.

Margin Analysis and Outlook

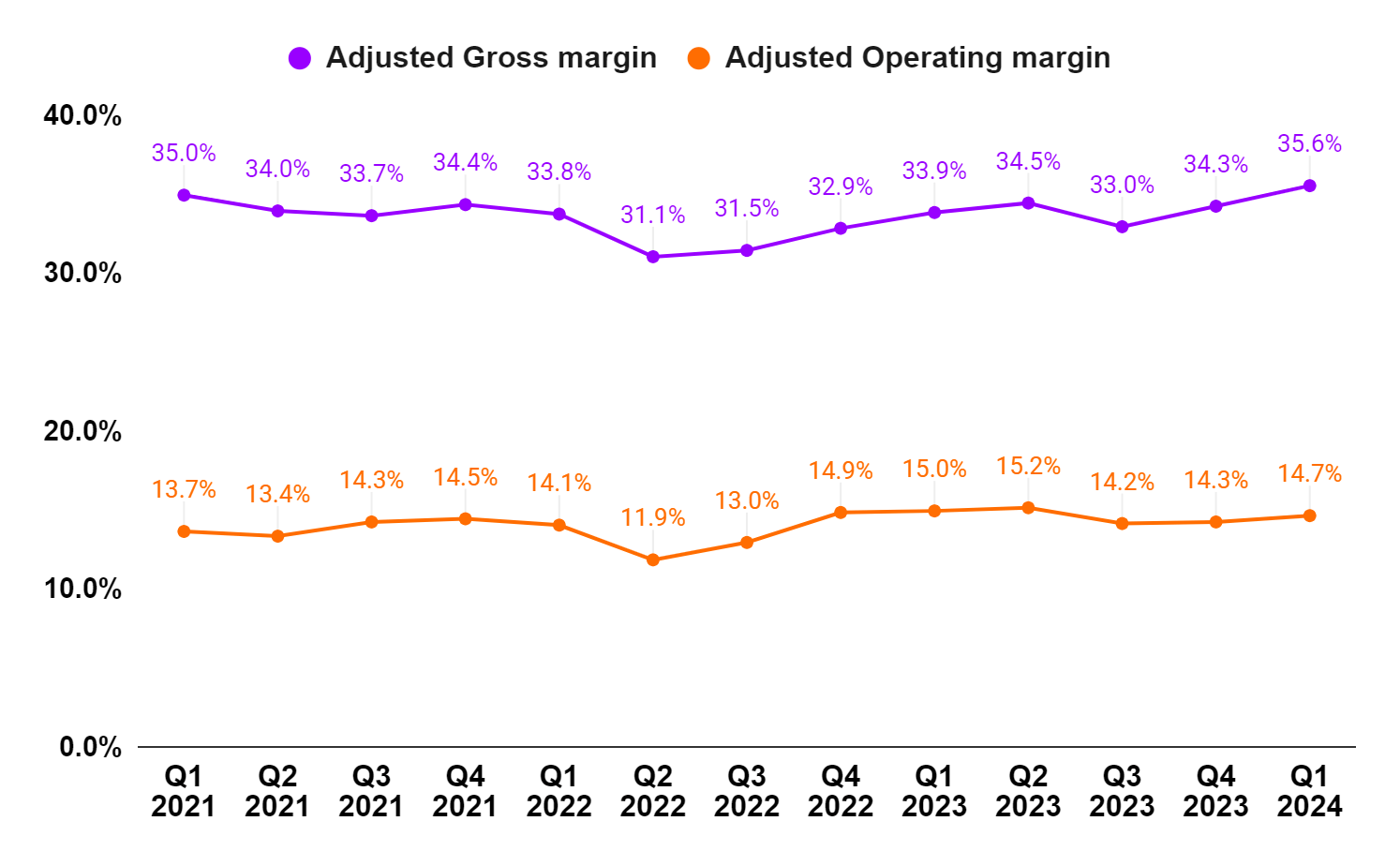

In Q1 2024, the company's adjusted gross margin saw a 170 bps Y/Y expansion to 35.6%, mainly driven by benefits from pricing, lower freight costs, strong plant productivity, and favorable material costs and mix. However, operating expenses as a percentage of sales increased by 100 bps Y/Y due to increased hiring and Life Sciences' acquisition-related expenses. The operating expense deleveraging more than offset the Y/Y gross margin improvement, resulting in the adjusted operating margin contraction of 30 bps Y/Y to 14.7%.

