PDYPY - DraftKings: It's Time To Fold

2023-04-13 14:47:57 ET

Summary

- DraftKings has experienced rapid growth since becoming public in 2020.

- The TAM for Sports Betting and iGaming in the US is large and growing.

- Competition is fierce in this fragmented market.

- The company has spent big on customers through advertising and promotions.

- The share price is significantly overvalued.

Thesis

DraftKings (DKNG) has been aggressively targeting new users in order to gain market share in the highly competitive online sports betting and iGaming space. The low barrier to entry and huge opportunity through legal changes in the US mean that DraftKings has many competitors, the two major of which already have profitable parts of their businesses.

The fragmented nature of the industry and DraftKings' speculative and expensive land grab have led it to be a risky business for new investors, even at 70% below their all-time highs. The stock price still has a lot of growth assumed and I am not convinced that it will be sustainably profitable. As a result, it is a sell from here.

Company Profile

Only just a decade old and made public through a 2020 SPAC, DraftKings has seen almost exponential growth in a very short period of time. Founded by 3 friends and former co-workers , it became a household name in the US as a main provider of the ever popular fantasy sports games that cover golf, baseball, ice hockey and of course football (or American football for us Europeans). Since then, and realising the huge opportunity available for moving into sports book betting and iGaming with the regulatory environment changing in the US, DraftKings went all in and expanded quickly, including a number of acquisitions, notably the recent purchase of the digital brand and assets of Golden Nugget Online for $1.56 billion, specifically targeting the iGaming opportunity.

Opportunities for Growth

The total addressable market in North America for both sports betting and iGaming are large and recent changes to the regulatory landscape in the US has investors rightfully excited as it grows quickly. It is not easy to ascertain exactly how big the opportunity could be as states slowly roll out changes. As a frame of reference: CFRA Research analysts suggest that an optimistic case sees a $42 billion addressable market in North America for both sports betting and iGaming combined. Google the term TAM and Sports Betting or iGaming and you quickly realise that there is a wide spread of forecasts.

What we do know, is as of February 2023 , 36 of the 50 states have legalised sports betting, 3 of which are legal but their markets are not yet live for companies to operate. Just a few have fully legalised iGaming, and at their 2022 investor day, DraftKings management suggested that about 13% of the US population are legally allowed to play online casino games. This leaves both categories with lots of potential growth and with state budgets weakened and recovering from Covid and inflationary measures, there is an increasing likelihood that more states will follow this opportunity to bring fresh taxation into their coffers.

DraftKings management see their total addressable market across North America for both Sports Betting and iGaming at around $80 billion. For those of you paying attention, that's double what the independent research company mentioned above forecast. DraftKings currently have a market share of around 25% for US Sports Betting and 19% of iGaming.

Further, management shared their long term gross revenue at maturity target would be between $6.7- $9.5 billion. They also share that their long-term adjusted EBITDA target is just over $2 billion. Taken at a midpoint, that would make their EBITDA margin target a smidge under 25%, which is also around the target of main competitor Fanduel owned by parent company Flutter Entertainment ( PDYPY ).

Since going public, DraftKings has demonstrated an impressive ability to grow revenue, from just $71 million Q2 2020 to $855 million in the most recent quarter. Management uses adjusted EBITDA as its preferred profitability metric for earnings calls and thus far, the company has been unable to produce a profit. The most recent quarter saw an adjusted EBITDA loss of $50 million, which as you can see from the yellow columns and the right hand vertical axis, means that they are close to breaking even on an adjusted EBITDA basis with management guiding for adjusted profitability for FY 2024.

Income of DraftKings since going public (Compiled by Author from Information from Company's Earnings Presentations)

Risks and Competition

The growing opportunity of US Gambling means that there is plenty of competition for DraftKings. There are currently over 50 online sportsbooks but the top 3 currently share around 80% of the market share. FanDuel owned by large international operator Flutter Entertainment sits at number 1, BetMGM ( MGM ) is 3rd with DraftKings currently sandwiched between them at number 2.

