DREUF - Dream Industrial: Sweet Dreams Are Made Of These

2023-03-20 09:37:03 ET

Summary

- The REIT can realize 53% average lease renewals in its Canadian portfolio in 2023.

- The REIT has managed to take advantage of very low interest rates with having its debt structured in Europe, more than 100 bps lower than North America.

- The REIT trades at a rare 17% discount to NAV and can realize high spreads over its debt with going-in cap rates being greater than 6%.

Introduction

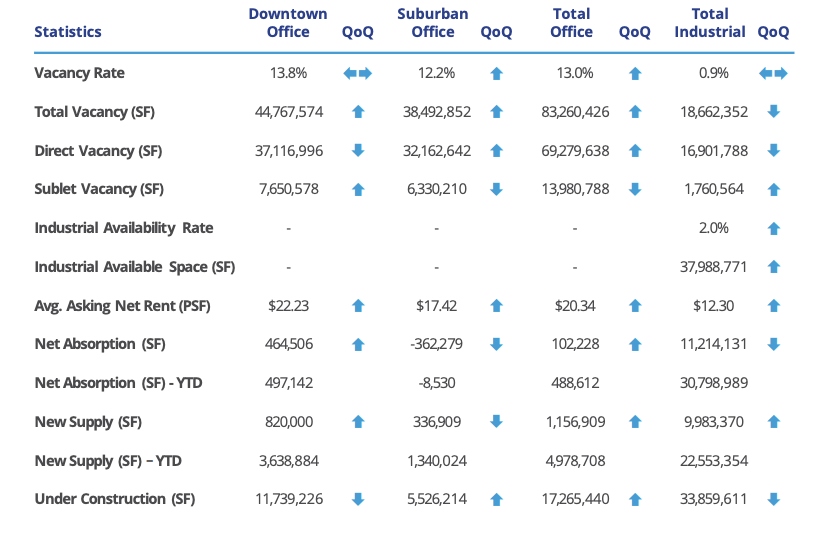

The industrial boom in Canada has continued. The Colliers Market Report for Q3 2022 showed that several markets have availability levels less than half of 2021, and smaller markets such as Waterloo and Victoria are approaching zero vacancy. Vacancy Rates have reached record lows and rental rates per sq. ft have reached record highs. Vancouver became the first market in history to exceed $20 per sq. ft. average asking net rents for industrial space. New supply is only 70% of net absorption which makes for highly imbalanced supply-demand making this very much a landlord market.

{kind=link}

National Market Snapshot Q3 Report 2022 (Colliers Canada)

