NVMI - DQ Is A Deep Value Opportunity Before Earnings

2023-08-01 19:04:00 ET

Summary

- DQ is currently trading at a large discount to its intrinsic value.

- Relative to its peers DQ is severely underpriced.

- DQ's revenue growth has been impressive since 2018 and even if profits fall DQ will be severely undervalued.

Daqo New Energy Corp. ( DQ ), a leading Chinese polysilicon manufacturer, has a sharp focus on producing high-purity polysilicon, Daqo DQ plays a crucial role in the solar photovoltaic (PV) industry, supplying this vital raw material to solar cell and module manufacturers worldwide. Armed with long-term supply contracts, Daqo enjoys a stable revenue stream, shielded from the fluctuations that often plague the market. As the solar industry continues its ascent, DQ stands to reap the rewards of its expansion efforts and increasing production capacity. I think current negative sentiment has created an opportunity to buy shares at a significant discount.

Daqo's share price has had a rough start to 2023 along with many other companies in China. I believe that DQ has been unfairly punished and that its shares are significantly undervalued.

DQ shares lost 36% this year as headwinds and a polysilicon glut have caused concern for its future prospects. Predictions of falling revenue and falling profits have directly impacted the company. Combine this with the current attitude regarding China’s economic recovery and you get a perfect storm. Shareholders that bought into the growth have been punished.

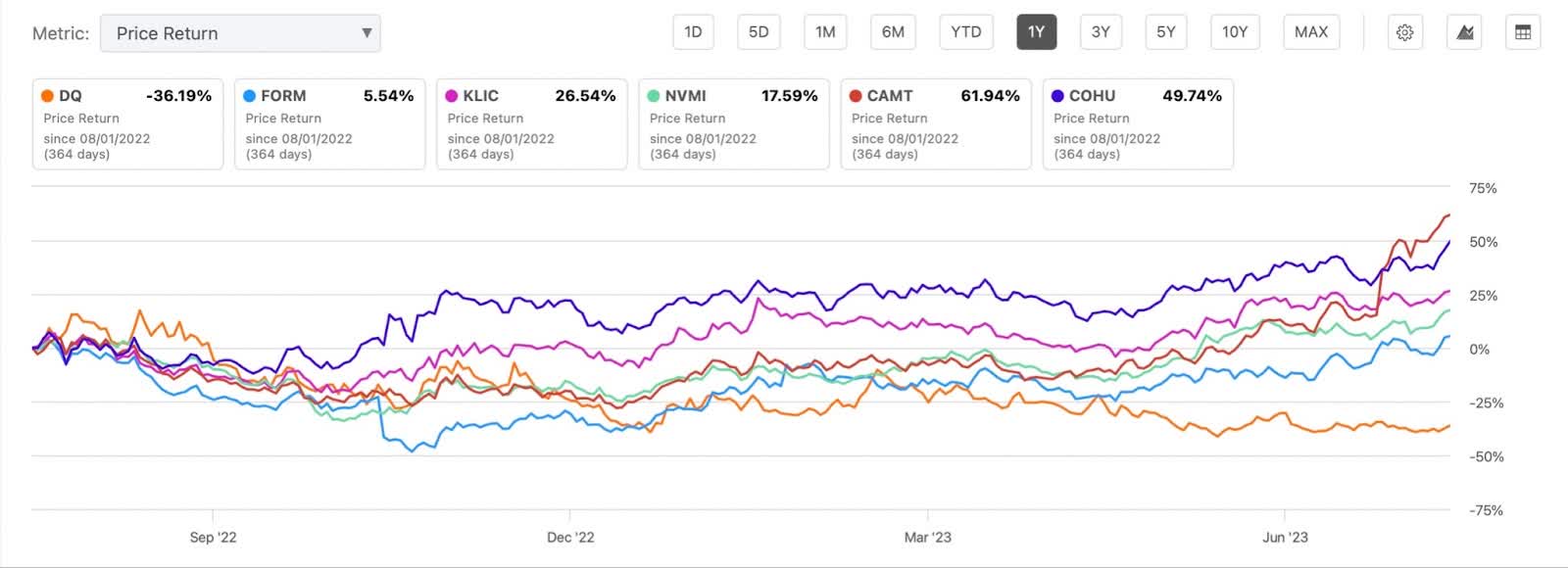

The 1 Year Chart

{kind=link}

Despite all of the negative sentiment, DQ’s competitors have done quite well this Year.

{kind=link}

In fact, all five of DQ’s closest competitors have seen strong returns on their share price.

Price Return DQ and Peers (Seeking Alpha)

{kind=link}

DQ’s negative returns on share price stand out. DQ’s -36% one year return definitely lags far behind CAMT’s 61% return and COHU’s 49% year to date.

CAMT now trades at a PE of 27 and COHU currently trades at a PE of 21 while DQ trades at a PE of 2.5. DQ clearly does not trade anywhere near its highest priced competitors.

