AWK - Down 20% YTD American Water Works' Dividend Growth Case Appears Compelling

2023-10-03 11:00:00 ET

Summary

- American Water Works' stock has declined by about 20% year-to-date, following the trend of most water stocks.

- Water stocks are typically stable and recession-proof due to the essential nature of water services.

- American Water Works has a strong track record of dividend growth and robust future growth prospects, making it an attractive investment opportunity for those seeking growing income.

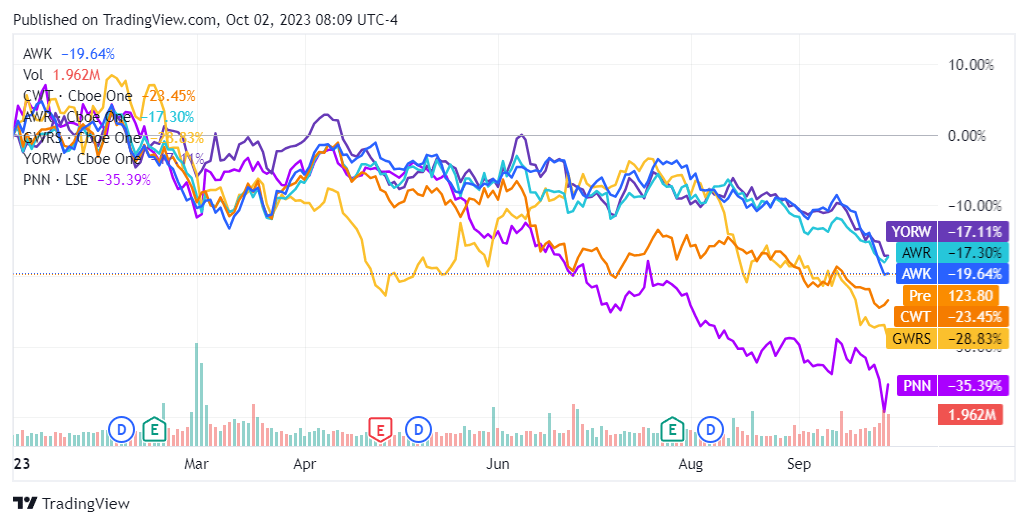

Shares of American Water Works ( AWK ) have declined by about 20% year-to-date. The stock has followed the trend of most water stocks, which have also declined significantly over the same period.

Water Stocks YTD Price Action (Seeking Alpha/TradingView)

{kind=link}

The decline in water stocks can be largely attributed to a diminishing interest among utility stocks overall, particularly in the context of a rising-rates environment. However, if you have followed water stocks for a while, you also know that they rarely dip significantly or trade at a discount, in general.

Why? Well, water is a basic need, and that makes water utilities remarkably stable, even when the market is doing its rollercoaster thing. Think about it – no matter what's happening in the world, people still need clean water, and companies in the water business are there to provide it.

This essential nature of their services makes water stocks pretty much recession-proof. Because of this, water stocks don't often go on sale, but when they do during market dips, it's like finding a great deal on something you know you've always wanted to have exposure to.

Combined with the fact that American Water Works' dividend growth prospects appear very strong, investors could see the stock's recent dip as a compelling opportunity to acquire some shares.

American Water Works: A Short Overview

American Water Works Company, founded in 1886 and headquartered in Camden, New Jersey, is by far the largest publicly traded water and wastewater utility company in the United States. The stock trades with a market cap of $24.1 billion, and for context, the second highest-valued water utility is Essential Utilities ( WTRG ), with a market cap of about $9.1 billion .

Dedicated to delivering essential services, American Water serves a notable customer base, extending its reach to over 15 million individuals across 46 states. The company's regulated portfolio encompasses an extensive network comprising 53,500 miles of pipeline, 490 water treatment plants, 175 wastewater facilities, 1,110 wells, and 73 dams.

Beyond its domestic operations, American Water plays a pivotal role in serving the needs of the U.S. government and military, catering to 17 installations with water and related services.

