DRDGF - Downgrading Sibanye Stillwater To A Hold Amid Rising Risk Premiums

2023-05-25 16:32:27 ET

Summary

- Sibanye Stillwater Limited misfortunes seem endless as additional obstacles have slowed its PGM production. Moreover, exogenous features are intensifying.

- Although we anticipate higher PGM prices and a sector-based recovery, we have decided to exclude Sibanye from the pack as its stock is in vulnerable territory.

- Value can be unlocked at Keliber with a potential IRR of 27%, and Sibanye's stake in DRDGOLD is paying dividends.

- Nevertheless, a high country risk premium, an undesirable forward book value, and continuous internal obstacles lend us various reasons to downgrade Sibanye Stillwater Limited stock.

In spite of a minor recovery among South African Platinum group metals ("PGM") stocks, Sibanye Stillwater Limited ( SBSW ) fortunes have continued to erode as it has experienced additional setbacks within its U.S. PGM segment and ongoing external pressure in South Africa.

In a recent 13-F filing , it was revealed that Michael Burry added 800,000 Sibanye Stillwater shares to his portfolio, aligning with our previous outlook. However, today we change our stance on Sibanye and downgrade the stock to hold as we believe it is a "negative" outlier among the available PGM stocks.

Let us delve into a more detailed discussion about Sibanye Stillwater's recent events.

Bullish Features

Turnarounds and New Value

A foundation for a bullish outlook on Sibanye relates to the fact that it can be considered as a recovery play. As mentioned in our previous coverage and as observable in the company's latest half-year report, Sibanye has faced numerous internal and exogenous challenges in the past year, leading to an exponential drawdown in its stock price. However, the argument remains that expected returns and past events tend to be inversely related, especially when past events were non-core.

