LCII - Dorman Products: Getting Closer To Pulling The Trigger

2023-09-17 08:34:44 ET

Summary

- Dorman Products, a supplier of aftermarket automotive parts, has experienced mixed financial results despite increasing sales and cash flow.

- The stock has dropped while the broader market has seen gains, catching the attention of value investors.

- The company's financial performance has been volatile and shares still don't make sense to be excited over, but it's not far off from that point.

One of the most frustrating things about investing is that, even when things are going reasonably well, shares to the company that you own can still experience downside. One good example of this that I could point to involves Dorman Products ( DORM ), a major supplier of replacement and upgrade parts in the motor vehicle aftermarket industry. Sales continue to climb, and while cash flow is generally performing well, overall bottom line results have been mixed. The stock was never cheap, nor was it really expensive. But even so, general concerns about the market has caused the stock to drop some even while the broader market has seen some nice upside. As a value investor, this immediately catches my attention because it could represent a good opportunity. And to be perfectly honest, shares are getting close to the point where I might upgrade them. But at the moment, I've decided to keep them rated a ‘hold’.

An interesting ride

Back in early March of this year, I performed my first deep dive into Dorman Products. The first thing that I noticed about the company was the fact that it had a rather lumpy operating history. Overall sales had been robust, but profits and cash flows were inconsistent from year to year. I found myself excited about guidance that management had issued for the 2023 fiscal year. But even with that bullish outlook, the stock was priced high enough to justify a ‘hold’ rating. Since then, things have not gone exactly as I thought they would. When I rate a company a ‘hold’, it is because I view the stock experiencing upside or downside that would be more or less in line with what the broader market sees. But that is not what happened here. While the S&P 500 has jumped 10.7%, shares of Dorman Products have dropped by 13.8%.

