DCI - Donaldson Company: Fairly Valued After The Rise

Summary

- Donaldson Company has defied expectations, with sales, profits, and cash flows climbing in what is definitely a difficult environment.

- Shares of the business have soared in response to these developments, but this doesn't mean that further upside exists.

- At present, shares look fairly valued or within that range.

From time to time, every one of us misjudges an investment opportunity. Although the most painful result from this is downside when we were expecting upside, it's almost as painful when we see a company that we passed up significantly outperform the market and our own expectations. An example of the latter taking place over the past year can be seen by looking at Donaldson Company ( DCI ), a firm that produces and sells filtration systems and replacement parts associated with them. Driven by robust fundamental performance, both on the top line and bottom line, shares of the company have moved nicely higher after I rated it a ‘hold’ to reflect my view that shares should perform along the lines of the market. In retrospect, I ended up being too conservative on this name. With that in mind, I must risk again missing out on some upside. I say this because, while I was clearly wrong before, I do think DCI shares look more or less fairly valued at this moment and, as a result, I cannot rate the business any higher than a ‘hold’ right now.

Great performance lifted shares higher

In the middle of June of 2022, I performed a detailed analysis in order to figure out whether or not Donaldson Company made for an attractive investment prospect. In that article, I acknowledged that the business had done well to continue its growth in recent months. I also concluded that the future for the company and for long-term investors in it would likely be right. Leading up to that point, shares had declined and, as a result, were looking cheaper than they did previously. But I didn't think that they had fallen enough to justify attractive upside. This led me to keep the company at the ‘hold’ I had assigned it previously. Since then, the business has blown past any reasonable expectations I could have set for it. While the S&P 500 is up 9.4%, shares of Donaldson Company have seen upside of 37.5%.

