DBX - Dropbox: In Value Territory

Summary

- Dropbox fell 11% in Friday's trading following the 4Q22 results release.

- However, after digging into the transcripts and financials, I believe that there is a net-positive takeaway and Dropbox is still executing well.

- At a P/S of 3.4, P/E of 14.5 and P/FCF of 10.5, Dropbox definitely provides a strong risk-reward profile and is in value territory.

Relooking Dropbox

In 2021, I had written two deep dive articles on why I believe that Dropbox (DBX) is a boring but stable and fundamentally strong company. Over the past 1.5 years, Dropbox's price has remained relatively flat and experienced a 11% drop last Friday following its 4Q22 results.

However, I believe that Dropbox has been executing well and according to my original thesis two years ago. While macro headwinds have caused Dropbox to underperform internal expectations and much of the growth came inorganically in 4Q22, I believe that Dropbox remains fundamentally sound & the current price means Dropbox is now in value territory. Additionally, given Dropbox's SaaS nature and $2.5b ARR, this also provides downside protection since a third of its market cap is recurring in nature.

Therefore in this article, I will be highlighting some key positives and negatives of 4Q22 results, sharing my opinions on why Dropbox has been executing well and finally providing simple and quick valuations to give a gauge of how much value you can be getting from buying Dropbox today! Should you wish to read my deep dives on Dropbox, you can view them here:

- Dropbox: A 'Boring' But Solid Cloud Company (Jul 2021)

- Dropbox: You'll Be Boxing Yourself If You Don't Buy The Drop (Nov 2021)

The Negatives

While Dropbox posted earnings beat, I believe that most investors and analysts could have been spooked through some of the comments during the earnings call. There were two notable negatives that might worry investors:

- Dropbox underperformed their addition to paying users expectations, attributed to two reasons. (1) High churn from education (2) Softness in teams and plus plans due to macro headwinds

- ARPU fell to $134.53, vs $134.78 for the same period last year

- ARR growth for 4Q slowed to +$83m, where $50m was from

In general, this suggests that the economy isn't doing too well and we should expect further softness in the upcoming year. Investors seemed to be spooked by this, but I personally believe that it is an overreaction.

It should already have been evident that we are living in a period of huge macroeconomic uncertainty now, and many tech and non-tech companies have already started to show weaknesses in their financials. Be it advertising dollars or commerce volume, growth is stagnating and even declining hence this will inadvertently affect subscription dollars. This was also evident in slowing organic ARR growth and falling ARPU. However, I would note that FX headwinds had a $4.2 impact on ARPU hence there was a 3% growth on a constant currency basis.

The Positives

Despite the worrying macro-economic conditions, I actually extracted more positive sentiments from the recent earnings and call:

- No of paying users underperformed in 4Q but still increased 5.8% the full year to 17.77 million vs 16.79 million for the same period last year

- Management diligently followed up on their buyback plan, reducing share count by almost 10% the past 1.5 years. There is still >$700m left in their authorised buyback plan, meaning there is still room for another 10% reduction

- Revenue & FCF is still expected to grow in 2024 at 6% and 8% respectively on their lower estimates range

- GAAP gross margins grew to 80.7%, up from 79.5% the year prior

- Management remained optimistic on the 2024 $1 billion FCF goal

Hence on a net basis, I felt that Dropbox overall results was positive to me as a shareholder. Fundamentals continued to improve with growing revenue, margins (despite inflation) and paying users while management has executed well on their buyback program. If share prices continue to stay low, this will allow even more shares to be bought back in the coming year, and shareholders will directly benefit from this.

SMB Threat

Another aspect that investors could be worried about is that Dropbox's target market is mainly SMBs, who usually fare worse off in a recession. However, due the nature of Dropbox's business -- Cloud SaaS, this means that Dropbox is a necessity to operations and companies will have to continue paying their subscription to use it. For businesses of SaaS nature, users also tend to delay upgrades rather than cancel their plans altogether.

