REVG - Douglas Dynamics Still Offers Upside From Here

Summary

- Douglas Dynamics has had a nice run in recent months, with fundamental performance pushing shares higher.

- This may deter investors from buying in now, but the move higher doesn't mean shares don't offer additional upside.

- In all, the company still makes for a solid prospect for investors to consider.

For some jobs, a truck is necessary. Whether this be to haul something, to carry significant loads of tools, or something else, a truck can be an indispensable tool without which certain jobs might not be done. But trucks are not naturally structured to meet every possible use case. So to compensate for that, attachments and other equipment have been produced over the years to enable them to do more. Examples of this include snow and ice control equipment, sand and salt spreaders, and more. One company that provides these products and that also upfits various vehicles with racking, storage solutions, and more, is Douglas Dynamics ( PLOW ). Despite broader economic concerns, the company has been doing quite well for itself in recent quarters. Revenue, profits, and, by some measures, cash flows, have all been on the rise. In response to this, shares of the company have moved higher at a time when the broader market has dropped. Because of this, I would make the case that the easy money has already been made. But based on how shares are priced at the moment, I believe that some additional upside might be on the table.

Plowing through the market pain

Back in late March 2022, I wrote an article that took a bullish stance on Douglas Dynamics. In that article, I acknowledged that the pandemic had impacted the company's fundamental performance for a couple of years. But outside of that, the firm's overall fundamental condition was favorable and, while shares weren't exactly cheap, they were getting close to that point. Based on the assumption of continued growth, I ultimately concluded that the company offered some attractive upside moving forward. And because of that, I ended up rating the company a 'buy' to reflect my view that shares should outperform the broader market for the foreseeable future. The results since then have been amazing. While the S&P 500 is down 15.3% since the publication of that article, shares of Douglas Dynamics have generated an upside of 10.6%. Frankly, this return disparity is far beyond what even I anticipated.

{kind=link}

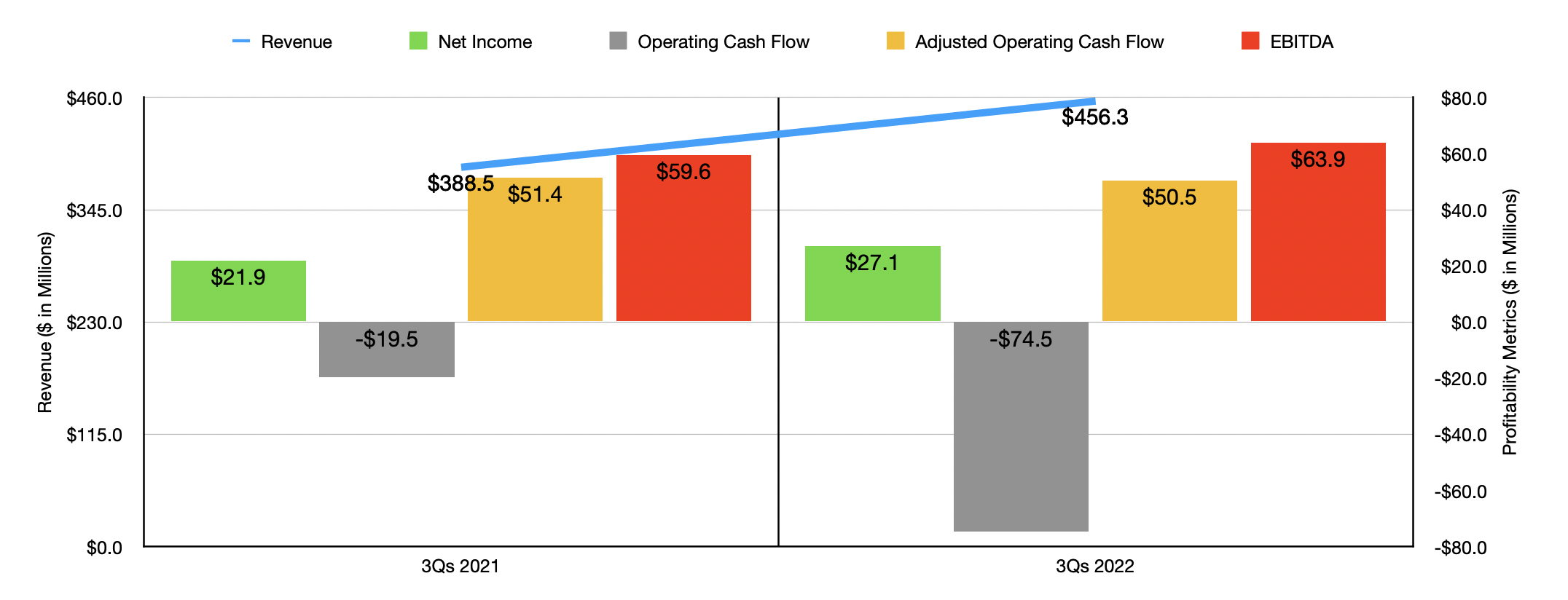

This return disparity may seem odd given the broader economic concerns we are faced with. But the fact of the matter is that the market has rewarded robust fundamental performance. Consider results for the first nine months of the company's 2022 fiscal year. During that time, revenue came in at $456.3 million. That's 17.5% higher than the $388.5 million reported one year earlier. Management has not offered much in the way of detail on this. But they did say that the revenue increase during this time was driven primarily by management's decision and ability to increase prices and by strong order volume for some of its offerings. This includes preseason order volume associated with the company's snow-related offerings.

