DRUNF - Dream Unlimited: Deep-Value Or Dividend Growth Maybe Both

2023-04-18 08:44:52 ET

Summary

- Dream Unlimited is traditionally a poorly performing sum-of-the-parts deep-value real-estate play, but that's changing as recurring income takes up a greater portion of earnings.

- A focus on growing recurring income allows DRM to pay a growing dividend and consistently buy back shares, in addition to compounding book value and growing earnings.

- Eventually, DRM could be a dividend growth/compounder stock, with deep-value assets as a bonus/margin of safety.

- The valuation should increase as the narrative around the stock changes.

- Insider ownership and net buying suggests shareholders have people within the company working to see value crystalized.

Introduction

Posts, articles, and reports about Dream Unlimited Corp (DRM:CA)(DRUNF) is something of a genre on the internet. This article draws on many of those, but especially from Tyler at Canadian Value Stocks. Maybe this article can add something to the genre.

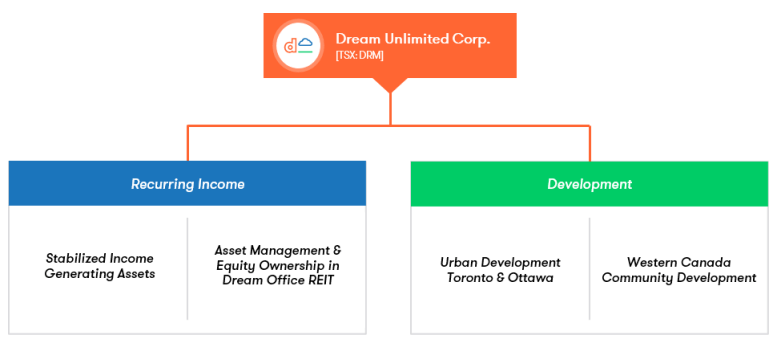

As most readers will know, Dream owns, manages, and develops real-estate. This includes management of multiple public REITs and private funds, equity in most of those vehicles, wholly owned properties, and multiple development projects across Canada. They also recently started a real-estate lending business. Dream is a real-estate hydra, constantly sprouting new heads.

A bare-bones breakdown of Dream Unlimited Corp.and its tentacles (Dream Unlimited 2022 Annual Information Form)

{kind=link}

Background

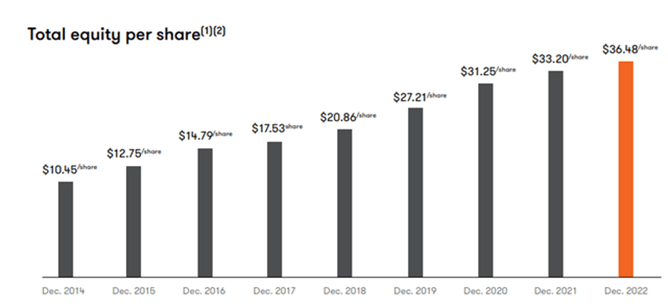

The big draw behind Dream seems to always have been management and valuation. CEO Michael Cooper is something of a real-estate wizard, having begun in the 1980s with $500,000 in equity and compounded it at around 20% to today, where it’s worth about $1.5B on the books, but could be a bit less or a lot more, depending on who you talk to.

Cooper sold a pile of real-estate to General Electric in 2007 (good timing), sold a European office REIT to Blackstone in 2019 (good timing), and most recently partnered with GIC Singapore Sovereign Wealth Fund to acquire and manage a competitor’s industrial REIT, to name a few of his successes. In addition, he opportunistically buys back shares, has begun a growing dividend, and owns 45% of the business. Much has been written about Michael Cooper, but his competence and shareholder alignment are rarely questioned.

Cooper knows how to compound (Dream Unlimited Corp. 2022 Annual Report)

{kind=link}

Regarding valuation, it is always mentioned that Dream has multiple assets that are accounted for at cost on the balance sheet but are potentially worth much more. For example, they have a Colorado ski-hill carried at $40M but recently pulled in $12.6M in EBITDA, and 8,900 acres of land in Alberta and Saskatchewan purchased in the 1990s and 2000s carried at $52K/acre. Considering the 20 years this land has had to compound and Canada’s short supply of housing, the value of each acre has at least doubled.

Dream also owns 14 acres of Toronto’s distinguished Distillery District which has been developed significantly since purchasing a 50% stake for $7.75M in 2004, in addition to operating an asset management business valued on the books at $43M which earned $26M in 2022. With fee-bearing capital nearly doubling since 2022, the manager is likely to increase earnings considerably in 2023.