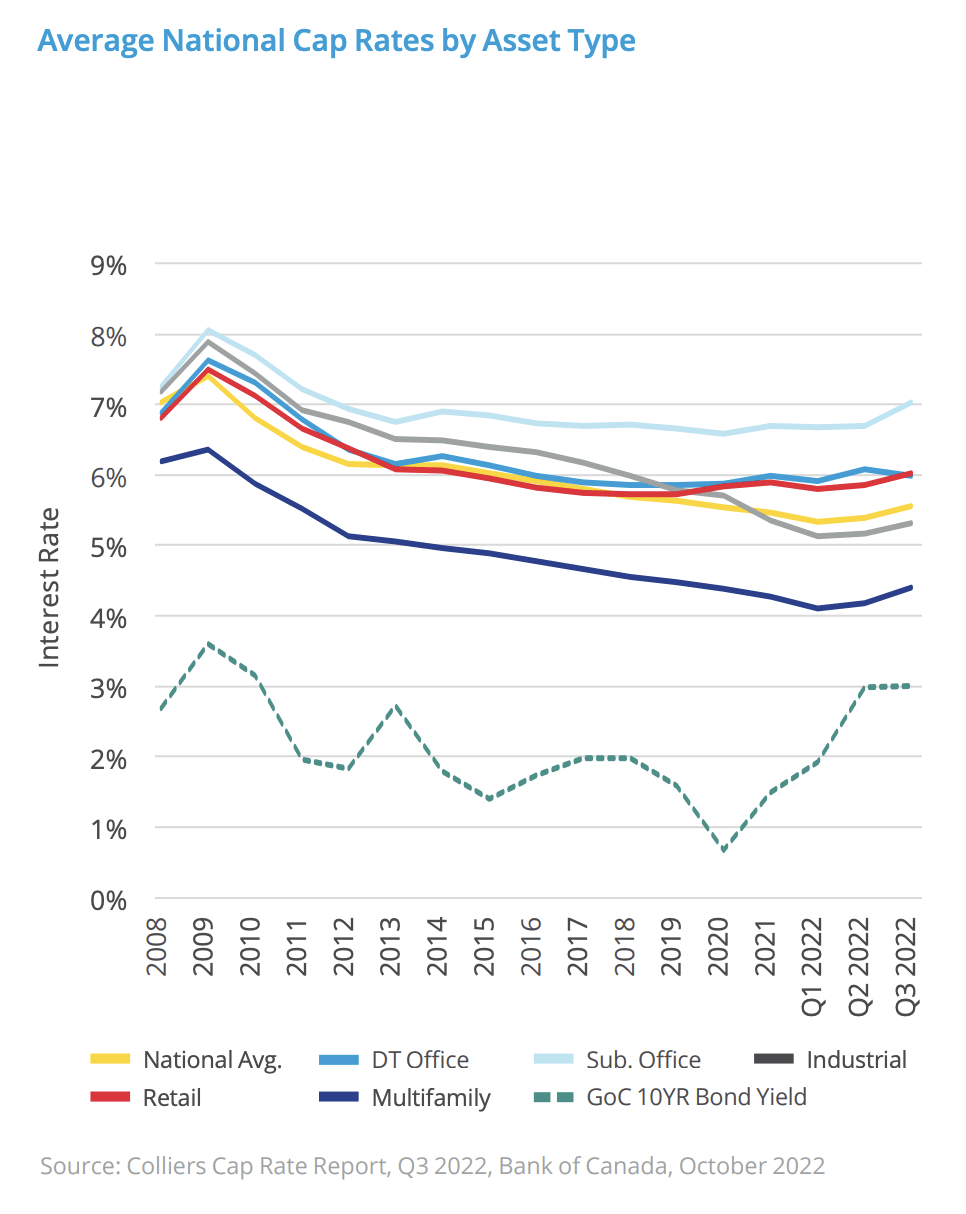

This has been the result of heightened demand for industrial space to accommodate a growing e-commerce platform during the pandemic and has blossomed into a full-blown distribution and logistics network that encompasses millions of square feet. More recently, volatility in the stock market has also prompted a shift to greater investment in the commercial segment as investors look to real estate as a hedge against inflation. The result of this high demand has resulted in low cap rates in the sector. You would be hard pressed to find Class B industrial properties with cap rates over 5%. The spread between the going cap rates and rapidly rising interest rates has become razor thin so one has to dig through the weeds to find value in the space.

{kind=link}

I believe I have found one however in Dream Industrial REIT ( DIR.UN:CA )(DREUF) which is the purpose of this article.

Background

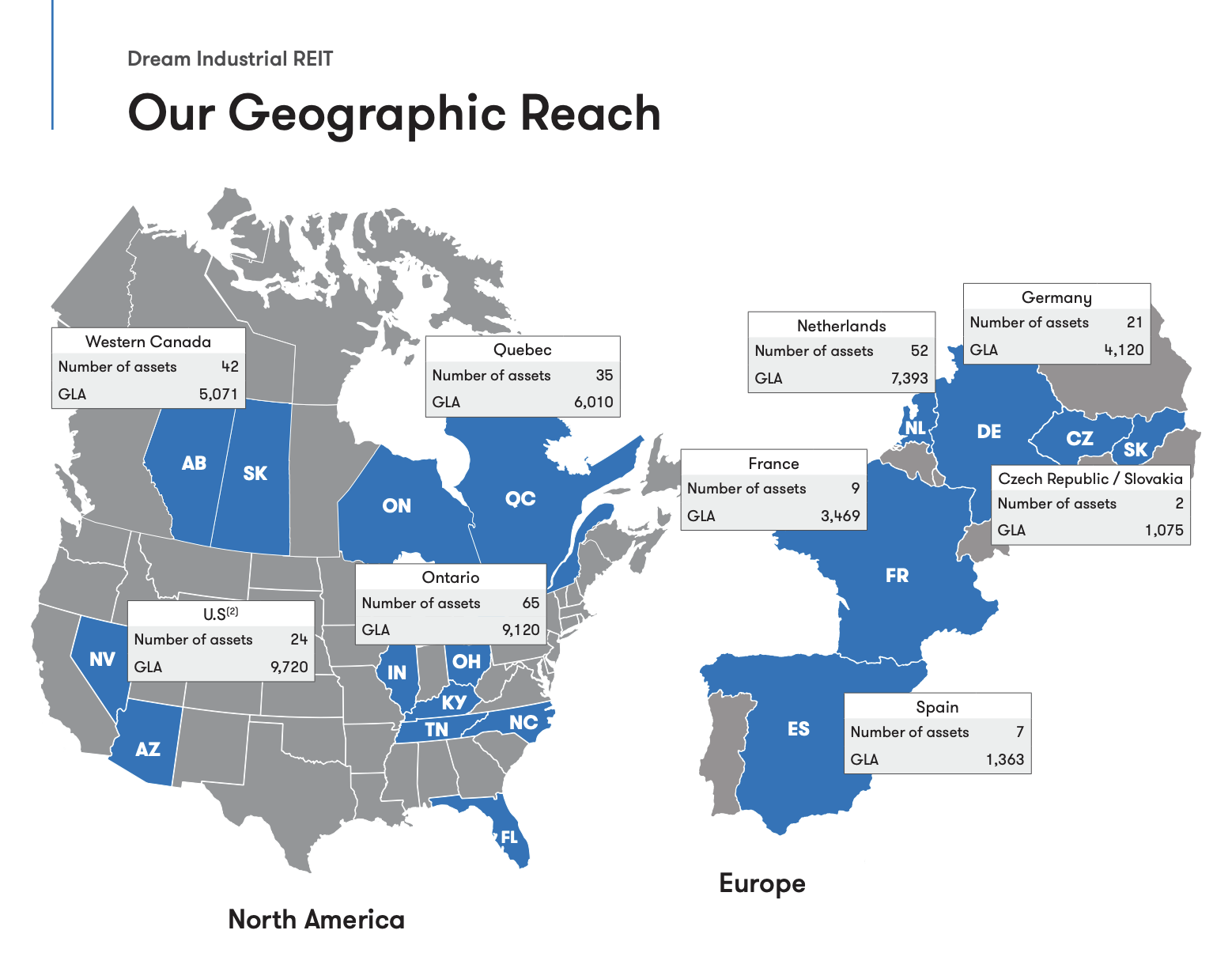

DIR owns 239 industrial assets across the globe with the bulk of these assets in Canada, though the company has aggressively expanded in Europe recently. The REIT is well diversified by geography and class.

