DRVN - Driven Brands: A Stabilizing Quarter Underscores The Value Case Technical Risks Remain

2023-11-07 13:07:44 ET

Summary

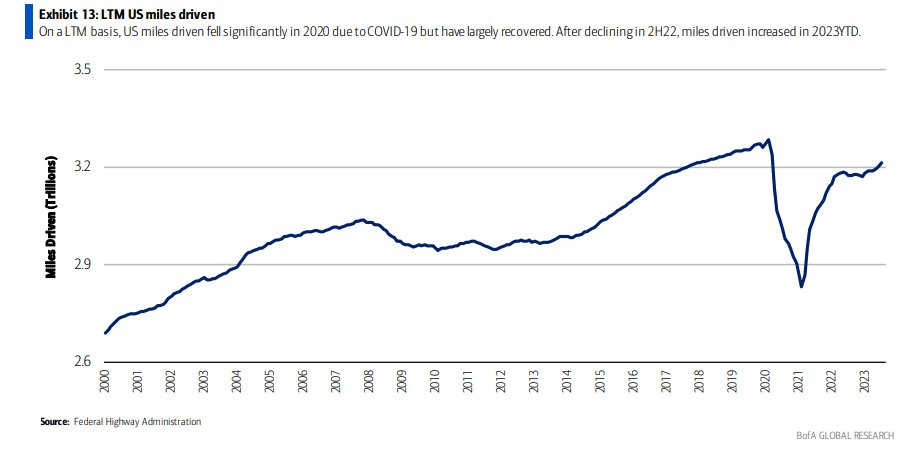

- Miles driven numbers are rebounding, indicating a return to work and bullish prospects for Driven Brands.

- Driven Brands is the largest automotive services company in North America with a diversified business model.

- The stock is undervalued but faces significant technical risks, with a buy rating overall.

- I outline key price levels to watch as momentum turns a bit more positive.

Miles driven numbers continue to be on the rebound as the ‘return to work’ push persists. I keep tabs on this automotive indicator periodically, and it is generally seen as bullish for Driven Brands (DRVN). Following a sharp stock price free fall in August, I see the shares as undervalued, but with significant technical risks. Overall, I have a buy rating on the stock.

USA Miles Driven Reaches A New Cycle High

{kind=link}

According to Bank of America Global Research, Driven Brands is the largest automotive services company in North America with a growing and highly franchised base of more than 4,800 locations across 49 states and 14 international countries. The company's platform of brands includes a wide range of consumer and commercial automotive applications, separated into four reporting segments: Paint, Collision & Glass, Maintenance, Car wash, and Platform Services. The majority of its locations are franchised.

The Charlotte-based $1.9 billion market cap Diversified Support Services industry company within the Industrials sector does not have positive trailing 12-month GAAP earnings and it does not pay a dividend. With earnings not due out until February of next year, shares trade with a still-lofty 44% implied volatility percentage while short interest on the stock is material at 4.7% as of November 6, 2023.

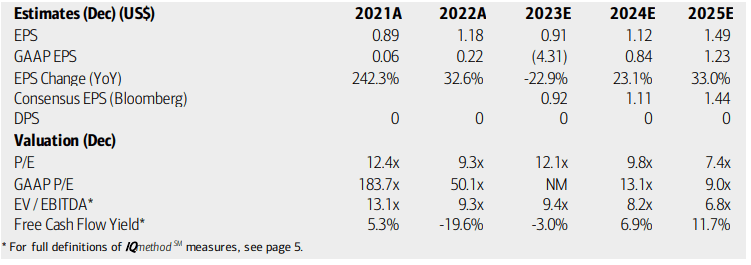

Earlier this month, Driven Brands reported operating EPS of $0.20, topping the Wall Street consensus by $0.02 while quarterly revenue verified at $581 million, also better than expected. System-wide sales summed to $1.6 billion, a 10% increase year-over-year, helped by a 6% jump in same-store sales with 55 new stores added in the quarter. With a diversified business model, adjusted EBITDA also tallied above what the street was expecting.

The big quarterly move was in August , though. In a rare “beat and cut,” the company lowered its sales outlook from $2.35 billion to $2.30 billion and reduced its adjusted EBITDA forecast from $590 million to $535 million due to profitability challenges in its Car Wash segment and weak retail traffic trends. Heightened competition in its PCG space was also seen as a key risk. Still, following a decent Q3, the fundamental story appears intact despite risks of easing miles driven numbers across the country, growth in EVs, and rising interest rates.

