D.UN:CC - Dream Office: A Look At That 60% Discount To NAV

Summary

- Dream Office is a rare breed of REIT that is actively buying back shares.

- We examine the fundamentals, the NAV and the implied cap rates.

- We tell you the main risk factors that investors should look at before diving in based solely on the high dividend yield.

All values are in CAD unless noted otherwise.

Real estate has not been the best place to be over the last 3 years and many REITs are teetering at or below COVID-19 lows. This is more true in the office sector than any other as the work from home trend has punctured the idea that real estate only goes in one direction. We have looked at a few different office REITs previously (See Hudson Pacific Properties Inc. ( HPP ), Orion Office REIT Inc. ( ONL ) & Allied Properties Inc. ( AP.UN:CA ). Today we examine another one based in Canada. This one comes from a management that we do thoroughly admire . Let's see if we can make a good case for it.

The REIT

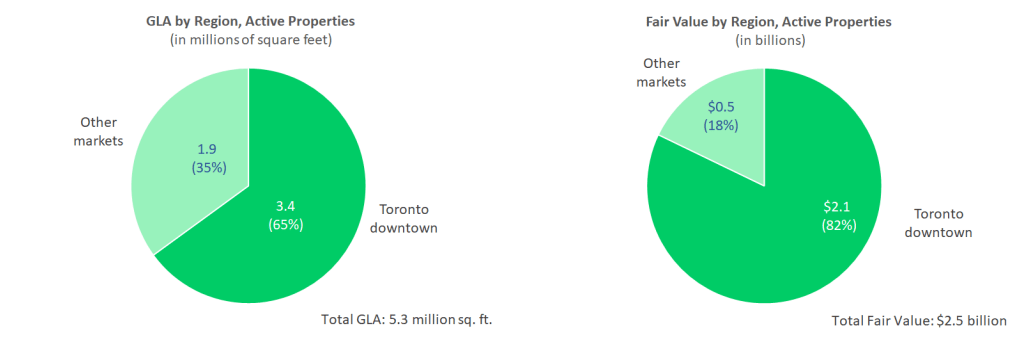

Dream Office Real Estate Investment Trust ( DRETF ), ( D.UN:CA ) owns 27 active investment properties spanning 5.3 million square feet of gross leasable area or GLA. 18 of the 27 reside in the heart of Toronto.

{kind=link}

The balance 8 properties are located in Toronto suburbs, Calgary, Saskatoon, Regina and Kansas. Yes, exactly one of their properties is in Dorothy Land. In addition to the above 27, this office REIT also has two Toronto properties under development having around 0.1 million square feet in GLA.

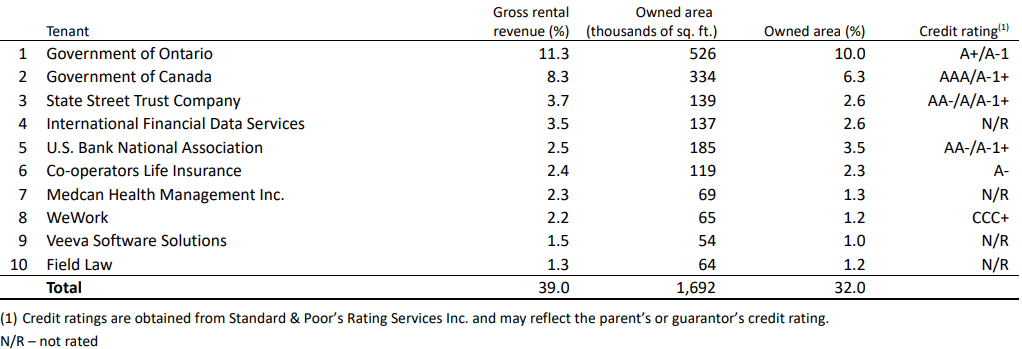

The top tenants occupy around 32% of the square footage and contribute 39% of the gross rental revenue. There are some highly rated names in the list. And then there is WeWork Inc. ( WE ) which looks like it is included just to give you an ascorbic acid overdose.

{kind=link}

Overall, the list looks fine though and you will always find an oddball tenant in any REIT's lineup.

Performance

Moving on to the performance, we can see that Dream Office has underperformed the general REIT index over the last five years. However, it has handily beaten some of the other Canadian office REITs.

Y-Charts

In fact in early 2022 it was momentarily even ahead of iShares S&P/TSX Capped REIT ETF ( XRE:CA ). We will get more into the mechanism of this decline a bit later.