{kind=link}

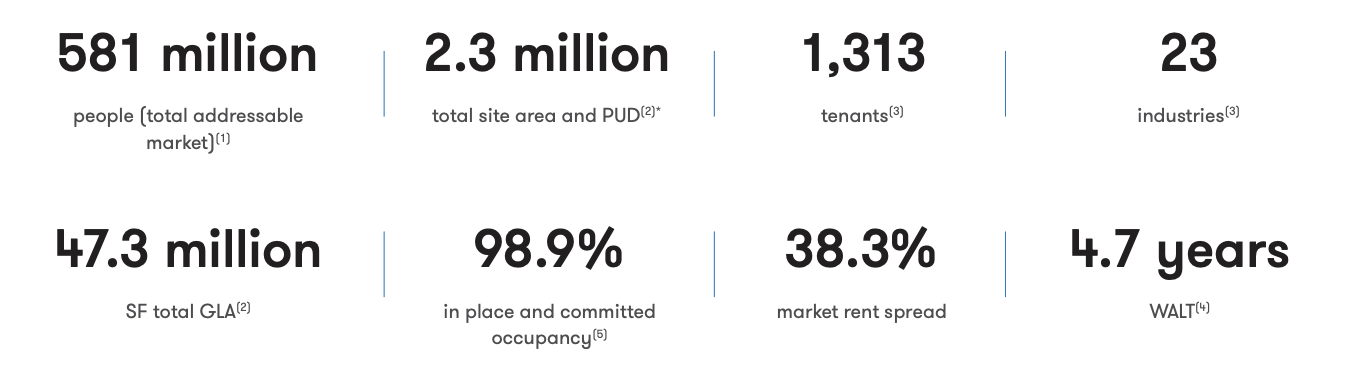

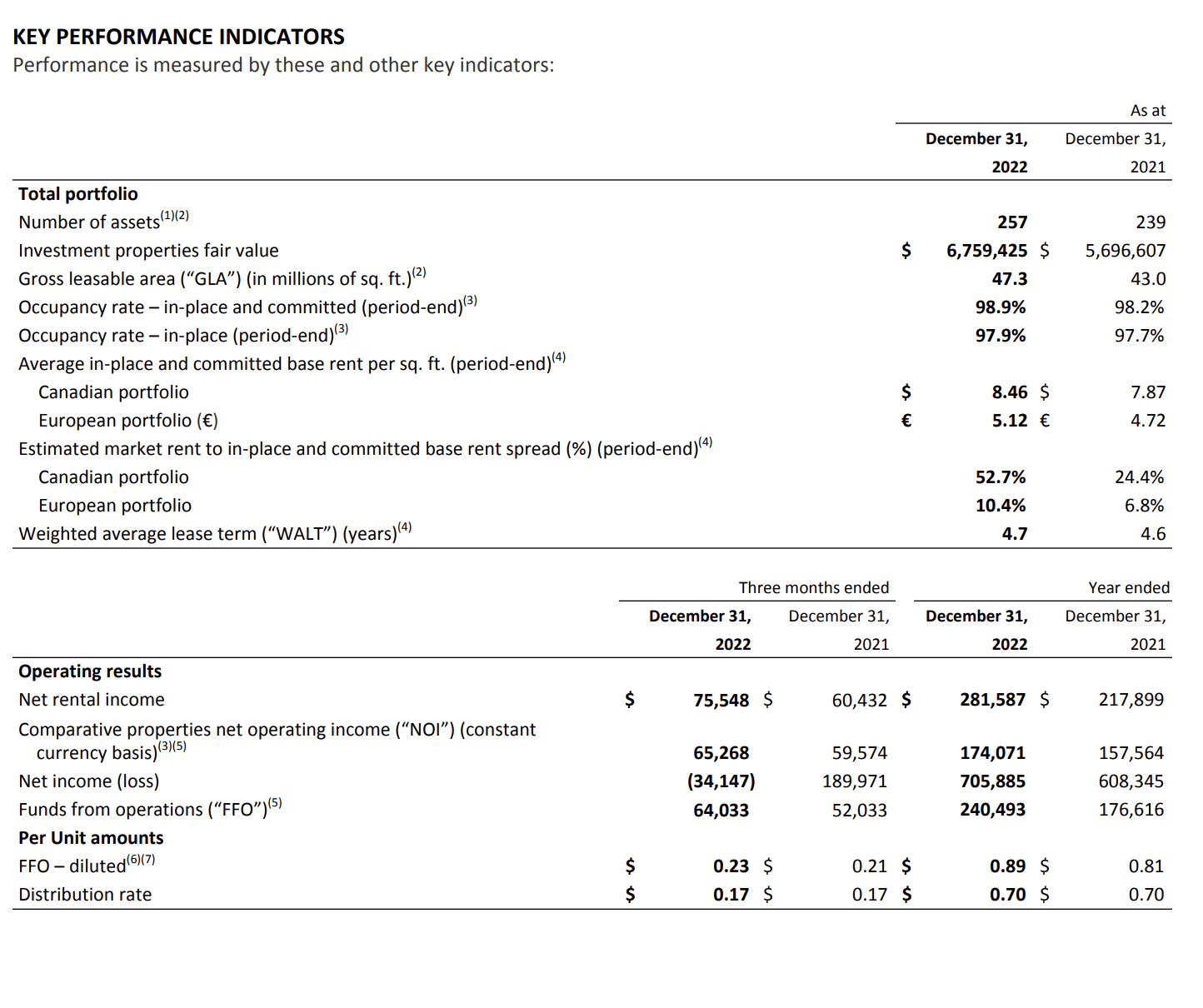

The REIT boasts a ~99% occupancy rate which is just what I like to see. It has a WALT of less than five years which is less than ideal, but given the 38.3% average rent spreads realized in 2022 this number is less concerning.

{kind=link}

{kind=link}

Fiscal 2022 results were nothing short of impressive. Net rental income increased 29% YoY with most of that being driven by increased rents in Ontario and Europe. The increase in rents was primarily driven by high leasing spreads and acquisition activity in 2022. The increased rental revenue led to a 9.9% YoY increase in FFO per share.

{kind=link}

Rental spreads on new and renewed leases where average in-place base rent increased by 10% and 7.6% in Ontario and Quebec respectively, and is almost unheard of in those markets. Below are examples of some of the highest new and renewed leases where average in-place base rents increased in fiscal 2022:

- 130,000 sq ft. of the 600,000 sq. ft. vacancy in Blois, France achieved a 7% spread in November 2022.

- In Ontario, DIR signed 270,000 sq. ft. of renewals achieving an average spread to expiry of 75% and contractual rent growth above 3%.

