DCI - Donaldson Company: Overvalued Company With Slow Revenue Growth

2023-06-26 08:11:14 ET

Summary

- Donaldson Company's Q3 FY23 net sales increased by 2.6% compared to Q3 FY22, driven by growth in Off-Road, On-Road, and industrial solutions segments.

- DCI stock is currently overvalued, with a slow growth rate that doesn't justify its high valuation, leading to a hold rating.

- The company faces risks from disruptive technology and changes in industry market trends, which could negatively impact its operations and financial health.

Donaldson Company ( DCI ) manufactures filtration systems and replacement parts. They work in three segments, Industrial products, and Engine products. In the Industrial Products segment, they provide dust and mist collectors; gas and liquid filtration for food and industrial processes. In the Engine Products segment, they offer air filtration systems, indicators, and liquid filtration systems. DCI recently announced its Q3 FY23 results. I will review its Q3 FY23 results and talk about its growth potential in this report. I think its growth rate doesn't justify its high valuation. Hence I assign a hold rating on DCI.

Financial Analysis

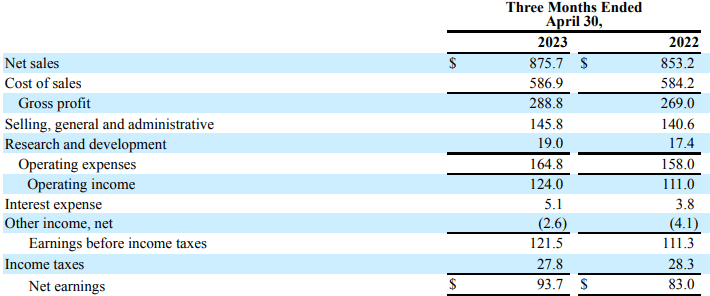

DCI recently posted its Q3 FY23 results . The net sales for Q3 FY23 were $875.7 million, a slight rise of 2.6% compared to Q3 FY22. I believe increased Off-Road and On-Road and industrial solutions segment sales were the major reason behind the revenue increase. The Off-Road and On-Road sales grew by 10.7% and 5.3% in Q3 FY23 compared to Q3 FY22. I believe the rise in Off-Road and On-Road sales was mainly due to the extensive global equipment production. The revenues from the industrial solutions segment grew by 13.8% in Q3 FY23 compared to Q3 FY22. I believe a 13% revenue rise in its industrial filtration solutions business which was driven by industrial gases part sales, and a 22% revenue rise in its Aerospace and defense business which was driven by a strong recovery in the commercial aerospace industry, was the main reason behind the revenue rise in its industrial solutions segment.

{kind=link}

Their gross profit margin for Q3 FY23 was 32.9% which was 31.5% in Q3 FY22. I believe gross margin improved mainly due to the reduction of the inflation rate for input costs and high pricing benefits. The net earnings also increased by 12.9% in Q3 FY23 compared to Q3 FY22. In my opinion, the financial performance of DCI wasn't very noteworthy. The flat revenue growth in the mobile solutions segment and the 12.6% revenue decline in the life sciences segment hampered their revenue growth. In my opinion, raising prices might help them in the short term and to some extent, but they might not be able to solve the demand problem in the long run with the higher pricing. Therefore, I believe that if the current trend continues, their revenues may drop in the upcoming quarters.