Buybacks From A REIT?

REITs are generally lean, mean, share issuing machines. It is rare when REITs talk about share buybacks. It is even rarer when they actually do it. Compared to traditional non-REIT companies, their hands are usually tied because of the extremely high amounts they have to pay out to maintain their REIT status. Generally, there is very little leftover to do any buybacks. Most also live for empire building (here you can see exhibit A which will cut is dividend because it couldn't stop buying properties). So buybacks and REITs go together like cayenne pepper on vanilla ice cream. Dream broke the mold here.

The REIT took advantage of the price decline by buying back units in the last couple of years. We can see that the purchases were accretive as they were at a price that was well under the published net asset value or NAV.

A company buying a $35 valued share for under $20, would generally make us extremely excited. Of course, the offset here is that they could be in denial about their cap rates and that could neutralize some of the good news.

{kind=link}

The current cap rates according to Dream are lower than when the risk free interest rates were negligible. Their office properties merit only a 114 basis points spread over the risk free rate. If this is a dream, the dream office team definitely does not want to wake up. We do believe that a realistic liquidation value is higher than the share price today. We also believe that the $35 NAV is likely extremely optimistic.

Q3 Numbers

The overall portfolio occupancy increased from 84.6% in the comparative prior year quarter to 85.7% in Q3 due to their Toronto properties coming out ahead in the expirations versus commencement/renewals, sale of one property in Saskatoon in Q3 and reclass of a Toronto property as under development. Toronto downtown by itself only moved the needle by 0.1%.

{kind=link}

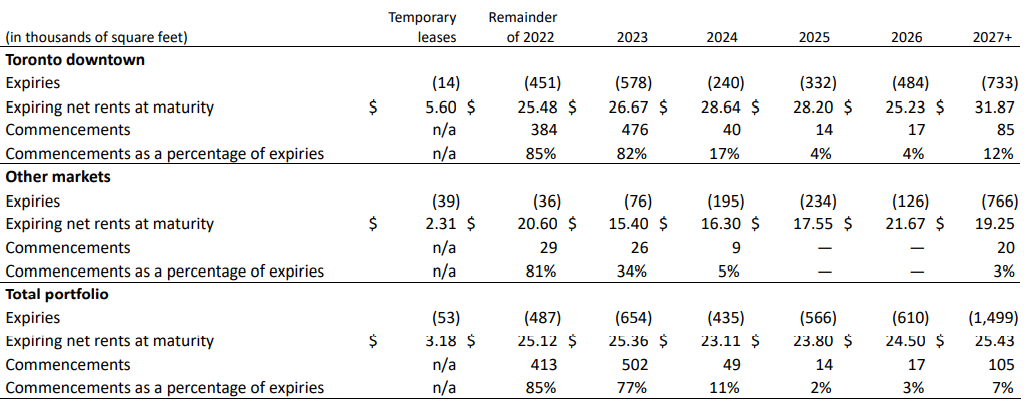

The weighted average lease term or WALT stood at 5.3 years at the end of Q3. The REIT had a substantial portion of the expiries for the remainder of 2022 and 2023 offset by lease commencements as at the end of Q3.

{kind=link}

While the overall occupancy at the end of Q3 was higher, the Toronto properties experienced a decline in the weighted average during the quarter. The REIT did receive higher rates on new and renewing leases, but overall the rental revenues moved slightly lower.

{kind=link}

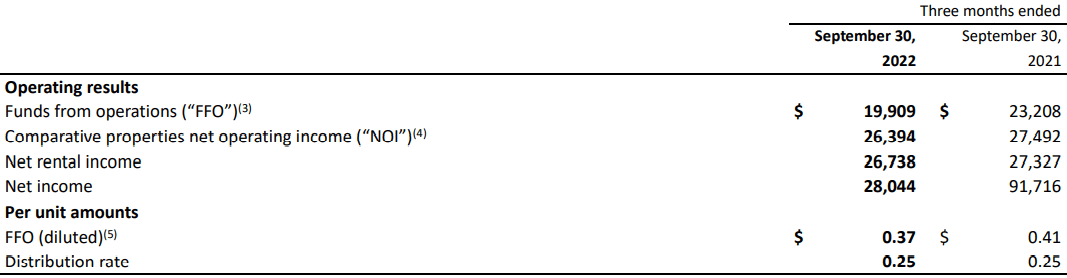

The REIT also felt the pinch from higher interest expense on their floating rate debt and despite some of this offset by the accretive buybacks mentioned previously, the year over year funds from operations (FFO) showed a decline.

