DREUF - Dream Industrial: Cheap But Risky

2024-01-03 19:20:12 ET

Summary

- Dream Industrial REIT is a discounted industrial REIT in Canada with a forward P/FFO of 13.65X, making it an interesting investment opportunity.

- The REIT owns 322 industrial assets, mostly in Canada and Europe, with a high occupancy rate of 97.2%.

- Dream has potential for growth through marking leases to market and has a strong history of same-store NOI growth.

We are continuously scouring the REIT universe for opportunistic investments, particularly in fundamentally advantaged sectors. One of the sectors we like most at a property level is industrial, but the sector is getting rather pricey with an average P/FFO multiple of 19.7X.

As discussed in a recent article , Canada often offers lower valuation REITs, so our search for industrial value has led us to Dream Industrial Real Estate Investment Trust (DIR.UN:CA) (DREUF). It does indeed trade at a discounted valuation with a forward P/FFO of 13.65X making it an interesting candidate for further diligence.

In this article, we will discuss its property portfolio, balance sheet, growth prospects, management, and our overall take on the stock.

Property portfolio

Dream Industrial owns 322 industrial assets, mostly in Canada and Europe with a total of 70.6 million square feet. That spots average building size at just over 219K which is quite large, but typical of publicly traded REIT portfolios which tend to lean toward larger assets.

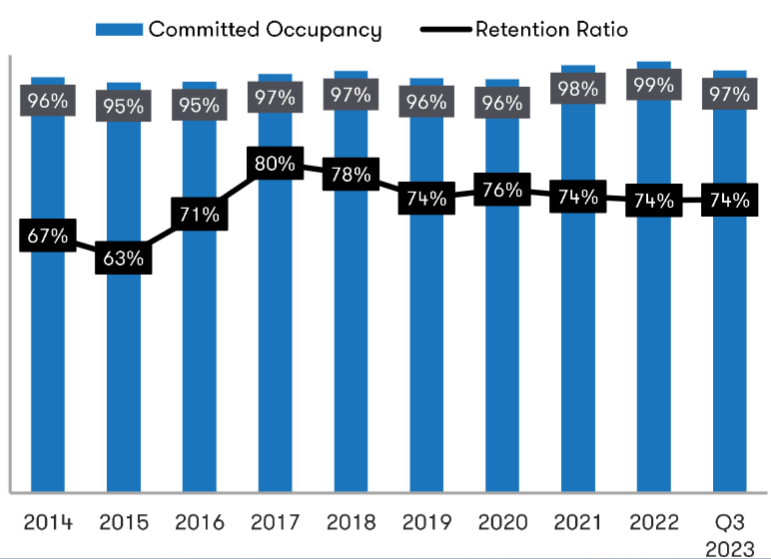

These properties are 97.2% occupied which is high by historical standards but typical of the industrial sector today. The low vacancy in the sector is one of the key reasons why landlords have the power to push rents up so aggressively.

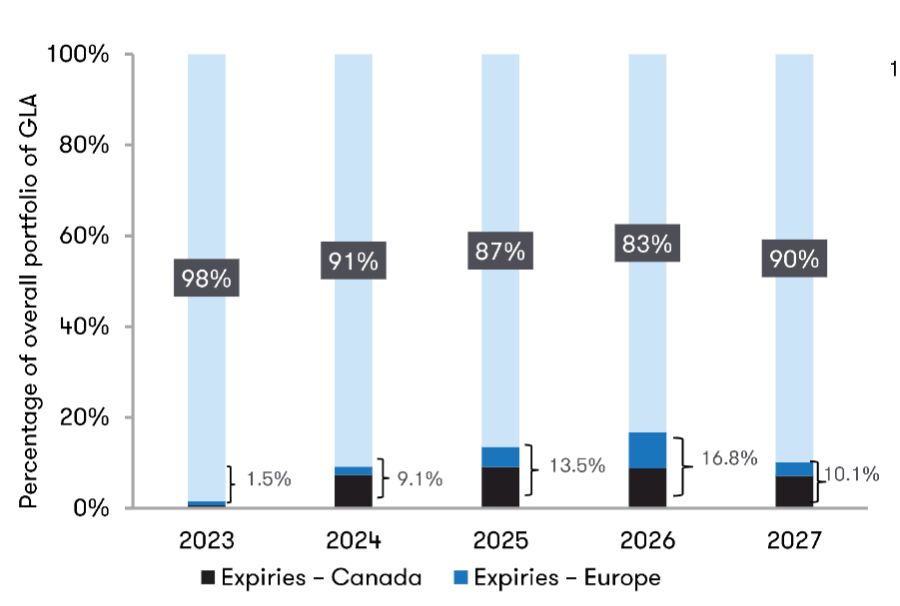

Dream's weighted average lease terms are moderate to long resulting in a laddered expiry schedule with roughly 10% of square footage rolling each year.

