MMM - Dow Inc.: A Long-Term Compounder Now On Sale

2023-06-02 12:26:10 ET

Summary

- Dow Inc., A.K.A. The Dow Chemical Company has been compounding its cash flows for over a century.

- The company is now selling at roughly 8x normalized earnings.

- As investors pile into technology businesses, I see Dow as an under-the-radar buy.

- I provide an analysis of Dow's five competitive advantages.

- In the decade ahead, I project returns of 14.5% per annum.

125 Years Of Compounding

The Dow Chemical Company was founded in 1897 by Herbert H. Dow. Now operating within Dow Inc. ( DOW ), the company converts hydrocarbon-based raw materials into chemicals, and eventually plastics and other materials. The company also produces, buys, and sells chemicals such as ethylene and propylene. The production of Dow's raw materials can be traced back to crude oil and natural gas. Despite being a cyclical business, the company's survived and thrived, compounding cash flows for over 125 years. There are three keys to Dow's enduring business model, let's discuss.

A Diversified Business Model

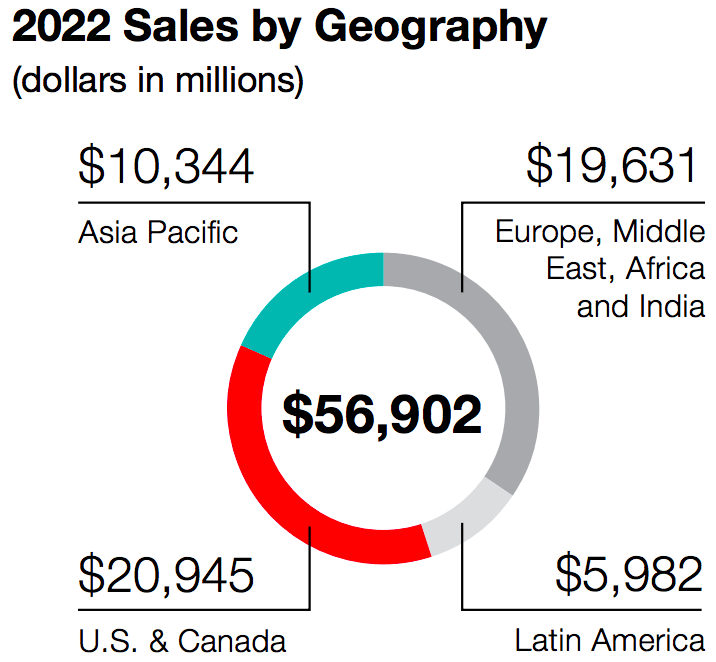

One of the keys to Dow's resilience is its diversified business model. Dow's operations are diversified across four continents (North America, South America, Asia, and Europe) giving the company exposure to multiple economies and multiple currencies.

{kind=link}

Dow manufactures for several different end markets including automotive, food packaging, construction, cosmetics, children's toys, telecommunications, sporting goods, agriculture, healthcare, and infrastructure. Many of these industries have limited sensitivity to economic downturns.

During the pandemic lockdowns of 2020, Dow's diversified business model and flexible CapEx spend allowed it to outperform competitors LyondellBasell ( LYB ), Eastman Chemical Company ( EMN ), and Basf SE ( BASFY ) on a free cash flow basis:

Dow breaks down its sales into three categories, with the largest being packaging and specialty plastics:

Sales By Operating Segment (Dow Inc 2022 Annual Report)

A Strong Balance Sheet

Prudent financial management has allowed Dow to survive brutal recessions even as competitors falter. Today, Dow has an exceptional balance sheet with $19 billion of current assets covering $10 billion of current liabilities. Dow has $14 billion of long-term debt, which is just 2.5x its average operating income over the past three years. All of this lends a hand in Dow's investment grade credit rating .

Five Competitive Advantages

The third key to Dow's enduring success is its plethora of competitive advantages. Dow Inc. has a substantial economies of scale position as one of the largest companies in the chemicals industry, reducing its cost per unit of production.

On top of this, new competitors face substantial barriers to entry, such as the enormous cost of building facilities, the need for significant R&D, depressed capital markets, and a lack of intellectual property (At the end of 2022, Dow Inc. had 26,300 active patents). ESG has caused old-age companies to become starved for capital. Investors have been buying up the IPOs of ESG friendly technology companies in recent years, increasing competition in an already popular sector. Meanwhile, the chemical industry receives less attention. This is good news for Dow Inc.; it likely means less competition and more sustainable profits.

