DRMTY - Dr. Martens: Healthy Company But Fairly Valued

Summary

- The UK based boots' manufacturer Dr. Martens has seen a price fall of over 45% in the past year, despite sustained growth and good margins.

- Some fall in margins is expected as it makes investments, among other things, in e-commerce. But growth is expected to stay healthy.

- It's a healthy company, but its P/E indicates near fair valuation. It's past price trends don't encourage confidence for now either.

Since its successful IPO in 2021, British boot maker Dr. Martens (OTCPK: DOCMF ) has seen its price fall to a third of its opening price. Initial investors might well look at the dire warning in the song which inspires the title as one for DOCMF. Or given enough time, it might just turn out to be like the “timeless, durable products” that the company calls the boots.

Which one will it be? Before anything else, I’d like to highlight that in a year like 2022, when inflation hung over the stock markets like it hasn’t in a really long time, companies with robust margins were, and continue to be, prized. So at the initial glance, it was perplexing that Dr. Martens, whose margins aren’t terribly far from those of the biggest luxury fashion companies in the past years, saw a poor price trend. Over the past year, its price is down by 46.2%. In fact, just a few months into its IPO, the price trend has been downwards.

The company

It could be both the wearing off of initial hype about it, as well as the weakness in markets that started setting in. It’s probably a bit of both. But make no mistake, Dr. Martens is a unique brand with an engrossing story. At its start in 1960, the target market for the sturdy boots was the British working classes before rock bands and early goth culture popularised it. It was widely adopted by the youth and then revitalised in the early 2000s as fashion designers gave their own interpretation to the classic boot.

Strong margins

Going by its margins, it remains coveted even now. For its financial year ending March 2022, the company had a gross margin of 63.7% and an operating margin of 24.9%. This is even better than the margins for Cartier owner Richemont ( CFRUY ), a bonafide luxury company, whose gross margin was at 62.7% and operating margin was at 17.9% at the same time. Of course, they address different markets, their product types are different and Richemont has made smart financial decisions since , which have improved its margins, but this comparison does provide a sense of how high Dr. Martens' margins are.