Lastly, not carried at all on the balance sheet is a steadily growing incentive fee payable on the sale of Dream’s industrial REIT, estimated to be worth more than $250M at present. There’s no doubt Dream’s balance sheet has value to be unlocked.

The accruing incentive fee is tucked away on page 28 of Dream Industrial REIT's Annual Report. It doesn't even appear in Dream Unlimited's reports. It's like they don't want anyone to know about it, which is good for determined investors. (Dream Industrial REIT Annual Report 2022)

{kind=link}

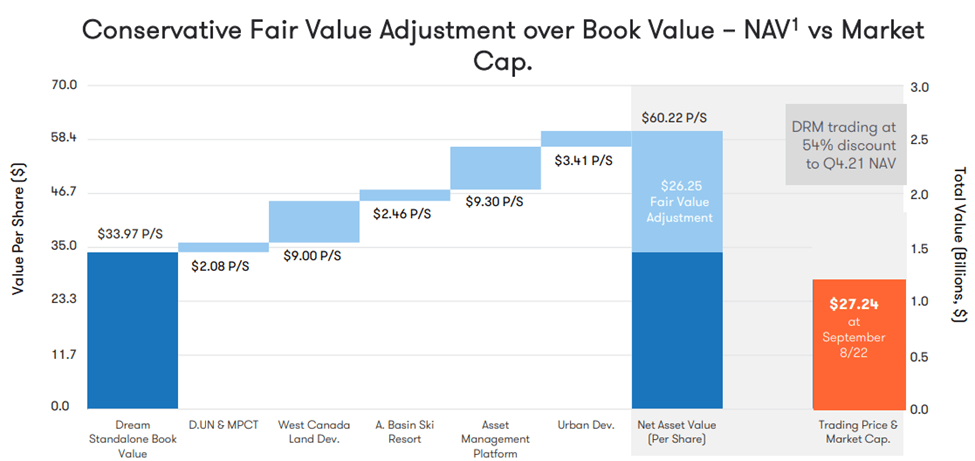

That was the upside. The downside is that management, for all its successes, was an enthusiastic repurchaser of shares at prices far above today’s (bad timing) because they believed DRM’s NAV to be around $60/share. The chart below shows the rationalization. It comes from a Q2 2022 investor presentation but has been conspicuously absent from more recent presentations.

Management's estimate of NAV 6 months ago (Dream's Q2 Investor Presentation)

{kind=link}

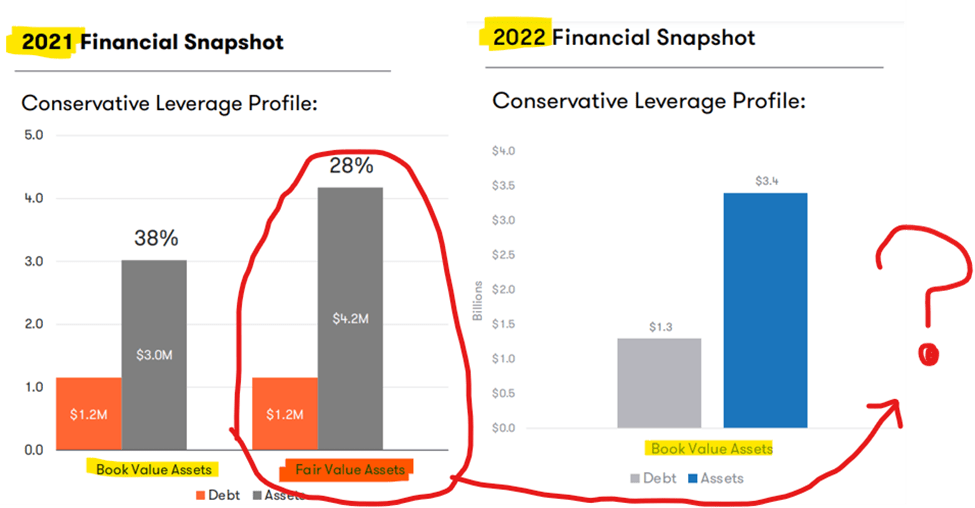

A similar thing happened to Dream’s debt-to-asset slide of the presentation, which used to show debt-to-fair value of assets, but no longer does. Going from disclosing NAV/fair value estimates to omitting them is certainly an ominous development.