{kind=link}

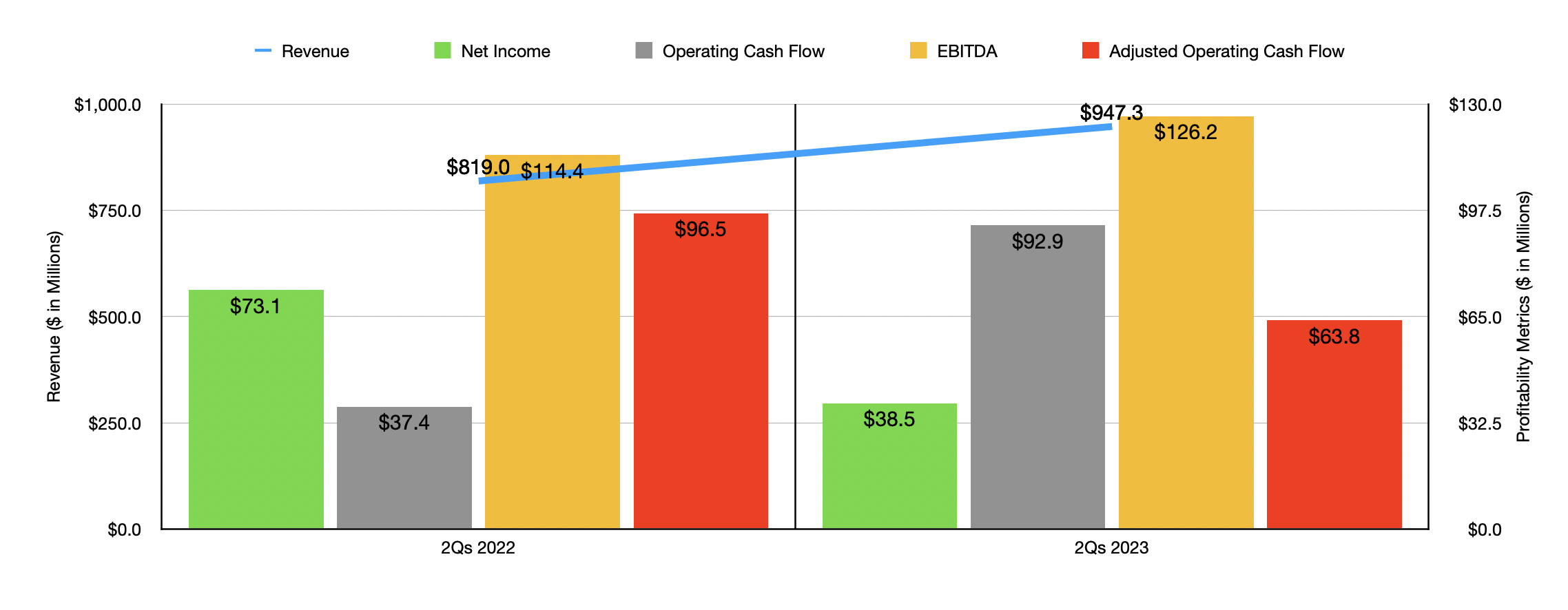

To say that some pain was completely unwarranted would be perhaps an overstatement. And this brings us back to the overall financial performance of the company and how it can be volatile from time to time. For starters, we should touch on revenue. So far this year, sales have been $947.3 million. That represents an increase of 15.7% over the $819 million the company reported the same time last year. This increase in sales was driven largely by the company's purchase of SuperATV back in October of last year. But without that purchase, sales still would have inched up about 2%, thanks to price increases aimed at offsetting inflation and by the introduction of new products to the market.

On the bottom line, the picture was more complicated. Net profits, for instance, totaled only $38.5 million. That's barely over half of the $73.1 million the company reported one year earlier. A decline in the company's gross profit margin from 33.5% to 32.5% caused some of this pain, with the drop largely associated with the sell-through of higher cost inventory that was purchased in 2022 when inflation was higher than it is now. Even more problematic, however, was a jump in the company's selling, general, and administrative costs. These expenses rose from 21.8% of sales to 24.8%, largely because of higher interest rates on its customer accounts receivable factoring programs and because of the lower margins from the aforementioned acquisition of SuperATV.

{kind=link}

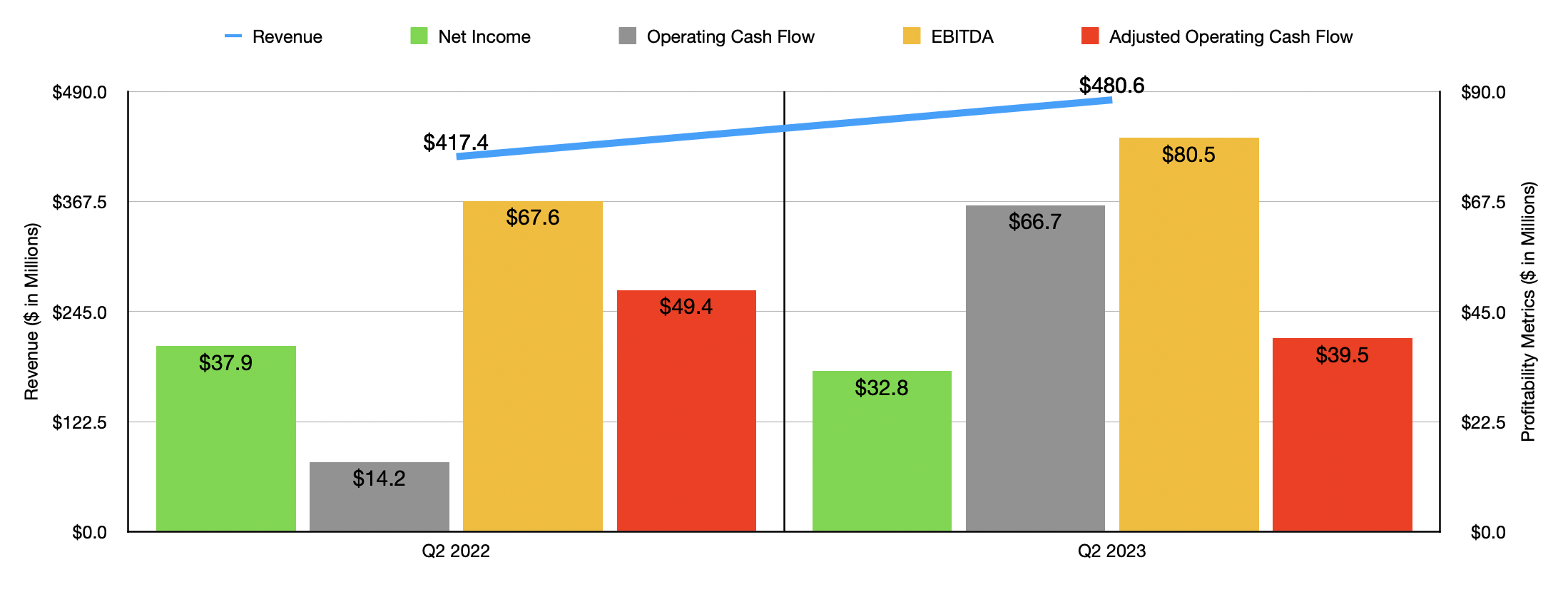

Other profitability metrics were all over the map. For instance, operating cash flow shot up from $37.4 million to $92.9 million. But if we adjust for changes in working capital, we would get a decline from $96.5 million to $63.8 million. On the other hand, however, EBITDA for the business improved from $114.4 million to $126.2 million. For those curious, the most recent quarter on its own showed results that were very similar on a year over year basis to what the first half of the year in its entirety demonstrated. These results, for reference, can be seen in the chart above.