Robust Growth Track Record & Future Growth Prospects

As I mentioned, American Water Works' dividend growth prospects appear very strong. But before we jump into the dividend, it's important to explain what has powered the company's robust dividend growth track record and why this trend is likely to remain in place moving forward. Essentially, let's look at the company's growth track record, as well as its future growth prospects.

Past Track Record

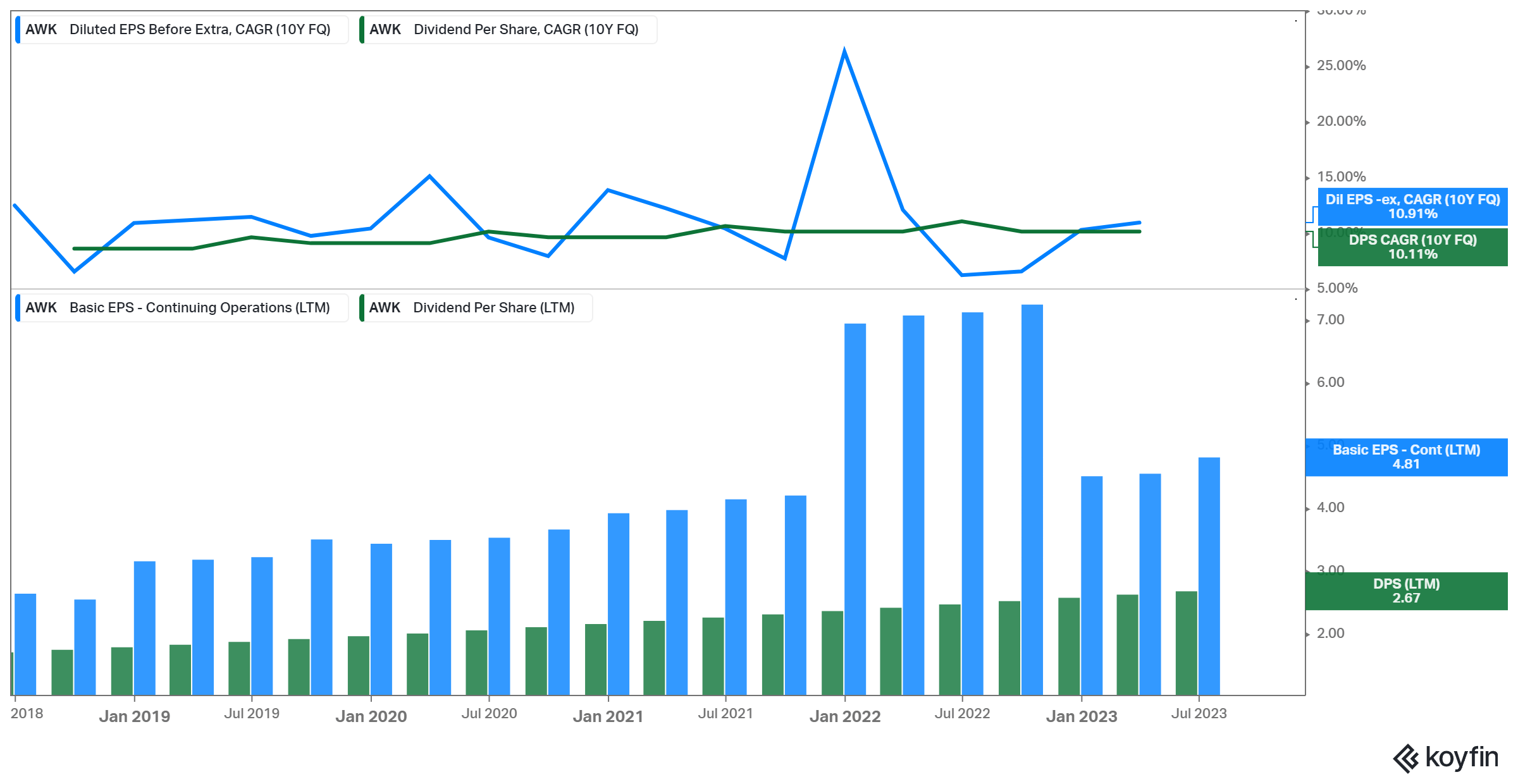

Over the past decade, the company has consistently delivered impressive compound annual growth rates of 10.9% and 10.1% in earnings per share and dividend per share, respectively, demonstrating stability with minimal fluctuations. Notably, the company has increased its dividend every year for the past 15 years.