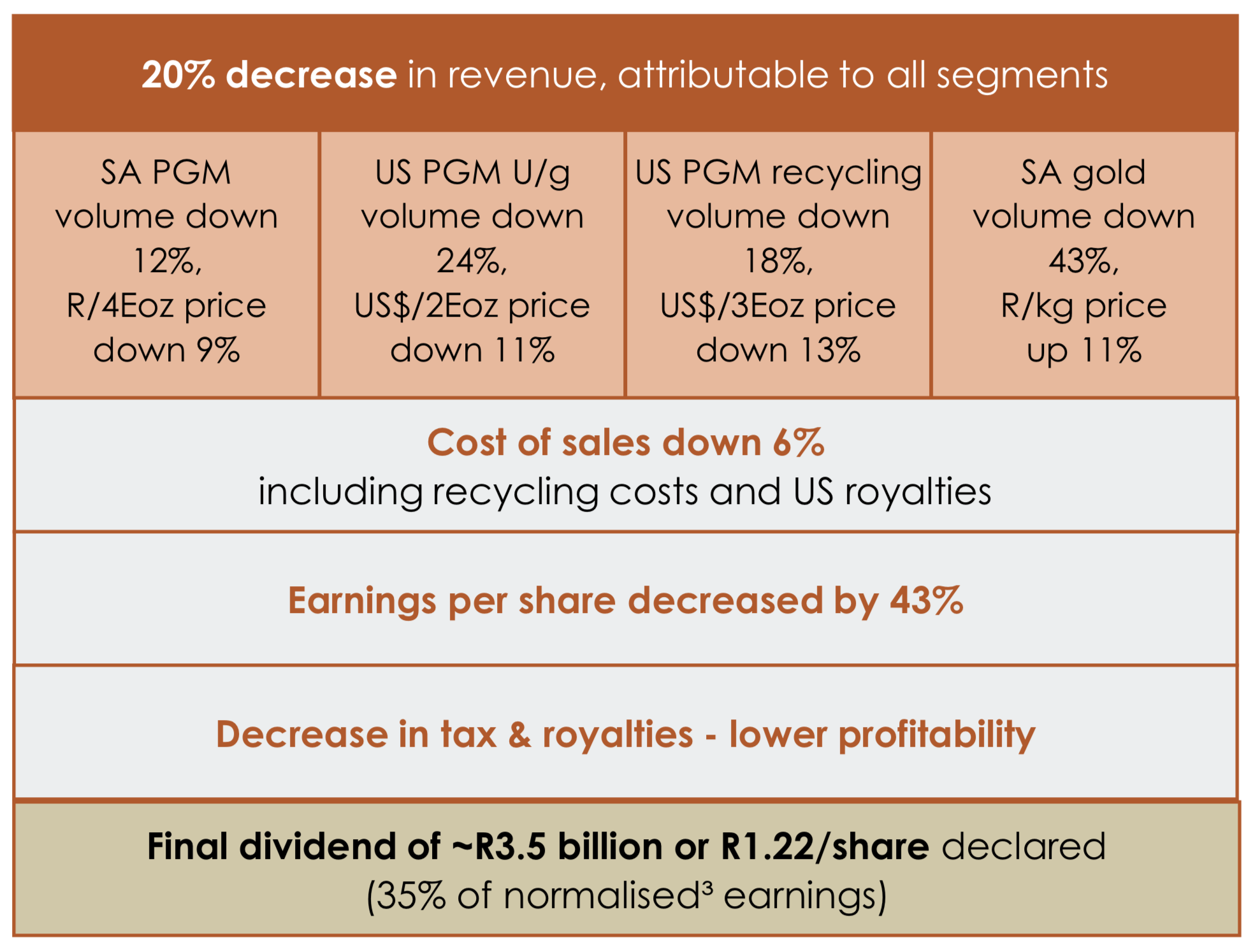

Production Summary (Sibanye-Stillwater)

{kind=link}

We mentioned in our previous analysis that Sibanye's U.S.-based operations likely recovered after a flood in Montana disrupted its regional PGM mining endeavors. However, our prediction was premature as no recovery was reflected in the firm's latest production report, as U.S. PGM showed a severe decrease in half-year production and a rise in all-in-sustaining costs. Moreover, the firm's West Mine in Montana suffered from a shaft incident earlier this year, leading to Sibanye lowering its regional PGM guidance to 460K-480K oz from prior guidance of 500K-535K oz.

It may seem like Sibanye's U.S. PGM operations are doom and gloom. However, we still consider the properties' unfortunate events in the past year as non-core and believe investors will rationalize soon by pricing long-term cash flow potential instead of short-term frictions.