{kind=link}

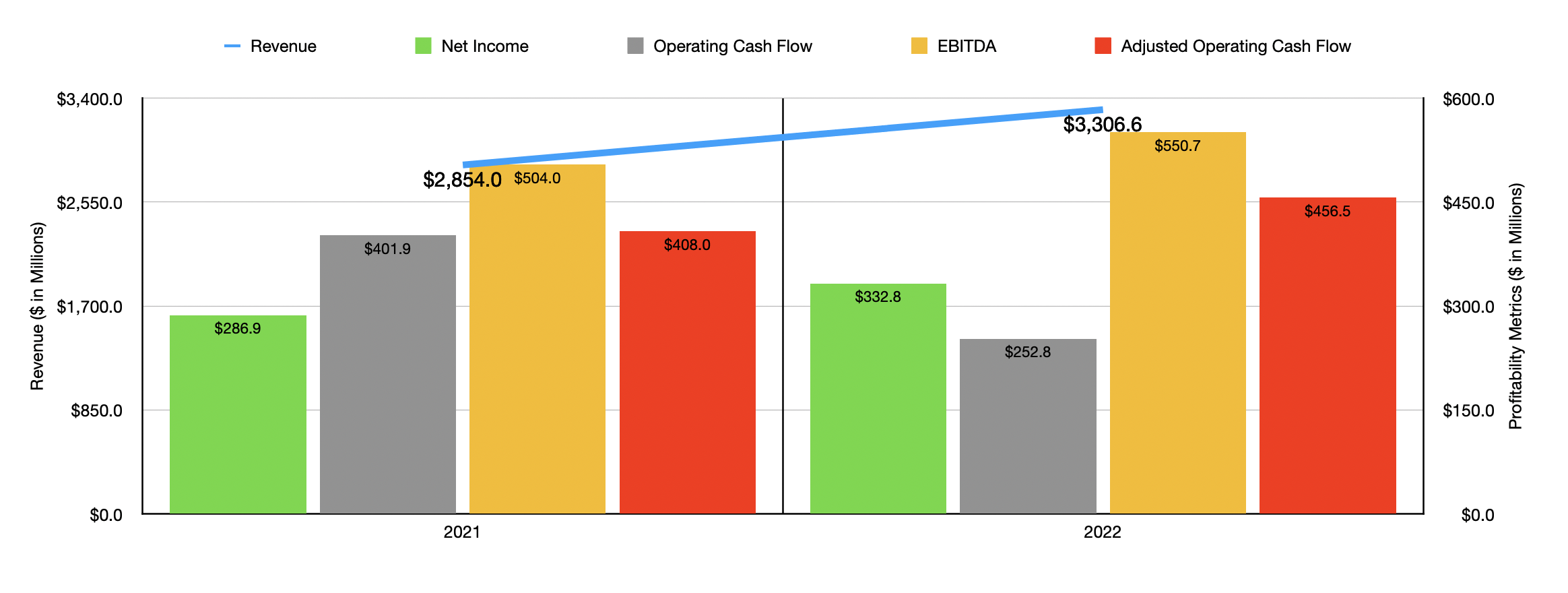

To understand why this return disparity exists, I think it would be instructive to look at how the company performed during its 2022 fiscal year . During that time, revenue came in at $3.31 billion. That's 15.9% higher than the $2.85 billion the company reported only one year earlier. Interestingly, revenue would have been even greater in 2022 had it not been for foreign currency fluctuations impacting sales to the tune of $87.1 million. The increase in revenue for the business reflected $345 million of additional sales associated with its Engine Products segment. This increase, totaling 17.6% year over year, was driven mostly by after-market revenue shooting up 17.6% because of higher pricing and continued high end-market demand. Off-road revenue made up a smaller portion of the sales increase, but ultimately shot up 23.7% year over year. This rise, according to the company, was thanks mostly to increased pricing, higher equipment production levels, and strong sales for exhaust and emissions products in the EMEA (Europe, Middle East, and Africa) regions. The other segment that the company has, called the Industrial Products segment, saw revenue pop 12%, with industrial filtration solutions leading the way, followed by robust demand for the company's gas turbine systems.

On the bottom line, the picture also improved. Net income of $332.8 million in 2022 beat out the $286.9 million reported only one year earlier. Operating cash flow managed to fall, dropping from $401.9 million to $252.8 million. But on an adjusted basis, it would have risen from $408 million to $456.5 million. Also on the rise was EBITDA. From 2021 to 2022, it shot up from $504 million to $550.7 million.