The end result here was increased profits as well. Net income jumped from $21.9 million to $27.1 million. This came despite the fact that the gross profit margin for the company dropped from 27.2% down to 24.9%, driven by inflationary pressures. Other profitability metrics have been somewhat mixed. For instance, operating cash flow actually declined from negative $19.5 million to negative $74.5 million. If we adjust for changes in working capital, however, the decline would have been more modest from $51.4 million to $50.5 million. Over the same window of time, however, EBITDA for the company expanded from $59.6 million to $63.9 million.

{kind=link}

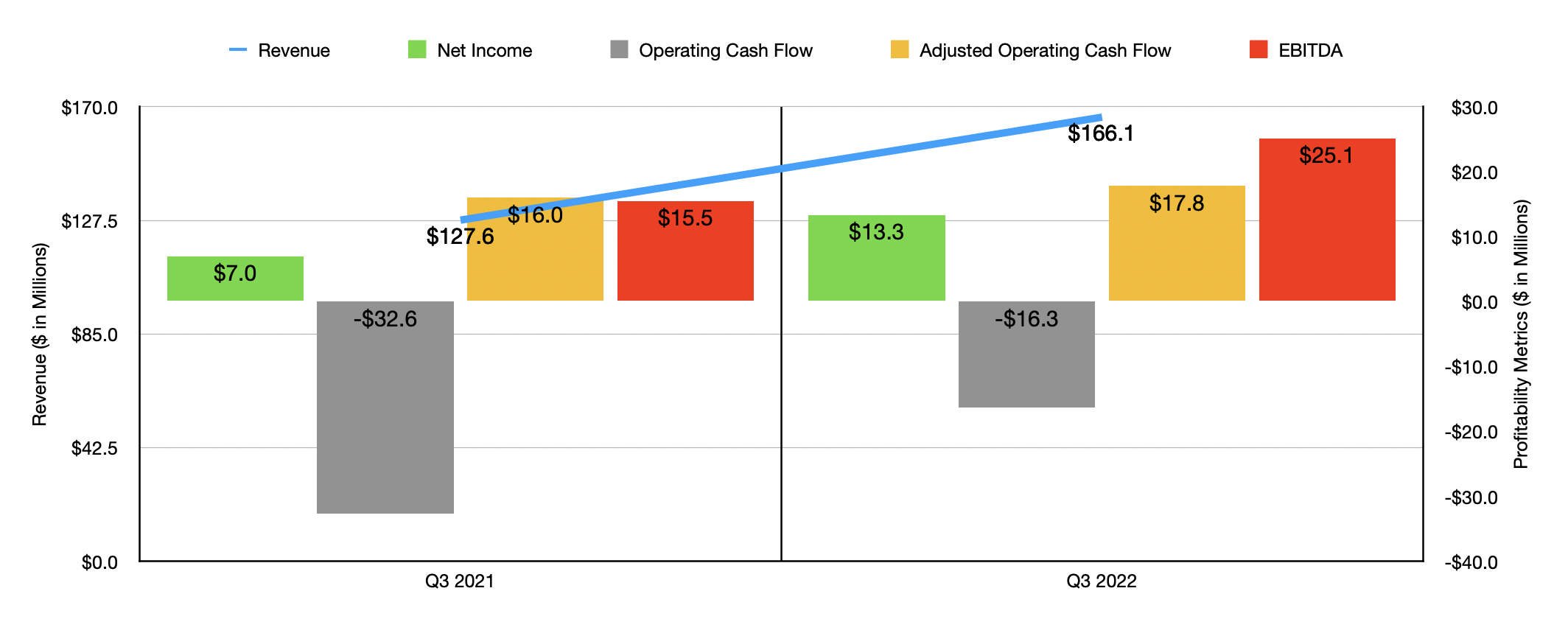

In this economic environment, it makes sense to worry about the fundamental picture of the business changing rapidly. But that doesn't appear to be a problem in this case. To see what I mean, we need only look at data for the third quarter on its own. Sales of $166.1 million dwarfed the $127.6 million reported in the same period of 2021. This resulted in a near doubling of net profit from $7 million to $13.3 million. Operating cash flow improved from negative $32.6 million to negative $16.3 million, while the adjusted figure for this went from $16 million to $17.8 million. Meanwhile, EBITDA rose from $15.5 million to $25.1 million.

In addition to doing well in the first nine months of the year, management is forecasting overall results for 2022 to be positive compared to 2021. Revenue for the company, for instance, should be between $600 million and $630 million. Earnings per share should be between $1.65 and $2.05. At the midpoint, that would translate to net income of $42.3 million. The firm also said that EBITDA should be between $80 million and $95 million. No guidance was given when it came to other profitability metrics. But if we assume that adjusted operating cash flow will increase at the same rate that EBITDA is expected to at the midpoint, then we should anticipate a reading for it of $72.5 million.