Technical Analysis

{kind=link}

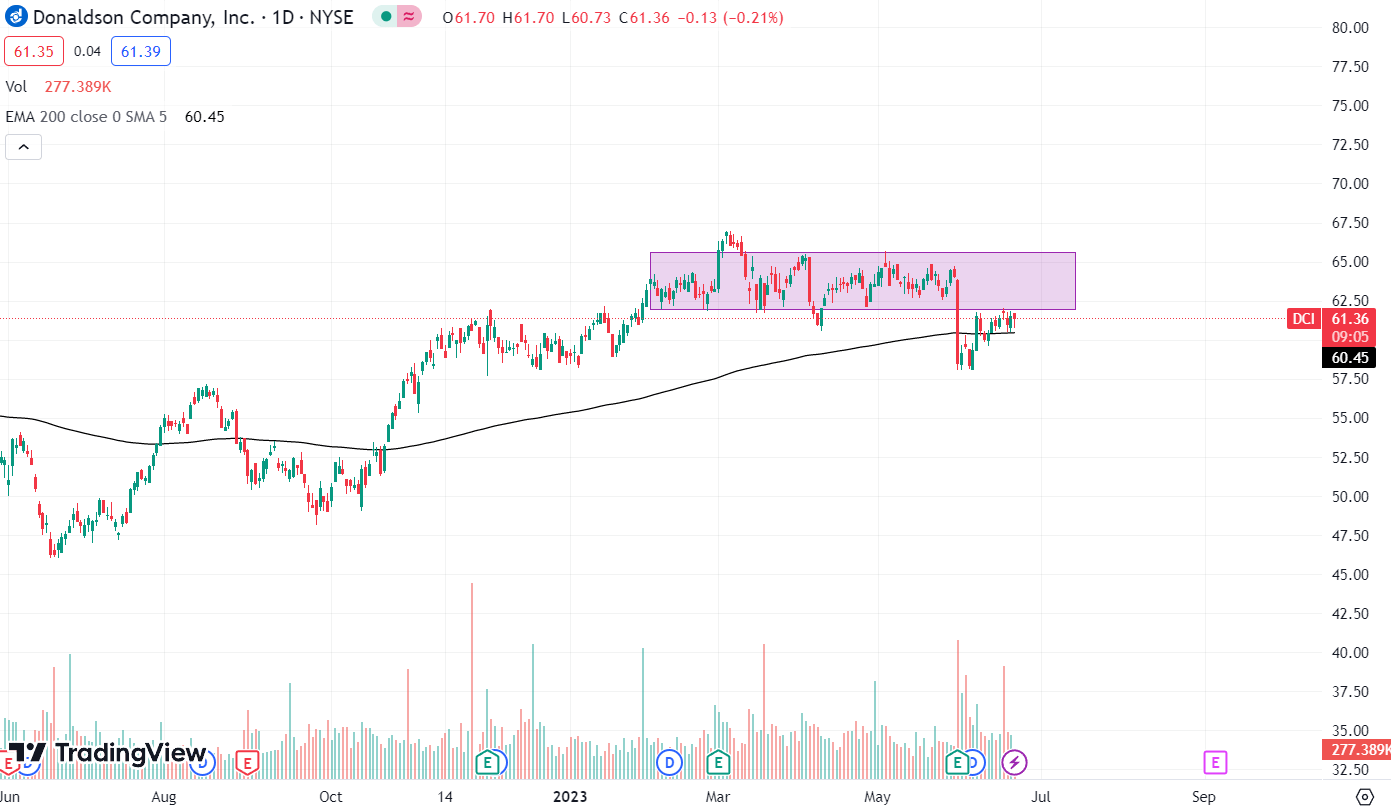

DCI is trading at the $61.3 level. If we look at its price action over the past three months, we can see the size of red candles is much bigger than that of green candles, indicating a selling pressure in the stock. In addition, it gave a breakdown from the $62 level and is headed to retest the level. I believe after testing the level; the stock might continue its downside trajectory. Hence looking at its price action, I think it is best to avoid the stock for now.

Should One Invest In DCI?

First, talking about DCI's valuation. I will use PEG and P/E ratios to judge to valuation. The PEG ratio of a firm can be calculated by dividing the P/E ratio by the annual EPS growth, and the P/E ratio is calculated by dividing a company's stock price by the earnings per share. DCI has a PEG [FWD] ratio of 2.02x compared to the sector ratio of 1.65x, and it has a P/E [FWD] ratio of 20.17x compared to the sector ratio of 17.09x. I believe DCI is overvalued after looking at the ratios and its slow growth rate. The management has provided revenue guidance for FY23, which is just 4.2% higher than FY22 revenue. So I think one should pay a high premium to only high-growth companies, and I believe DCI is currently not worthy enough to trade at high valuations.

Their industrial solutions segment has done well, and I believe with continued recovery in the commercial aerospace industry, their industrial solutions segment might do well in the coming quarters. However, if we look at its life sciences segment, it is currently facing weakness, and it is one of the major reasons behind the modest revenue growth of the company. I believe the life sciences segment might continue to struggle in the coming quarters due to the weakness in the disk drive market. In addition, the management has also revised its FY23 sales guidance for the life sciences segment. Earlier, the predicted sales decline in the life sciences segment was around 5%-9%, but now it is revised to be around 10%-12%. Hence I think this might hamper its revenue growth, and I expect its FY23 revenue growth to be less than 5% which I believe is quite less, and I don't see any positive factor that might increase or benefit its share price in 2023. So I don't think they might be able to provide returns to the investors in 2023. In addition, their revenue growth doesn't justify its high valuation; hence I think it is not worth buying DCI.

So looking at its weak price action, slow growth, and high valuation, I believe it is not worth investing in DCI right now. Hence I assign a hold rating on DCI.

Risk

Their business actions are influenced by certain industry market trends, and disruptive technology may pose a threat to their expansion. Changes in technology that can lower or eliminate the market for their products could negatively influence them. Wider use of technology offering diesel engine substitutes, such as equipment electrification, is one of these threats. Such disruptive innovation might displace current businesses and products while also opening up new markets, which would have extremely detrimental effects on the company. If they do not adequately anticipate future client needs or may take too long to adjust to such disruption, this could negatively affect their operations, financial health, and cash flow.

Bottom Line

The price action that the stock is making is bearish and indicates that more downside is possible. In addition, DCI is overvalued, in my opinion, and the current growth rate doesn't justify the high valuation. So looking at all the factors, I assign a hold rating on DCI.

For further details see:

Donaldson Company: Overvalued Company With Slow Revenue Growth