{kind=link}

The quality of Dream's portfolio looks good with a concentration on logistics and distribution which are the institutionally preferred types. I personally like light manufacturing space as well, but that tends to trade at significant discounts to distribution.

Tenants appear to be happy with the properties as retention ratios are consistently high in the 70s.

{kind=link}

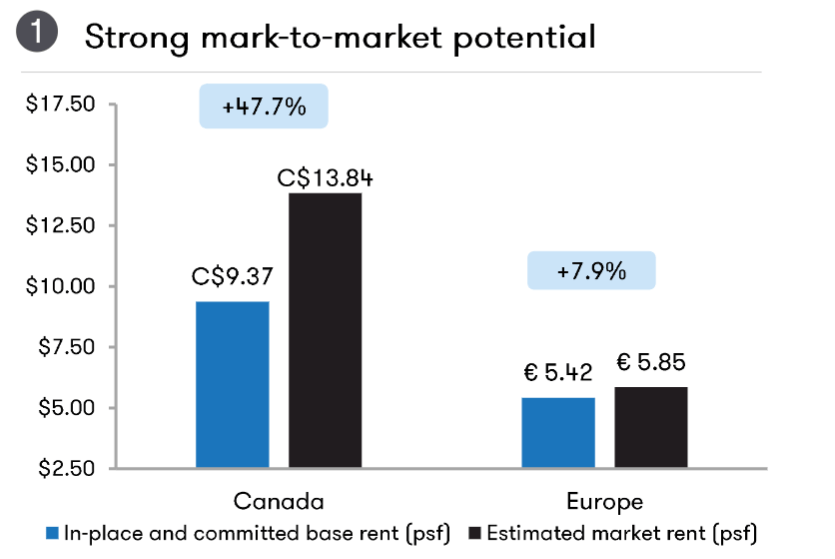

Growth from mark to market

Much like the U.S. REITs, Dream has a significant opportunity to mark leases to market. In other words, existing rental rates are substantially below where leases are getting signed today.

On average, Dream has a roughly 30% upside in rental rates across the portfolio. The gap in Canada is significantly larger than it is in Europe.

{kind=link}

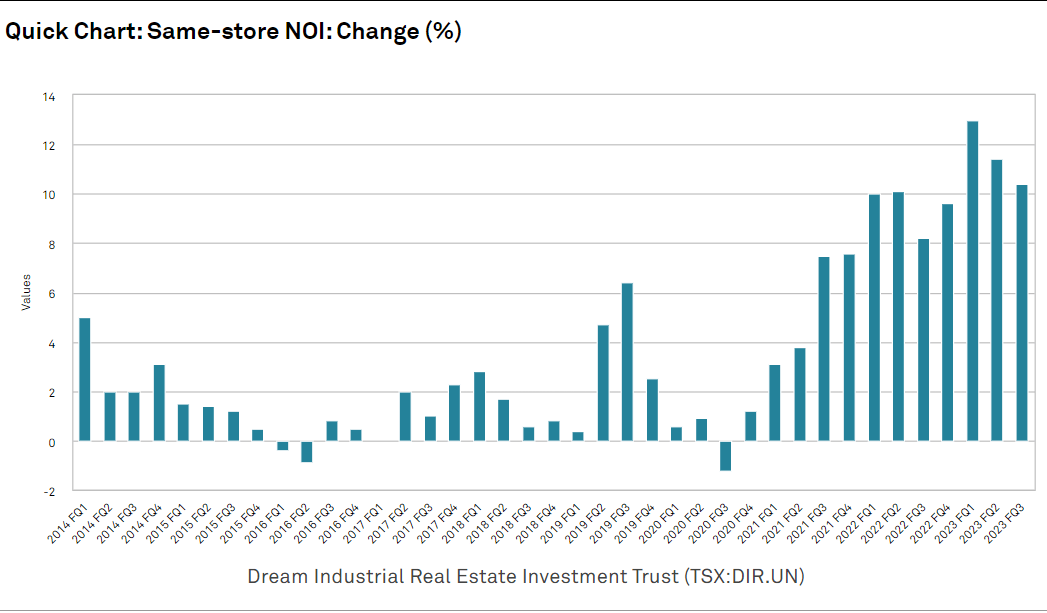

Dream has a fairly strong history of same-store NOI growth.