PDYPY, the parent company of Fanduel, has an EBITDA margin of around 9% currently. MGM around 13.5%. PDYPY has decades of experience and is the world's largest bookmaker. MGM has brick and mortar casinos that are becoming profitable again after the pandemic. DraftKings is a pureplay without the additional protections and income streams of its two major rivals.

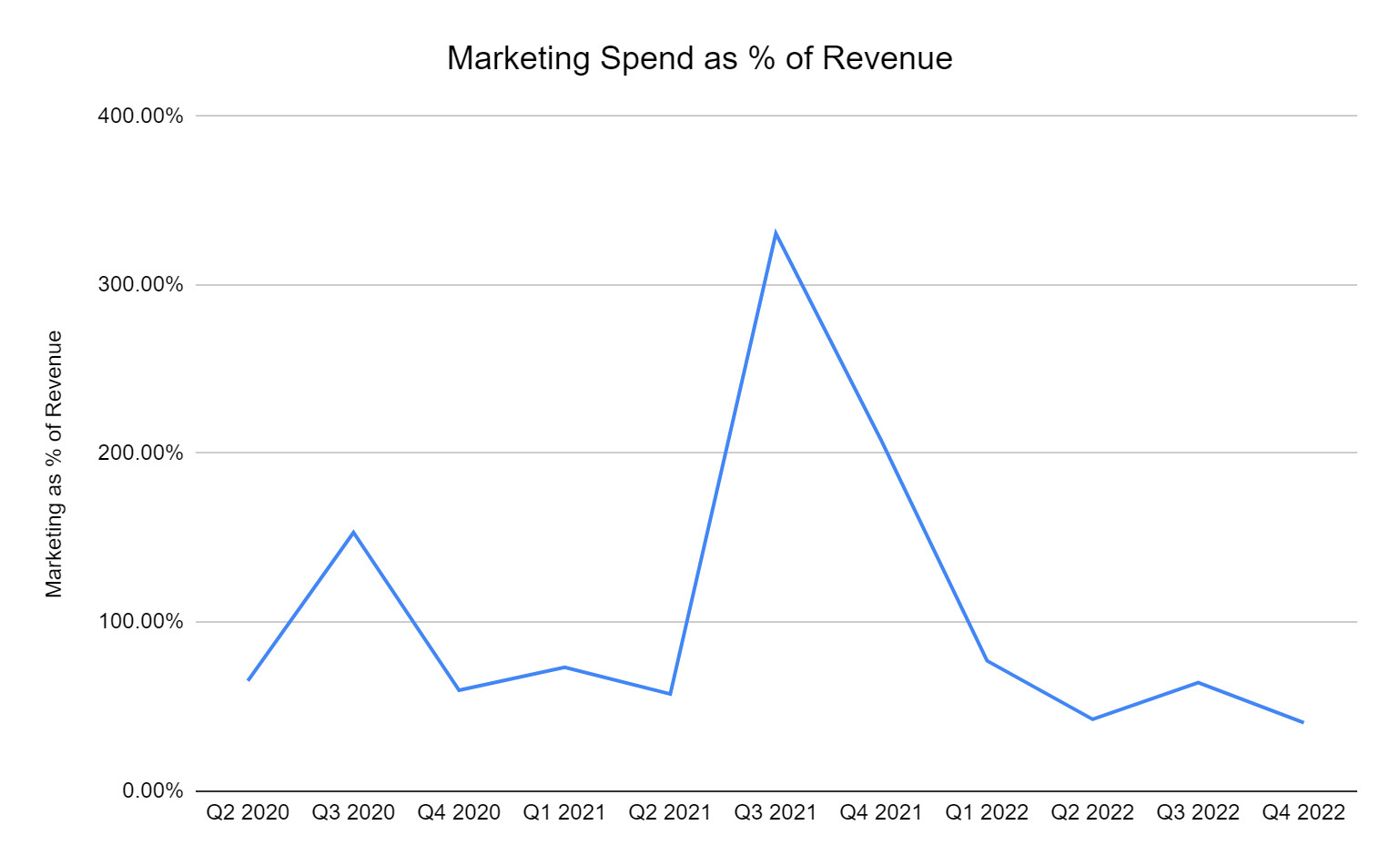

Further, DraftKings has been spending big in order to gain its market share. This has so far been sustainable but I question whether they can continue this level of spending through the next Full Year. The following series of charts will help me demonstrate this.

