RCKY - Dr. Martens: Highly Differentiated Brand With Upside

2023-06-15 00:04:22 ET

Summary

- Dr. Martens has a loyal fanbase that continues to grow. Its high-quality production and timeless design are key value drivers.

- The company has achieved a CAGR of 43% in revenue and maintains a strong EBITDA margin of 20%.

- Dr. Martens is trading at a discount compared to its underperforming peers, suggesting it has been oversold following the margin deterioration.

- Dr. Martens has opportunities for further growth through e-commerce, global expansion, and product innovation.

Investment thesis

Our current investment thesis is:

- Dr. Martens has a loyal fanbase which has been increasing as the brand goes mainstream. Its high-quality production and timeless design keeps consumers interested.

- Revenue has grown at a CAGR of 43% and the company has an EBITDA-M of 20%. We believe healthy growth is possible in the coming years, although margin deterioration remains a risk.

- Dr. Martens is trading at a discount to peers it outperforms, implying it has been oversold.

Company description

Dr. Martens plc (DRMTY) (DOCMF) designs, produces and sells footwear globally. It offers originals, fusion, kids, and casual, as well as accessories. Dr. Martens plc was founded in 1945 and is based in London, the United Kingdom (where it is listed).

Share price

Dr. Martens' share price has substantially declined since it was listed several years ago. This is a reflection of a change in consumer sentiment as financial improvement has slowed.

Financial analysis

{kind=link}

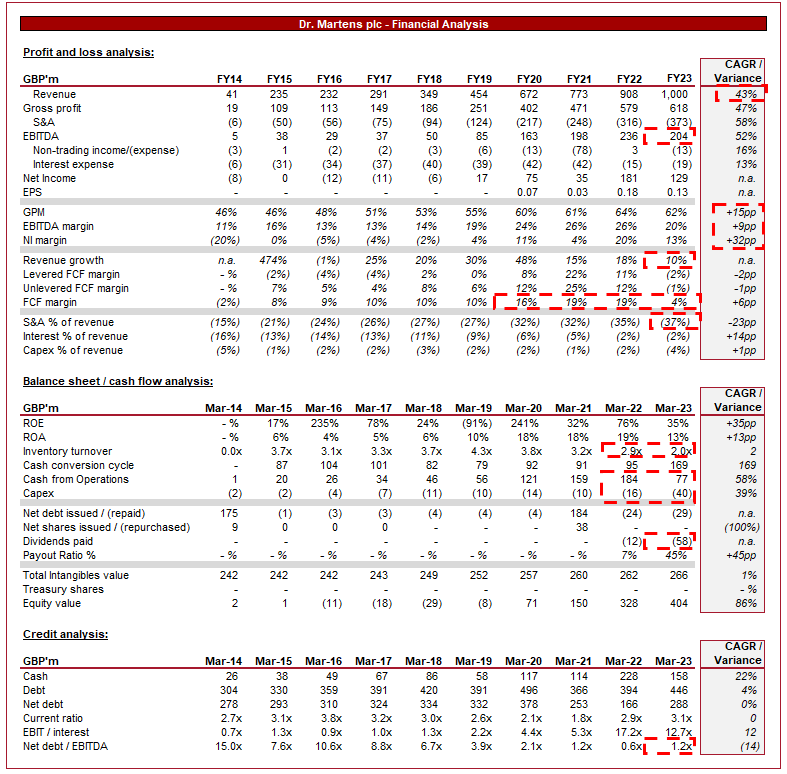

Presented above is Dr. Martens' financial performance for the last decade.

Revenue & Commercial Factors

Dr. Martens has grown its revenue at an impressive rate in the last decade, achieving a growth rate of 43%. This has slowed in recent years compared to the consistent 20%+ growth achieved between FY16-FY20. Despite this, growth remains in excess of 10%, which we believe is impressive given it operates in a niche.

Dr. Martens' products are not materially different from generic competition. Its boots (the most popular product) are high-quality but a comparable product can be found for a similar price. The selling point of Dr. Martens is its design and cultural influence. The brand is notorious for its yellow stitching, similar to adidas' ( OTCQX:ADDYY ) 3 strips, and has developed a cult following in alternative cultures through smart marketing and also word-of-mouth development. The brand is particularly popular amount the LGBT and Punk communities. Similar to Streetwear, the brand has seen its popularity increase as the mass market develops an interest in cultural niches. Once customers are acquired, the quality of the product is a key factor driving repeat purchases and continued word-of-mouth marketing due to customer satisfaction.