- In Quebec, DIR signed two renewals for a combined 130,000 sq. ft. space achieving a 201% spread compared to prior rent.

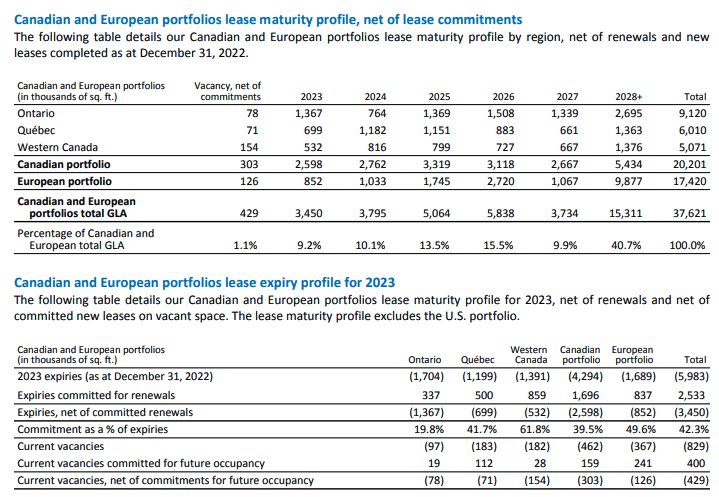

As a result of robust demand on the industrial space, management expects leasing spreads to reach an average of 35% in 2023, but 53% in the Canadian portfolio. 12% of lease renewals come due in 2023 and 28% in the next two years which will greatly improve FFO even if no further acquisitions are completed.

{kind=link}

During 2022 DIR acquired $565 Million income producing assets that added more than 2.6 Million sq. ft. of high quality logistics space in land-constrained markets across Canada and Europe. In November 2022, DIR announced its intention to acquire a 10% stake of Summit Industrial Income REIT ( SMU.UN:CA ) in an all-cash transaction valued at C$5.9 Billion or $23.50/share. The assumption of debt has not been made public. The transaction is a JV agreement with GIC, a global wealth fund, who will own the remaining 90% in Summit. DIR will increase its GLA from 46.5 Million sq. ft. to 69 Million sq. ft.

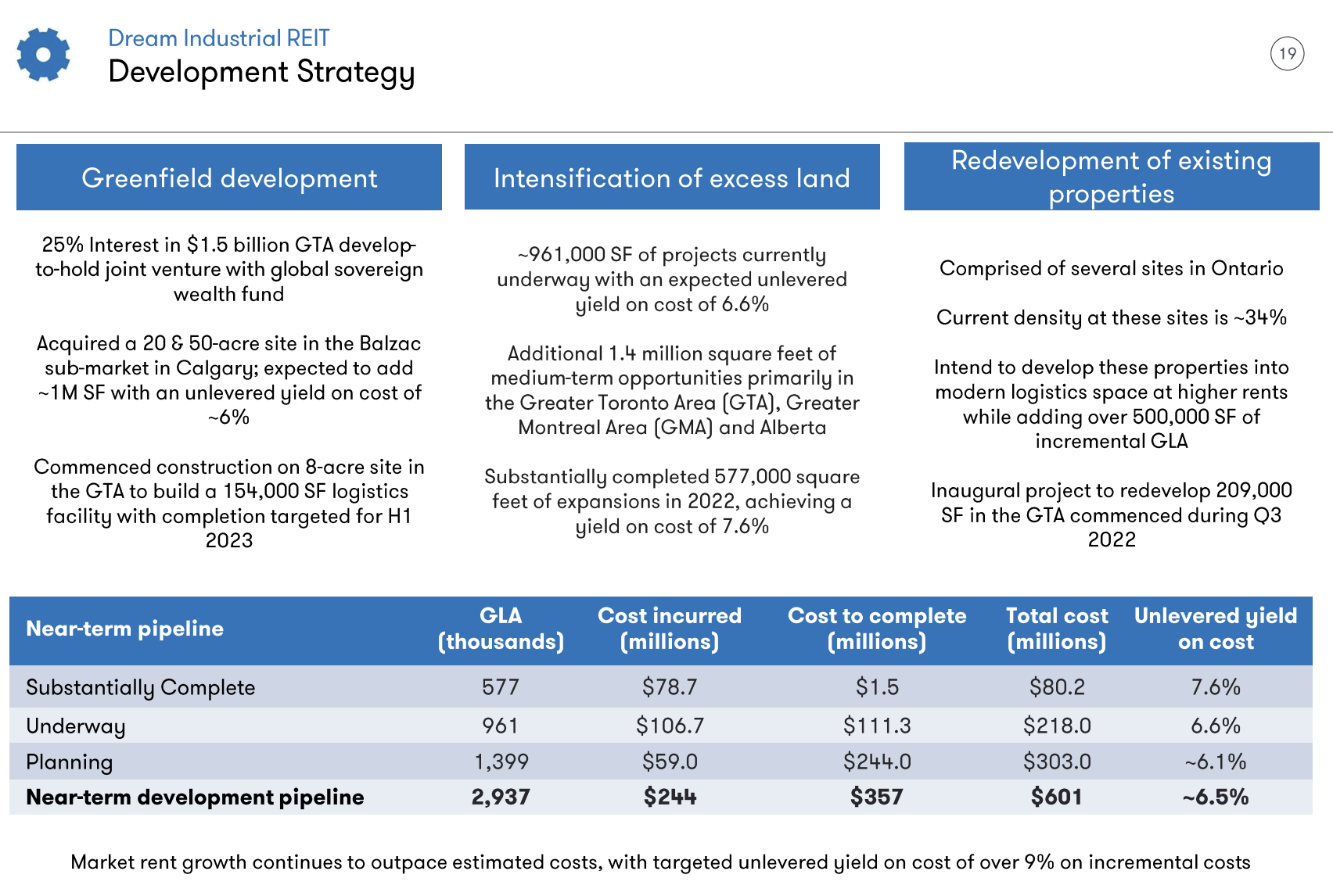

DIR also has 961,000 sq. ft. feet of projects underway across Canada with a total expected cost of $218 Million. Each project expected to deliver unlevered yields over 6% which is greater than the going cap rates for most industrial projects these days. As a result of acquisitions/developments there should be little doubt revenues will greatly improve once again for 2023.