American Water Works' EPS & DPS 10-Year CAGRs (Koyfin)

{kind=link}

This success is largely attributed to the robust business model of American Water Works, leveraging the indispensable nature of water for residential, commercial, and military purposes. By tapping into this essential demand, the company has expanded its distribution network and operations while minimizing risks.

Moreover, the company has made significant progress in securing general rate cases. A prime example is evident in its latest Q2 results , where the company provided a comprehensive update on its standing. Management highlighted that year-to-date, the company has secured approval for an additional $273 million in annualized revenues from general rate cases for the year 2023. Moreover, there's an approved and effective $67 million in additional annualized revenues from infrastructure surcharges in 2023.

Currently, the company is actively pursuing general rate cases in four jurisdictions and has submitted applications for infrastructure surcharges in one jurisdiction, representing a combined annualized revenue request of $155 million. This strategic growth initiative aligns with the standard practices of water utilities, and American Water Works adeptly leverages it to bolster its financial performance.

Furthermore, beyond the factors mentioned earlier, American Water Works enjoys a steady, naturally occurring expansion driven by the increasing population within its service areas. Remarkably, in the previous fiscal year, the company accomplished a historic milestone with the addition of 70,000 new customer connections . This achievement was realized through a synergistic blend of organic population growth and the strategic acquisition of 26 diverse, regulated water and wastewater systems.

The great thing about acquisitions is that the company can usually achieve efficiencies via cost synergies and economies of scale. Recent acquisitions, such as the micro acquisition of The Village of Broadlands water system and the proposed acquisition of Audubon Water Company , highlight the company's commitment to expanding its ecosystem. Finally, by late 2024, the company expects to close the acquisition of privately owned- Appalachian Utilities.

Future Expectations

Due to the consistent patterns in water consumption, population expansion, rate adjustments, and strategic acquisitions, American Water Works' leadership has successfully delivered one of the most accurate and reliable forward-looking projections available in the equity market.