{kind=link}

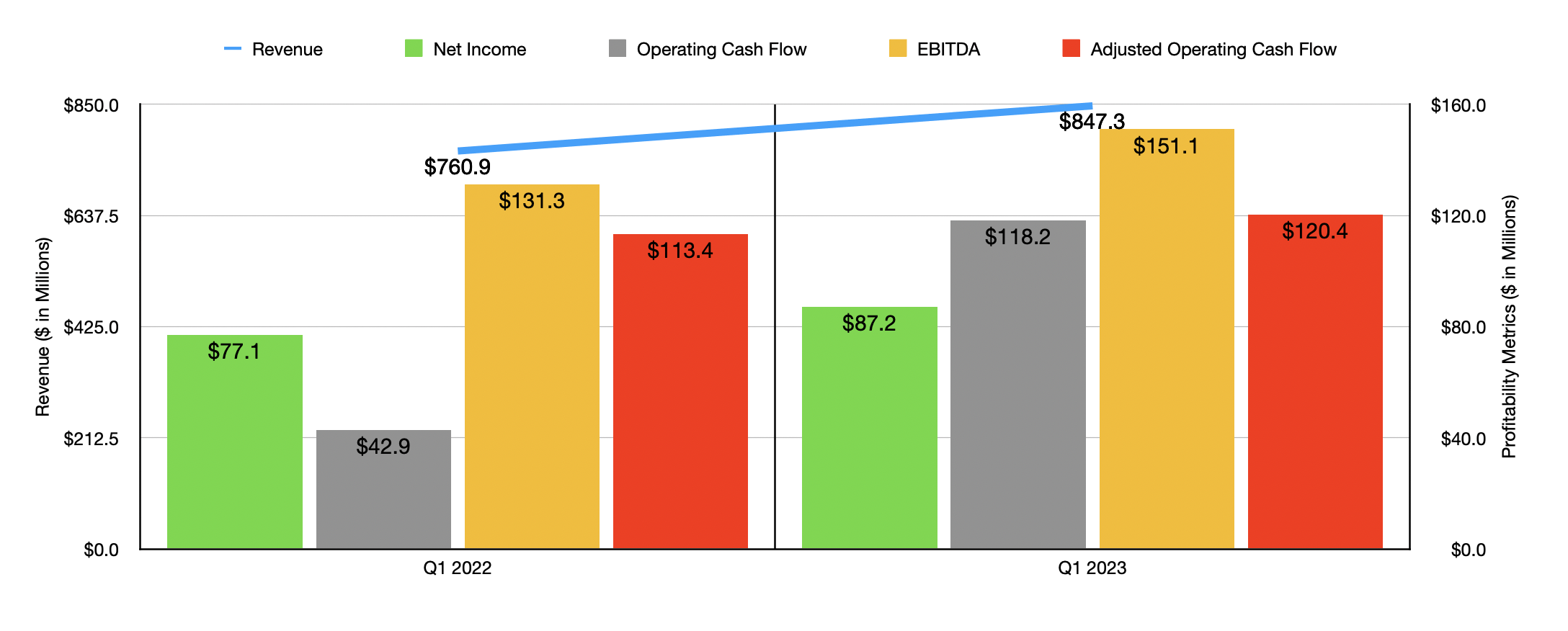

So far, management has also reported data covering the first quarter of the company's 2023 fiscal year. During that quarter, sales came in at $847.3 million. That's 11.4% higher than the $760.9 million reported only one year earlier. The lion’s share of this sales increase came from its Engine Products segment, with revenue shooting up 14.7% from $527.2 million to $604.5 million. This increase, management said, was driven largely by a 14.1% increase in revenue associated with its aftermarket sales and by a 15% increase in off-road sales. Interestingly, for the company as a whole, sales would have been higher had it not been for foreign currency fluctuations. Under the Engine Products segment, this impacted sales negatively to the tune of $39.1 million and, for the Industrial Products segment, to the tune of $19.7 million.

The bottom line for the company also improved during this time. Net income, as an example, shot up from $77.1 million to $87.2 million. Operating cash flow fared even better, skyrocketing from $42.9 million to $118.2 million. But if we adjust for changes in working capital, the increase would have been smaller from $113.4 million to $120.4 million. And finally, EBITDA for the business expanded from $131.3 million to $151.3 million. For those wondering, margins remained virtually the same across all its major cost categories. In the face of the kind of inflation we are dealing with, this should be considered a great development.