A classic case of the disappearing fair value estimate (Dream's Q4 Investor Presentations 2021, 2022)

{kind=link}

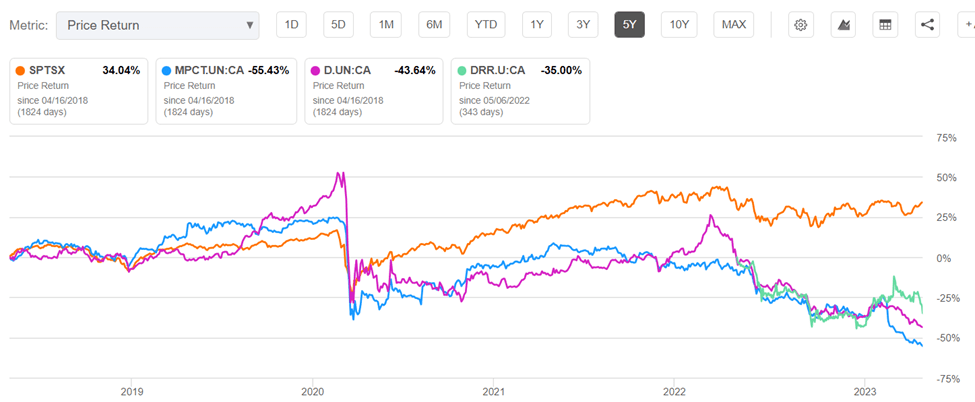

Additionally, close to a quarter of Dream Unlimited’s asset value is made up of a 38% share in its office REIT, a 32% stake its Impact REIT, and an 11.8% share of its Residential REIT. To make things more complicated, Dream’s Office REIT owns shares of its Industrial REIT, making the calculation difficult. Rising rates have caused a REIT-apocalypse, meaning, if the market is right, the ~$700M of equity in these REITs is at least halved.

Dream's REITs have badly underperformed. Is this an unwarranted sell-off or a warning sign? (Seeking Alpha)

{kind=link}

In short, the equity Dream has in its REITs is in bad shape, at least according to public markets. Do these REITs deserve to trade at 40% of book value? I’m not sure. Fortunately, I don’t have to be sure. Because even if the market is right, the undervalued assets mentioned during the upside pitch likely make up for the potential overvaluation of the REIT equity. If the REIT equity turns out to be underappreciated by the market, then Dream Unlimited would be looking good.

Previous times there was such a spread between public and private valuations of real-estate were good buying opportunities. (Hazelview Investments 2023 Global Real-Estate Outlook)

This level of analysis is probably sufficient to create a bull-thesis for DRM; the downside risk vs upside reward, especially given quality of management, seems to be favorable, though there is room for short-term misgivings.

Customary Sum-of-the-parts Analysis

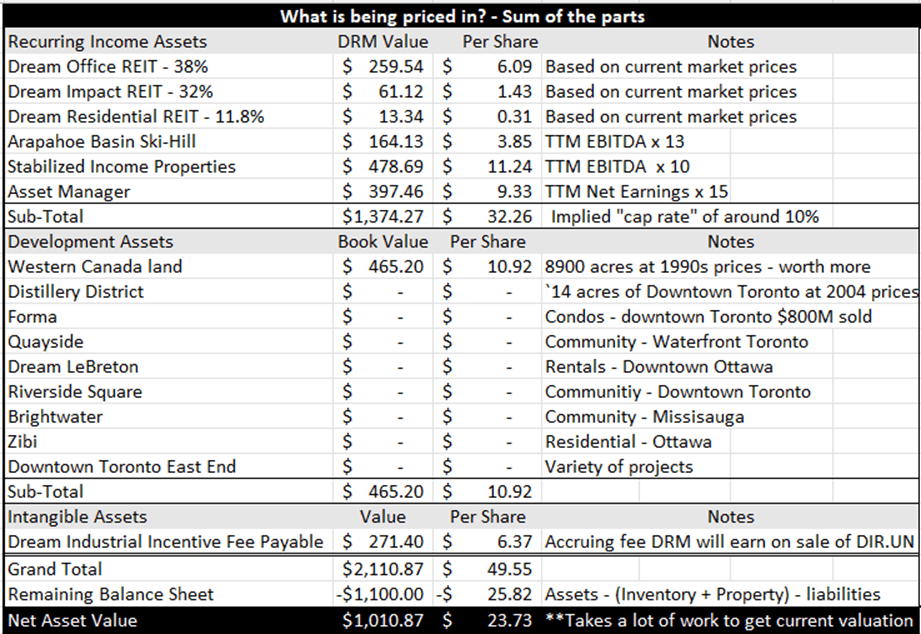

To take a closer look, here’s an extremely rough sum-of-the-parts analysis that tries to figure out what is being priced in:

Assuming the market uses the sum-of-the-parts method to value DRM, this analysis is useful to me because I can look at the assumptions being priced in and determine for myself whether there is a margin of safety. Looks like there is to me. (Author's calculation)

{kind=link}

It certainly appears that a lot is priced in. First thing I notice is that to get the current price we essentially need to ignore the entire development pipeline, except for the land in Western Canada that is likely worth double its book value. That alone is rather astonishing since the development portfolio is where most of the future growth comes from.