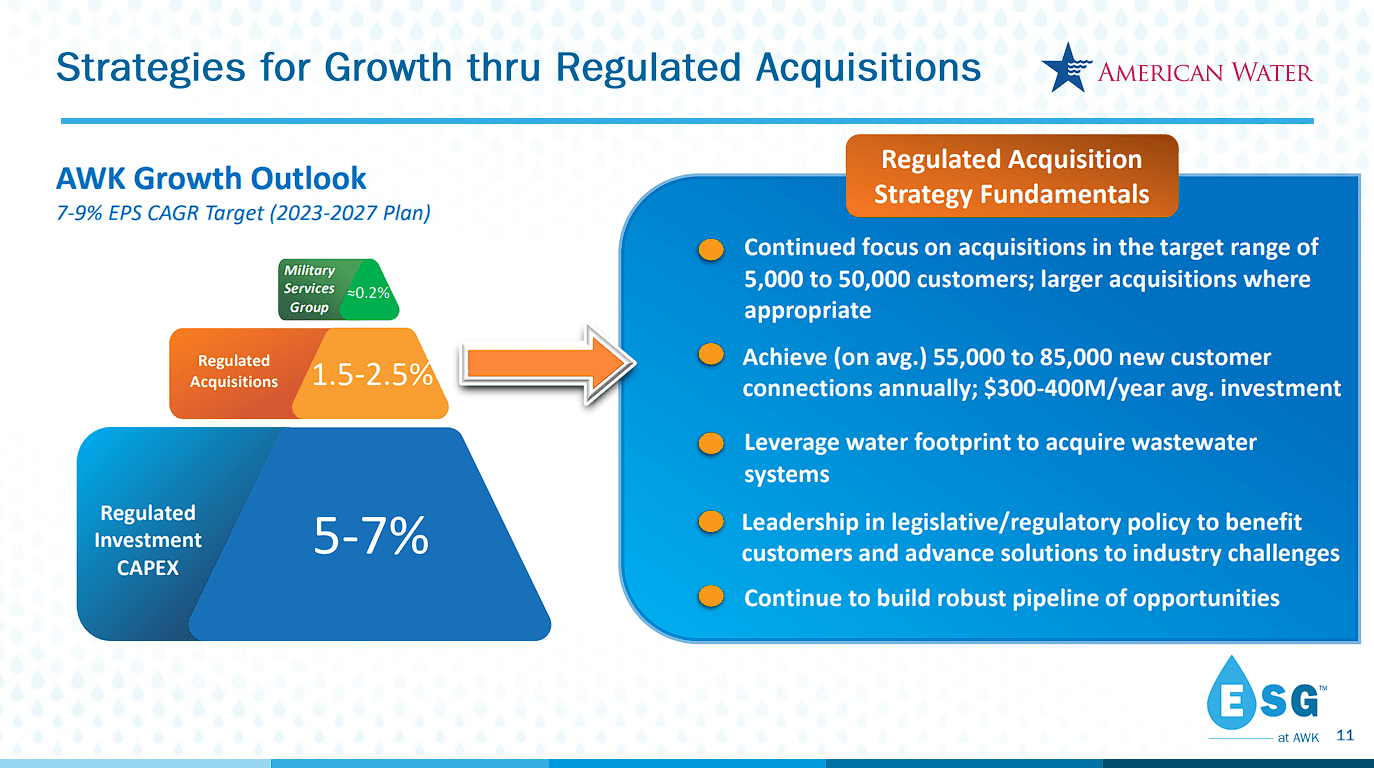

Notably, the company anticipates a robust compound annual growth rate of 7% to 9% in earnings per share until 2027. This growth is underpinned by a 5% to 7% surge attributed to regulated investment capital expenditures, a 1.5% to 2.5% increase from regulated acquisitions, and approximately 0.2% growth stemming from military services.

AWK's EPS Growth Outlook (August Investor Presentation)