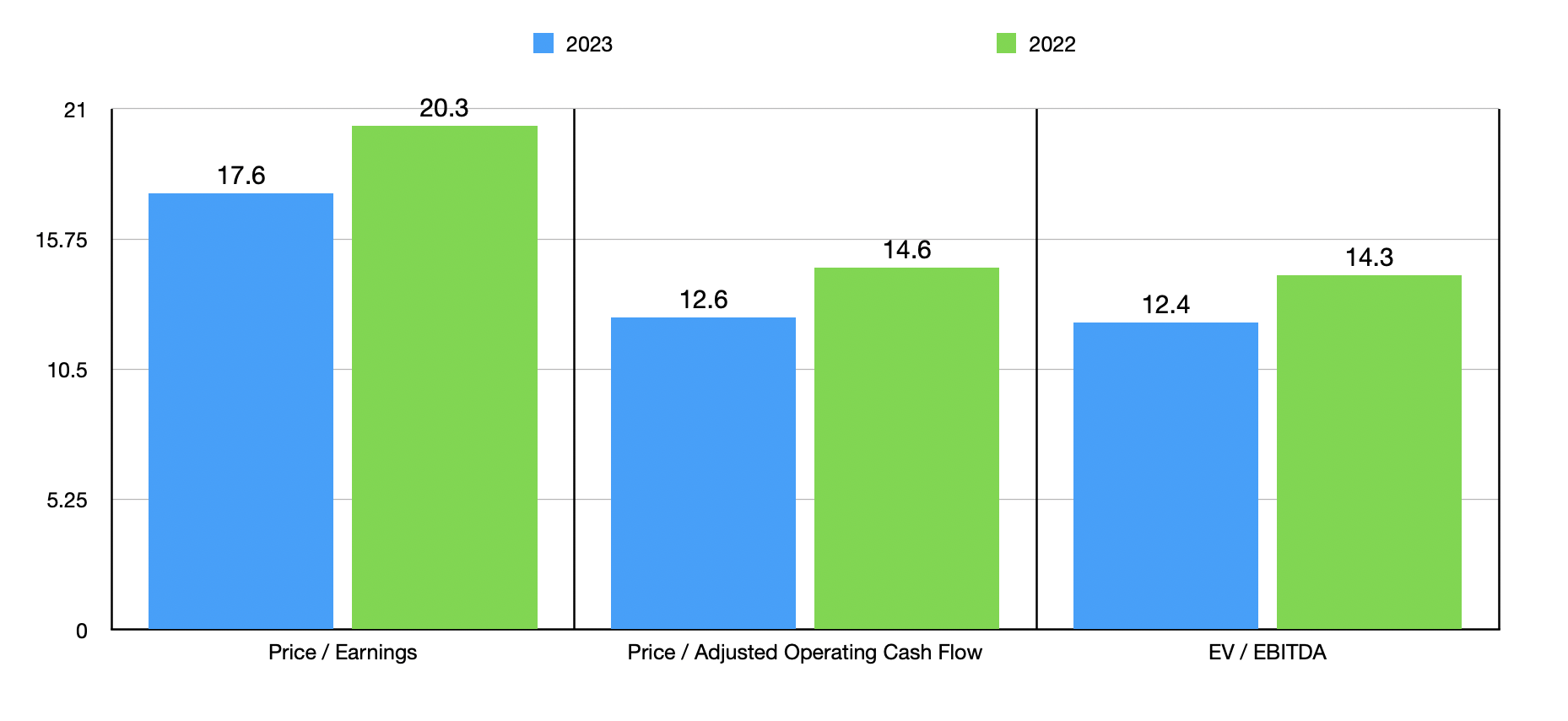

Even though the company is experiencing a bit of pain right now, management has high hopes for the current fiscal year as a whole. Earnings per share, should come in at between $4.35 and $4.55. At the midpoint, that would translate to net profits of $140.5 million. This would stack up nicely against the $121.5 million in profits the company generated in 2022. A good portion of that increase would be driven by higher revenue, with sales totaling between $1.95 billion and $2 billion this year. By comparison, last year, sales were $1.73 billion. Unfortunately, management has not provided any guidance for the year when it comes to other profitability metrics. But if we assume that they will increase at the same rate that net profits should, then we should anticipate adjusted operating cash flow of $196 million and EBITDA of $249.1 million.