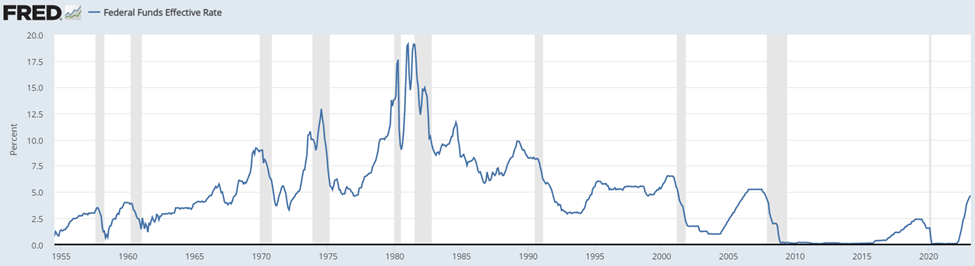

Secondly, the equity in the REITs may not be worth their book value, but I doubt they’re worth the 40% of it that the market is pricing in either. Rising rates certainly hurt, but Canada’s central bank has paused rate hikes and the USA seems poised to do the same, especially as inflation in both countries is quickly trending down. Interest rate problems have likely peaked. Moreover, historically speaking rates are still below average; this is not the end of the world.

{kind=link}

Commercial real-estate, in addition to rising rates, has had to combat Covid. I’m not too worried about Dream Office REIT long-term because the offices are 90% downtown Toronto and I think the strength of the work-from-home movement will ebb with a weakening job market. Moreover, when I imagine 20 years ahead, real-estate in the financial district of Toronto is very likely to be fine, probably better than fine.

In short, to arrive at the market’s valuation of Dream Unlimited, you must believe the development pipeline is basically useless, REITs are permanently impaired, and office real-estate in downtown Toronto will need to take a 60% write-down. Note that this analysis ignores the effect of dividends and buybacks. Tom Hayes likes to say, “Amateurs deal in absolutes and experts deal in probabilities.” I don’t mind the probabilities here.

Analysts agree. They think the fair value is much higher than the current price, even more than book value. Analysts are usually optimistic, but the spread between their price target and the actual price is very large relative to the past:

Analysts appear to think this downturn is in price, not value of DRM. (Seeking Alpha)

I’m not a financial analyst, just a guy who likes researching stocks, so I’m going to take the bold position of splitting the difference between the analysts and the market, which leaves us at a reasonable trading value of around $34-$36/share, i.e. book value. We took the long cut to arrive at a number we could have easily googled but I think there was value in it. Knowing what’s priced in and what’s assumed is useful.

Here’s a return estimator for a few scenarios should we take book value as the reference point going forward:

I didn't use NAV because Dream has almost never even traded above book (Author's Calculation)

{kind=link}

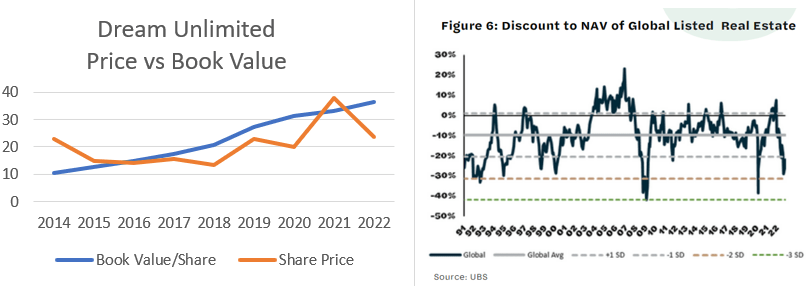

It looks pretty good to me. However, the problem with deep-value sum-of-the-parts stories is that they rarely trade at the sum of their parts; 1+1 usually equals 1.5. Management might be great and the valuation eye-poppingly low, but complicated sum-of-the-parts stories like this one tend to disappoint, and DRM is no exception:

Public real-estate often trades below NAV, and DRM is an extreme example, rarely being able to trade even book (Author's Calculation and Hazelview Investments 2023 Real-Estate Outlook)

{kind=link}

Investors in Dream for the discount-to-NAV story are waiting for others to read through the fine print of the annual report, open Excel, and do the math. That’s a big expectation; investors at $20/share in 2015 are still waiting for that to occur, no matter how undervalued the western Canadian land may be on the books. We might get some mean reversion if real-estate turns out to be temporarily underappreciated by the market, but will the stock ever trade at fair value this way? I doubt it.