The difficulty with investing in the fashion industry is that consumer trends change. What is popular today may not be popular tomorrow, contributing to heightened risk around the outlook. For this reason, we have seen consolidation under a single umbrella, such as LVMH ( OTCPK:LVMHF ) or V.F. Corp ( VFC ). Our view is that Dr. Martens has developed impressive differentiation to the extent possible. The forward risk is reduced somewhat by its deep integration into cultures, which support consistent purchases.

As we mentioned previously, the fashion industry is highly competitive and driven by changing consumer trends. Taking this a step further, we will consider key trends impacting the industry and how they impact Dr. Martens' commercial position.

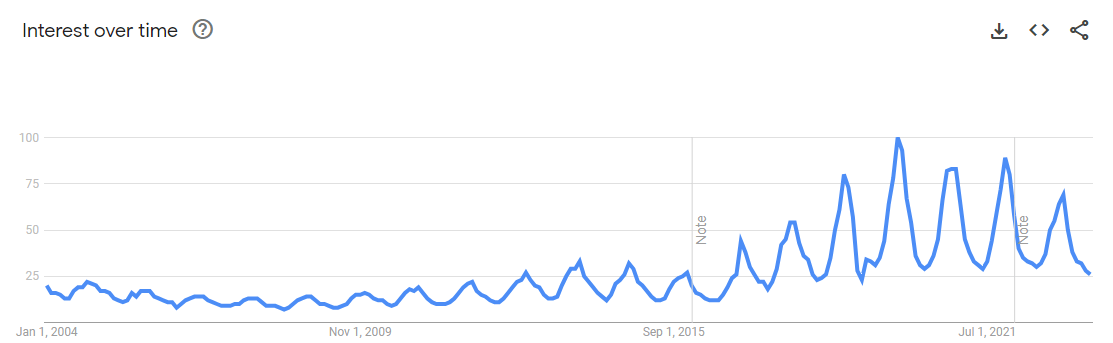

The resurgence of vintage and nostalgic fashion has significantly impacted the fashion industry. Consumers are increasingly thrifting clothes, looking for universally fashionable products with longevity. Dr. Martens' boots in particular have benefited well from this. The brand's iconic boots, which originated in the alternative subcultures with influences from the mid-20th century, have gained renewed popularity among consumers. As the following illustrates, interest in the brand has been on an upward trajectory in the last decade.

{kind=link}

Further, there has been a notable shift in consumer preferences towards casual and comfortable footwear . This has been accelerated in part by the Covid-19 pandemic but is a longstanding trend, likely due to an overarching reduction in clothing formality. Shoes and Boots are notorious for the lack of comfort and need to "break them in". Dr. Martens has innovated in this regard to incorporate comfort without losing shape or durability.

The Streetwear trend we touched on previously has also expanded to Dr. Martens. The fundamental ideals of Streetwear is a rejection of the mainstream and a focus on authenticity, expressionism and unity. This similarly aligns with how Dr. Martens sees the world. It is unsurprising, thus, that we have seen members of the culture embrace the brand.

China represents a key fashion market globally. The country has been ravaged by the Covid-19 pandemic, remaining stubborn with its zero-Covid policy until late 2022. Following the relaxing of these rules, the country has faced a rapid increase in cases, contributing to severe disruption and travel restrictions. The expectation is for this to ease in the coming year, representing a natural tailwind.

Influencer marketing has become a powerful tool for brand promotion and reaching target audiences. Although we believe Dr. Martens has done well to engage with influencers and collaborated with popular brands, it has been unable to generate the hype others have. This is likely in part due to its reduced resources, restricting the ability to invest in customer acquisition.

There are several key opportunities we see which have the ability to support the positive trends to keep Dr. Martens on its current trajectory.

The rise of e-commerce and digital integration represents a key opportunity for Dr. Martens. With the increased popularity of the brand, the company can now focus further on directing customers to its online presence (as opposed to retailers). We believe this is a key strategy management must pursue as its customers are incredibly loyal, and thus encouraging direct sales should be highly successful. The company's current DTC mix is 52%, so further development can contribute to increased margins and distribution diversification.