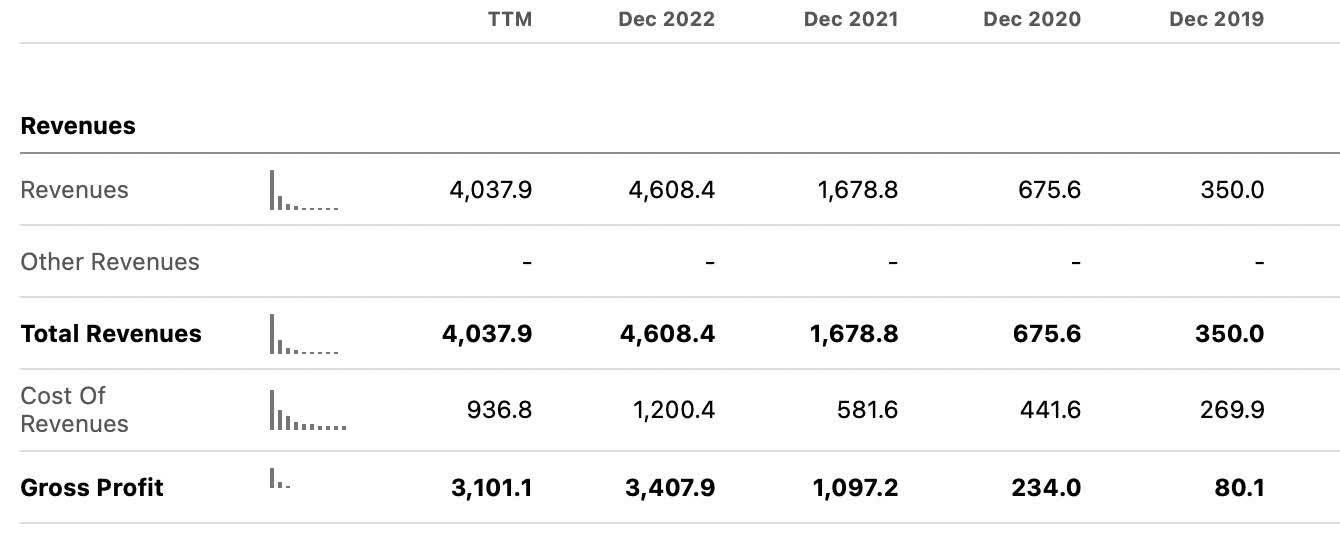

Allegedly a polysilicon glut as discussed here has caused DQ to suffer, but Daqo has remained profitable and grown earnings. Revenues have also increased dramatically since 2019. In 2019 DQ had revenue of $350 million, and now in 2023 they should report over $4 billion in revenue. The chart below shows how much revenue has grown.

{kind=link}

With DQ’s earnings report coming soon in August of 2023, I expect to hear some good news. I believe that this combined with the current improvement in sentiment towards companies in China could provide a large move after earnings.

Considering the current discount to its peers, we believe that DQ is worth over $100 a share. At Pink Sands, I use a proprietary methodology using qualitative and quantitative data. In this case, our qualitative data and quantitative data helped me determine a reasonable PE range with which to value a company.

The primary reasoning for our current target is that we believe that DQ should have a PE closer to that of its competitors. There are factors such as leadership, growth and revenues that make us create a range of possible values. An important factor in assessing DQ’s current value was utilizing a comparable company analysis which showed DQ’s severe undervaluation.

Although this year might be a slight slowdown, DQ’s ability to create low-cost products has been an advantage that should continue and the need for solar options and implementation of solar technology is only increasing. Considering the limited shelf life of these materials means that continued production will be necessary. DQ should be able to meet product demand at lower costs than its competitors creating a virtuous cycle in the future.

For these reasons, I believe a fair PE for DQ currently would be between a 7 times multiple and a 14 times multiple. This was modified downwards because of country risk and geopolitical risk. If DQ were located elsewhere and still reporting the numbers it does, we believe the company would be worth way more.

I believe this gives us a fair value range of between $105 and $210 per share. This wide range in values reflects the uncertainty currently in solar markets and the economy in China. Even if earnings drop, we believe the company is worth way more than the current price. I also believe that DQ should also receive a better multiple then it is currently receiving because it is still in an overall growth industry. DQ also has advantages over its competitors.

A way more conservative estimate could put DQ at a four times multiple which would still give us a value of around $60 which compared to its current price of $38 presents a large discount. I believe the margin of safety is quite large currently in DQ and this is what creates the best deep value opportunities.

So that you better understand my methodology it is important to note that I am not solely using PE values to create potential values. I am using sentiment and market dynamics to predict what I believe will be the correct PE in the near future. The method is multimodal but I am simplifying it to its most basic elements for the sake of article length and the proprietary nature of my methodology. I believe that being generally right is way more important than being precisely wrong. I often see people use precision as a measure of validity when there is no correlation between the two.

Risks

Government quotas desiring local solar manufacturing could impact exports. We believe the geopolitical risk to be the biggest risk to DQ. Because DQ is located in China that carries significant country risk and currency risks as well. This is why I am comfortable with the lower range of my targets. The solar technology field is highly competitive and of national interest. This could cause unforeseen regulation and market issues. Daqo as a company also needs to demonstrate that it will continue to grow profits or it will likely appear to be a value trap instead of a value. We should all learn a lot at the next earnings call on August 3rd .

Conclusion

I believe DQ presents a great opportunity to buy a potential multi bagger. I estimate the intrinsic value of the company to be between $100 and $215. This wide range is predicated on the current uncertainty not only in the market but specific to the economic recovery in China. If the Government in China utilizes stimulus, DQ could directly benefit from it. I consider this a great deep value opportunity but I would not go all in. A small investment in DQ as part of a balanced portfolio might be wise but caution is necessary. The country risk, sector risk and geopolitical risk need to be thoroughly investigated before investing your money. As always, please perform your own due diligence and feel free to share your thoughts in the comments.

For further details see:

DQ Is A Deep Value Opportunity Before Earnings