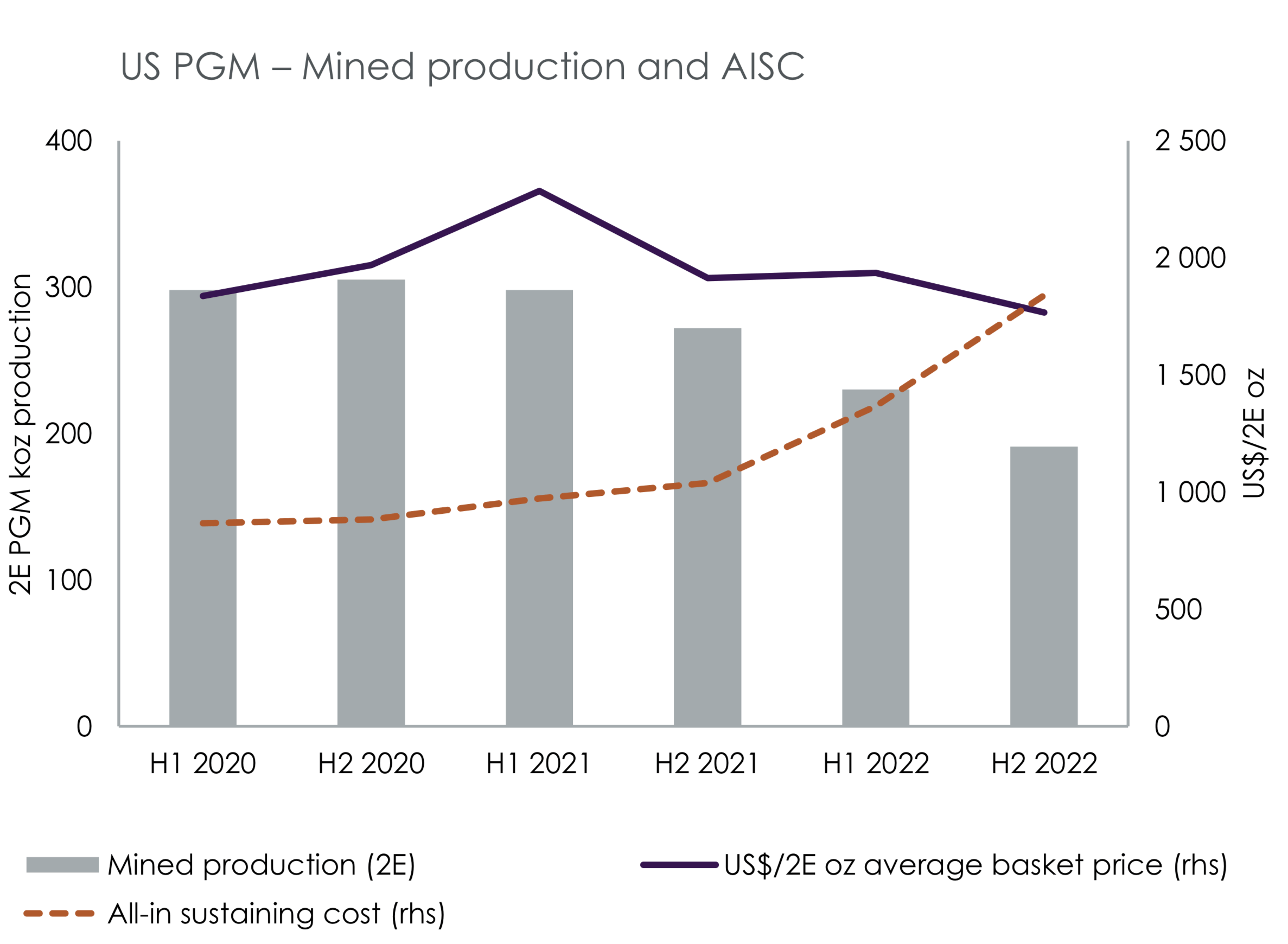

U.S. PGM Mines (Sibanye-Stillwater)

