DPRO - Draganfly Is Likely To Have Another Tough Year But Short Selling Seems Dangerous

2023-04-20 04:00:30 ET

Summary

- Draganfly’s Q4 2022 revenues fell by 19.6% year on year to below $1 million and I expect the company to struggle to surpass the $5 million mark for 2023.

- Draganfly closed an $8 million equity offering on March 31, but I think that it could need another capital increase before the end of the year.

- However, short selling seems dangerous as the short borrow fee rate is over 13% and the lowest available strike price for call options is $2.50.

- I think that investors should avoid DPRO stock.

Introduction

I’ve written four articles on SA about Canadian drone maker Draganfly ( DPRO ), the latest of which was in February when I said that there could be significant stock dilution around the middle of 2023 as cash was running out and that it could be a good time to open a small short position as the short borrow fee rate was just above 6%.

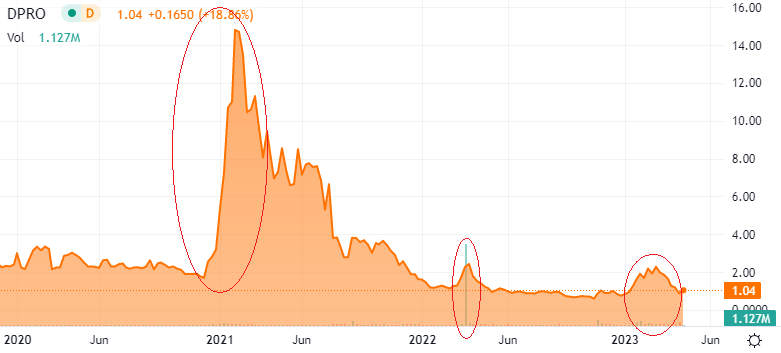

Well, the share price has slumped by over 50% since my previous article as the company closed an $8 million stock offering in late March. In my view, the Q4 2022 financial results of Draganfly were underwhelming and I think there could be further pain ahead for shareholders. That being said, short selling seems dangerous at the moment as the short borrow fee rate is in the double digits again and it takes over two days to cover. Let’s review.

Overview of the recent developments

In case you're not familiar with Draganfly or my earlier coverage, here's a brief description of the business. The company sells delivery, medical response, and rescue drones among others, and is the oldest commercial drone maker in the world, having started operations in 1998. Draganfly also offers flight services, and artificial intelligence and data solutions and it has a total of 23 issued patents.

{kind=link}

In its latest corporate presentation , the company claims to be a "leading and rapidly growing drone manufacturer and solutions provider" as well as being "recognized as a leading North American drone solutions provider".