Further, although the company is already international, Dr. Martens has substantial growth potential across much of the developing world, including Asia and South America, which are underserved regions relative to its core markets. Expanding its global footprint enables the company to diversify its revenue streams and importantly increase its total addressable market ((TAM)).

Finally, product innovation remains a must. Although the company is famous for footwear, it has the capacity to maintain its key expertise while expanding. The expansion into bags is a perfect example of this. They are incredibly popular and maintain a focus on leather as a raw material.

Economic & External Consideration

Current economic conditions represent a key risk to the business in the near term. Inflationary pressures and rising interest rates are contributing to reduced discretionary spending, as consumers focus on living expenses. This is likely the reason for the slowdown in revenue growth to 10% in the most recent period.

Our expectation is for current conditions to remain uncertain in the coming year, as inflation continues its slow decline. This will likely mean flat growth in FY24. Overall, however, we do not see this as a factor which can change the current trajectory of growth.

Margins

Dr. Martens' margins are very good. The company has a GPM of 62%, EBITDA-M of 20%, and a NIM of 13%.

Margins have overarchingly improved across the decade, reflecting scale economies through the production of purely leather footwear, as well as consistent pricing increases.

This has been offset in the recent year, as EBITDA-M declined c.6%. This is partially due to inflationary pressures as an increase in input costs and operational costs cannot be wholly passed on to consumers. Further, the company faced lower-than-expected demand (especially in the US), and a supply bottleneck at the distribution facility in Los Angeles.

Balance sheet

Dr. Martens' inventory turnover has materially declined in the most recent year, falling from 2.9x to 2x. This is a reflection of the unexpected soft demand (and mismanagement) contributing to stockpiling. The concern is that this stock will need to be discounted in the coming year, resulting in further margin erosion.

Dr. Martens is conservatively financed, with a ND/EBITDA ratio of 1.2x. This gives the company increased flexibility if required.

Cash flows have generally been consistently strong, although the recent inventory build-up has diminished this somewhat. Our expectation is for this to bounce back in the coming year.

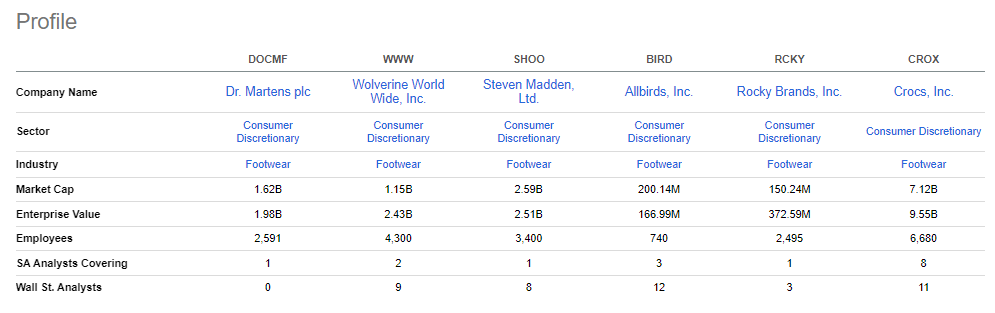

Peer analysis

In order to assess Dr. Martens' relative performance, we have compared it to the following footwear businesses.

{kind=link}

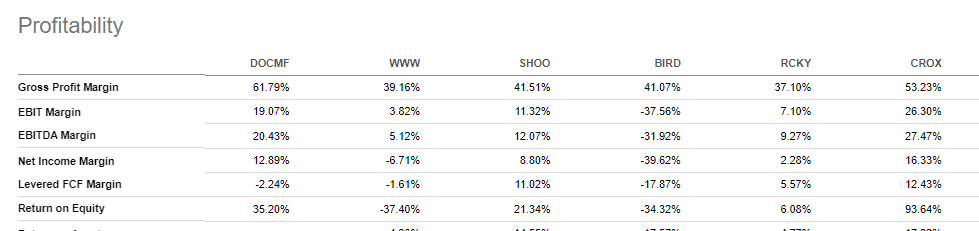

From a profitability perspective, the company performs extremely well. Its EBITDA-M is noticeably above every peer except Crocs ( CROX ), a company we are highly bullish on. This margin outperformance is all driven by its GPM superiority, reflecting the pricing power the brand affords, supporting our view that its commercial position is impressive.