{kind=link}

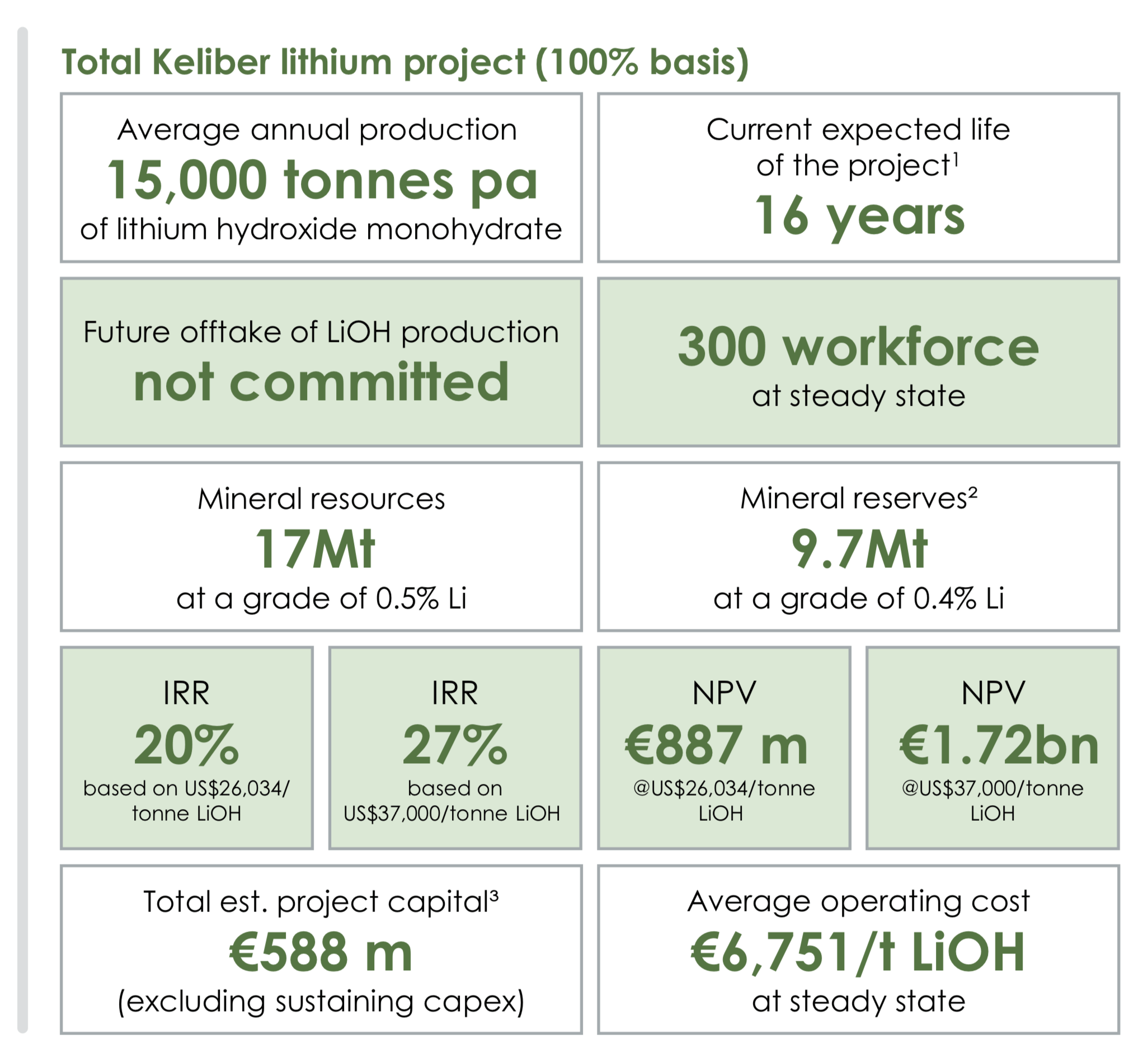

Furthermore, a concise outlook of Sibanye's new Keliber lithium project in Finland shows encouraging signs. In our view, an internal rate of return worth 20% to 27% and a mine life of 16 years is lucrative and will add financial value to the firm. In addition, Sibanye could recognize key synergies from the project, such as intertwining supply chains in its Euro area projects and lowering its bank-financed cost of debt (because of a higher ESG rating).

Keliber Mine Forecast (Sibanye-Stillwater)