{kind=link}

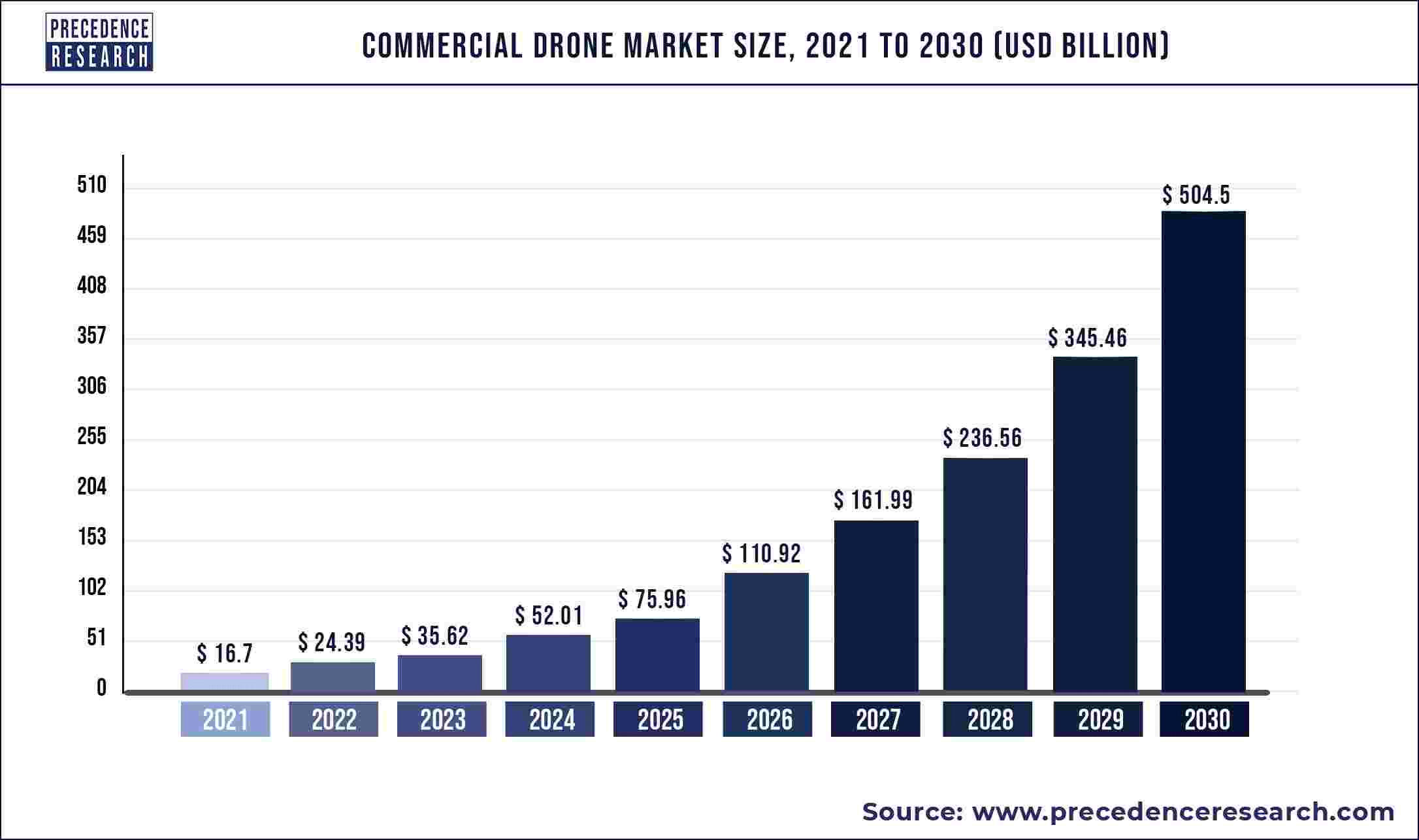

While all of this might sound impressive at first sight, keep in mind that many companies claim to be leaders in their fields despite having an inconsequential market share and looking at Draganfly’s financial results over the past several years, I would say that the company has squandered its first mover advantage. According to data from Precedence Research , the global commercial drone market was estimated at $24.39 billion in 2022, with North America accounting for 38% of that figure. The market is forecast to grow at a compound annual growth rate ((CAGR)) of over 46% between 2022 and 2030.

{kind=link}

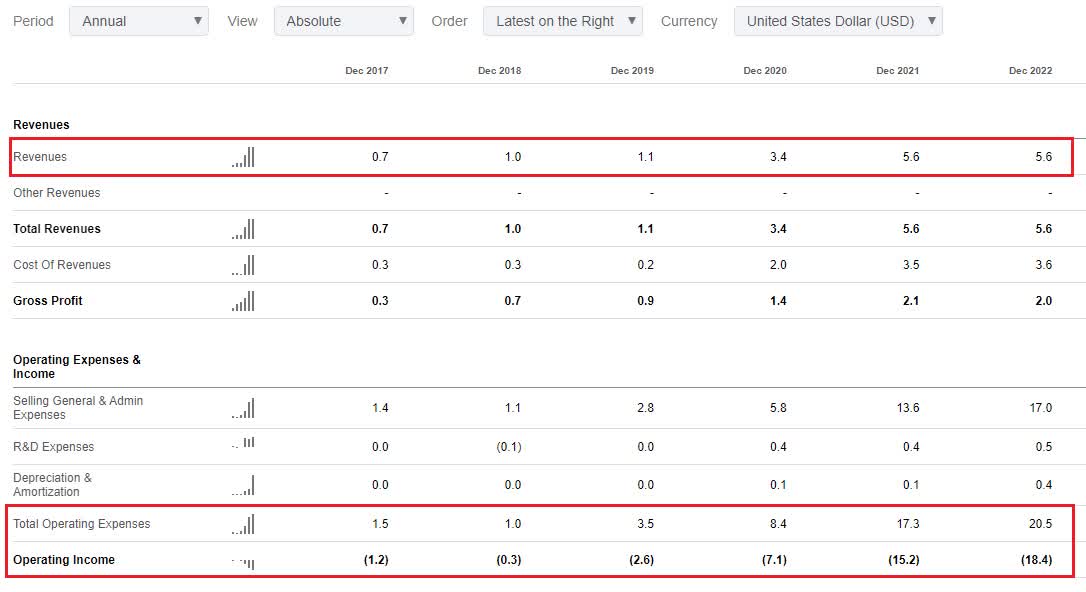

Yet, Draganfly’s public financial results show that annual revenues didn’t surpass the $ 5 million mark until 2022, growing at a CAGR of 51.6% over the past five years. In addition, operating expenses grew at a CAGR of 62.5% over the same period leading to the operating loss to soar from $1.2 million in 2017 to $18.4 million in 2022.