{kind=link}

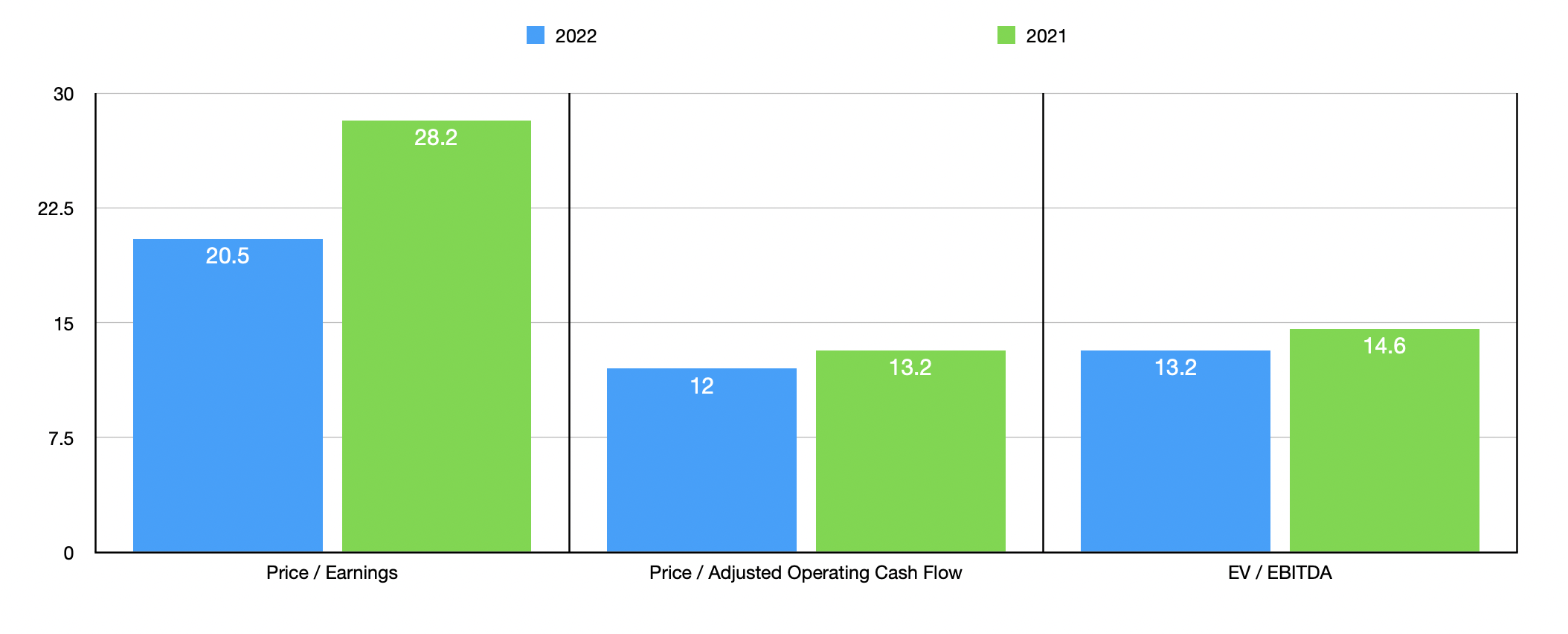

Based on these figures, the company is trading at a price-to-earnings multiple of 20.5. This is down from the 28.2 reading that we would get using data from 2021. The price to adjusted operating cash flow multiple is even lower at 12, down from the 13.2 reading that we would get using data from the prior year. And the EV to EBITDA multiple should be around 13.2. That stacks up favorably against the 14.6 reading that we get using data from the year before. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 11.4 to a high of 76.1. Only one of the five firms was cheaper than Douglas Dynamics. Using the price-to-operating cash flow approach, the range was from 8.5 to 132.6. And when it comes to the EV to EBITDA approach, the range was from 8.3 to 36. In both of these cases, two of the five companies were cheaper than our prospect.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Douglas Dynamics |

| 20.5 |

| 12.0 |

| 13.2 |

| Astec Industries ( ASTE ) |

| 76.1 |

| 132.6 |

| 36.0 |

| REV Group ( REVG ) |

| 51.1 |

| 8.8 |

| 14.6 |

| Wabash National ( WNC ) |

| 25.8 |

| 8.5 |

| 11.5 |

| The Shyft Group ( SHYF ) |

| 25.7 |

| 21.9 |

| 19.1 |

| Terex Corp. ( TEX ) |

| 1.4 |

| 41.4 |

| 8.3 |

Takeaway

Based on the data provided, I must say that I continue to be impressed by the performance achieved by Douglas Dynamics. I believed when I wrote about the firm previously that shares would outperform the broader market. But I would not have guessed by this much. Shares have gotten a bit more expensive since I last wrote about the firm. But given the continued fundamental improvements and how affordable shares still are, I think that some additional upside is probably on the table. Because of this, I have no problem keeping my rating for the company at the 'buy' level I had it at previously.

For further details see:

Douglas Dynamics Still Offers Upside From Here