{kind=link}

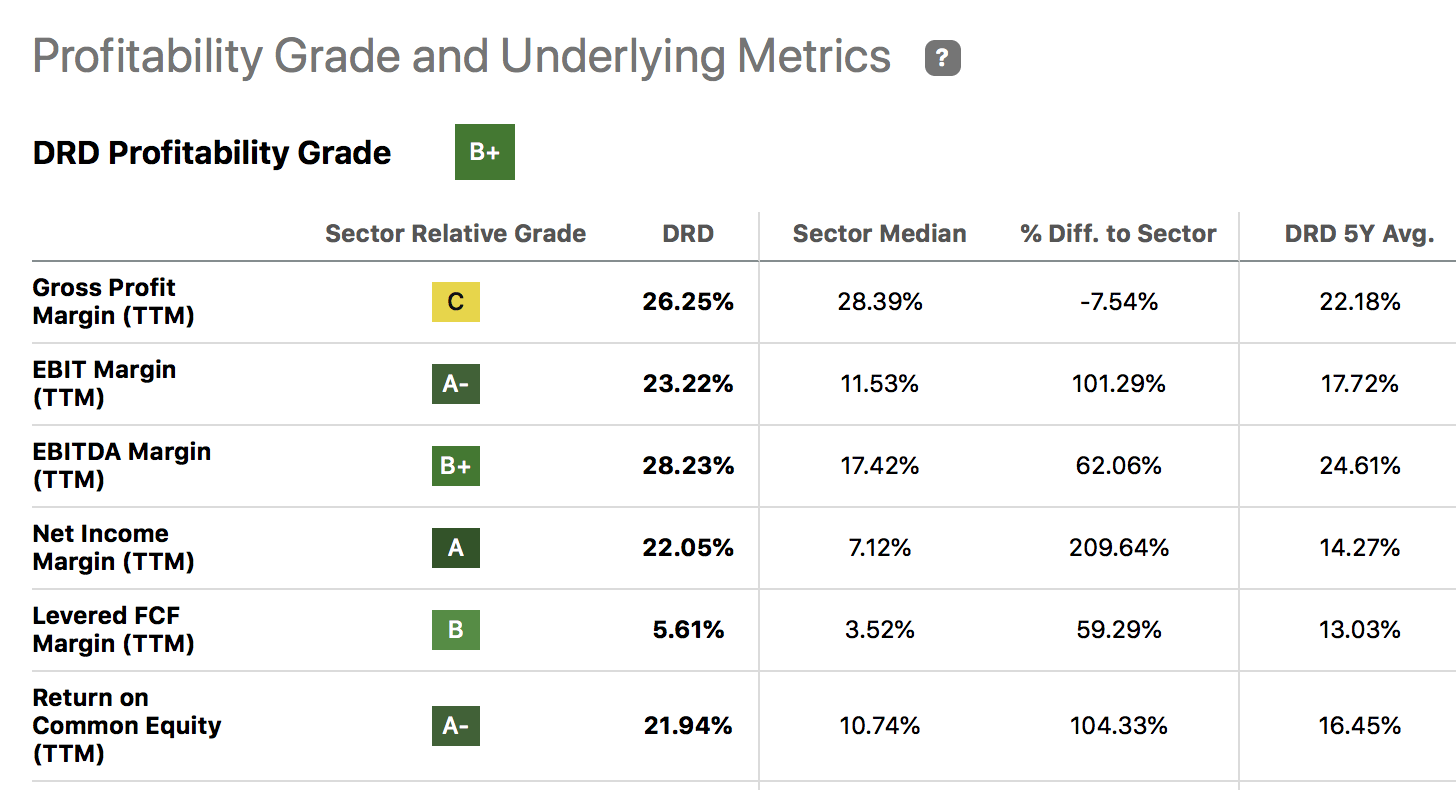

Lastly, Sibanye's 50.1% ownership in DRDGOLD Limited ( DRD ) might provide it with critical momentum. DRD has key exposure to the tailings business and gold prices, which are both headwinds in today's climate. Our baseline for this is that gold prices may continue to proliferate as U.S. dollar tail risk is at a multi-decade high, and gold mines could expand in the coming quarters as they realize above-average profits.

DRDGOLD Common-Size Profit Margins and Cash Flows (Seeking Alpha)

{kind=link}

Challenges

Although we have spoken of South Africa's challenges rather frequently, it cannot be stressed enough how much of a risk it is to invest in South African equities in today's climate. Sure, many might argue that most mining jurisdictions are unsafe and struggle with grid issues. However, it must be highlighted that these issues are a more recent phenomenon in South Africa, meaning market participants never priced such matters before, and higher risk premiums are due to send baseline stock valuations downwards.