This chart shows marketing spend as a % of revenue. The last quarter saw this number fall to 40% but there are alarming quarters when this amount is comfortably above 100% of total revenue.

Marketing Spend as % of Revenue (Writer's Calculations based on Data from Company's Earnings)

{kind=link}

During this time, a lot of the cash raised from going public in 2020 was wiped out and now for the first time, the balance sheet shows almost an equal amount of cash and debt. Management has stated that it should have at least $700 million left in cash by the end of FY 2023.

Balance Sheet since going Public (Compiled by Author from Information from Company's Earnings Presentations)

The company has diluted shareholders to the tune of nearly 43% since going public, which made sense as the share price was very high. As its cash levels get lower and it yet isn't profitable, it will need to either continue to dilute shareholders, raise debt at higher interest rates than they could have in the past or to become more efficient and look for sustainable cash flows. Probably a combination of all 3.

DraftKings really needs to find a way to make some money soon if it is going to retain its current market share. My concern is that, to date, growing numbers of customers has been facilitated almost exclusively by spending money through promotions, advertising and free bets in order to entice them. With competitors all doing the same, the price for acquiring gamblers is high.

The following chart can be a little overwhelming so please allow me to break it down. It shows the Monthly Unique Payers or MUPs (i.e. different individuals who have registered a bet within a particular month), the average revenue per monthly unique payer (ARPMUP), a personal calculation of how much each of these customers cost based on dividing marketing spend by the number of MUPs, and finally this marketing cost per customer vs the revenue generated by each one.

The column on the far right shows that the cost of convincing a customer to use DraftKings is more than the amount of revenue that that customer provides to the company. This is not sustainable. My concern is, if the company decide to slow down this marketing, particularly their promotional offers and joining bets, gamblers will simply sign up for a competitor. With a retention rate of 87% , more than 1 in 10 left for a competitor last year, despite these high acquisition costs.

| MUP |

| ARPMUP |

| Marketing Spend (in ) |

| Marketing Spend per MUP |

| Marketing Spend per MUP vs ARPMUP |

| Q2 2020 |

| 295,000 |

| $63 |

| $46,188 |

| $157 |

| 2.5x |

| Q3 2020 |

| 1,021,000 |

| $34 |

| $203,339 |

| $199 |

| 5.9x |

| Q4 2020 |

| 1,498,000 |

| $65 |

| $191,959 |

| $128 |

| 2.0x |

| Q1 2021 |

| 1,542,000 |

| $61 |

| $228,686 |

| $148 |

| 2.4x |

| Q2 2021 |

| 1,123,000 |

| $80 |

| $170,712 |

| $152 |

| 1.9x |

| Q3 2021 |

| 1,340,000 |

| $47 |

| $703,056 |

| $525 |

| 11.2x |

| Q4 2021 |

| 1,971,000 |

| $77 |

| $981,500 |

| $498 |

| 6.5x |

| Q1 2022 |

| 2,000,000 |

| $67 |

| $321,452 |

| $161 |

| 2.4x |

| Q2 2022 |

| 1,500,000 |

| $103 |

| $197,529 |

| $132 |

| 1.3x |

| Q3 2022 |

| 1,600,000 |

| $100 |

| $321,714 |

| $201 |

| 2.0x |

| Q4 2022 |

| 2,600,000 |

| $109 |

| $345,282 |

| $133 |

| 1.2x |

Valuation and Expected Returns

In order to produce this next table, I used current Seeking Alpha forecasts for revenue for 2023 and 2024 and then slowed down revenue at a pace that makes sense to me based upon the opportunity available. I worked up to managements 'maturity' target of 25% EBITDA and assumed an ultimate net income margin of 14%, which is a little over MGM's current 11.3% as DraftKings are an online/digital company without the expense physical casinos. As a sniff test, I also used $61 billion as a potential addressable market (averaging CFRA and DraftKings' management estimates), to see where that gets DraftKings in 2033 - a 15% share of the overall market, which sounds about right for a 10 year forecast.