S&P Global Market Intelligence

{kind=link}

It has clearly accelerated in recent years, largely due to the spike in market rental rates. While market rate growth is slowing, the existing rates take as long as 10 years to fully work through due to lease terms. Thus, I expect same-store NOI growth to remain quite strong for the next 5 years.

Growth from developments

Dream has quite a few projects in the works.

{kind=link}

3 factors in the above table are notable:

- 6.8% development yield.

- $554 million total cost.

- $347 million cost already incurred.

At a 6.8% development yield the spread over cost of capital is relatively small so I wouldn't anticipate a large amount of accretion from capital spent. However, the cost incurred figure represents capital that is currently producing no income so as that gets delivered it will create a nice pop in FFO relative to current FFO levels.

Dream has a market cap of just under $4B CAD, so a pipeline of $554 CAD is quite significant as a percentage.

Balance sheet

While Dream is investment grade, the most impressive aspect of its balance sheet is a weighted average interest rate of 2.33%.

{kind=link}

There are 2 reasons it has been able to achieve such a remarkably low cost of debt:

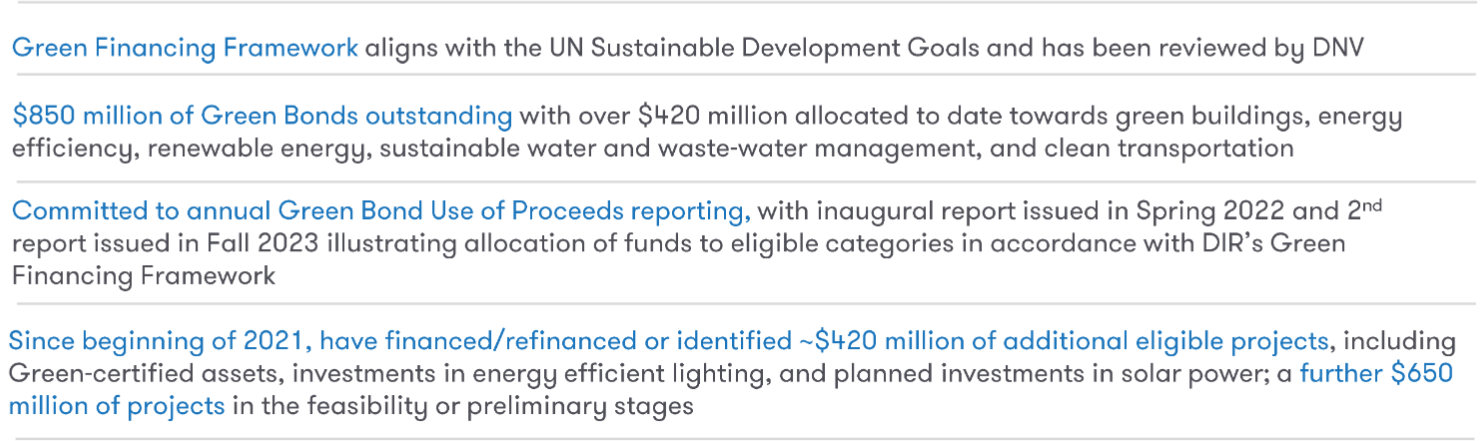

- European debt is cheaper.

- Green bonds.

Much like Prologis, Inc. ( PLD ) or STAG Industrial, Inc. (STAG). Dream puts a lot of solar panels on the roofs of its warehouses. These projects in themselves offer a decent return with IRRs in the 8% to 10% range.

{kind=link}

Perhaps the bigger benefit is that it provides access to Green bonds. Dream has accessed quite of bit of really cheap Green bond money.

{kind=link}

While having extremely cheap debt is unequivocally a good thing overall, it presents a risk in terms of growth to FFO/share.