{kind=link}

In the chart above, you can see what these projected financial results make the company look priced as. You can also see how the company is priced using data from 2022. Clearly, on a forward basis, the stock is looking more attractive. In addition to this, just objectively speaking, shares are not priced out of the range of what I would start to appreciate as a potential prospect. Taking that data then, I compared Dorman Products to five similar firms in the table below. What I found was that, using each of the three metrics, three of the five companies ended up being cheaper than it.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Dorman Products |

| 17.6 |

| 12.6 |

| 12.4 |

| LCI Industries ( LCII ) |

| 35.0 |

| 5.6 |

| 14.4 |

| Modine Manufacturing Co ( MOD ) |

| 13.6 |

| 18.5 |

| 11.2 |

| Dana Inc ( DAN ) |

| 16.7 |

| 3.8 |

| 8.1 |

| Gentherm ( THRM ) |

| 162.9 |

| 24.6 |

| 20.3 |

| American Axle & Manufacturing Holdings ( AXL ) |

| 21.3 |

| 2.2 |

| 4.5 |

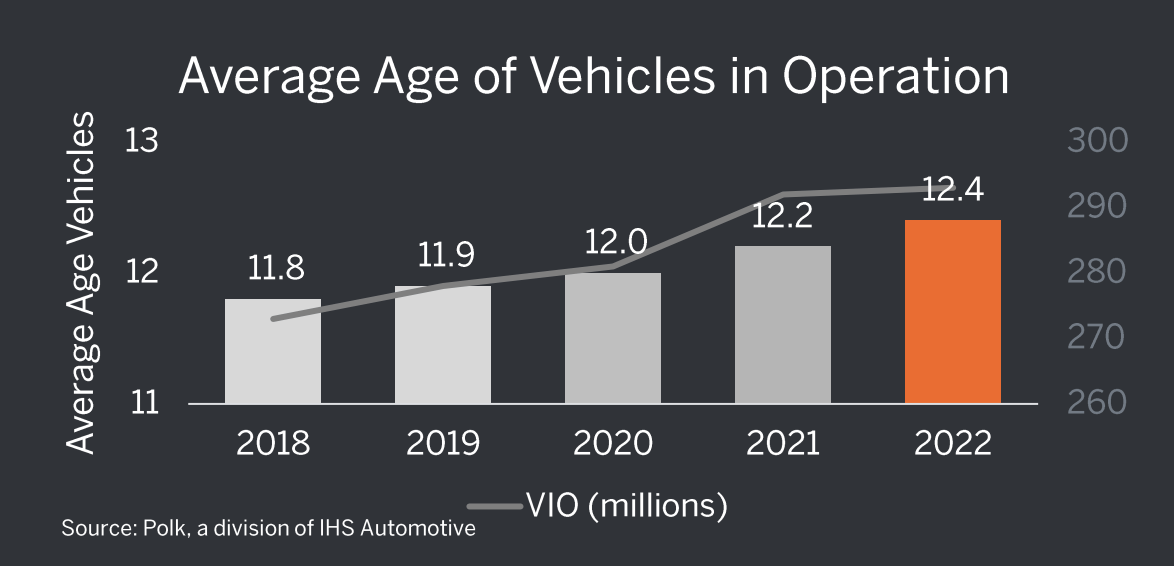

Taking a step back, it would be helpful to talk about the market more broadly. As I mentioned earlier, our prospect focuses on the automotive space. The fact of the matter is that this is a difficult market in some respects. Because of a couple of years of high levels of inflation, car prices are still elevated. In addition to this, high interest rates make acquiring cars prohibitive. But as a player largely focused on the aftermarket space, these factors might work in its favor. This is because aftermarket parts are more likely to be used in a vehicle as that vehicle ages. And the long-term picture there has been very positive. Back in 2018, for instance, the average age of vehicles in operation in the US totaled 11.8 years. That number came out to 12.4 years in 2022. More likely than not, that trend will continue.

{kind=link}

Takeaway

Operationally speaking, Dorman Products is not exactly the best company out there. I applaud its consistent revenue growth, but I do not like the volatility on its bottom line. After all, bottom line results are the most important in the long run. Long term, management will likely do well in growing the company further and shares are not priced outrageously high. But between the bottom line volatility and the pricing compared to similar firms, I do believe that there are still better prospects that can be had. But if I see the stock drop another 10% or 20%, things could become very interesting very quickly.

For further details see:

Dorman Products: Getting Closer To Pulling The Trigger