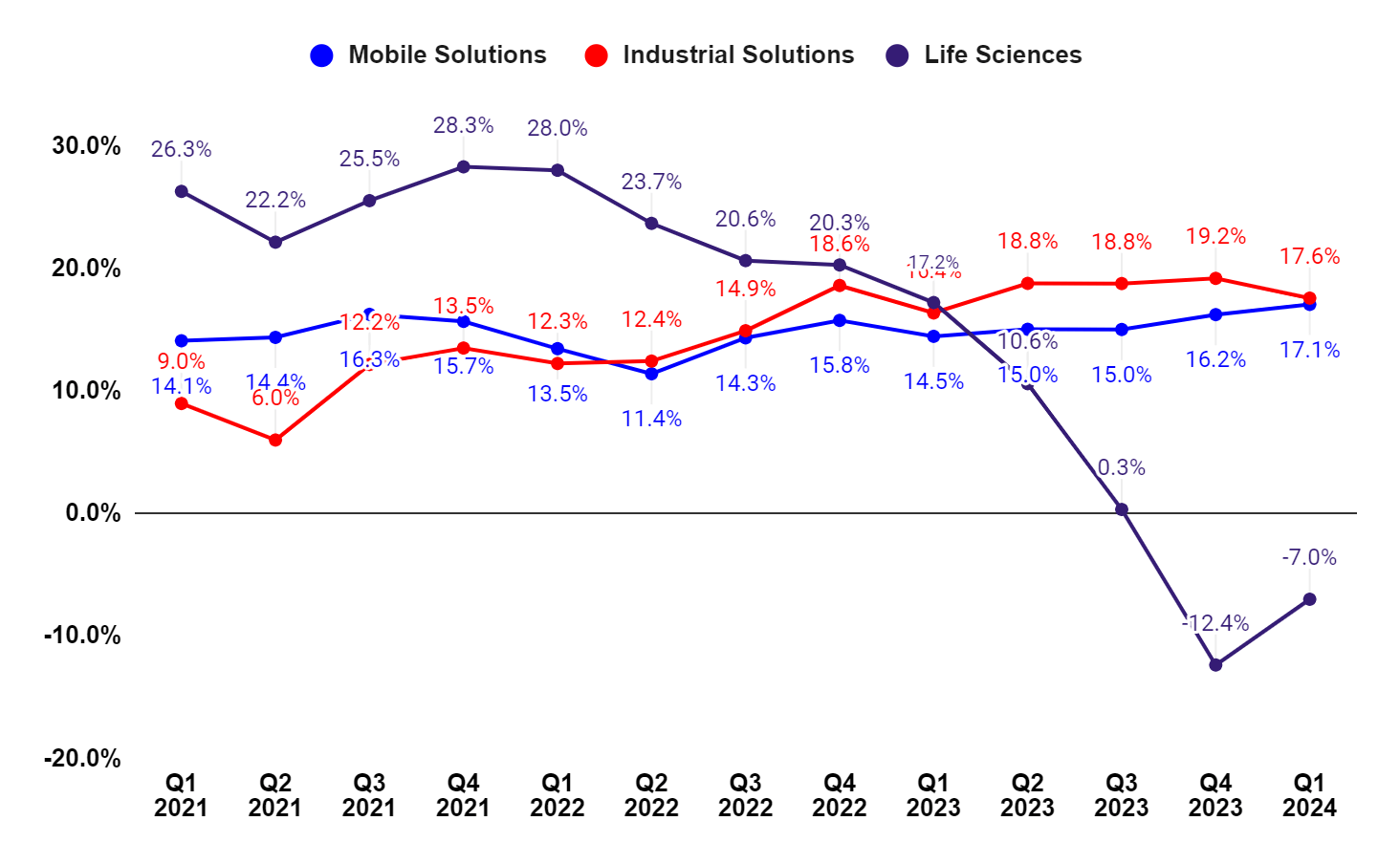

Segment-wise, the EBT or Pretax profit margin improved by 260 bps Y/Y and 120 bps Y/Y, respectively in the Mobile Solutions and Industrial Solutions segments. While Life Sciences' EBT margin declined Y/Y due to incremental investments in acquisitions and lower Disk Drive volumes.

DCI's Adjusted Gross margin and Adjusted operating margin (Company Data, GS Analytics Research) DCI's Segment-Wise EBT Margin (Company Data, GS Analytics Research)

{kind=link}

{kind=link}

Looking forward, I am optimistic about the company's margin growth prospects. The company's gross margin should continue to increase Y/Y benefiting from pricing improvement, cost deflation, and good plant performance as supply chain conditions improve. Seasonally, Q2 is usually lower because of holidays and we can see a sequential decline in Q2 FY24 as well but I won't be reading too much into it and Q3 FY24 and Q4 FY24 should be strong.

In terms of operating margin, the company has seen some headwinds as it is making incremental investments to scale recent life science acquisitions. Usually, life sciences EBT margins have been above the company average but have turned negative in recent quarters due to these investments. However, the good news is that they are sequentially improving with Q1 FY24 better than Q4 FY23 and management expects this sequential improvement to continue as the acquired businesses scale. For the full year, management expects the segment to post above breakeven margin indicating meaningful improvement ahead as the year progresses.

In addition, the company's operating margin should also benefit from volume leverage from sales growth acceleration in the coming quarters. So, I am optimistic about the company's margin growth prospects.

Valuation and Conclusion

DCI is currently trading at a 19.19x FY24 consensus EPS estimate of $3.20 and a 17.38x FY25 consensus EPS estimate of $3.53, which is at a discount versus the Company's 5-year average forward P/E of 22.28x.

The company has good growth prospects supported by easing Y/Y comps, good execution, and market share gains, recovery in aftermarket business in the Mobile Solutions segment and disk drive business in the Life Sciences Solutions segment, and future M&As. The margin growth prospects are also attractive with gross margin benefiting from pricing improvement, cost deflation, and increased plant productivity. In addition, a sequential improvement in Life Sciences segment profitability along with operating leverage from higher sales should benefit the company's operating margins in the coming quarters. Given the good growth prospects and attractive valuation, I continue to have a buy rating on the DCI's stock.

For further details see:

Donaldson Company: Attractively Valued With Good Growth Prospects