DDI - DoubleDown Interactive: A Cigar Butt Company

Summary

- DoubleDown Interactive is a small gaming company with growing margins, solid cash flow, and deeply negative net debt, but valued at a significant discount to book value.

- For a long time, the key risk factor for DDI investors has been litigation. Looks like this risk factor has been left behind.

- While the potential of bears is limited by a low float, acquisitions will allow the company to diversify revenue, which may lead to a revaluation of shares.

- Given that the nearest peer is trading at P/FCF 7.56, the upside potential we see is about 45%.

Investment Thesis

DoubleDown Interactive ( DDI ) is a small gaming company with growing margins, solid cash flow, and deeply negative net debt, but valued at a significant discount to book value. For a long time, a sword hung over the company in the form of a lawsuit that could deprive DDI of a significant part of its assets. It seems that this risk factor has been left behind. And although at the point the shares reacted with a 12% increase, DoubleDown remains a deep value case. The use of liquid assets accumulated on the balance sheet can reveal the value of the company. It is expected that cash will be used for M&A transactions, which will allow DDI to get a new growth driver, diversify revenue and improve profitability due to the synergistic effect. A high insider ownership share and a low float can limit the decline of the stock and lead to a squeeze in case of excessive demand. Given that the nearest peer is trading at P/FCF 7.56, the upside potential we see is about 45%. We rate shares as a Buy .

Company Profile

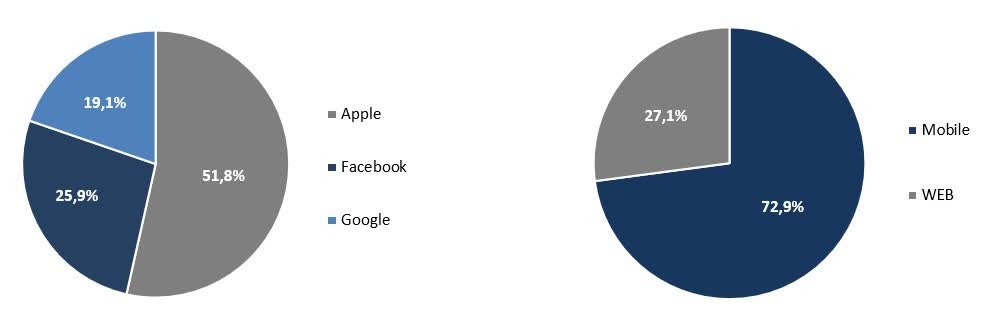

DoubleDown Interactive develops gambling games for mobile devices and in WEB format. At the moment, the company's portfolio includes four games, three of which are casinos and one is a zombie apocalypse RPG. Spinning Space is expected to be released this quarter, as well as releases of several games next year. The developer earns from in-game purchases of users mainly in the USA (87.5% of revenue). The share of WEB games in revenue is 27.1%, and mobile games - 72.9%. DoubleDown Casino's flagship game generates 96.6% of DDI's revenue.

{kind=link}

Created by the author

A True Value Case

In a letter to Berkshire Hathaway shareholders from 1989, Warren Buffett wrote that a cigar butt found on the street that has only one puff left in it may not offer much of a smoke, but the "bargain purchase" will make that puff all profit. By a cigar butt, the Oracle from Omaha meant shares of companies with a market capitalization below the liquidation value of the business. Such a company is DoubleDown Interactive.

With a current capitalization of $533.2 million, the company's book value is $843.1 million, of which net current assets account for $215.2 million or 25.5%. It is worth noting that the balance of Total Cash & ST Investments is $284.4 million, which corresponds to two-thirds of the market capitalization of DDI. DoubleDown also looks as cheap as peers.

| DoubleDown |

| Playtika (PLTK) |

| Churchill Downs (CHDN) |

| EA (EA) |

| Activision (ATVI) |

| P/E [TTM] |

| 18.80x |

| 15.13x |

| 16.41x |

| 41.07x |

| 32.97x |

| P/B |

| 0.56x |

| -24.73x |

| 12.61x |

| 4.73x |

| 3.38x |

| EV/Sales |

| 0.69x |

| 2.23x |

| 6.16x |

| 4.98x |

| 7.13x |

| P/Cash flow |

| 5.24x |

| 7.76x |

| 15.02x |

| 18.35x |

| 30.47x |

The valuation of DDI looks irrational since the company is trading at a significant discount to the liquidation value, which corresponds to firms burning shareholder value. DoubleDown, in turn, constantly increases marginality and generates a solid cash flow. According to the results of the last reporting period, cash from operations and free cash flow exceeded $100 million.

In the pursuit of value, it is important not to fall into a trap. DoubleDown does not look like a value trap, because a) the company increases its marginality; b) DDI generates solid cash flow; c) the firm has a strong balance sheet and deeply negative net debt.

In the second quarter, DDI showed a loss of $34.1 million due to the creation of a provision for legal costs of $71.5 million. The company's adjusted net profit is $37.4 million.

Liquid assets can become a potential driver for the disclosure of value. The probability of buybacks is unlikely since the company has a low float. However, management regularly talks about plans for strategic acquisitions.

" We are targeting - augmenting our business through strategic M&A opportunities, while we, of course, cannot make any assurances about the timing of a potential transaction" - In Keuk Kim , CEO.

Potential acquisitions will allow the company to get a new growth driver, diversify revenue and improve profitability due to the synergistic effect. In addition, a reduction in the balance sheet will lead to an increase in ROA and ROE due to an increase in asset turnover. Thus, the reasonable use of cash can become a driver for the revaluation of shares.

Ownership Structure As Fall Protection

Almost all shares are owned by affiliates, insiders, and employees. The largest shareholder of the firm is B. Riley Financial with a share of about 8.3%. B. Riley acted as an underwriter of DDI in 2021. The Korean parent company DoubleU Games owns a 67% stake. About 5% is in free float. Such a low float can limit the fall of stocks and lead to a squeeze in case of excessive demand. However, a low float also limits liquidity and creates a risk of high volatility for investors.

The Key Risk Factor Is Behind

For a long time, the key risk factor for DDI investors has been litigation. A group of people led by Adrienne Benson initiated a lawsuit against DDI and IGT for illegal activities in Washington State. According to the prosecutors, the total damage amounted to over $2 billion. DoubleDown management approved the upper limit of the settlement of the case at $201.5 million. IGT also allocated $150 million for court costs, but in its statement asking to reject the plaintiffs' petition, shared that it had made significant progress during negotiations with the plaintiffs.

On August 29, DoubleDown and IGT announced a settlement of the lawsuit. In total, the companies will pay $415 million, of which $269.75 million will be contributed by IGT, and the remaining $145.25m will pay DDI. DoubleDown has to allocate another $73.75 million in payment for the Benson case, and most likely this will happen in the next quarter. After the release, the shares reacted with a 12% increase, which is insignificant, given that the company has lost its main risk factor.

Conclusion

DoubleDown is a classic example of Buffett's cigar butt: the company demonstrates positive margins, generates solid cash flow, trades at a significant discount to equity, and a fair share of total cash & short-term investments has accumulated on its balance sheet, which is expected to be directed to M&A transactions. While the potential of bears is limited by a low float, acquisitions will give the company a new growth driver, allow it to diversify revenue, and improve profitability, which may lead to a revaluation of shares. Since the key risk factor seems to have been left behind, we are bullish on DDI.

For further details see:

DoubleDown Interactive: A Cigar Butt Company