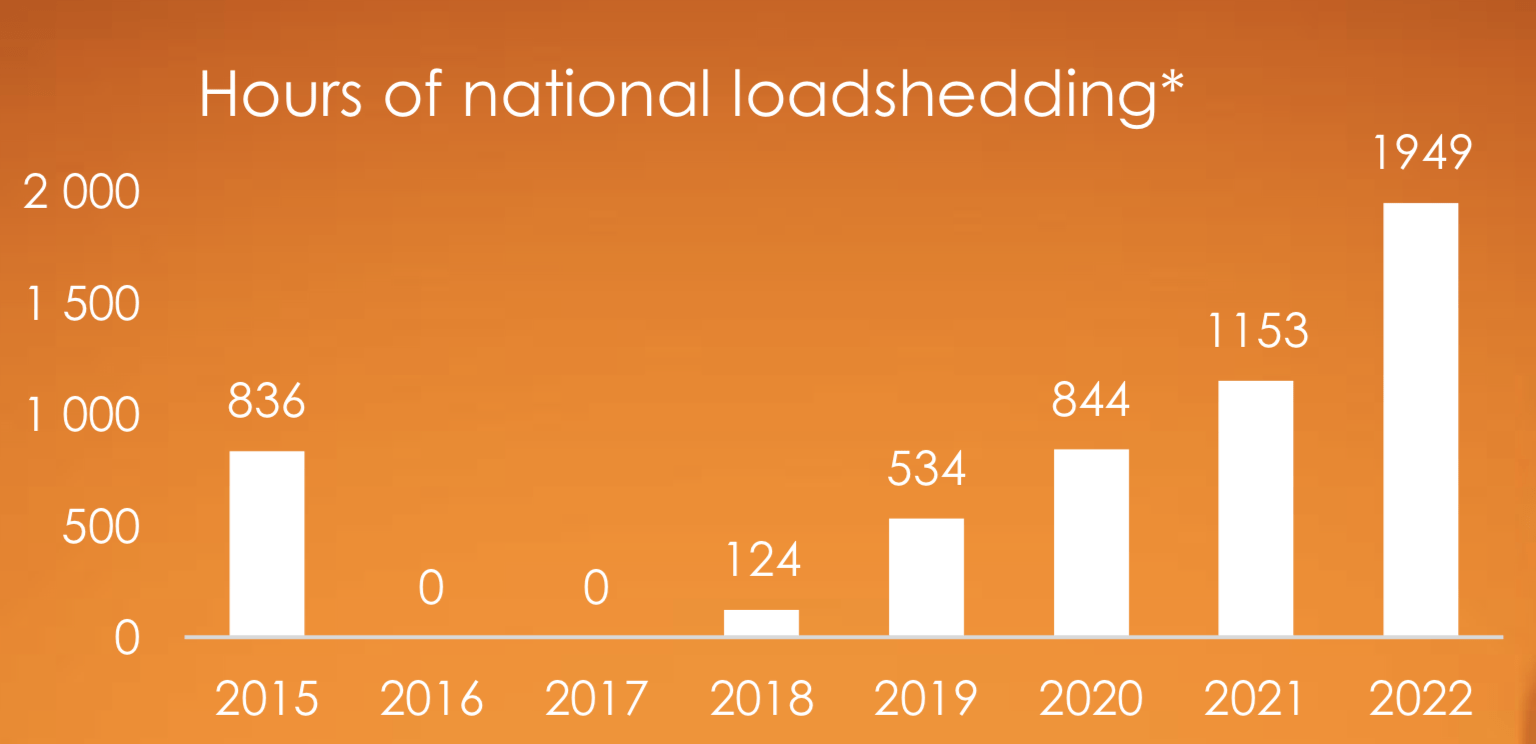

The diagram below illustrates the hours of national loadshedding in the country, which will only exacerbate, in our view. Higher PGM prices might realize due to a reduction in South Africa's lower output. Yet, we do not see that as a savior to Sibanye's income statement, as mining houses operate with extensive fixed costs, and Sibanye generally hosts deep mines.

