DBX - Dropbox: A Mature Business With Strong Free Cash Flows

2023-10-03 07:37:58 ET

Summary

- Dropbox has evolved into a mature business with a focus on strong free cash flows.

- Founder Andrew Houston's significant voting power suggests it's unlikely to be acquired.

- With growing paying user numbers and a healthy balance of cash and convertible debt, Dropbox has the potential to increase its share buyback program in the near future.

Investment Thesis

Dropbox (DBX) today is much more than just file sharing. Dropbox simplifies work processes, enhances collaboration, and provides a unified hub for individuals and teams to manage their digital content effectively.

This is no longer a particularly exciting story. Dropbox is now a maturing business. But what it lacks in topline growth rates, it more than makes up with strong free cash flows.

Dropbox is priced at 10x free cash flow next year's free cash flow. In fact, that's part of the problem with thinking about Dropbox, investors should not be thinking about a multiple expansion to drive investors' upside. The returns to this name will come from sitting on one's hands and waiting for a capital returns program to be announced soon.

This is not a blemish-free story. But on balance, there are more positives than negatives.

Dropbox's Near-Term Prospects

Dropbox provides a platform and a suite of tools to help individuals and teams manage and collaborate on their digital content seamlessly. At first, Dropbox focused on file storage, however, now Dropbox has evolved to become a comprehensive workspace for work-related tasks.

It allows users to share their content effortlessly. Some of its key features include cloud-based file storage, document collaboration with real-time comments and annotations, powerful search capabilities, secure file sharing, integration with various third-party apps, and additional tools like e-signatures, and more.

Recently, Dropbox has sought to refocus on product development. Their AI-powered initiatives , including Dropbox Dash and Dropbox AI, are set to improve its content management and search, providing users with more efficient ways to organize and access their files across various platforms. Dropbox is committed to enhancing user experiences and creating a more enlightened way of working, further solidifying their position in the cloud storage and collaboration space.

Moreover, Dropbox is actively integrating multiple workflow businesses into its core offerings, striving for a seamless and unified experience for customers. Standalone businesses like FormSwift (for legal documents) and Replay (video projects) are gaining momentum, demonstrating the company's potential for growth across different sectors.

Additionally, during the earnings call , we heard Dropbox's describe its strategic partnerships and dedication to responsible AI usage underscoring its commitment to staying at the forefront of technological advancements while prioritizing user privacy. In the near term, Dropbox's product-centric approach and strategic initiatives position them for continued success and innovation in the cloud services landscape.

That being said, Dropbox openly acknowledges the macro environment mentioned as witnessing elevated price sensitivity, particularly affecting Dropbox's Teams customers who are experiencing down-sell pressure due to economic challenges. This environment is also impacting Dropbox Sign and DocSend negatively.

Given this context, let's now discuss Dropbox's financials.

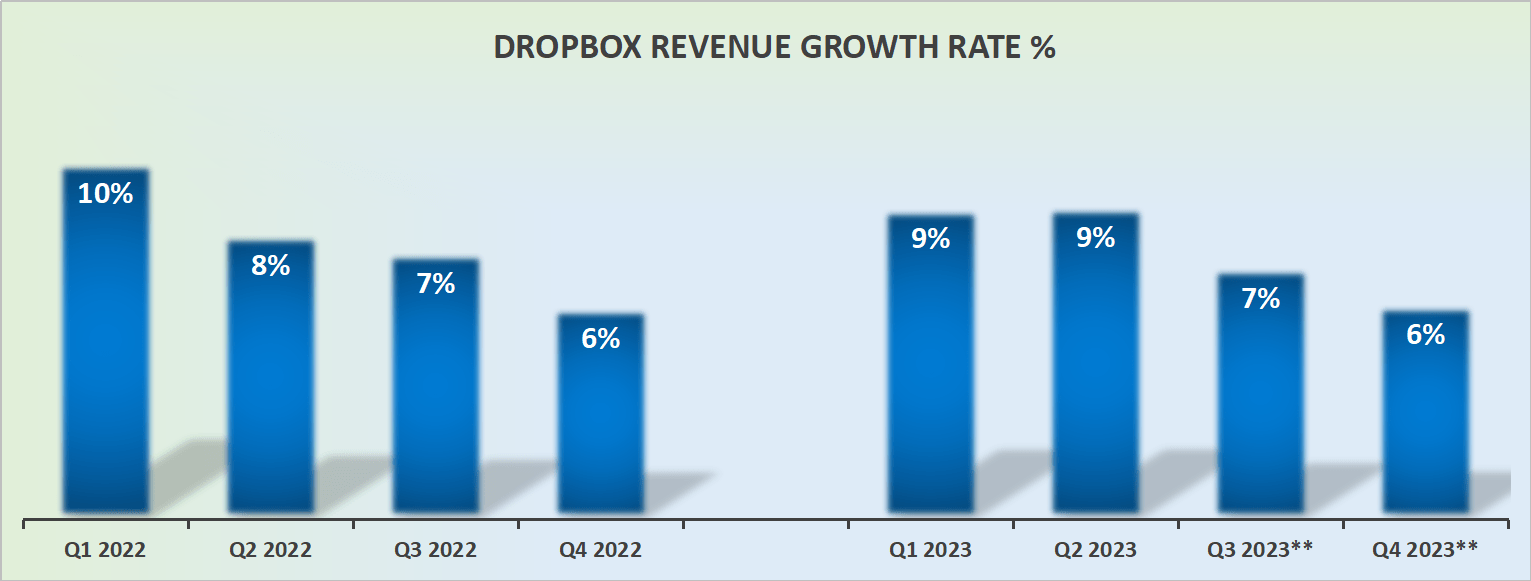

Dropbox's Revenue Growth Rates

{kind=link}

The graphic above is a reminder that Dropbox today is barely eking out mid-single digits.

