DKNGZ - DraftKings: Be Patient And Don't Rush To Buy Now

Summary

- DKNG has pulled back 30% from its August highs after surging nearly 60% from its May lows. We posited in our previous update that DKNG has likely bottomed, which materialized.

- DraftKings' Q2 release demonstrated that the company could navigate challenging macro headwinds well, vindicating management's confidence in its previous commentary.

- Coupled with its raised guidance for FY22, we are confident that the pullback is healthy and should not re-test its May lows.

- We discuss why we still decide to revise DKNG from Buy to Hold and urge investors to await a lower-risk entry point.

Thesis

We updated investors in our previous article on DraftKings Inc. ( DKNG ) that the market has been quietly accumulating since its May lows through July, even as the pessimism on DKNG reached feverish highs. Therefore, we are not surprised that DKNG surged more than 60% since our article toward its August highs, as it outperformed the broad market significantly. DKNG also met our price target ((PT)) of $19 before the market digested its rapid momentum spike, as such surges are often unsustainable.

Therefore, DKNG's post-Q2 earnings gains have been digested meaningfully, as it pulled back nearly 30% from its August highs. Investors are also assessing whether it could fall back to its July lows.

For speculative stocks like DKNG, it's critical for investors to be generous with their margin of safety, given that it has yet to prove sustainable profitability. Therefore, the market used DraftKings' positive Q2 release as an opportunity to draw investors into a bull trap (indicating the market denied further buying upside decisively) in August before digesting those gains.

Given the recent steep pullback, DKNG's valuations seem more well-balanced. Furthermore, we have yet to discern a constructive basing price structure that could indicate an accumulation phase similar to its May to July bottom.

As such, we revise our rating from Buy to Hold and urge investors to be patient as we await a more constructive and lower-risk entry level.

DraftKings' Line Of Sight Toward Adjusted EBITDA Profitability Improved

As an unprofitable company, DKNG has been battered over the past year as the market digested its unsustainable premium. However, we noted that the pummeling has been so intense that even the bears lost momentum at its lows in May. Therefore, it appeared that the market built up buying momentum through July, as DraftKings' headed into its Q2 release. Given the constructive price action, we posit that the market had anticipated a better-than-expected Q2 card, which DraftKings delivered with aplomb.

{kind=link}

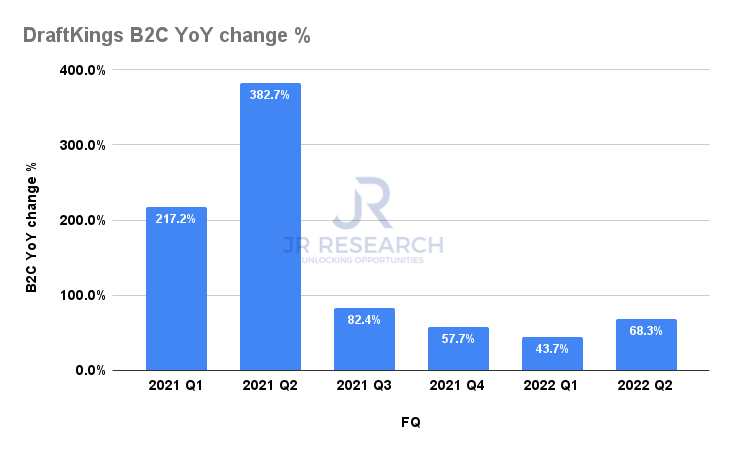

As seen above, DraftKings posted revenue growth of 68.3% YoY in Q2 in its B2C segment, demonstrating that its rapid growth momentum has remained robust. It was also better than Q1's 43.7%.

Furthermore, DraftKings has proved that the worsening macroeconomic environment has not impacted its growth cadence materially, which lent credibility to management's previous commentary. As a result, DraftKings justified its ability to navigate challenging economic cycles, proving its platform stickiness, as it also raised guidance for FY22.

