DOW - Dow: Chemical Maker Struggles With Earnings Decline And Macro Headwinds (Downgrade)

2024-01-12 00:17:22 ET

Summary

- Dow downgraded to Sell, from a prior Buy rating, more bearish than today's rating consensus on SA.

- DOW stock climbed by double-digit percentage points since autumn, presenting a good sell point as revenue/earnings/macro outlook is weak.

- Strengths include stable dividends, strong liquidity, and brand presence.

- Falling oil prices and weak forecasts may also impact some of its businesses.

Stock & Industry Snapshot

Several times while visiting the Texas Gulf Coast, I passed through a small, unassuming town called Freeport, and right before where the bay waters meet the open ocean and where the fleets of shrimp boats go out to sea, lies one of the biggest chemical plants in America.

That plant is run by none other than Dow Inc. ( DOW ), and today I'll be covering its stock.

According to the company , plants like this one help make possible some of the everyday products we may take for granted: mouthwash, garbage bags, cosmetics, paints, and more.

A few more quick facts about Dow, which trades on the NYSE and actually has corporate headquarters in Michigan, are that it is diversified across multiple business segments such as Dow Packaging, Dow Consumer Solutions, Dow Polyurethanes, and Dow Industrial Solutions.

For instance, one of their many solutions is producing industrial-grade cleaning agents for food, dairy, and beverage processing environments, a necessary solution to reducing risk of contamination in food processing plants.

I last covered this stock in early October when I called it a buy , and since then the share price has risen nearly 4%.

Dow - price since last rating (Seeking Alpha)

From key market data on Seeking Alpha, however, we can see that the materials sector has not performed as well as some other sectors, going up just +9.4% in 3 years, although industrials have gone up nearly +25%.

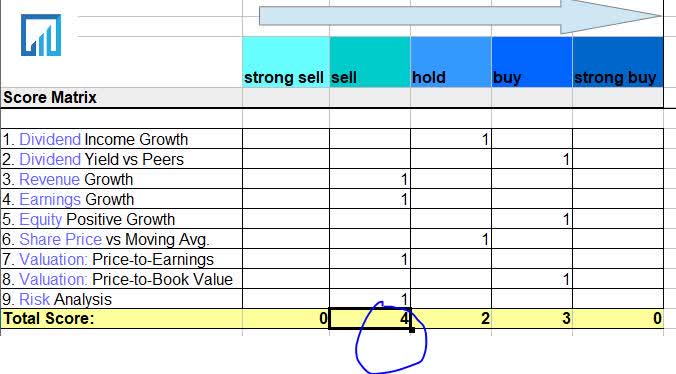

Scoring Matrix

We use a 9-point scoring method that looks at this stock holistically and assigns a total rating score, using a score matrix. Our approach focuses heavily on accounting statements and follows a logical progression to find relationships between earnings data, share price, and valuation.

{kind=link}

Today's Rating

Based on the score total in the score matrix , this stock is getting a rating of sell.

This is a downgrade from my prior buy rating.

Compared to the consensus rating on Seeking Alpha today, I am more bearish than the consensus:

Dow - ratings consensus (Seeking Alpha)

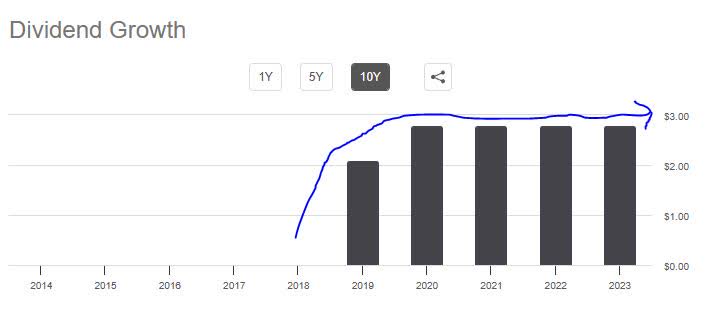

Dividend Income Growth

First, let's talk about dividend income growth potential as an income strategy with this stock. We can see the growth trend in the following chart:

{kind=link}

The data begins in 2019 when the dividend was $2.10/share/annually, and then it grew to $2.80 the next year (a 33% growth) and stalled at that rate. In fact, the history tells us the quarterly dividend of $0.70/share has not gone up in years.

Looking ahead I also have lower confidence in a dividend hike soon considering that earnings have seen a YoY decline, although the company has positive cash flow .

I think the evidence on dividend growth does not present a buy case however the dividend payout of $0.70/share has been steady without interruption, so I am inclined to say hold.