{kind=link}

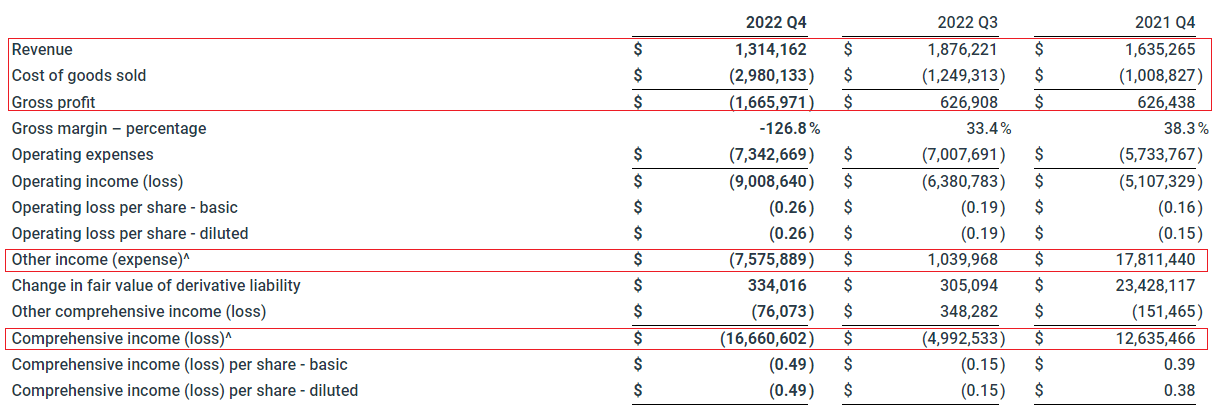

Turning our attention to the Q4 2022 financial results, I think that they were underwhelming as revenues fell by 19.6% year on year to just C$1.31 million ($0.98 million). Services revenues were particularly disappointing as they slumped by 41.2% year on year to just C$0.29 million ($0.22 million). The gross profit margin was negative as Draganfly booked a write-down of inventory of C$1.98 million ($1.48 million) arising from its healthcare data services and deep learning arm Vital Intelligence. In addition, there was a $1.08 million ($0.81 million) expense on impairment for notes receivable as well as a C$6.45 million ($4.82 million) expense for impairment of goodwill and intangibles. All of this boosted the comprehensive loss for Q4 2022 to C$16.66 million ($12.45 million).

{kind=link}

Unfortunately, there is no explanation in the 2022 annual report or the Q4 2022 earnings call about what led to the significant write down of inventory as well as the significant impairment expenses during the period. In addition, I find it disappointing that there was no explanation of what happened with a January 2022 deal for a minimum C$9 million ($6.75 million) manufacturing agreement for an AI consumer companion robot drone with a company named Digital Dream Labs. During the Q3 2022 earnings call , Draganfly Chief Operating Officer Paul Mullen said that the company expected to start seeing revenue from this partnership through early Q1 2023.