{kind=link}

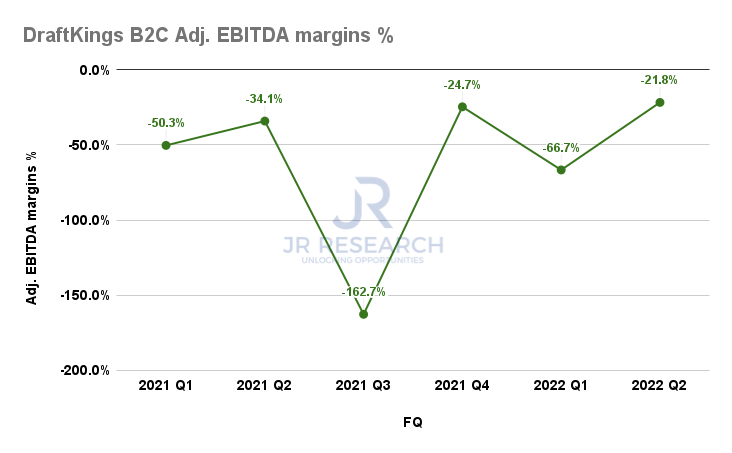

Furthermore, its robust topline performance came as DraftKings tempered its promotional spend. The company also expects to improve its fixed costs leverage as it dialed down its hiring momentum and reached adequate scale. Coupled with a timely transition of more ad spending toward national advertising, it's expected to improve its operating leverage moving forward.

Accordingly, DraftKings posted a much improved B2C segment adjusted EBITDA margin of -21.8%, also leveraging the early iGaming synergies of its recent Golden Nugget acquisition.

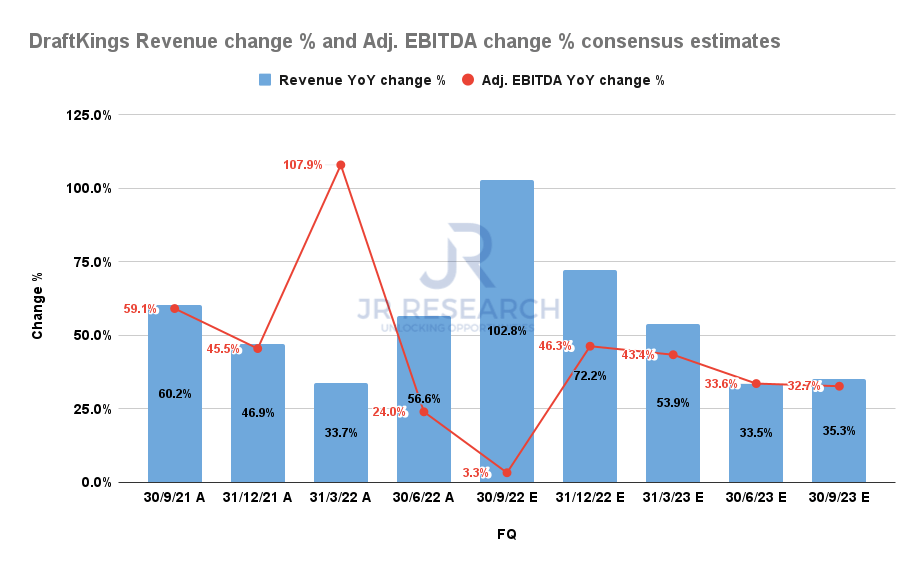

DraftKings revenue change % and adjusted EBITDA change % consensus estimates (S&P Cap IQ)

{kind=link}

Accordingly, the consensus estimates (bullish) indicate that DraftKings should continue its path toward achieving adjusted EBITDA profitability as it exits FQ4'23. Therefore, investors should expect DraftKings' adjusted EBITDA growth to continue improving, despite the recessionary headwinds.

As a result, management demonstrated its conviction by raising its FY22 guidance , which improved investors' confidence in its strategy. However, investors need to note that DraftKings' profitability could be impacted by hold variability headwinds in Q3, given the uncertainty over its hold in certain weeks on the upcoming NFL season.

Therefore, we believe the company guided conservatively to reflect these uncertainties but expect Q4's seasonal tailwind to mitigate the challenges seen for the next quarter. As a result, a better than expected Q3 performance could be instrumental toward a re-rating for DKNG.

Is DKNG Stock A Buy, Sell, Or Hold?