South African Electricity Problems (Sibanye-Stillwater)

{kind=link}

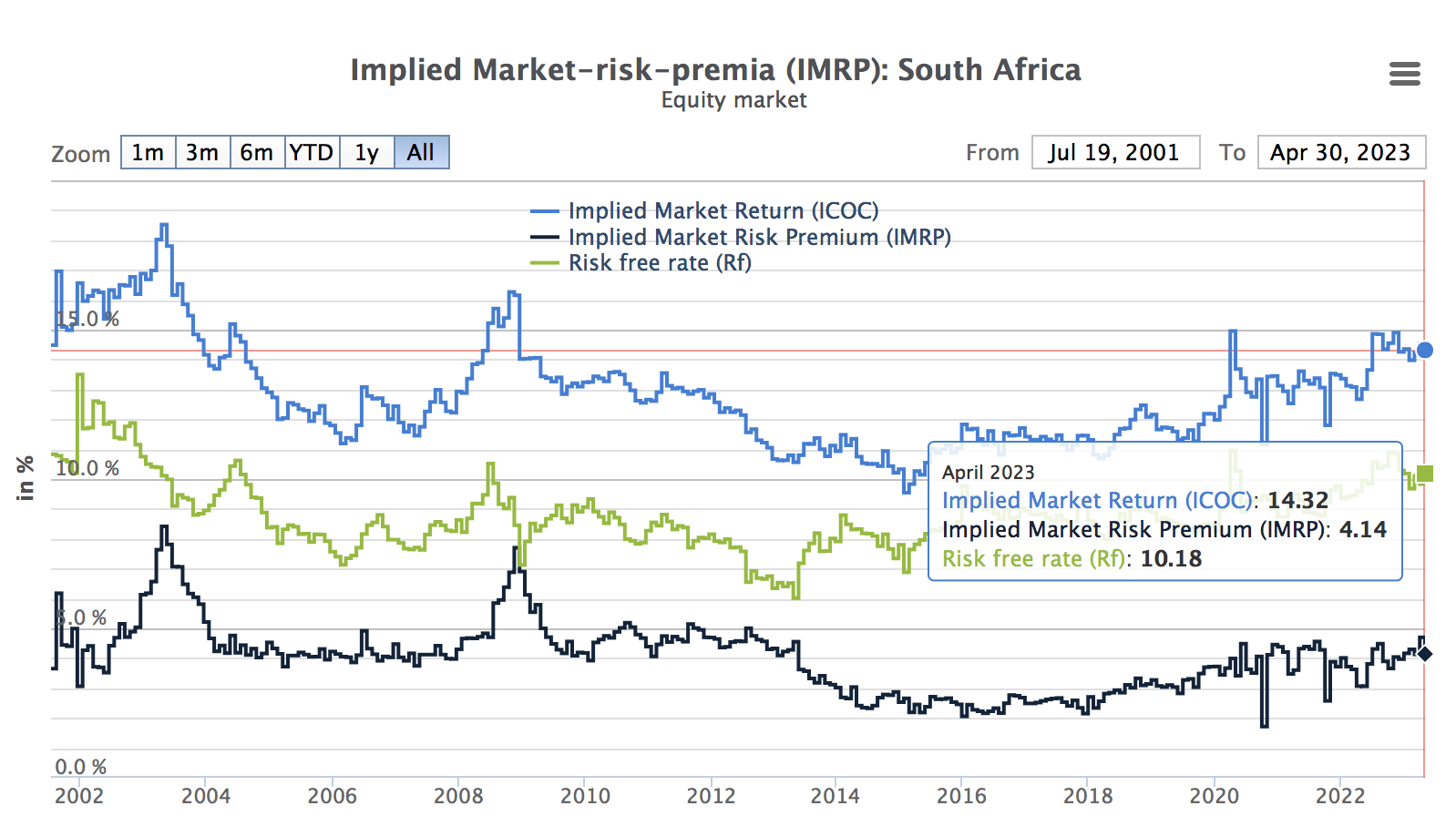

Furthermore, we expect country risk premiums in South Africa to rise substantially in the next twelve months as the 2024 national election looms. The national election is considered the most uncertain since the 1994 election, as trust in the ANC has dissolved. Additionally, populist politics from the Economic Freedom Fighters (a Marxist regime) has gained ground. And on the other end of the spectrum, the possibility of a minority coalition is not out of the question.

In basic terms, South African politics is a mess, and investors are likely to raise their country risk premium until matters are clearer. An interesting piece about a prominent investment fund founder, Magda Wierzycka, outlines the country's risk and the possibility that South Africa might already be a failed state; click on this link to visit the article.

South African Risk Premiums (market-risk-premia.com)

{kind=link}

To summarize, we think risk premiums on South African stocks are very high, and investors are likely to price most of them. Yes, Sibanye is listed as an American Depositary Receipt on the NYSE; however, traders will likely short the ADR if the South African-based stock declines to take advantage of an arbitrage opportunity.