On valuation , analysts at BofA see earnings having fallen sharply this year but then bouncing back strongly in 2024. Per-share profit growth is then expected to accelerate in 2025. The consensus outlook is actually even more optimistic when assessing the latest consensus forecast for 2025. While no dividends are expected to be paid on DRVN, its operating earnings multiple appears attractive so long as EPS growth materializes. Moreover, the firm’s EV/EBITDA ratio is well below that of the broader market, but DRVN is free cash flow negative in the last 12 months – but that is seen as inflecting positive next year.

Driven Brands: Earnings, Valuation, Free Cash Flow Forecasts

{kind=link}

If we assume normalized earnings of $1 and apply merely a sector median P/E of 16.9, then shares should be near $17 today. Driven trades well under its historical valuation multiples and the stock appears quite cheap on a price-to-sales basis. The valuation may even have upside potential should the multiple eventually revert to its long-term average. Its strong margin profile with revenue sales growth in the future should warrant a respectable P/E in my view.

DRVN: Significantly Below Its Long-Term Valuation Averages

Seeking Alpha

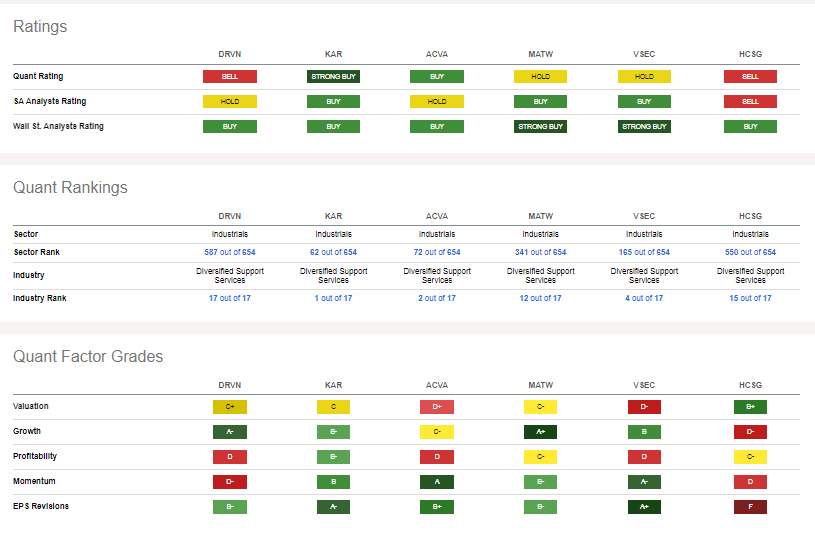

Compared to its peers , DRVN features a valuation in line with its competitors while the growth outlook is actually rated quite strong, but the earnings outlook is obviously tainted by the August guidance slash. With weak profitability and downright dreadful share-price momentum , the broader case for owning the stock here is not appealing. Still, EPS revisions have been to the good side, but considering that the company has traded lower in the past five earnings events, the market may be telling us something less sanguine.

Competitor Analysis

{kind=link}

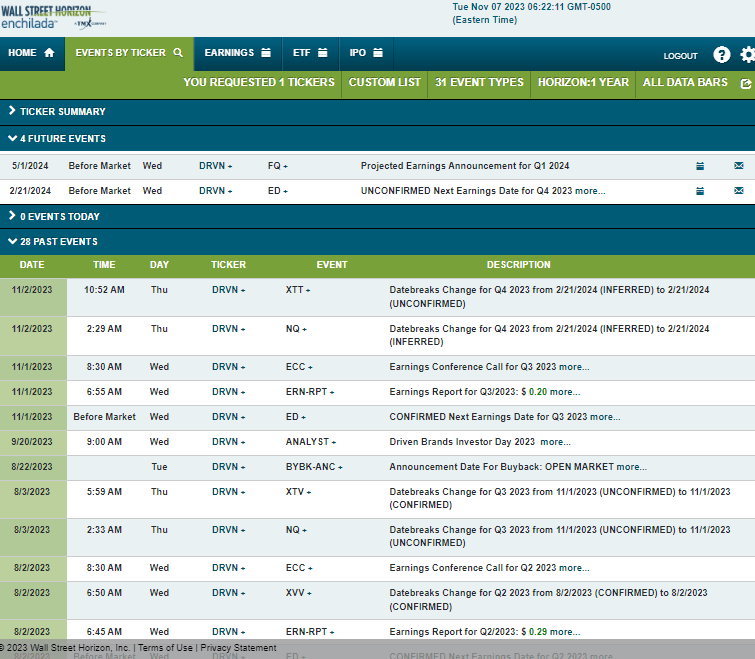

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q4 2023 earnings date of Wednesday, February 21, 2024, BMO. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