| Revenue |

| Growth |

| EBITDA Margin |

| EBITDA |

| Net Margin |

| Net |

| TAM |

| 2020 |

| $614 |

| 1.01% |

| 2021 |

| $1,296 |

| 111.07% |

| 2.12% |

| 2022 |

| $2,240 |

| 72.84% |

| 3.67% |

| 2023 |

| $2,990 |

| 34% |

| 2% |

| $60 |

| 0% |

| $0 |

| 4.90% |

| 2024 |

| $3,654 |

| 22% |

| 5% |

| $183 |

| 2% |

| $73 |

| 5.99% |

| 2025 |

| $4,202 |

| 15% |

| 8% |

| $336 |

| 4% |

| $168 |

| 6.89% |

| 2026 |

| $4,791 |

| 14% |

| 12% |

| $575 |

| 7% |

| $335 |

| 7.85% |

| 2027 |

| $5,414 |

| 13% |

| 15% |

| $812 |

| 8% |

| $433 |

| 8.87% |

| 2028 |

| $6,063 |

| 12% |

| 18% |

| $1,091 |

| 9% |

| $546 |

| 9.94% |

| 2029 |

| $6,730 |

| 11% |

| 20% |

| $1,346 |

| 10% |

| $673 |

| 11.03% |

| 2030 |

| $7,403 |

| 10% |

| 22% |

| $1,629 |

| 11% |

| $814 |

| 12.14% |

| 2031 |

| $8,069 |

| 9% |

| 25% |

| $2,017 |

| 12% |

| $968 |

| 13.23% |

| 2032 |

| $8,715 |

| 8% |

| 25% |

| $2,179 |

| 13% |

| $1,133 |

| 14.29% |

| 2033 |

| $9,325 |

| 7% |

| 25% |

| $2,331 |

| 14% |

| $1,306 |

| 15.29% |

I model that the company will have to continue to dilute as they become more profitable and at an annual increase of around 5.5% in diluted shares outstanding, I reach a total of 742.8 million. Using market averages of 3 for price to sales and 15 for price to earnings multiples out 10 years from now, I get the following valuation for DraftKings for 2033:

| Price to Sales Valuation |

| $19,583 million |

| Price to Earnings Valuation |

| $27,975 million |

| Average of 2 |

| $23,779 million |

| Diluted Shares Outstanding in 2033 |

| 742.8 million |

| Share Price 2033 |

| $32 |

| Return from current price of $19 |

| 5.49% |

I calculate that from here over the course of 10 years, based on the above expectations, that DraftKings will return around 5.5% per year. I would not expect it to beat or even match the market. My target price to receive a 10% annual return would be $12.34. This means the current price is around 54% overpriced . For me, it is a clear sell.

Summary/Opinion

DraftKings is a market leader in a large and exponentially growing opportunity of North American (mostly US) sports betting and iGaming. It has done well to achieve this in such a small time as a company and it has grown revenues quickly. The economic situation and market have both changed considerably in the past couple of years and despite being down around 70% from its all-time high, I still see the company as significantly overvalued.

There is a high risk to the investment. There is a lot of growth expected and there are a lot of competitors all vying for customers. This has led to a large amount of money being spent on marketing and promotions by DraftKings. They will not only need to reduce expenses but also hope that their retention rates hold and that they can stay a market leader and one of the first names potential customers think of for their betting needs. Remember, that their 2 main competitors are also currently profitable with much longer histories in this industry.

At the current prices available for new shareholders, I cannot see that this company can beat the market. In addition to an existential risk of more experienced and already profitable competition, I rate DraftKings a sell.

For further details see:

DraftKings: It's Time To Fold