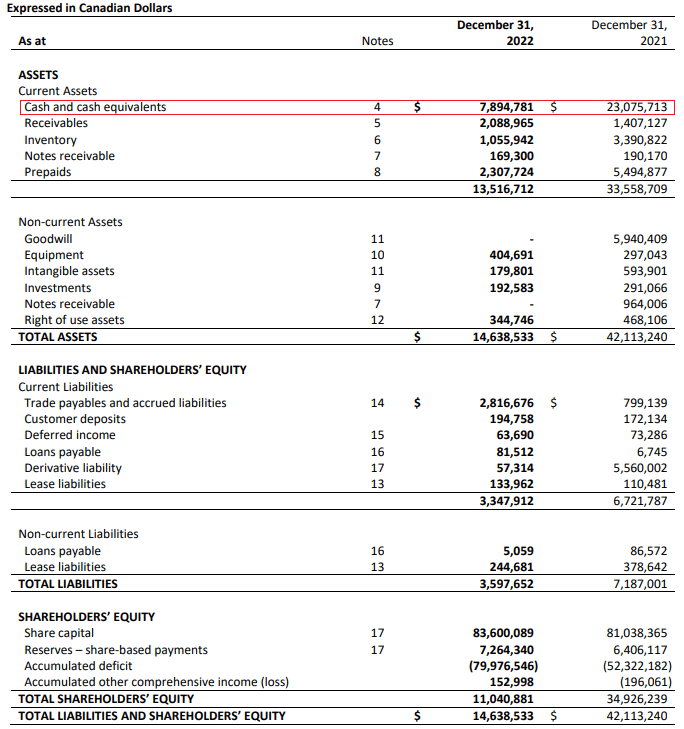

Moving on to the balance sheet, cash used in operating activities during Q4 2022 came in at C$4.02 million ($3 million) and this was the main reason for cash and cash equivalents slumping by C$3.83 million ($2.86 million) quarter on quarter to just C$7.89 million ($5.89 million) as of December. Overall, Draganfly is burning through its cash reserves faster than I anticipated and I find it unsurprising that the company decided to tap the equity market on March 31. It’s an asset-light business and there aren’t any notable tangible assets that can be sold to raise cash.

{kind=link}

Looking at what to expect for 2023, Draganfly said during its Q4 2022 earnings call that its numbers were constrained by its manufacturing capacity and that this should improve with the launch of its facility in British Columbia in March. Yet, I think this projection sounds overly optimistic considering how much revenues fell in Q4 2022, and I expect the company to struggle to surpass $5 million in revenues in 2023. Even if I’m wrong and revenues double compared to 2022, the company would still be deep in the red assuming the gross margin stands at about 33%. In my view, another significant stock increase is likely to take place by the end of 2023 as the cash burn rate stays about $1 million per month.

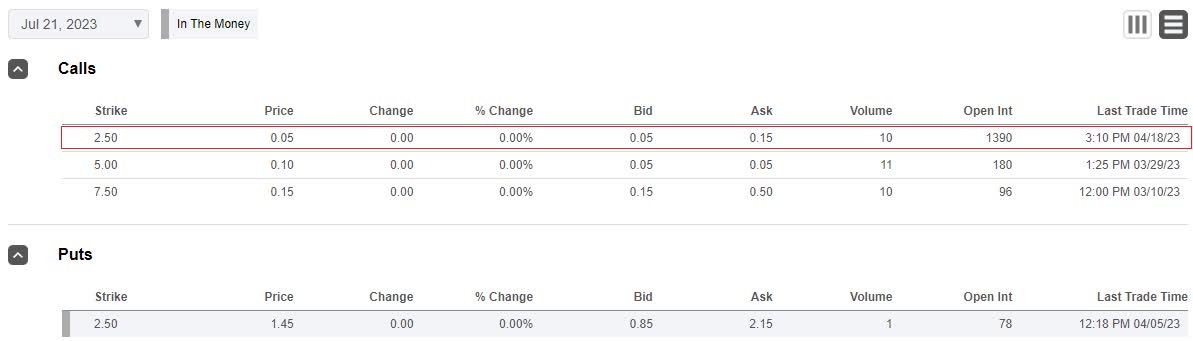

So, how do you play this? Well, short selling seems dangerous as data from Fintel shows that the short borrow fee rate stands at 13.58% as of the time of writing. This is more than double compared to my February article. In addition, the short interest is over 5% of the float and it takes more than two days to cover. Hedging opportunities are limited as the lowest available strike price for call options is $2.50 at the moment.

{kind=link}

Risks

Looking at the risks for the bear case, I think that there are two major ones. First, a potential increase in sales in Q2 or Q3 thanks to the new British Columbia facility could provide a significant short term boost to the share price. Second, the share prices of microcap companies can increase for spurious and unknown reasons. We've already seen this happen several times here over the past few years.

{kind=link}

Investor takeaway

Draganfly released weak Q4 2022 financial results, and a significant capital increase came sooner than I was expecting. In my view, the company is likely to have a tough 2023 as it struggles to increase sales and keeps burning through about $1 million in cash per month. That being said, I think that the window of opportunity for short selling has closed, and investors should avoid this stock. I probably won't write another article about Draganfly unless there is a major change in the fundamentals of the business, or its market valuation spikes again.

For further details see:

Draganfly Is Likely To Have Another Tough Year, But Short Selling Seems Dangerous