{kind=link}

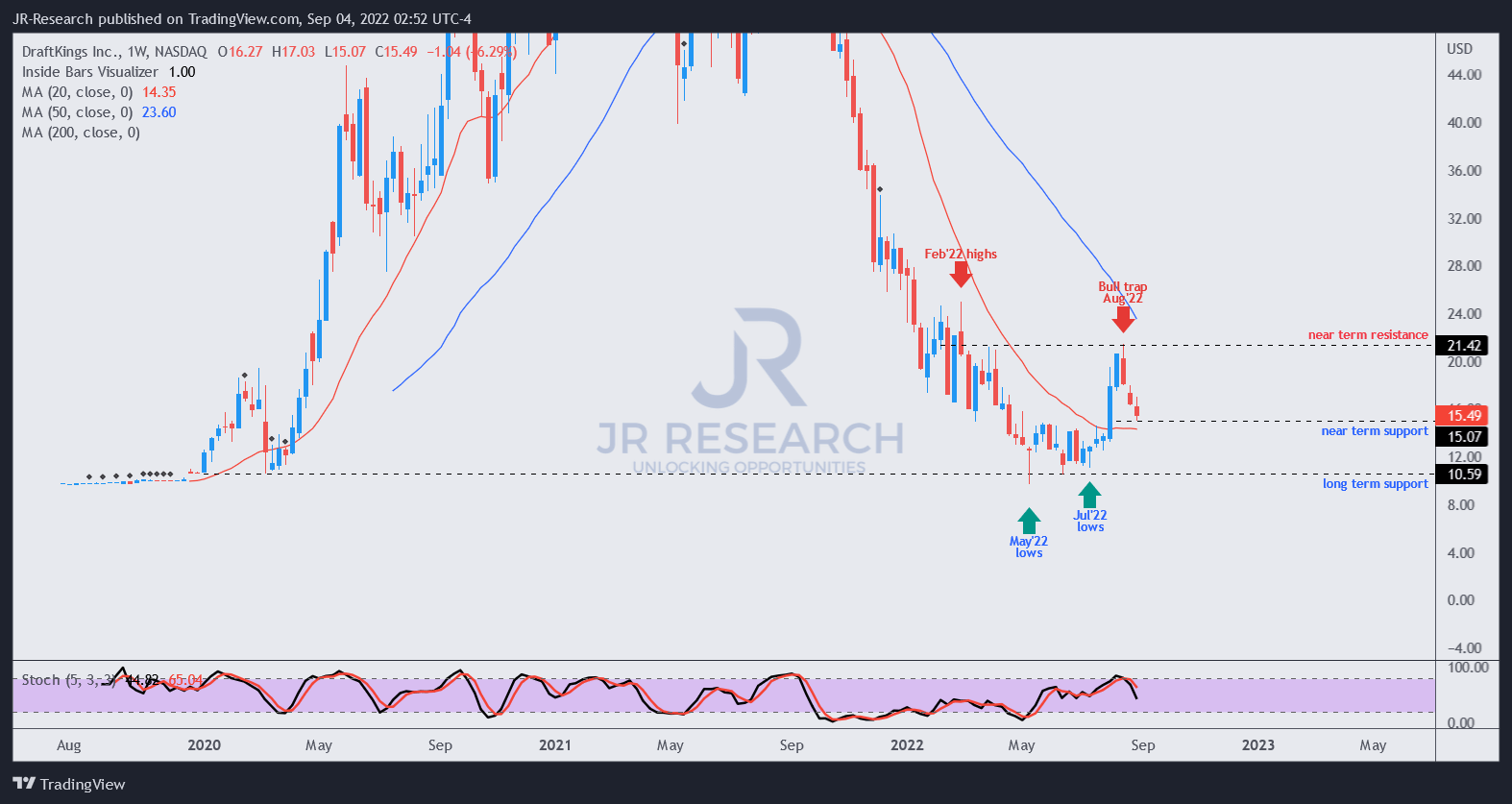

As seen above, DKNG's consolidation zone between May and July was highly constructive, indicating an astute accumulation phase, as we surmised in our previous update.

Therefore, investors who sold between May and July unloaded at DKNG's absolute lows, as they missed the opportunity to partake in the rapid surge toward its August highs.

However, we noted that DKNG formed a validated bull trap in August, leading to the pullback seen over the past four weeks. Still, we are confident that DKNG is unlikely to break below its May lows in the medium-term, given improved unit economics and a battered valuation.

Notwithstanding, we postulate that the current levels could still face near-term downside volatility, de-risking the entry levels for DKNG further, and helping to improve its potential for outperformance moving ahead.

Coupled with a more well-balanced valuation, we revise our rating from Buy to Hold and urge investors to wait for a better entry point.

For further details see:

DraftKings: Be Patient And Don't Rush To Buy Now