DKNGZ - DraftKings Q1 Earnings: Emerging Leader In The iGaming Market

2023-05-05 11:59:21 ET

Summary

- DraftKings beat across both top and bottom lines while also demonstrating a slate of excellent user metrics.

- Market share metrics are also very healthy, and the company established new markets faster than it had old ones.

- This occurred even while marketing spend and customer acquisition costs declined.

- By one measure, DraftKings is already first in the iGaming market nationally.

- All of this makes me optimistic for this stock and willing to call it a buy going forward.

Overview

Mobile sports-betting company DraftKings (DKNG) is up 8.87% in aftermarket trading in the wake of its latest earnings report . Beating consensus expectations across both non-GAAP EPS as well as revenue, DraftKings continued to grow revenues briskly at 84.7% YoY. Additional commentary by management included an upgrade to this year's guidance as well as references to adjusted EBITDA profitability within the current fiscal year. This article will review DraftKings' earnings report in-depth as well as comment on the company's current valuation.

Earnings Report Highlights

As mentioned DraftKings beat across both top and bottom line metrics handedly.

| Consensus |

| Actual |

| % Difference |

| Non-GAAP EPS |

| ($0.85) |

| ($0.51) |

| 40.0% |

| Revenue |

| $697.53M |

| $770M |

| 9.41% |

Source: DraftKings, Seeking Alpha

While this was an excellent showing there was a lot of other information worth noting in the earnings report.

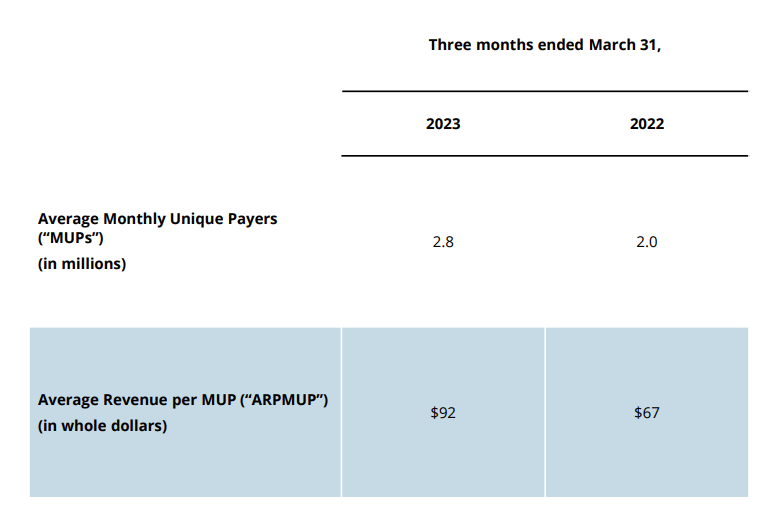

User metrics came in very strong across the board.

- Average Monthly Unique payers increased 40% YoY, from 2M to 2.8M

- Average Revenue per MUP increased 37.3% YoY, from $67 to $92

- Overall users grew 57%

- Parlay Mix of Handle (percentage of bets on platform with more than 1 leg) increased 4%

- Average leg count increased 10%

- Customer Acquisition Cost declined 27%

{kind=link}

Management expressed confidence across this growth and stated that it had seen 'no discernible impact from the challenging macroeconomic environment'. While it's too early to come to this conclusion, DraftKings' offering could prove to be relatively inelastic relative to overall consumer spending.

{kind=link}

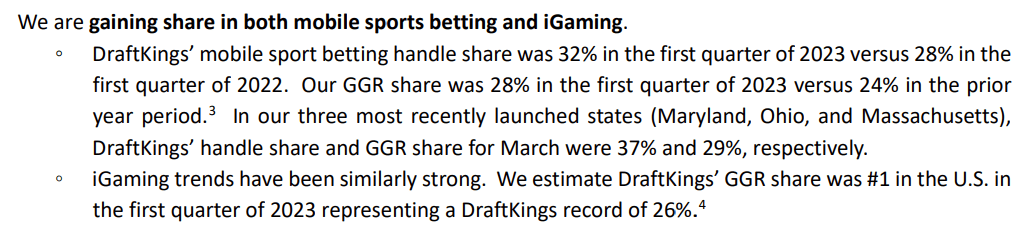

Market share metrics were also very healthy.

- Handle share (percentage of all money wagered on online sports betting) was 32%, growing 4% YoY.

- GGR share (gross gambling revenue, online sports betting) was 28%, growing 4% YoY.

- Handle share and GGR across new markets (Maryland, Ohio, Massachusetts) was even higher, at 37% and 29% respectively

- DraftKings estimates itself to be the market leader for iGaming (online betting) in the US, with a GGR share of 26% for Q1 2023

{kind=link}

As mentioned management also upgraded guidance for the current fiscal year:

- Today, we are improving our fiscal year 2023 revenue guidance range to $3.135 billion to $3.235 billion

- .. 2023 Adjusted EBITDA guidance range to negative $290 million to negative $340 million.

- We continue to expect our Adjusted Gross Margin rate to be in the 42% to 45% range for the year.

Valuation

DraftKings is trading as a growth stock and is priced well above the consumer discretionary median on a price/sales basis. As of its post-market price appreciation, the stock is trading at 4.67 price/sales multiple relative to the sector median of 0.82.

Assuming current revenue growth rates can be maintained, creating an implied growth rate of 75% going into 2024 and 70% going in to 2025, we see that DraftKings will still be trading at a sector premium at 2025 with all else held equal. Worth noting is that there is a 6.5% CAGR for the quantity of shares outstanding, derived from the overall share growth from the last 2 years.

| 2022 |

| 2023 |

| 2024 |

| 2025 |

| Revenue |

| $2.241B |

| $3.185B |

| $5.57B |

| $9.48B |

| Share Price |

| $23.21 |

| $23.21 |

| $23.21 |

| $23.21 |

| Float (Quantity of Shares) |

| 450.6 |

| 479.89 |

| 511.08 |

| 544.3 |

| Market Capitalization |

| $10.46B |

| $11.14B |

| $11.86B |

| $12.63B |

| Price/Sales |

| 4.67 |

| 3.497 |

| 2.13 |

| 1.33 |

Source: Excel, Seeking Alpha

With that being said DraftKings is currently the 2nd fastest-growing company in the Casinos & Gaming subsector and is growing well beyond the market average. Given its leadership in a relatively new market, it would be fair to assume that double-digit growth persists beyond the 3 year mark. The iGaming market in the US is estimated to grow at a 17.34% CAGR over the next 5 years.

As we currently do not have a track record of profitability or cash flow generation, it isn't possible to price DraftKings on this basis.

{kind=link}

Overall I think DraftKings is to be looked at as a long-dated growth stock. It will take 5 years or more for it to achieve sector parity on valuation and it will trade at significant premiums to the market until then. This is a stock trading on the basis of its ability to keep growing. Now that consensus has gotten significantly more optimistic, this will be difficult for the firm to keep pace with. Nonetheless, DraftKings has taken first place in its target market and should be able to continue growing.

Conclusion

This quarter DraftKings proved that it is a leading contender, if not the leading contender, in the fast-growing iGaming space. In particular it is interesting to see that the company achieved a faster growth curve timeline across its new markets. This was understood to be due to the company having a higher overall profile due to its previous national marketing campaign.

This growth also occurred against the backdrop of decreasing overall marketing spend, which speaks to the stickiness of the product. I am made more optimistic by the increasing per-user profitability metrics. The picture overall here looks good and I am bullish on DraftKings going forward.

For further details see:

DraftKings Q1 Earnings: Emerging Leader In The iGaming Market