{kind=link}

Valuation

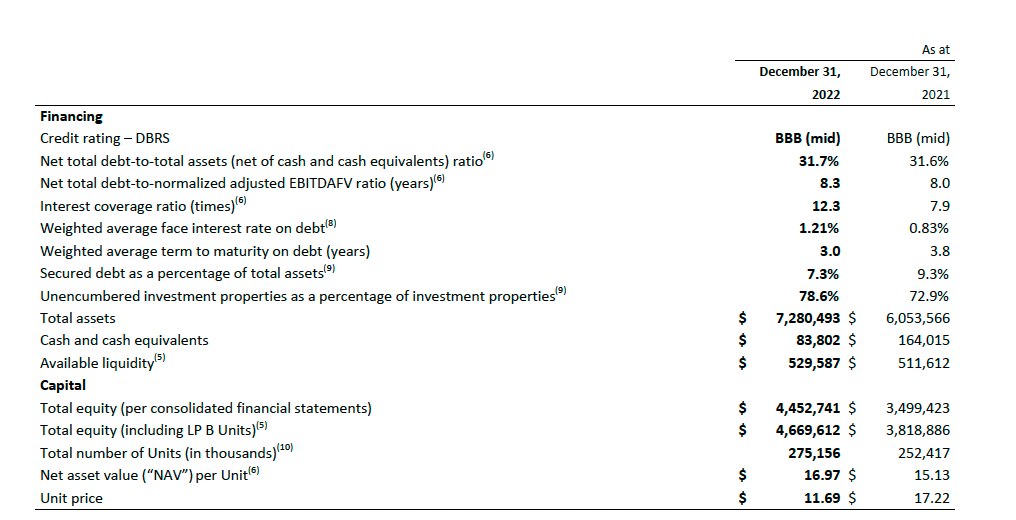

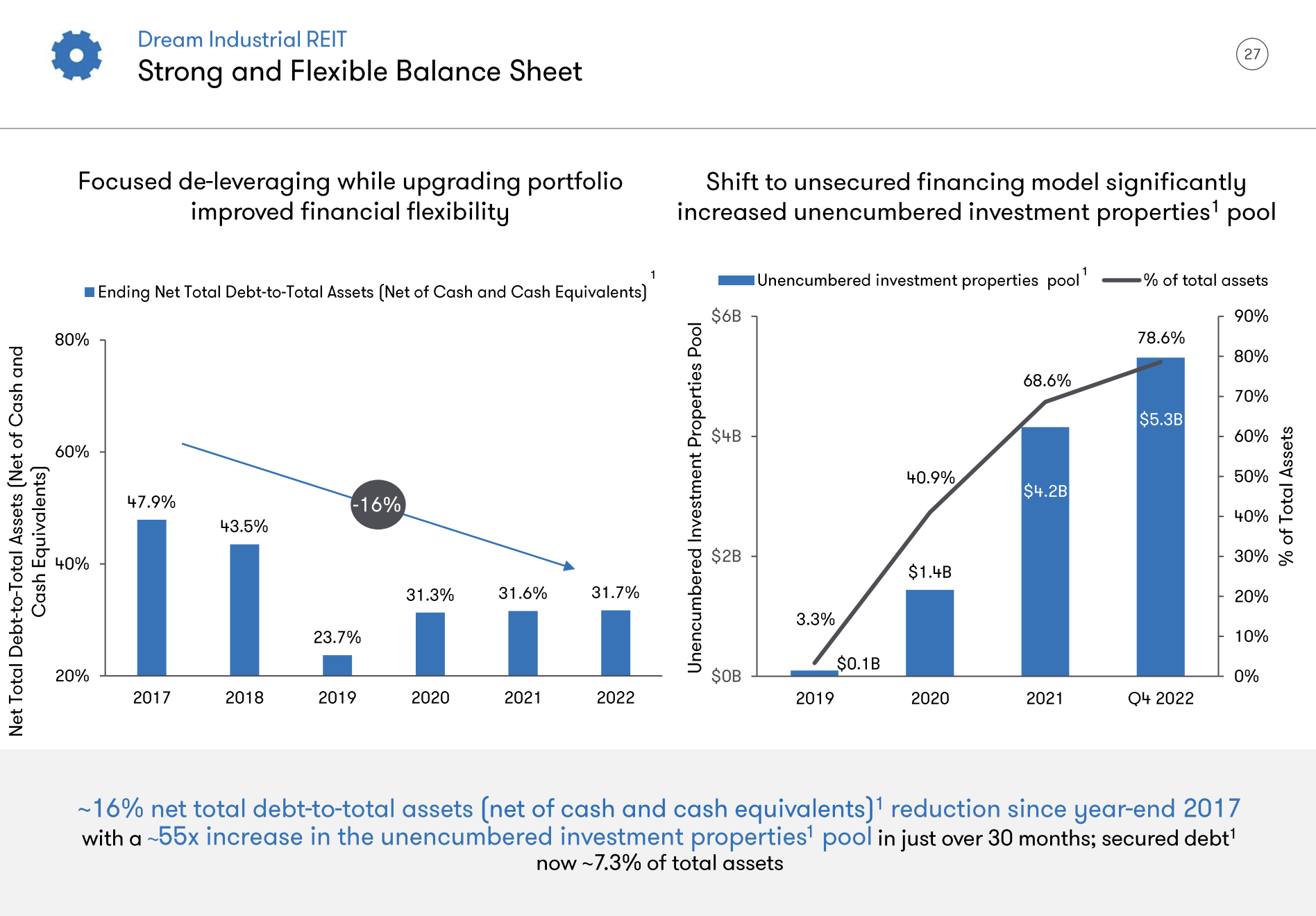

Net asset value increased by 12% YoY as a result of increased market rents and acquisitions. As I have mentioned in previous articles NAV is as much an art as a science and is very sensitive to the inputs. Most notably the cap rates, but your estimate will be all the more sensitive the higher leverage is. In this case debt to assets is fairly conservative at ~32%.