Since the existing debt is so cheap relative to today's interest rate environment, it will almost certainly have to be rolled up to a higher rate upon refinancing. Dream's debt term on average is only 3 and as these roll, I would imagine at least a couple of hundred basis points higher cost.

The mark to market growth is greater in magnitude than the increased interest expense, so it is not concerning from a solvency standpoint, but it does mitigate the growth rate.

Performance

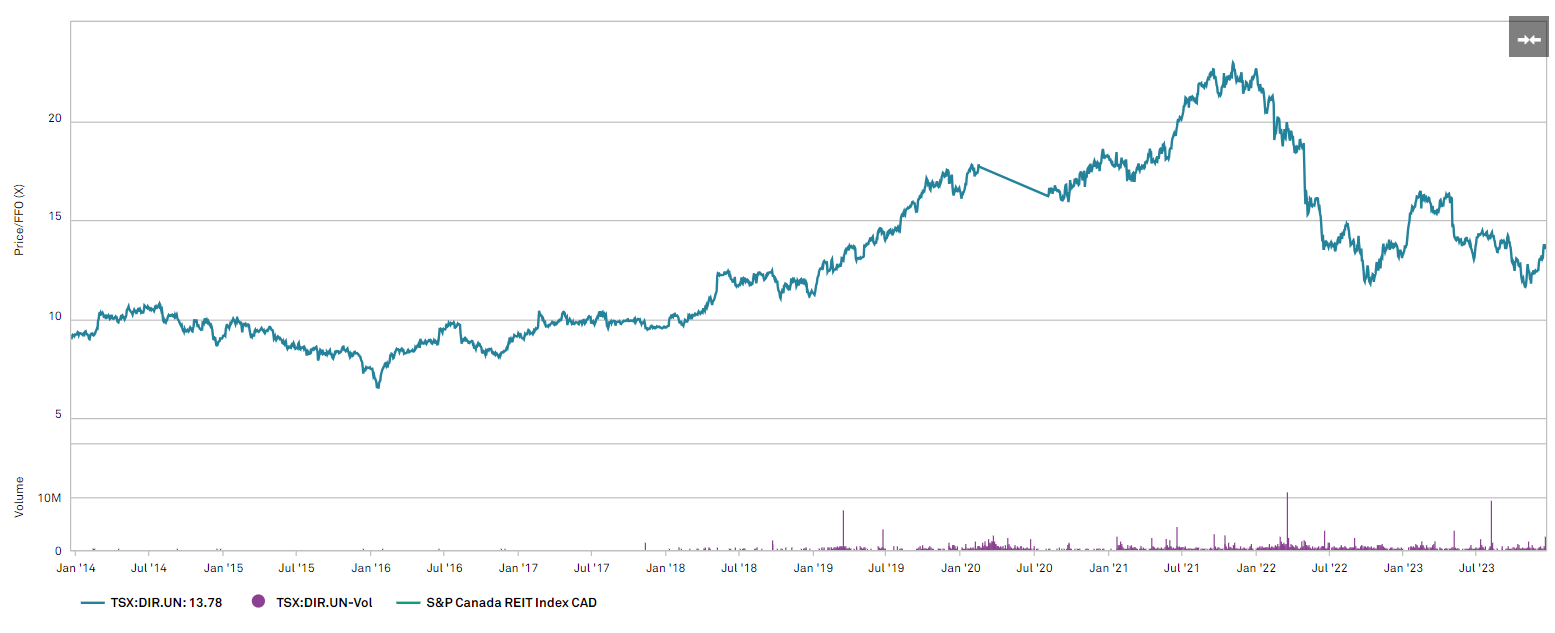

Dream has done fairly well over the last 10 years with a 212% return that significantly beats the Canadian REIT index.

S&P Global Market Intelligence

{kind=link}

Some of this performance was the result of multiple expansions as Dream used to trade below 10X.

S&P Global Market Intelligence

{kind=link}

Returns that come from multiple expansions are less repeatable than returns that are matched by earnings per share growth.

Another significant portion of the returns is likely attributable to the general tailwinds of the industrial sector. It is rather rare to find an industrial REIT that didn't outperform the REIT index.

So it was a nice return, but I wouldn't read into it as a sign of quality.

Management - yellow flag

Dream's properties and balance sheet are strong, but I do have some concerns about its management, specifically the compensation structure.