The challenge with margins

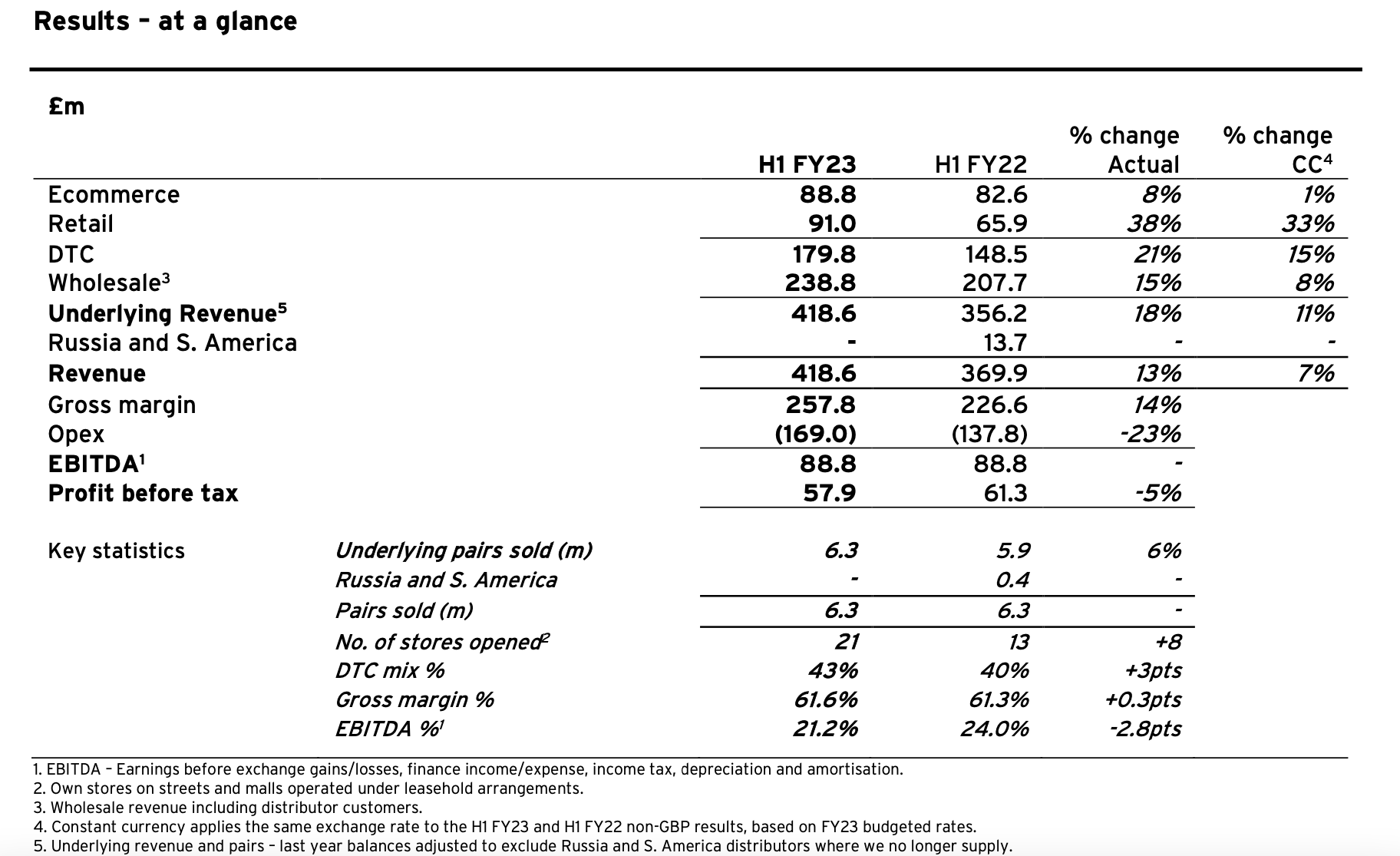

The present challenge for DOCMF however, becomes visible when we look at its numbers for the first half of its current financial year (H123, April-September 2022). While its gross margin has actually increased by 30 basis points (bps) to 61.6% compared to H122, its EBITDA margin has declined and its operating margin has seen a 349 bps fall to 15.65% as well. A double-digit rise in operating expenses is the reason, resulting in a decline in the absolute level of operating income for the first time after six years when we compare the latest figure to full-year numbers.

{kind=link}

However, nowhere does the company mention cost inflation as driving up these expenses in the release. In fact, it says elsewhere that “we have further pricing headroom...so we will offset cost inflation once again”. It does however mention investment in e-commerce as one of the reasons. It also says that it intended to start trial click, collect and return to the store at UK stores in the final quarter of the year.

Sustained growth expected

These sound like the right kind of expenses, which can work well for Dr. Martens in the future. E-commerce is already some 20% of its sales. Growth in the segment slowed down to just 8% year-on-year (YoY) as in-store shopping improved post-pandemic and China stayed in lockdown. For context, total revenue grew by 13% in H123. This growth is slower than during H122, when it was at 16.2%. But the company is optimistic that revenue will show “high-teens growth” for the full year.

It does expect its EBITDA margin to come in lower by 100-250 bps this year, but that’s because of the earlier-mentioned investments. Or as the company puts it, “…we made a proactive decision to continue with targeted investment for the future rather than reducing investment for short-term profit.”.

Further, even though it mentions a weakening environment, it doesn’t seem particularly perturbed by the recession that is likely to affect consumer discretionary companies. In fact, it expects “mid-teens revenue growth” starting FY24 onwards, which begins in April 2023. It helps that despite its very British roots, Dr. Martens has a market across Europe, the Americas and to a lesser extent in the Asia-Pacific region. I would still be looking out for how the potential recession impacts its financials, though.