{kind=link}

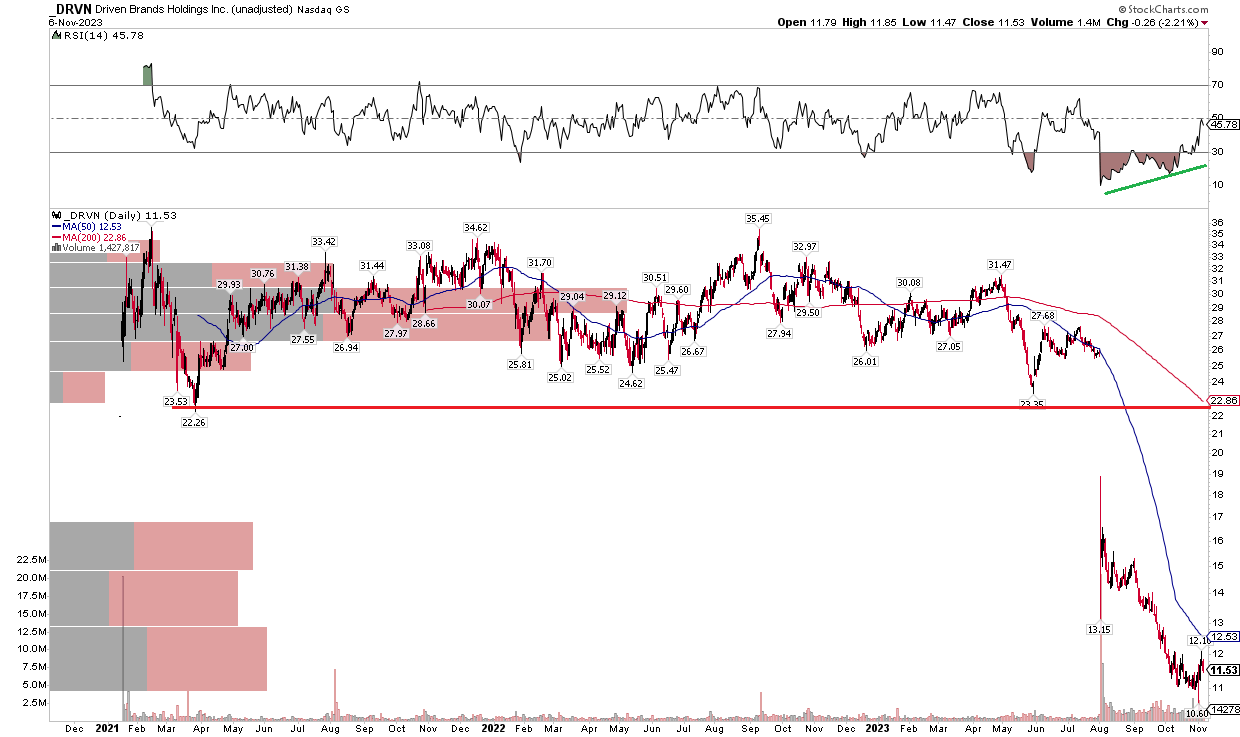

The Technical Take

DRVN’s chart is rather straightforward. Given limited price action history following the company’s go-public date closing in on three years ago, we have only a handful of important price levels to monitor. The major one is now a ways off (to the upside). Notice in the chart below that DRVN plunged through key support in the $22 to $23 zone back in the summer.

Shares reached a near-term low of $13.15, but the selling was not done in the wake of the guidance cut. A relief rally stalled, and shares drifted toward the $10 mark earlier this month. Today, the stock is about a buck above that nadir, and while there is a major air pocket with no volume in the $17 to $22 area, it will take a lot for the bulls to lift the auto services stock into that gap. The good news for the bulls is that there is a positive RSI divergence when scanning the momentum indicator at the top of the graph and price action that has moved down in Q4. Long with a stop under the $10 mark could work from a risk/reward perspective for those seeing fundamental value in the stock.

Overall, the trend is clearly with the bears, and it is an ‘avoid’ from a technical perspective.

DRVN: Bullish RSI Divergence Within a Bearish Price Trend

{kind=link}

The Bottom Line

I have a buy rating on DRVN. I assert that the Q3 report underscores that the business is not in turmoil (as the August report’s stock price reaction suggested). Also, momentum on the chart is improving, though a downtrend remains in play.

For further details see:

Driven Brands: A Stabilizing Quarter Underscores The Value Case, Technical Risks Remain