{kind=link}

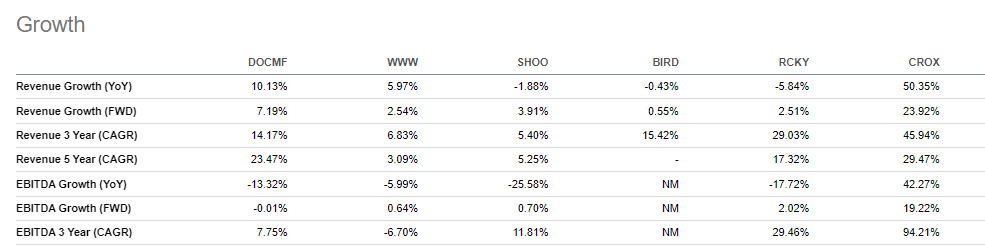

From a growth perspective, Dr. Martens continues its strong relative performance, although falls short of both Rocky ( RCKY ) and Crocs. The key for us is that it has clearly been a volatile period for retail, yet Dr. Martens has managed to continue its trajectory.

{kind=link}

Based on this, our view is that Dr. Martens should be trading at a premium to the cohort, except for Crocs.

Valuation

{kind=link}

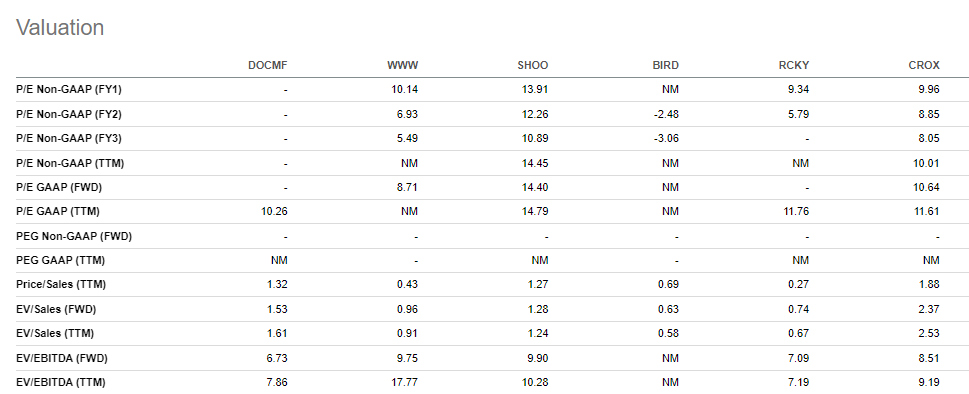

Dr. Martens is trading at a discount to the cohort average on both an LTM and NTM basis, despite its superior margins and growth. This suggests the stock is oversold relative to the rest, with investors harshly punishing the business for its margin slippage, without factoring in the strong absolute level.

{kind=link}

A rerating was required as it is extremely difficult for retailers to win back margins following a decline but this looks overdone. Dr. Martens' NTM FCF yield is currently 10%, reflecting the fundamentally impressive profitability of the business.

We should note that we are highly bullish on Crocs and consider it undervalued. We believe Dr Marten could reach a forward EBITDA multiple of 8-9x, with Crocs pushing for low double digits.

Key risks with our thesis

The risks to our current thesis are:

- A material margin deterioration in FY24. The Street is guiding a 1.7% erosion to EBITDA, which we consider reasonable. The key for us is for the company to remain at about 18% and have a key plan to return to a 20-25% level.

- A decline or flat revenue could spook investors further. We believe flat revenue is priced in by markets but they can react sporadically.

Final thoughts

Dr. Martens is an example of how to develop differentiation in a highly competitive industry. The company is highly focused on its niche and has developed a strong rapport with its core customers. As popularity increased, the company has not changed its vision or messaging, which is always a risk (Consumers hate the idea of "selling out").

From a financial perspective, the company is equally as attractive. Its trajectory is positive and margins are good. This is not an investment without risk but with a sufficient discount, Dr. Martens looks to be a good investment.

For further details see:

Dr. Martens: Highly Differentiated Brand With Upside