The question of high inventories

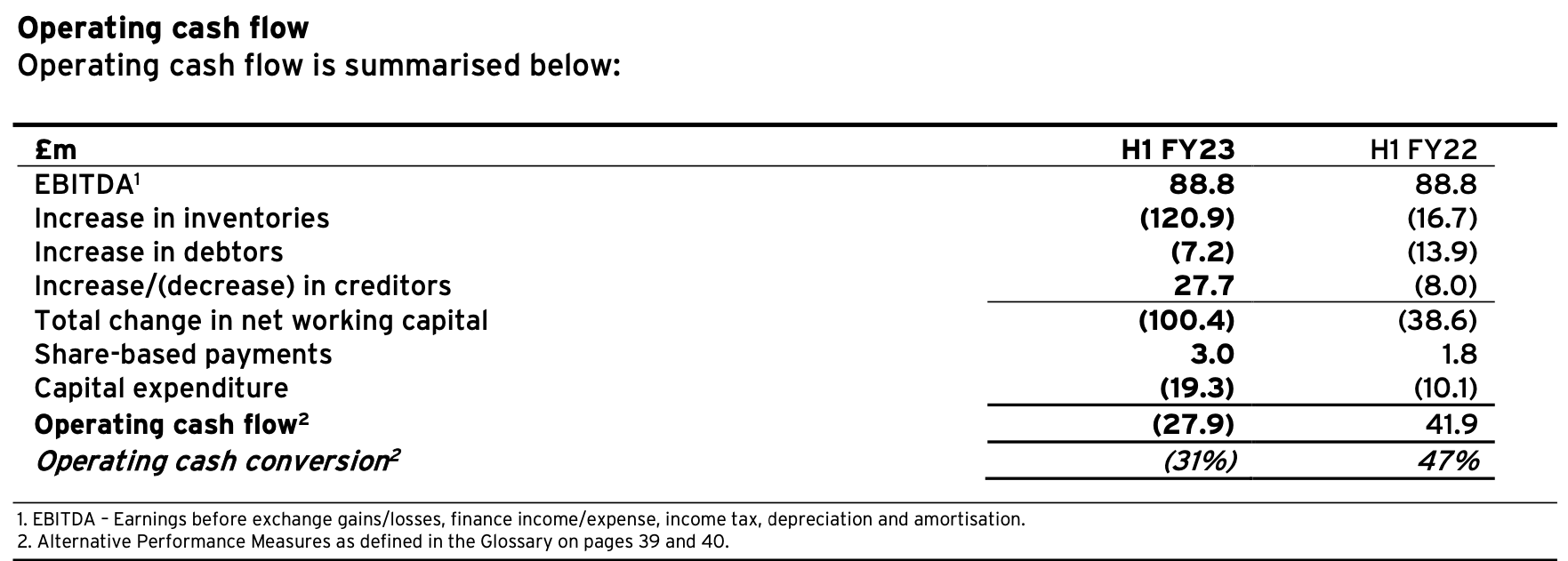

In total, the company’s income statement looks alright to me, its balance sheet doesn’t indicate any challenges either. With regard to the cash flow statement, the increase in inventories is glaring to £120.9 million from £16.7 million in H122, resulting in a negative operating cash flow.

But the company has a good explanation for this, too. It was a conscious decision on its part to increase inventories ahead of the peak season of the third quarter, since availability was weak, particularly in the markets of the US and Japan last year. Considering that it has been cash flows haven't been a problem in the past, I am willing to buy the explanation. But if inventories continue to stay high in the next financial update too, that might be a cause for concern since they can indicate slowing demand.

{kind=link}

What next?

In the last month, its price has started rising too, up by 15.6% since then. Its price-to-earnings (P/E) ratio at 12.8x isn’t super-low compared to that for the consumer discretionary sector at 14.2x, but it does indicate some 10% upside to Dr. Martens. If the stock markets continue to stay positive as they have so far in 2023, it could be reached quite soon.

But we can’t say that for sure, going by the fear of recession and expectation of continued high inflation. And going by DOCMF's past stock market performance, it tends to behave like any other consumer discretionary stock, despite good margins and sustained growth even during a challenging year. It doesn't help that its margins are expected to decline, even if for a good reason.

Moreover, DOCMF’s price momentum has just about turned positive. I’d like to put a Buy on it because it's a healthy company and a well-established brand, but for now, I’d go with a Hold, only because I see limited upside right now. This can change.

In other words, these boots are indeed made for walking, but in the best sense of the phrase. I’m not sure if I want to walk in them right away, though.

For further details see:

Dr. Martens: Healthy Company But Fairly Valued