{kind=link}

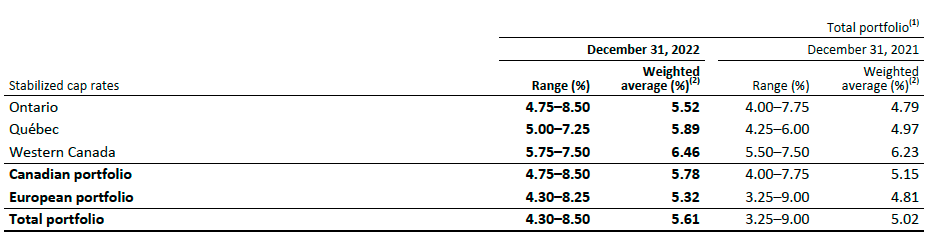

The cap rates DIR has used to value its portfolio are more than fair and actually more aggressive than with what were provided in the Colliers Canada Cap Rate Report Q3 2022 . Although the cap rates to value properties might have been a tad aggressive, the purchase of Summit was also a tad rich at ~27x FFO where DIR trades at only half that. However DIR only bought a 10% stake and the management fees it collects on the properties will make the premium paid dissipate over time. Therefore, ~$17/NAV seems more than fair which puts DIR at a 17% discount to NAV.

{kind=link}

Toronto

{kind=link}

Ontario

Q3 2022 Cap Rate Report (Colliers Canada)

Vancouver

Q3 2022 Cap Rate Report (Colliers Canada)

Calgary

Q3 2022 Cap Rate Report (Colliers Canada)

Edmonton

Q3 2022 Cap Rate Report (Colliers Canada)

Ottawa

Q3 2022 Cap Rate Report (Colliers Canada)

The REIT however has gotten to be the more expensive choice within its peer group aside from Rexford, but most of its other peers, especially Stag, are concentrated in more "tier two" assets.

| Company |

| Ticker |

| P/FFO |

| Dividend Yield |

| Dream Industrial REIT |

| ( DIR.UN:CA ) |

| 15.73x |

| 4.95% |

| Stag Industrial |

| ( STAG ) |

| 14.47x |

| 4.61% |

| Rexford Industrial |

| ( REXR ) |

| 29.0x |

| 2.67% |

| Nexus Industrial REIT |

| ( NXR.UN:CA ) |

| 11.92x |

| 6.65% |

| Pro REIT |

| ( PRV.UN:CA ) |

| 11.43 |

| 7.83% |

Risks

Rising rates in Canada is something no REIT has been immune to as financing costs is such a large expense and can have a dramatic impact on FFO. However rising rates are not going to impact all REITs equally.

One of the biggest things to look at is leverage. If looking at DIR purely on a Net Debt-to-Gross Book Value, it would appear the most conservatively financed in its peer group. On the other hand on a Net Debt-to-Adjusted EBITDA basis it appears among the least other than Pro REIT.

| Company |

| Ticker |

| Net Debt to- Adjusted EBITDA |

| Net Debt-to- Gross Book Value |

| Pro REIT |

| ( PRV.UN:CA ) |

| 9.8x (annualized) |

| 49.82% |

| Dream Industrial REIT |

| ( DIR.UN:CA ) |

| 8.3x |

| 31.70% |

| STAG Industrial |

| ( STAG ) |

| 5.2x |

| 40.0% |

| Nexus REIT |

| ( NXR.UN:CA ) |

| 5.33 |

| 43.7% |

Low vacancy rates and rapidly rising rental rates in the Canadian Industrial market provide ample confidence that assets could be sold at or above book value and make investors whole if the REIT failed to make its mortgage payments. However, that seems extremely unlikely.