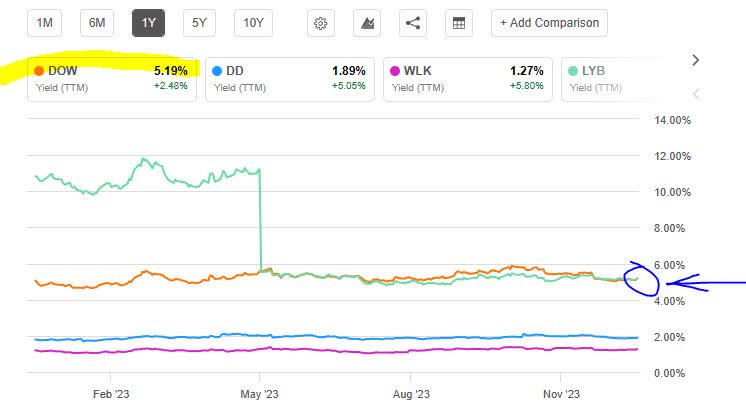

Dividend Yield vs. Peers

My last coverage of this stock boasted of its attractive dividend yield, and I can do so again as it is past the 5% mark.

However, I want to compare against 3 other peers in this sector and pick the best one or two, using the dividend yield comparison tool :

{kind=link}

Dow leads the pack with a trailing yield of +5.19%, tied with chemicals maker LyondellBasell Industries ( LYB ), while Dupont de Nemours ( DD ) and Westlake Corp ( WLK ) are trailing behind with less than 2% yield.

I will reiterate my prior view then and call it a buy at this yield of over 5%, worth snagging especially now in the larger environment of more competitive yields in non-stocks (CDs, fixed-income, etc.) and therefore folks looking to get the best return on capital invested.

Revenue Growth

In this part, we will look at YoY revenue growth but also anticipate what it will do going forward. As the saying from a popular Wall Street movie goes, I am here to guess what the music will do in a month or year from now.

From the income statement , we know that total revenues dropped to $10.73B in the quarter ending September, vs $14.11B in Sept 2022, a 24% YoY decline.

This is what the company said in its Q3 remarks as a driver of this:

Declines in all operating segments due to slower global macroeconomic activity. Sales were down 6% sequentially, as volume gains were more than offset by lower local prices.

We can see in the following graphic a running theme of drops in demand and or drops in price, leading to lower revenue trends:

Dow - business segment sales decline (company Q3 presentation)

Although the FY23 Q4 results are not due out for another few weeks, on Jan. 25th, we can form an educated guess on where things could be going in 2024 with this firm.

Just from the Q3 earnings release and presentation, I could gather that macroeconomic factors affect this firm, driven by consumer caution, lower industrial activity, weakness in the EU market, and decrease in global manufacturing indexes.

It is understandable that this would cause a headwind to a company that produces materials that both industry and consumers purchase.

I want to point out that, according to Statista , the purchasing managers' index (PMI) has been on a steady decline in the US since 2021:

{kind=link}

Although there was a slight uptick in December in the PMI, it does not necessarily point to strong growth expected for 2024. Here is what a Jan. 5th article by S&P Global had to say on that topic:

Some encouragement regarding the near-term global growth trend can be derived from the slight acceleration in growth during December, having been driven by an increased in new order inflows, which showed the largest rise since last June. Similarly, business expectations about the year ahead lifted higher in December, also striking the most optimistic tone since last June.

However, both of these forward-looking gauges remain weak by historical standards, hinting at sustained sub-par growth .

Therefore, I am convinced the case here is for a sell , not only due to double-digit YoY revenue declines but also macro factors causing headwinds to this company.

Earnings Growth

Now that we discussed the top line at great length, we will briefly touch on the bottom line.

Based on the income statement , it too saw a drop to $302MM in earnings (net income) in Q3 vs $739MM in Sept 2022, a 59% YoY decline.

It appears total operating expenses were not huge drivers to the decline, as they only grew modestly on a YoY basis, 3%. However, net interest expense grew by 23%. This, along with the drop in top-line revenue appears to be some of the key drivers of bottom-line declines.

I am convinced it is a sell case here too, due to double-digit earnings declines along with a continuation of the high interest-rate environment for now and how that could impact debt costs, as well as the macro headwinds to revenue that also impact earnings looking ahead.

Equity Positive Growth

On the equity front, the picture is rosier.

We can see from the balance sheet that total equity grew to $20.08B in Q3, vs $18.62B in Sept 2022, a YoY growth of 7.8%.

In addition, the company boasts of +$13B of available liquidity , no debt maturities until 2027, and strong credit ratings:

Dow - financial strength (Dow q3 presentation)

At the same time, I would note that long-term debt had gone up to $14.02B in Q3, vs $12.2B in Sept 2022, for a 16% YoY increase.

However, we are talking about Dow, a company with +$58B in assets, so in relation to that the debt level is barely 25% of the amount of assets this firm has. In addition, the debt level is considerably down from the $15.8B in March 2021, so on a longer-term basis it is on the decline.

The evidence, I think, points to a buy in this category.

Share Price vs. Moving Average

The following is today's YCharts I pulled, showing a share price of $53.20 (as of this article writing) and its relation to the 200-day SMA of $52.72:

The share price is practically flat vs the long-term moving average right now, having dipped from its recent price spike. However, it is also around $6/share up from its autumn lows, or a +13% price growth since then.