Investor Return Prospects

From a total return vantage point, Sibanye provides lucrative prospects as it pays a substantial dividend. Additionally, the stock's most recent drawdown allows investors to lock in a substantial income-based return.

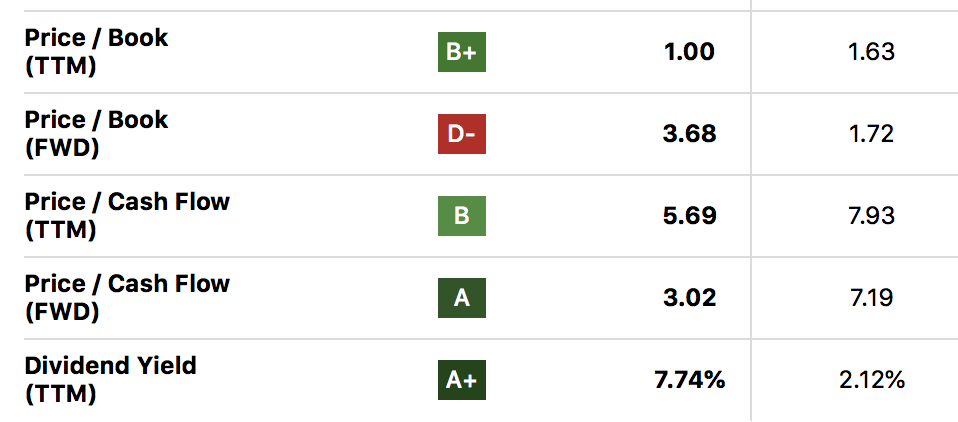

However, on the downside, Sibanye is an incredibly volatile stock. If the stock's recent downside had to reoccur, the asset's dividend benefits might be irrelevant. Moreover, the company's forward price-to-book ratio spells trouble as lower output and a lower asset base valuation might come to haunt the company's investors.

SBSW Valuation (Seeking Alpha)

{kind=link}

Final Word

Although a case can be made for a recovery opportunity, Sibanye Stillwater Limited's ongoing struggles have caused principle-agent conflict, leading to further drawdowns in its stock price (since our preceding analysis). Based on our outlook, there is a reasonable basis to conclude that Sibanye will be an underperformer in the coming quarters, leading to us downgrading Sibanye Stillwater Limited stock to a Hold.

For further details see:

Downgrading Sibanye Stillwater To A Hold Amid Rising Risk Premiums