DRM's stock price since its IPO in 2014. The price has hardly changed, and the value has increased dramatically. (Seeking Alpha)

What could get the stock to closer to NAV, or at least to book, is if investors didn’t have to do a sum-of-the-parts calculation. Instead of analyzing and valuing dozens of businesses, investors can analyze one. That would make a huge difference.

The Recurring Income Story

Dream Unlimited’s earnings/cash flows are becoming more predictable. About half their assets are in the development portfolio which generates lumpy earnings, while the other half generate stable recurring income. As developments finish, Dream plans to retain many of them and collect their cash flows, furthering the ratio of recurring income assets to development assets, thereby making cash flows for the entire company more predictable and valuation simpler.

Dream's rentals are growing quickly (Dream Q4 Investor Presentation)

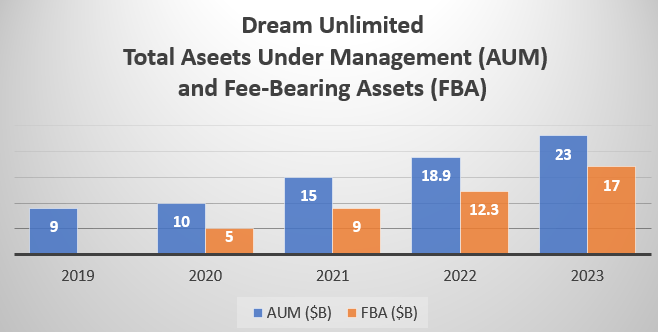

In addition, the asset manager is only three years old, but already has $17B of fee-bearing assets, providing another increasing stream of recurring income. The recent deal to acquire Summit REIT with GIC is significant because it completely legitimizes Dream’s asset management platform and provides a source of significant capital, increasing scale of future investments and fee-related earnings. Brookfield is an example of masterfully deploying this strategy, and it’s exciting to see Dream begin to do the same.

Growth in AUM and FBA has been extremely quick. (Author's Calculation from Dream's Annual Reports)

{kind=link}

As this transition from asset values to asset income streams takes place, valuing Dream by its cash flow/earnings/FFO will become increasingly simpler and more accurate. The more predictable the earnings and simple the valuation, the higher Dream will trade; multiplying FFO by a multiple is a lot easier than estimating cap rates for dozens of properties.

Why then doesn’t Dream just supply some cash flow/earnings metric, such as FFO, like other real-estate conglomerates? I think the answer to that is that the numbers are not yet pretty, or fully representative of the value. Let me show you what I mean.

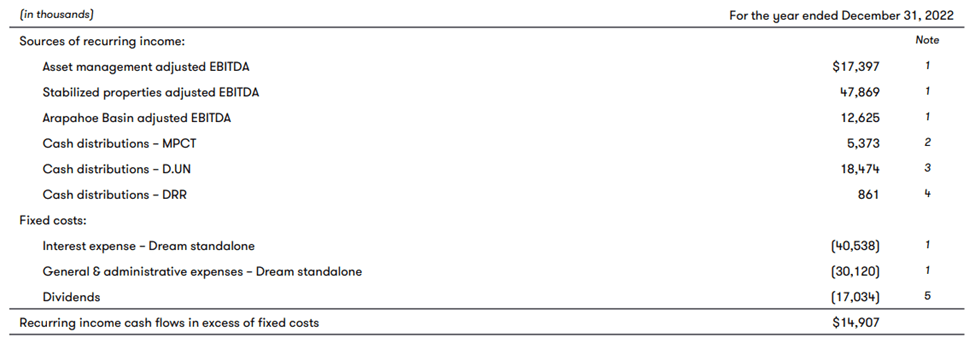

Here’s a slide showing income generated from their recurring income portfolio less fixed costs for the entire company (including development):

I like this slide because it's a step in the right direction towards simplicity and clarity (Dream's Q4 Investor Presentation)

{kind=link}

Dream’s recurring income portfolio generated around $32M dollars above fixed costs, some of which it used to pay a dividend. Having half the company pay for the whole thing is good news but doesn’t do much for the valuation. If we were to derive a multiple of recurring cash flow at the current market cap, it would be around 31x ($1,000/$32). That doesn’t look cheap! Not a good metric yet.