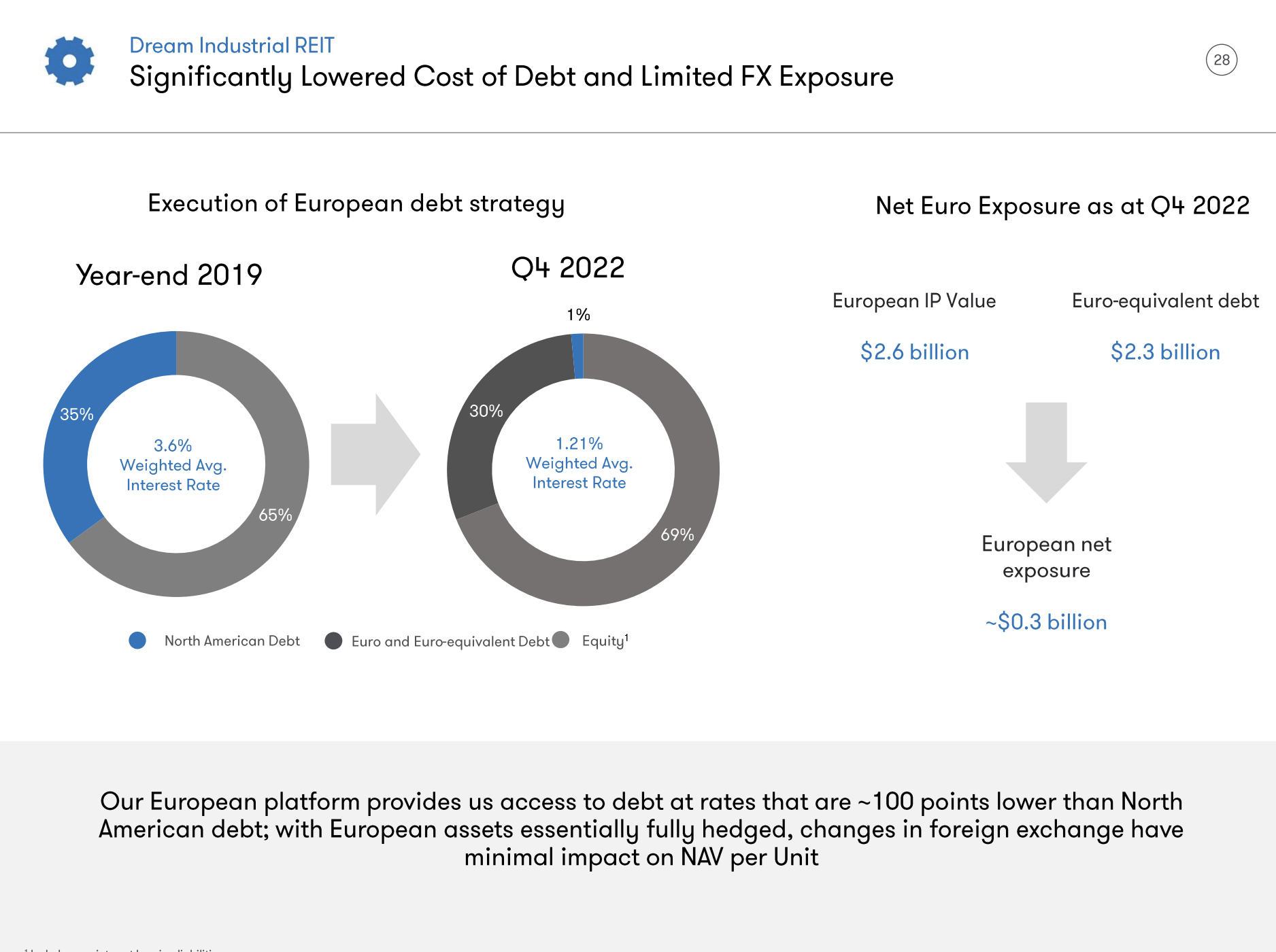

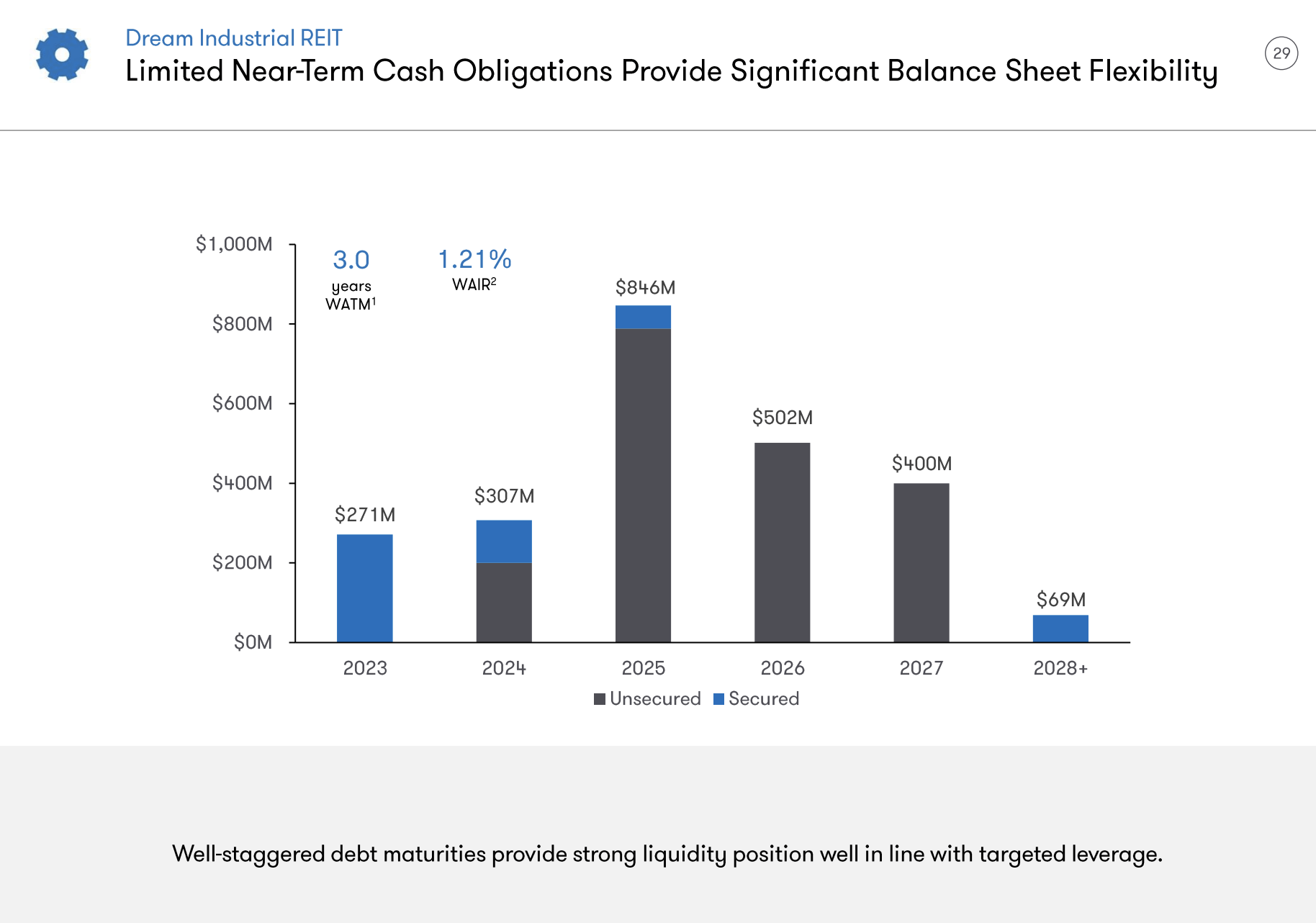

Although 8.3x Net Debt to-Adjusted EBITDA is a little on the high side, the REIT has benefited from very low interest rates as a result of having 69% of its debt structured in Europe where it has been taking advantage of lower rates than it would find in Canada. The interest rate savings have been more than 100 bps. At 2022 FYE, the weighted average interest rate it was paying on debt was 1.21%. You would be hard pressed to find a single North American REIT that had debt on the books at 2022 FYE with rates this low. Furthermore, with 34% of its portfolio in Europe or $2.6 Billion in IP value, this debt acts as a natural hedge against FX rates which minimizes the impact on NAV.