Management is compensated by the size of the company and transaction volume. From the annual report:

"Base annual management fee calculated and payable in cash on a monthly basis and in arrears on the first day of each month, equal to 0.25% of the historical purchase price paid (including the amount of all hard and soft construction costs) by the REIT for the North American Properties"

In addition to the base fee which is based on size, management earns fees for buying properties.

"Acquisition fee equal to (i) 1.0% of the historical purchase price of a North American Property, on the first $100 million of North American Properties and, prior to the Separation Date, European Properties acquired in such fiscal year; (ii) 0.75% of the historical purchase price of a North American Property on the next $100 million of North American Properties and, prior to the Separation Date, European Properties acquired in each fiscal year; and (iii) 0.50% of the historical purchase price on North American Properties and, prior to the Separation Date, European Properties in excess of $200 million in each fiscal year."

In the most recent quarter, G&A plus advisory fees were just under 7% of revenue. This is a fairly normal amount of expense for a company of this size, so I don't take issue with the magnitude of compensation, but rather the incentivization of it.

Since fees are directly tied to property purchases and the size of the company, it incentivizes management to grow for the sake of growth. It is impossible to prove motivation, but the numbers do hint to me that there is some non-accretive growth going on.

In particular, I would point to 2 data points.

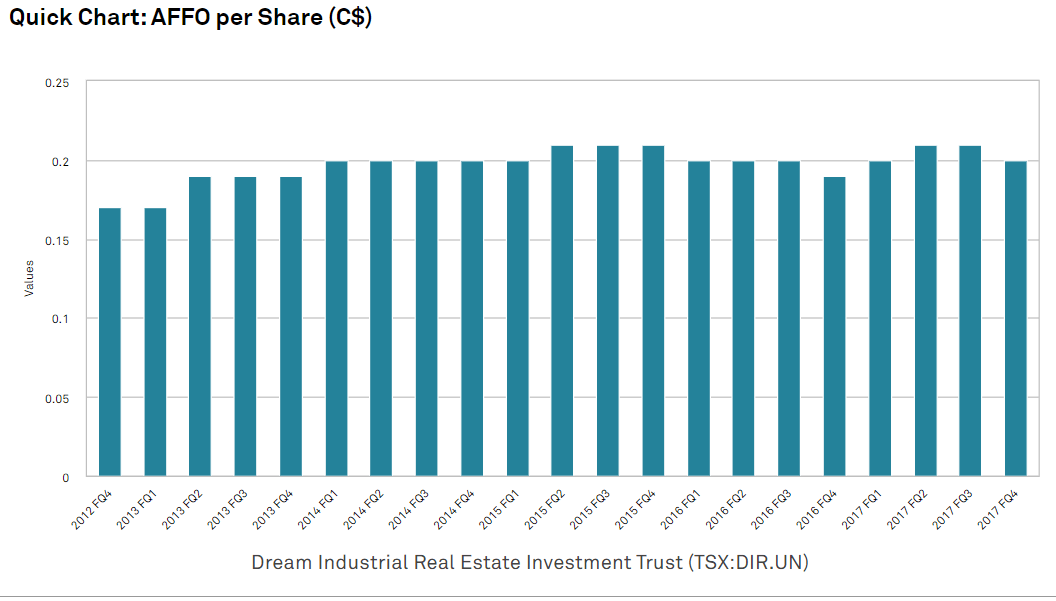

- AFFO/share growth is weak given how strong same-store NOI growth has been in the sector.

S&P Global Market Intelligence

{kind=link}

- Share count is increasing rapidly.

S&P Global Market Intelligence

{kind=link}

It stands to reason that a management team that gets compensated by volume would want to issue tons of shares and buy properties whether or not it is accretive to AFFO/share.

Please note that these terms are fairly common for external management. In many cases, it turns out to not be a problem at all. The reason for my elevated concern here are the terms in combination with the exploding share count. I see this as potential evidence that incentives might not be entirely aligned with shareholders.

Overall take

The valuation is nice, and the properties are strong. Marking rents to market rates should provide growth for at least 5 years.

However, the NOI growth does not seem to be translating well to AFFO/share growth, so I feel like the discounted multiple is largely warranted. In my opinion, Dream is trading roughly at fair value. Perhaps it is worth owning for the dividend yield, but for my goals of maximizing total return, I think there are significantly better options in the industrial sector.

For further details see:

Dream Industrial: Cheap But Risky