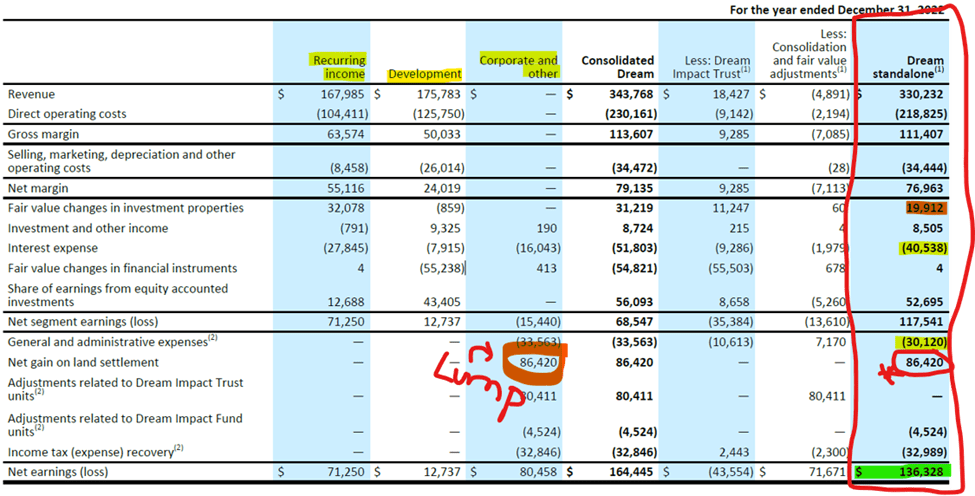

To get a number more representative of the whole company, we need to include the development portfolio. This gets challenging as development’s cash flows are non-recurring, lumpy, and unpredictable, in addition to just being hard to decipher in Dream’s reporting. For example, from page 25 of Dream’s 2022 Annual Report:

If you’re a little confused looking at this, then you’re not the only one. That alone should be indicative of why Dream continues to trade at such a discount. Who, except professional analysts and Dream enthusiasts, would put in this much work? (Dream 2022 Annual Report)

{kind=link}

You can see an $86M net gain on land settlement that wouldn’t be included in recurring income or FFO, in addition to fair value changes, highlighted in red. Highlighted in yellow are where Dream got the interest expense and G&A expense numbers for the prior slide.

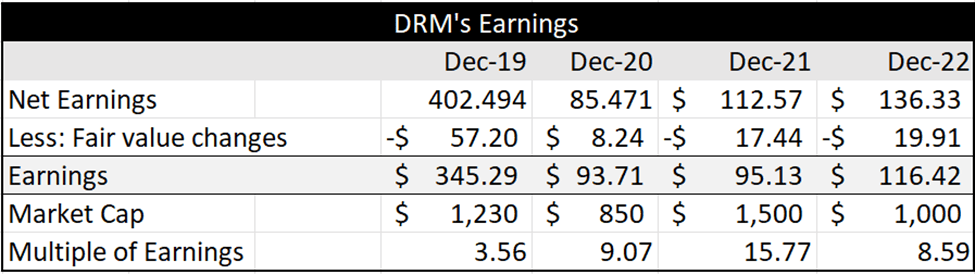

To calculate an earnings number that made sense for DRM I just took net earnings (in green) and subtracted fair value changes (in red) to get ~$116M of earnings for 2022 ($136 - $19.9). We could add back depreciation and amortization, but I'm going to keep it simple for now.

I went ahead and did this for the last few years:

Note that we could spread the accruing incentive fee DRM earns on the sale of the industrial REIT over these years and would get much lower multiples. That's a fairly large margin of safety on these calculations. (Author's Calculations)

{kind=link}

As we can see, in addition to this information being difficult and time consuming to collect, it has flaws. In 2019, Dream sold its Global REIT to Blackstone, artificially inflating earnings. However, since then, this way of measuring earnings seems to have been a fair representation of value. Aside from the occasional sale of a REIT, this might be a metric that is useful to investors.

It certainly seems to that suggest DRM, relative to an assumed 15% growth rate, at 9x earnings was undervalued in 2020, at 15.7x earnings was fairly valued in 2021, and at 8.6x earnings now, is currently undervalued. This is a similar conclusion reached by our conservative sum-of-the-parts analysis. Finding two valuation methods that corroborate each other is a big win when trying to value Dream.