{kind=link}

DIR does have a fairly short-dated debt maturity profile at only three years which is more conducive to a lower rate environment but has only 24% of it due in the next 24 months. 35% is due in 2025 which skews the average to the left. There is little doubt that interest rates will have an impact on FFO over the next couple years, but the negative impact should be more than offset as the REIT renews leases coming off its current book at much higher rates and as new developments come on line with yields of at least 6%. In addition, DIR's unencumbered assets represent 78% of total assets which acts as an additional source of liquidity. For these reasons the leverage profile is not as concerning as it appears.

{kind=link}

{kind=link}

Verdict

If the above points were not enough to convince you about the investment quality of this REIT just remember Dream Unlimited ( DRM:CA ) was the same parent company of Dream Global REIT which was sold to The Blackstone Group in December 2019 in an all-cash transaction valued at $6.2 Billion which richly rewarded shareholders. The group has a history of delivering strong returns to shareholders even going as far as to beat the market indices at various points.

{kind=link}

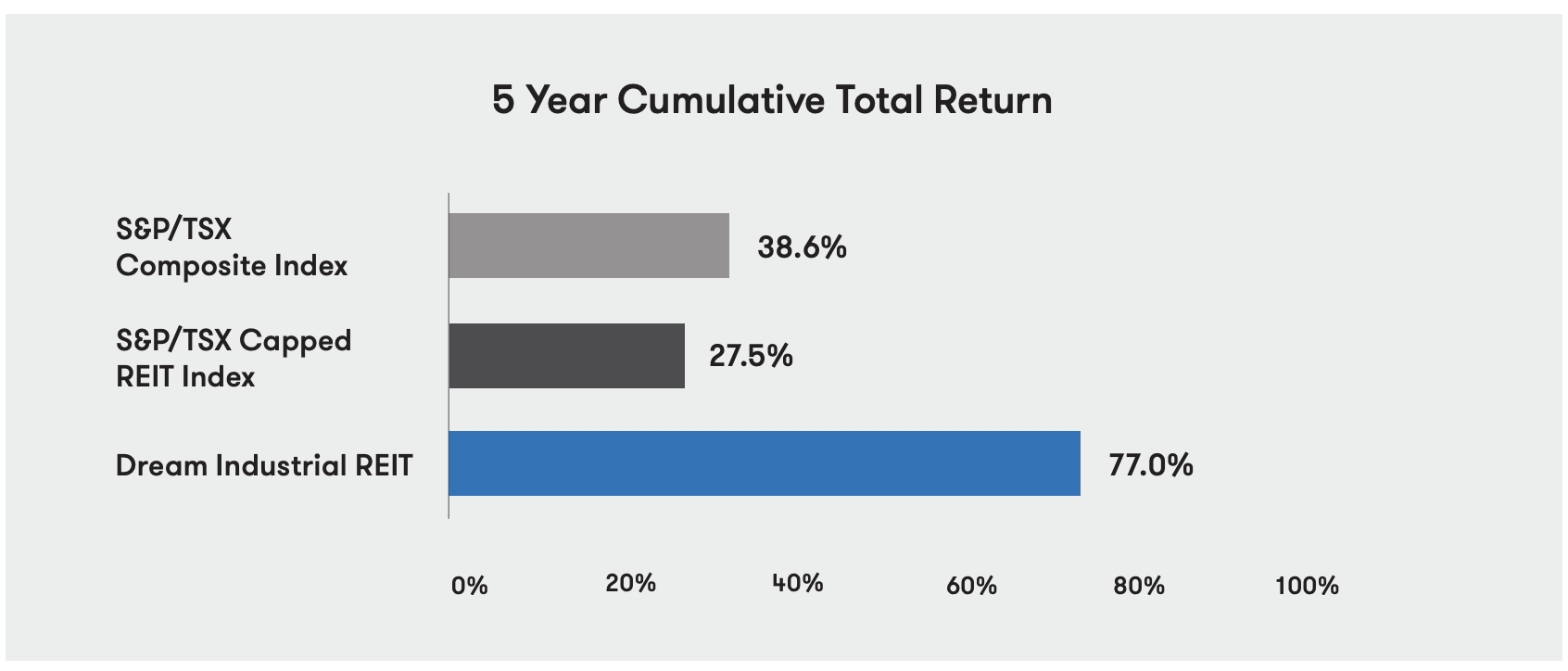

The REIT has realized a 24% total return over the last six months when I was more bullish on the stock, it has blown its peers out of the water in that time. I still strongly believe that double digit returns are in the REIT's near term future. The current 5% dividend yield is accompanied by a conservative payout ratio of 78% on FFO. Furthermore, the REIT trades at a 17% discount to NAV and with greater concentration in assets with yields over 6% combined with lower cost of debt than its peers they should still see spreads of over 3% on assets which will result in further NAV growth. The current discount to NAV is among the highest in its history as it usually trades above NAV. Although the FFO should see strong growth in 2023 as a result of capturing higher leasing spreads I don't envision increased dividend payments as the REIT would be wise to get ahead of debt repayment to keep rising interest expenses at bay.

For further details see:

Dream Industrial: Sweet Dreams Are Made Of These