So, it seems what I have here is a company with double-digit revenue and earnings declines, a weak macro forecast, and single-digit equity growth, that is trading near its moving average but double-digits above its autumn lows.

The larger sectors of materials and industrials have also not performed strongly as I mentioned earlier, and we can see from market momentum data that Dow has severely underperformed the S&P500 index in the last year.

I don't think it makes a great buy case here but also is still too cheap to just sell off. I say hold, but with the assumption, that it could be a longer-term hold until the macro effect improves and is reflected in earnings since there have always been macro recoveries eventually and the economy goes in various cycles.

Valuation: Price-to-Earnings

Here, we want to touch upon the forward P/E ratio, from valuation data on Seeking Alpha.

We see that the P/E is now 37.32, while the sector is only averaging around 18.

What I think is driving this elevated multiple is the steep gap between the double-digit earnings decline and the share price that is double-digit percentages above its autumn lows.

I cannot see why a 37x price multiple would be justified, with that type of earnings performance and a weak forward macro outlook.

In this peer group, I would pick Westlake Corp. which has a much better valuation at 15.8x forward P/E, even though it too has a rift between rising share price and declining earnings.

I will call Dow a sell at this valuation.

Valuation: Price-to-Book Value

Also from valuation data , we can see the forward P/B ratio is now at 1.96, pretty much in line with the sector average.

Tying back to the earlier discussion on share price and equity, what we know is there was a significant share price growth since autumn but it is still near its moving average for now, while equity has also grown by single digits.

This combination of share price at or below average, along with growing equity(book value) is what I am looking for, so I would call this metric a good buy case.

Risk Analysis

We already highlighted the decline in the PMI index and touched upon on a weak macro outlook in this case for 2024, so what is another downside risk this company can face going forward?

In an October article in Reuters , it was mentioned that some of Dow's business segments are affected by the price of oil:

The company added it expects to see benefits from rising oil prices in the next few quarters.

Prices of Dow products such as polyethylene, poly vinyl chloride and other base metals increase on the back of rising crude oil.

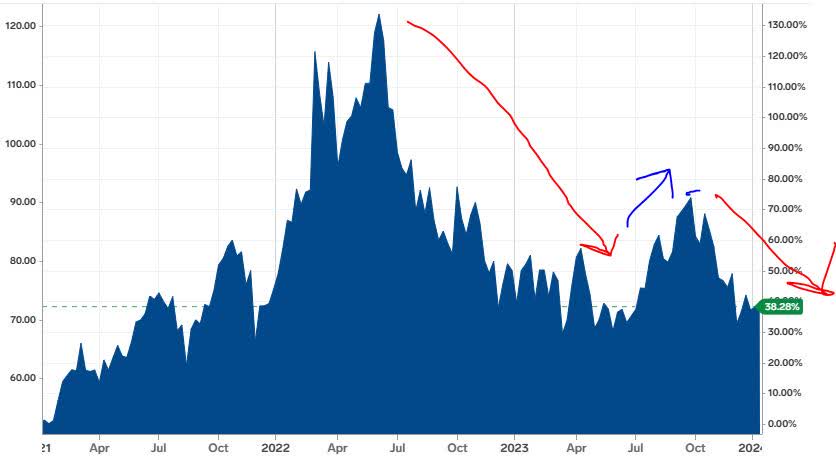

I think the downside risk therefore is a further decline in oil prices. At the time of the company's remarks, oil was on a rebound in October. However, if you look at the chart below from Business Insider , oil has dropped since then and going into 2024:

{kind=link}

In addition, a Jan. 9th article by CBC indicated we are in an environment of oversupply, and expectations of sluggish oil prices looking ahead:

Deloitte forecasts the average WTI (West Texas Intermediate) price will remain low through 2026 before rebounding slightly in the years leading up to 2030 - however, prices still aren't expected to climb over $80 a barrel.

So, in addition to the other macro factors I mentioned earlier, the issue of oil price I think will cause headwinds to this company's segments affected by that. Hence, the case here points to a sell , as there is too much not working in favor.

Quick Summary

To briefly summarize, I am downgrading this stock to a sell, from my buy rating last year. On a holistic basis, the thesis points to a sell rather than a buy or hold right now.

It has seen double-digit percentage price growth vs this autumn, although earnings and revenue have seen double-digit declines, and several macro factors including oil prices will not be in this company's favor going into 2024.

The firm has ample liquidity, positive cash flow, and has seen equity growth too. It also still has a +5% dividend yield.

My portfolio strategy on this one would be to take advantage of the 4% price gain since my prior buy rating, take the capital gain and redeploy elsewhere.

If I were to have a hold strategy, for dividend income purposes, I think I would have to hold on to this one far longer than I would like to, as I think the evidence shows there will be more likelihood of downside than upside this year.

For an investor looking to hold for many years, it is still a solid and well-established company that I think could recover when macro factors are in its favor again, but personally rather than playing that waiting game I see better options right now.

For further details see:

Dow: Chemical Maker Struggles With Earnings Decline And Macro Headwinds (Downgrade)