{kind=link}

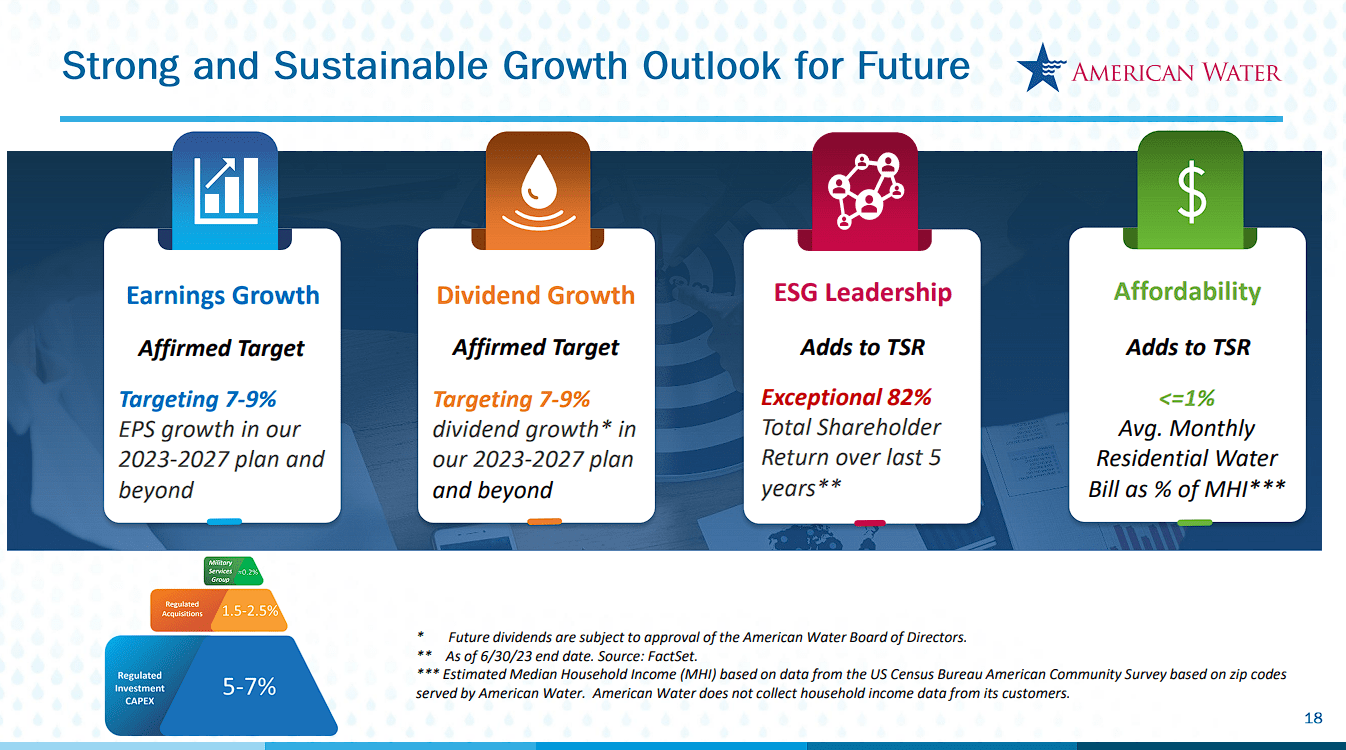

In line with this outlook, management also anticipates growing the dividend at a rate of 7% to 9% per annum over the same period.

AWK's DPS Growth Outlook (August Investor Presentation)

{kind=link}

This level of specificity in growth estimates over an extended period is rare among companies and sets American Water Works apart. The unparalleled visibility into its growth prospects distinguishes it significantly from your average stock out there. This level of assurance is invaluable to dividend growth investors, as it provides them with confidence in the sustained and predictable trajectory of their income over an extended duration.