{kind=link}

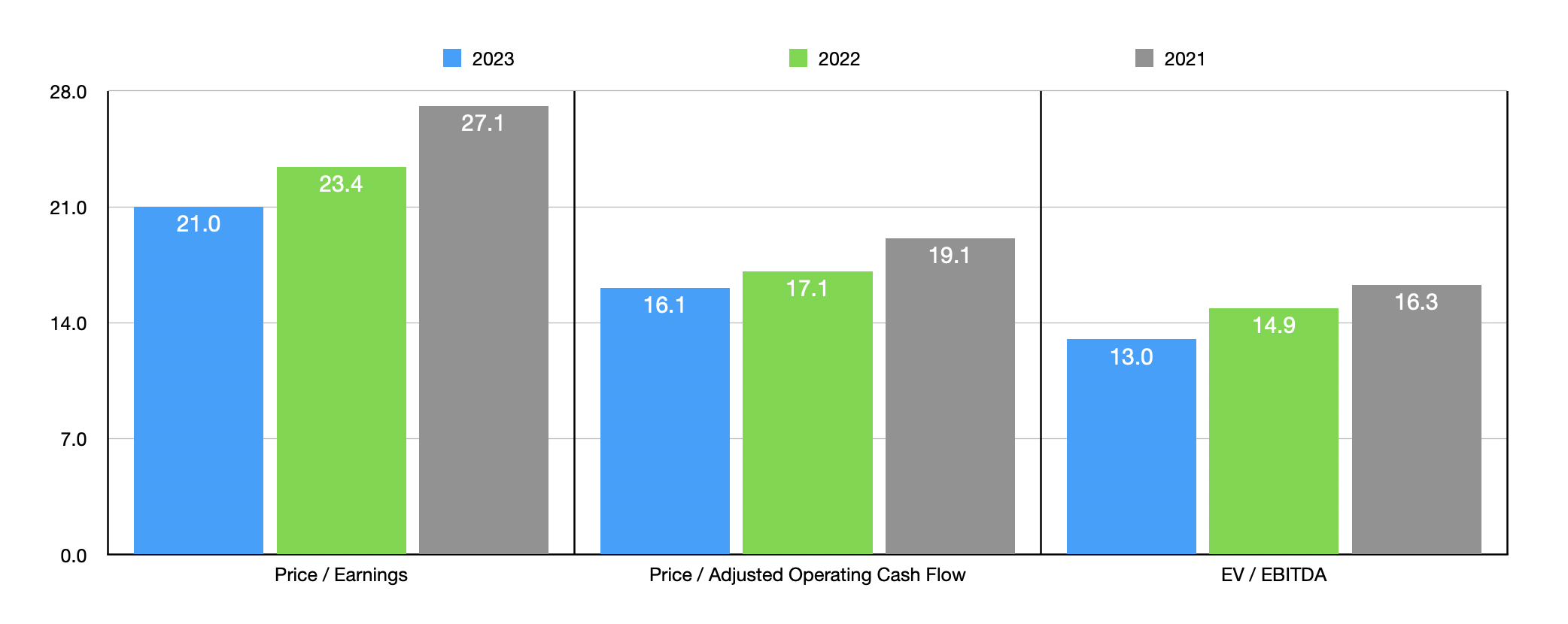

For the 2023 fiscal year in its entirety, management is expecting adjusted earnings per share of between $2.91 and $3.07. At the midpoint, that would translate to net income of $370.5 million. If we assume similar year-over-year increases for the other profitability metrics, we would get adjusted operating cash flow of $484.7 million and EBITDA of $633.7 million. Based on these figures, the company is trading at a forward price-to-earnings multiple of 21. The forward price to adjusted operating cash flow multiple should come in at 16.1. And the EV to EBITDA multiple should be 13. Using, instead, the data from 2022, these multiples would be 23.4, 17.1, and 14.9, respectively. For context, in the chart above, I also provided valuation multiples using data from 2021. As part of my analysis, I also compared the firm to five similar businesses. On a price-to-earnings basis, these companies ranged from a low of 6.4 to a high of 36.4. Using the EV to EBITDA approach, we get a range of between 3.8 and 22.3. In both cases, four of the five companies are cheaper than Donaldson Company. And finally, using the price to operating cash flow approach, the range would be from 5.8 to 20.5. In this case, three of the five firms are cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Donaldson Company |

| 23.4 |

| 17.1 |

| 14.9 |

| Mueller Industries ( MLI ) |

| 6.4 |

| 5.8 |

| 3.8 |

| Crane Holdings Co. ( CR ) |

| 16.8 |

| 15.0 |

| 10.0 |

| Parker-Hannifin ( PH ) |

| 36.4 |

| 18.3 |

| 22.3 |

| EnPro Industries ( NPO ) |

| 13.9 |

| 15.1 |

| 8.6 |

| Standex International ( SXI ) |

| 20.3 |

| 20.5 |

| 11.7 |

Takeaway

Fundamentally speaking, I am most certainly impressed with how Donaldson Company is doing. The business continues to grow both its top and bottom lines even though we are going through difficult economic circumstances. Looking back, I regret the rating that I assigned the company. After all, it's clear that I was too conservative in my assessment. Fast forward to today, however, and I risk making that same decision now. While I acknowledge that the company is a solid operator in the current environment, shares are right on the edge between a ‘buy’ and a ‘hold’. When faced with a situation like this, I often go with the more conservative assessment so as to err on the side of caution. And today is no exception.

For further details see:

Donaldson Company: Fairly Valued After The Rise