Dow Inc. has more focused operations than competitors like Sinopec, Shell ( SHEL ), and Exxon Mobil ( XOM ). These competitors are primarily focused on upstream and downstream oil and gas, producing petrochemicals on the side. Dow, on the other hand, operates solely in the chemicals industry.

The company also sports a strong, 125 year-old brand name. The brand enables Dow to attract talented employees and new customers.

Lastly, North American chemical companies have access to very low-cost natural gas, which is used in the production of Dow's raw materials. Global competitors in Europe and Asia rely primarily on high-cost, oil-based feedstocks. This gives Dow Inc. an additional cost advantage as 72% of its long-lived assets are in North America.

Turbulent Times

2022 was a turbulent year for Dow Inc. There were lockdowns in China, conflicts in Europe, and consumer confidence crises in North America. In 2022, Dow took loses on Russia/Ukraine assets to the tune of $118 million. And, global currencies fell against the U.S. dollar, a net negative for Dow's sales. Q1 2023 was no better, with high energy (Input) costs and weak demand in Europe, a planned maintenance shutdown of the Sadara plant, and non-recurring licensing activity. Dow Inc. and competitor LyondellBasell Industries N.V.'s operating margins are thus at relative low-points in the cycle:

But, some of these negatives should reverse in the years ahead.

Why Dow Inc. Is Cheap

Tailwinds

Famed macro investor Stanley Druckenmiller recently announced he's shorting the U.S. dollar. Looking at the fundamentals, I think the odds are on Druckenmiller's side; the U.S. has a negative balance of trade, record high in government debt to GDP, and inflation rates that exceed the rates on treasuries. Dollar weakness is good news for Dow Inc.; 63% of Dow's sales are in geographies outside the U.S. and Canada.

China's reopening is also good news, as are the trends we see in artificial intelligence [AI], electric vehicles, and green energy. These futuristic build-outs will require more materials from companies like Dow Inc. Amazon's ( AMZN ) AI robotics and grocery store self-checkouts are just the beginning of AI build-outs that will require more plastics, as well as performance materials and coatings from Dow Inc. Dow may also be able to use AI to improve its manufacturing efficiency, through AI robotics, increasing margins.

Shareholder Remuneration

In recent years, Dow's management has done a terrific job. They've kept things simple, focusing on cost reductions. They have also returned a ton of cash to shareholders through both buybacks and dividends. The company substantially reduced its share count in 2022, increasing intrinsic value:

In the 2022 annual report , the company stated: " We have approximately $2 billion remaining on our latest $3 billion open share buyback program." And, Dow's dividend yield now sits at 5.70% as investors eye a hard landing in 2023.

Normalized Earnings

In the Q1 2023 earnings call , Dow's CFO said: "So I think a more normalized EBITDA for us is in that $9 billion to $10 billion range in a normalized macro." This is roughly what the company made in 2021 and 2022. Combined, the company had an average net income of $5.4 billion over these two years, and $5.6 billion of average free cash flow. Dow has been underspending slightly on CapEx, and is guiding toward $2.2 billion of CapEx in 2023.

Dow's Free Cash Flow in 2022, 2021, and 2020 (Bottom Line):

Operating Cash Flow, CapEx, Free Cash Flow (Dow Inc 2022 Annual Report)

In a recessionary environment, 2023 numbers could be much lower, but I believe the company's normalized earnings are approximately $4.5 billion ($6.36 per share). On a $35 billion market cap, that's a normalized PE of just 7.8x (A 13% earnings yield).

Long-term Returns

Over the next 10 years, I believe Dow Inc. is capable of growing its $4.5 billion of normalized earnings ($6.36 per share) at 4.5% compounded annually.

- Some of the tailwinds for Dow's growth are share buybacks, product price growth, and cost reductions. Over the very long-term (Say 30 or 40 years), the price of Dow's materials and chemicals should grow alongside inflation, a net positive for Dow's sales and profits. I expect modest product price growth in the decade ahead.

- Some headwinds for Dow's growth are forced investment in decarbonization and a substantial dividend obligation, resulting in little cash available for reinvestment.

In the decade ahead, I estimate compound annual returns of 14.5% for Dow Inc.:

| Normalized EPS (Current) |

| $6.36 |

| Dividend (Current) |

| $2.80 |

| Compound Annual Growth Rate |

| 4.5% |

| Year 10 EPS |

| $9.88 |

| Terminal Multiple |

| 12.5x |

| Year 10 Share Price |

| $123.50 |

| Annualized Return (Dividends Reinvested) |

| 14.5% |

Note: This is a base-case estimate.