The Valuation & The Takeaway

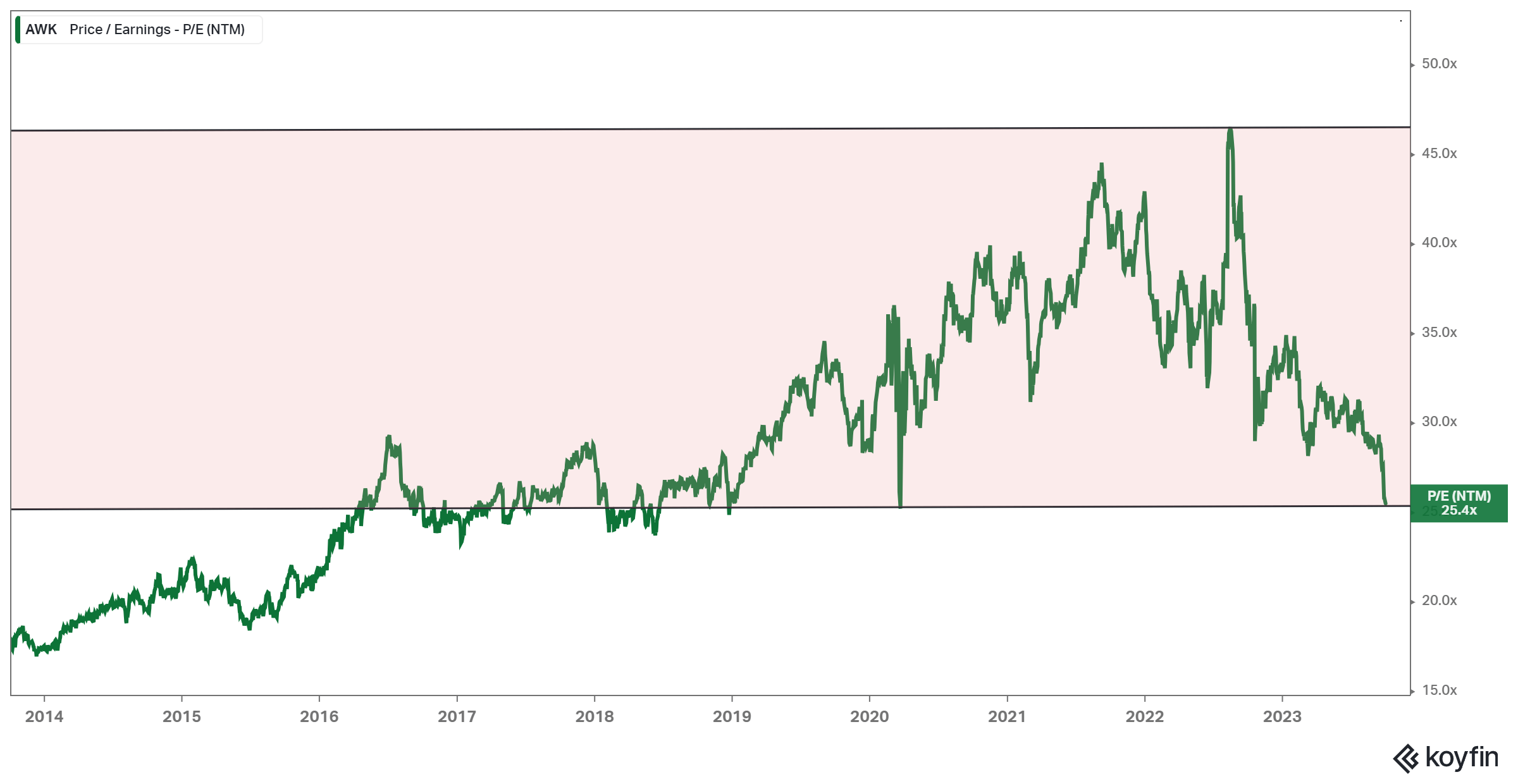

As I mentioned at the beginning of this piece, water stocks have historically traded at premium valuations due to their one-of-a-kind qualities. American Water Works has been no different. At one point, shares ended up trading close to 45 times their forward earnings.

The ongoing valuation compression that all water stocks have experienced, combined with continuous underlying EPS growth from the company, has resulted in the stock's forward P/E having declined to a much more reasonable 25.4X.

AWK's Historical Valuation (Koyfin)

{kind=link}

One could argue that this is still a relatively rich multiple, especially given that the stock's yield, even after the stock's decline, is hovering close to 2.3%. This figure may not evoke much enthusiasm in a landscape where the federal funds rate exceeds 5%.

That said, I believe that it is also quite unlikely that shares will see a further valuation compression from here. This is for two key reasons.

Firstly, the company's multi-year outlook is not only strong (8% EPS & DPS growth at the midpoint), but it also provides visibility several years into the future. This alone commands a premium versus a company whose similar growth prospects would only be backed by Wall Street analysts' projections.

Secondly, the aforementioned utilities that come attached to a water stock remain in place. It's one thing to project high-single-digit growth from a cyclical company whose future financials are susceptible to multiple factors, and it's another thing to have such projections supported by a company whose business model is highly predictable and recession-proof in a highly regulated industry (a moat).

Thus, while the current dividend yield may appear modest, there is a convergence of a robust long-term outlook and solid growth rates. Coupled with the company's inherent qualities, its investment case presents a compelling proposition for those seeking predictable dividend growth.

For further details see:

Down 20% YTD, American Water Works' Dividend Growth Case Appears Compelling