Dropbox faces competition from several prominent companies in the cloud storage and collaboration space. This is not an exhaustive list, but instead some of the competitors that come to mind.

For instance, Google Workspace ( GOOG )( GOOGL ), offers free cloud storage, productivity tools, and collaboration features integrated with popular applications like Gmail and Google Drive. Microsoft's OneDrive and Microsoft 365 ( MSFT ) provide top cloud storage solutions and productivity tools. Box ( BOX ) is another competitor, although this one specializes more in cloud content management for enterprises, rather than individuals and small businesses.

Additionally, companies like Apple ( AAPL ) with iCloud and Trello ( TEAM ) also vie for a share of the market by offering unique collaboration and file-sharing features. Again, not an exhaustive list by any stretch. However it clearly provides a framework to think about Dropbox's competitors.

And we get it. There's no investor coming to Dropbox for a particularly alluring racy story. Instead, investors are here for the free cash flow.

The Crown Jewel of the Investment Thesis

Dropbox is expecting around $840 million of free cash flow this year, but approximately $1 billion the following year. That's the crux of the bull thesis. This puts Dropbox priced at 10x next year's free cash flow.

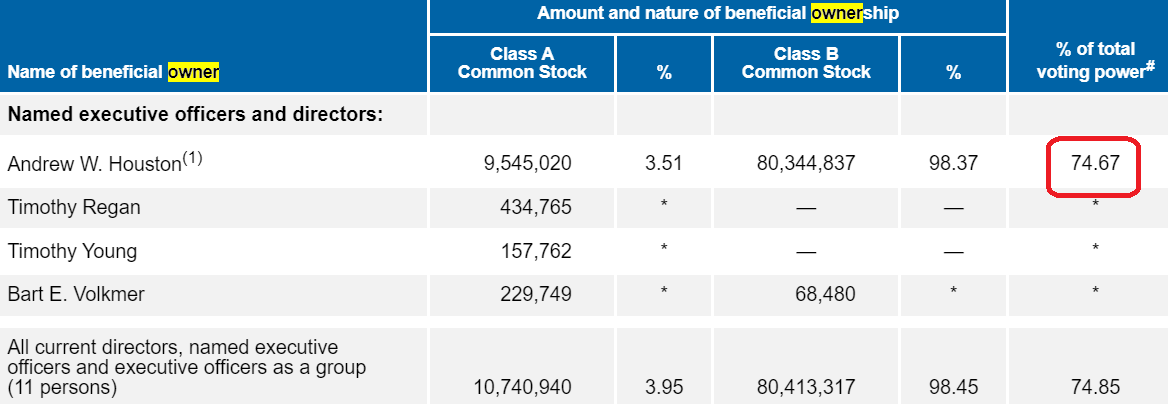

Further, given that Dropbox's founder Andrew Houston has so much voting power in the company, I can't see any way this company gets acquired, see below.

{kind=link}

Consequently, what we see is what we get. A business that's likely to continue ticking along over time, seeking to provide more innovative tools in an attempt to attract more users. And yet, in actuality, as you can see in the graphic that follows, there's still an increasing number of paying users embracing Dropbox's offering, even now.

DBX Q2 2023 presentation

Furthermore, Q2 2023 saw its paying users increase nearly 5% y/y to 17.9 million. On the other hand, naturally, I question how much, if any, pricing power Dropbox earnestly has when there are so many "free alternatives" competing for individuals and small startup content.

On the other hand, nearly 12% of its market cap is made up of cash which is nearly equally matched by its convertible notes , with the net figure being that Dropbox's cash and convertible debt match each other. Meaning that next year, there will be more than enough capital coming to the business so that Dropbox could in 2024 meaningfully increase its share buyback program.

The Bottom Line

Dropbox, while no longer an exciting growth story, has transformed into a mature business with a focus on strong free cash flows. Priced at 10x next year's free cash flow, its investment thesis does not rely on multiple expansion but rather on capital returns through an upcoming program.

Despite macroeconomic challenges affecting some portions of its business, Dropbox's strategic initiatives and product-centric approach position it for continued success in the cloud services landscape.

While competition exists in the cloud storage and collaboration space, Dropbox's solid free cash flow generation and founder Andrew Houston's significant voting power suggest it will likely continue as a stable business offering innovative tools to attract users.

Ultimately, there are more positives than negatives to think about here.

For further details see:

Dropbox: A Mature Business With Strong Free Cash Flows