It wasn’t easy though, and that’s the point. When you look under the hood and dig around a little bit, it’s possible to see that Dream is a compounder at a low valuation. However, until this fact becomes more readily apparent, I doubt Dream will trade at fair value.

However, with recurring cash flows, as opposed to lumpy gains, taking up a greater percentage of earnings, DRM could begin to demand higher multiples and approach fair value. It just won’t happen overnight.

This is especially when we account for Dream’s debt in the context of higher interest rates.

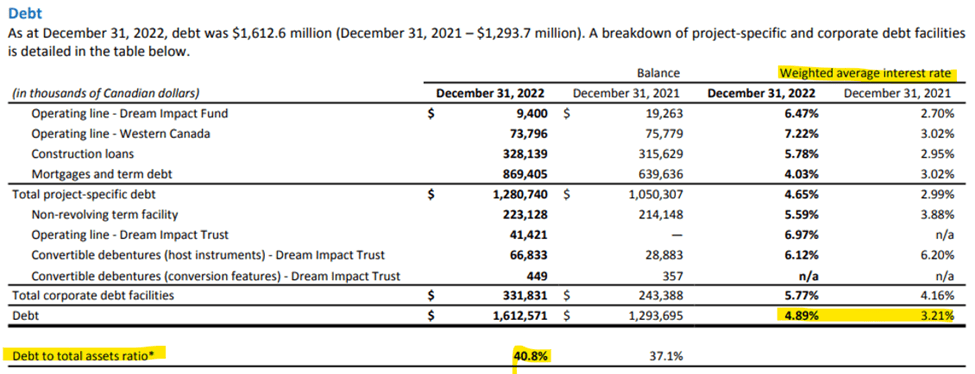

Debt

Being a real-estate company, Dream uses debt. Here’s a breakdown:

Less than 10% of debt is directly associated with DRM. This is something Brookfield makes sure to highlight in presentations, so I point it out here as well. (Dream's 2022 Annual Report)

{kind=link}

Over the last year, Dream added $300,000 of debt, primarily mortgages. The debt-to-assets ratio is not extreme at around 41%, and this is likely overstated as condo inventory, land inventory, and the ski-hill are carried at amortized cost, not fair value. Perhaps the value of the office building assets is overestimated, but likely not enough to increase debt as a percentage of assets significantly, if at all.

I like that 75% of the debt is project specific, meaning that if a project or property were to become unprofitable, Dream could just default on the loan and hand the keys to the bank, instead of having to liquidate other properties to raise cash. This reduces systemic risk to DRM significantly.

More concerningly, Dream’s weighted-average interest rate jumped from 3.21% to 4.89% from 2021 to 2022. That is a rather large jump, and interest expenses increased proportionately from $22M in 2021 to $41M in 2022, decreasing recurring income after fixed costs year over year. Unfortunately, it looks like interest expenses will increase again this year as a quarter of Dream’s debt matures in 2023, and I doubt they’ll get a lower rate than they already have.

Maturities are fairly staggered but 2023 has a fair chank maturing. (Dream's 2022 Annual Report, Author's Preparation)

I don’t think Dream will have a problem refinancing, seeing as their debt-to-assets ratio is low, and they already generate cash above what is required to service their debt. Additionally, recurring income streams are set to increase with greater AUM in the manager, completion of rental units, and general rent hikes. Overall, I don’t have any concerns regarding Dream’s debt.

That said, while it’s nice Dream doesn’t have to raise cash to pay debt obligations, I would love to see recurring income after fixed costs begin to increase. This would allow for larger dividend increases, more special dividends, buybacks and crucially, make the argument for a re-rating stronger. Higher interest rates and refinancing are likely going to delay this wish in 2023, but if I move my time horizon out a little longer, that possibility remains.

But now I’m sounding hopeful, and hope is not an investment principle.

Follow the Insiders

Personally, at this point in the analysis I’m still on the fence over Dream. Despite the fact management compounds capital, debt is more than under control, and there is deep-value evident after a little digging, I continue to wonder if it will ever be realized.