Risks

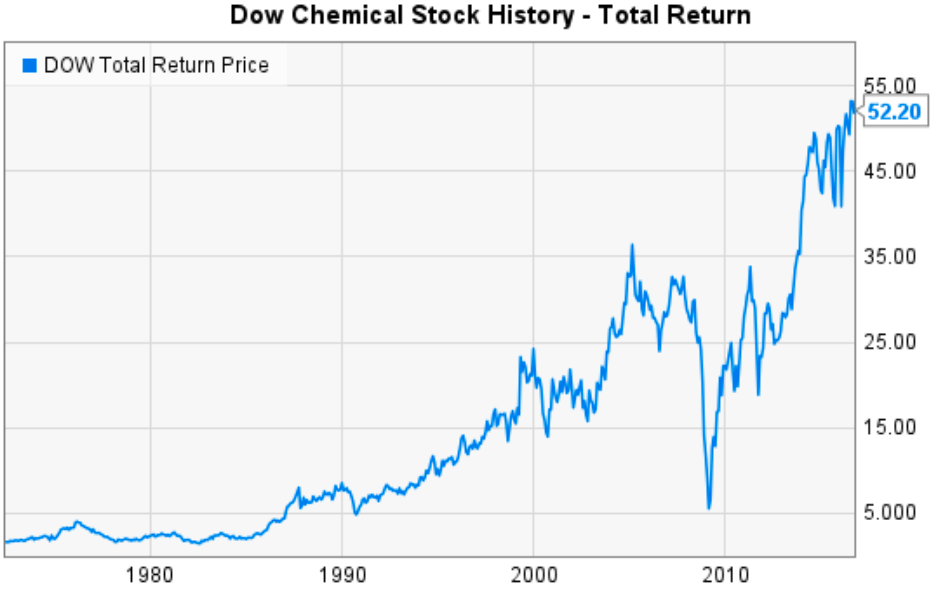

Terrible recessions can cause economic activity to grind to a halt. Faced with low demand and high input costs, Dow's cash flows may temporarily falter. This caused a panic in The Dow Chemical Company's share price in 2009:

{kind=link}

Dow's management handled the GFC quite well, and current management has the company's balance sheet is in great shape. Still, I would not rule out the possibility of a dividend cut in a bad recession (2009 Example provided below). This would be at management's discretion as the company has ample working capital. I believe there is a chance free cash flow drops significantly below the current dividend obligation over a one year period; this is a short-term volatility risk as a cut would likely result in selling pressure. Other analysts have claimed the dividend is secure.

Below are The Dow Chemical Company's net income and free cash flow figures from 2007-2009 :

| ____________ |

| 2007 |

| 2008 |

| 2009 |

| Net Income |

| 2,887 |

| 579 |

| 336 |

| Free Cash Flow |

| 2,409 |

| 2,435 |

| 392 |

While the company eventually recovered and surpassed its 2007 numbers, you can see that Dow Inc is a cyclical business. Many analysts have a neutral rating on Dow, citing global economic woes.

On fines and lawsuits, Dow has far less risk than a company like 3M ( MMM ) in my opinion. This is because 3M is so heavily involved in consumer goods where lawsuit risks are high, meanwhile, Dow is typically providing the chemicals and materials to make goods. However, Dow has faced minor lawsuits in the past such a securities lawsuits, pollution fines/lawsuits, negligence lawsuits, and price fixing lawsuits, the largest being a $835 million settlement in 2016 for polyurethane price fixing.

Irrational competition/price wars is another risk. Competitors BASF SE and LyondellBasell are looking to expand capacity. If supply should exceed demand, industry profitability could be impaired. Thus far, Dow's competitors have remained quite rational in terms of maximizing profitability; but, in the unlikely event of a price war, profitability could be impaired.

Excessive regulation could hurt Dow's business. Governments have to walk the thin line between chemical shortages and environmental initiatives. Regulate too much, and chemical companies will shut down production. Dow's European assets may require more government support. But, the long-term trend has been more regulation. While I do not know the probability of future events, excessive environmental restrictions could cause compliance costs at Dow Inc. to increase.

In Conclusion

Dow's shares trade at just 7.8x my estimate of normalized earnings. The cheap valuation can be largely attributed to a gloomy economic outlook, as well as the ESG trend. Meanwhile, prudent financial management, a diversified business model, numerous competitive advantages, and organic price growth have led to 125 years of favorable economics for Dow Inc. (Previously the Dow Chemical Company). A recession may cause short-term pain. But, adopting the mentality of a business owner, Dow Inc. looks like a strong buy. I expect the world and shareholders to benefit from Dow's essential products and manufacturing excellence for decades to come.

Until next time, happy investing.

For further details see:

Dow Inc.: A Long-Term Compounder, Now On Sale