{kind=link}

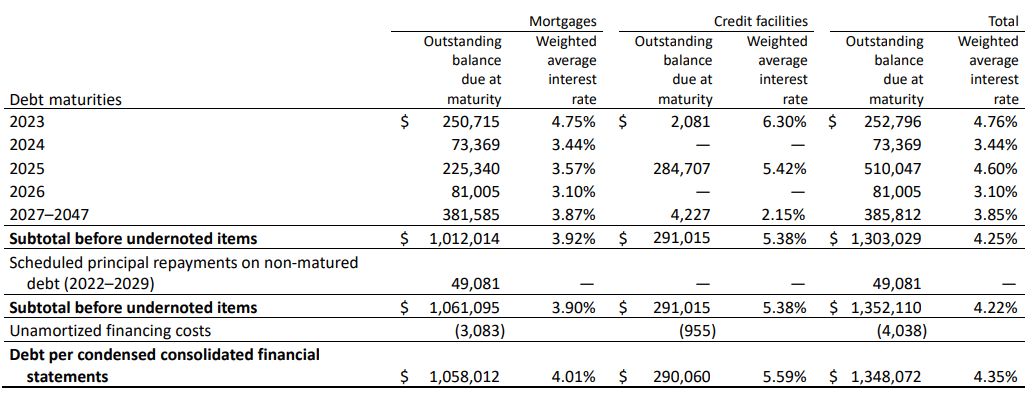

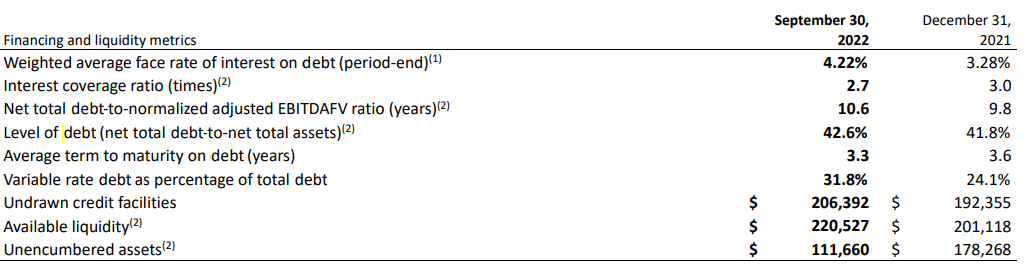

That Debt Load & The Cause Of The Decline

Dream has taken on predominantly fixed rate debt. But even the amount that is variable has swung the overall interest expenses up quite meaningfully. We can see below the shift from 3.28% to 4.22% within 9 months.

{kind=link}

Compounding the issue here is that even the fixed rate is not fixed for long. Weighted average maturity is at 3.3 years and Dream has reduced its unencumbered assets over the last 9 months. It did do a swap on a portion of its variable debt following Q3-2022 but that cost the REIT a hefty 5.37% fixed rate. So there are challenges ahead and it won't be pretty unless office demand really picks up.

Verdict

Trophy Class A office properties are likely going to be more resilient compared to suburban Class B ones. Dream's focus on the former definitely helps in a way, but the 5% cap rates still seem farfetched in this era. Headline risk continues to be high as many companies have been vocal about reducing office space use. Shopify Inc. ( SHOP ) recently confirmed that it no longer intends to occupy any of the 343,000 square feet of office space it has being using at "The Well". That location is a 50%-50% ownership by Allied Office Properties and RioCan REIT ( RIOCF ). A cursory look at that property will tell you that is about as good as it gets for location and quality. Our point being that no one in this asset class is immune from what is happening today.

The implied cap rate based on the current stock price for Dream, is about 7%. What we mean here is that if the properties were sold at a 7% cap rate, shareholders would get about $15 after paying off the debt. That actually looks about in line with what we think is fair. Similarly, the well covered (payout ratio 65%) 6.8% dividend yield looks enticing, but again, we think that is the minimum margin of safety you need here. So while the company believes the shares are heavily discounted, we think they are properly priced. We are rating the stock as Hold and prefer to play office space via diversified REITs having a heavy offering of industrial and or residential space.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Dream Office: A Look At That 60% Discount To NAV