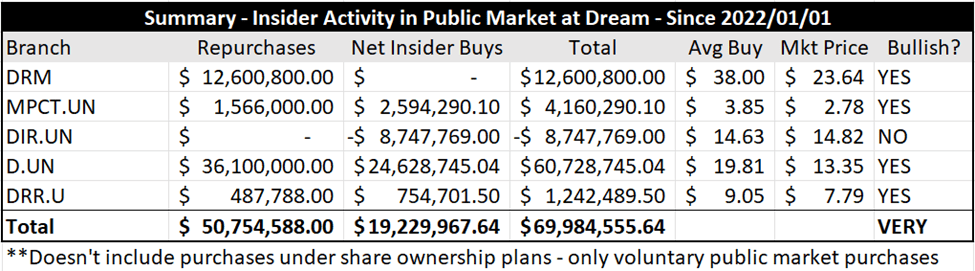

Dream, being incredibly complex and difficult, and me, not being a real-estate expert or even a financial expert, went to SEDI, Canada’s archaic website for checking insider activity in public companies. Insider buying and selling can tell an investor a lot about a company’s prospects because insiders have better information far earlier than the market. Buffett is often attributed with the quote, “There are lots of reasons insiders sell stock, but only one reason they buy.” I was delighted to find out Dream’s insiders and entities are buying.

Dream has options, rights, and it appears management is required to purchase shares as part of an ownership plan (a good thing). I excluded all those transactions however and included only those voluntarily made with cash in the public market by the insider or entity. In other words, only purchases/sells that are certain to mean something are included. Here’s a breakdown of what I found:

I spent some pretty tedious hours on SEDI preparing this, and am glad I did so. You can learn a lot from public filings. (SEDI public filings, Author's Preparation)

Except for the industrial REIT and a few directors, high profile insiders, and the entities themselves, have being buying shares like crazy. First thing to note is that Michael Cooper, the founder, controller, CEO, and 45% DRM shareholder, is an active buyer of stock amongst Dream’s various entities, personally and through control of companies. He even put shares of the Impact REIT and Residential REIT into a Registered Education Savings Plan ((RESP)), presumably for his children. Cooper is planning on Dream to be around for a while.

Secondly, DRM itself hasn’t seen much insider buying since they were buying back stock in 2022 at sky-high prices. I don’t think this is indicative of a problem at the parent company, I think it's more likely that insiders are buying the dip in the higher yielding REITs, as DRR.UN, MPCT.UN, and especially D.UN, are being heavily bought. I would love to see DRM being bought, but insider buys of investment vehicles it has considerable equity in is also a good sign.

Thirdly, the insiders appear to be sellers of the industrial REIT. For example, Dream Office REIT, which holds shares of Dream Industrial REIT, sold a pile of shares. This doesn’t worry me too much as the proceeds of that transaction were presumably used to repurchase shares of the office REIT, as it is trading at a steep discount to book, while DIR.UN is trading at a premium.

That premium could be why insiders are sellers, but I think it also has to do with the fact DRM, the parent company, has the least equity in it and earns considerable fees for managing DIR.UN. In addition, the accruing incentive fee payable to DRM on the industrial REIT’s sale is already above $250M. Insiders appear to prefer the company earning the fees rather than the one paying them.

There is more to conclude, but I’ll leave that to the comment section. Here’s a summary:

The market timing of these insiders and entities has been pretty poor. Perhaps we don't just follow them in immediately... (Author's Preparation, SEDI public filings)

{kind=link}

Since January 1st, 2022, Dream entities and insiders have voluntarily net bought $70M of shares. They bought those shares at prices considerably higher than they sell for now. To me, this means my analysis is on track; the business is high-quality, and the valuation is undemanding. This is a very bullish development.

Another important point about insiders voluntarily increasing their skin in the game is that they will be more motivated to unlock the value of their shares. Me, just a guy who lives far away, can’t really do anything except write articles, wait, and to some degree, hope value will be unlocked. But now I know I have well-aligned insiders who understand the business better than me, are down on their purchases, and are probably just as eager to see value unlocked. It’s not a guarantee, but it’s good to know people with the power to change things want the same thing I want.

This assurance is important for me, especially because Dream Unlimited continues to be a sum-of-the-parts value story.

Conclusion

I’m no longer on the fence regarding Dream Unlimited. I like the assets, I like the management, I like the valuation, I like that debt is not a concern, and I like that insiders feel the same.

Investors are certainly in no rush to build a position, as the full effect of rising rates is not yet known, but publicly listed real-estate as a sector has rarely been this cheap. Dream Unlimited, on a book value per share basis, was only slightly cheaper when we thought the world was going end in March 2020.

As such, DRM may see some mean-reversion in the short-term, but the catalyst to unlock value, I believe, will be the narrative around Dream Unlimited changing from a pure deep-value asset story to a cash flow, dividend growth, share buyback story, with undervalued assets as a bonus.

I’m a buyer in slow, small amounts.

For further details see:

Dream Unlimited: Deep-Value Or Dividend Growth, Maybe Both