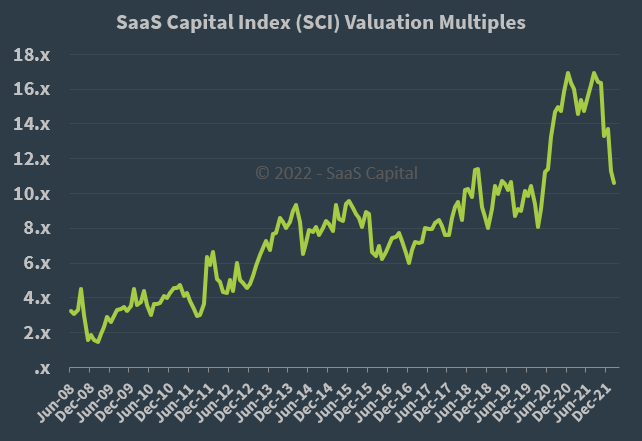

Companies who end up churning are usually those that go under. To put things into perspective, there was a peak business bankruptcy rate of 60,000/year during the 2009 GFC while Dropbox has over 600,000 business teams and 17.7m unique users. Even if we assume the bulk of revenue comes from business teams, and all business bankruptcies are Dropbox's customers, this only increases churn by an absolute 10%. A 10% churn still provides an ARR of $2.25 billion. Even if this repeats for a second straight year, ARR still remains at $2 billion with no additions. At an $8 billion market cap, this represents a P/ARR of 4 at the extreme worse case. This multiple (industry average) was last seen in... you guessed it, 2009!

P/ARR Historical Multiple (SaaS Capital)

{kind=link}

Hence, it is evident that Dropbox is already priced for the extreme worse. I don't like to hassle predictions on the long term SaaS multiples but from a value perspective, it is clear that the upside is much greater than the downside!

Where Is The Value At?

The value of Dropbox is clear, and I want to provide more figures. Using a $22 price, Dropbox has TTM multiples of:

- P/S: 3.4

- P/E: 14.5

- P/FCF: 10.5

- P/FCF (ex SBC): 18.5

This is cheap, no matter what comparisons you want to use. In the long run, I believe Dropbox can grow FCF easily by 10-15%. A simple & conservative breakdown is as follows:

- Increase in paying users +5 to 7% (Constant 2.5% freemium conversion, already on the low end of HBR's 2-5% estimate)

- Growing ARPU +2-3% (Inflation pegged, excluding cross and upselling to be conservative)

- Other growth can come from cross/up-selling and margin expansion, all of which Dropbox are already doing, but will leave out now to be conservative.

Hence, we can see that Dropbox has very attractive financials and we are paying a P/FCF of 10.5 for a 10% minimum growth.

Good Capital Management

With strong FCF, we also need to ensure that it is accretive to shareholders, and this is another aspect that I like Dropbox for. With free cash flow, we can see that management has been engaging in active buybacks to enrich shareholders, together with prudent investments to enhance the Dropbox ecosystem. In a period where many SaaS companies have started moving to larger and pricier acquisitions for growth, Dropbox has stuck to their strategy of small, targeted acquisitions to expand their ecosystem.

Their success has been reflected in the company's high and growing ROIC. Just look at their ROIC compared to competitors!

A Final Angle

Finally, I look at Dropbox using management's $1b FCF target. Following my due diligence, I am relatively confident in Dropbox executing and hitting their target. For this valuation, I will use Dropbox's FCF ex. SBC to be conservative.

| Scenario |

| 1 |

| 2 |

| 3 |

| SBC % of FCF (43% in FY22) |

| 45% |

| 45% |

| 40% |

| FCF ex SBC () |

| 550 |

| 550 |

| 600 |

| P/FCF Multiple |

| 15 |

| 20 |

| 25 |

| Market Cap () |

| 8250 |

| 11000 |

| 15000 |

| Upside % from $8bn Market Cap (2Y Upside) |

| 3.1% |

| 37.5% |

| 87.5% |

For P/FCF I have used three plausible scenarios. First, P/FCF of 15 represents the low range of blue-chip SaaS - Oracle ( ORCL ) and SAP SE ( SAP ). P/FCF of 20-25 represents the average of blue-chip SaaS before the pandemic boom. Dropbox's P/FCF has also largely trended within that range, hence it is reasonable to expect a recovery given strong fundamentals.

Therefore, even at worse, I will still be seeing 3.1% growth in Dropbox's intrinsic value over the next two years, and the upside is extremely large, even when using plausible, realistic FCF and multiples.

Conclusion

In all, I have illustrated that Dropbox is a quality and value investment today. You might notice, I have not done any complex models or projections usually shown in other articles. However, this is because the value in Dropbox is glaring to me. Sometimes, investing can be simple. Dropbox is a simple business. Not a market leader, not fast growing, but this allows the company to thrive under the radar - providing a niche offering to SMBs and providing strong accretive FCF to investors.

I will note some risks before ending. Admittedly Dropbox is unloved by the market and will require strong catalysts to be revalued at a premium. I don't see many strong catalysts beyond future earnings beat for now. If macro-environment deteriorates worse than expected, earnings targets would also be revised downwards. However, I mainly used TTM multiples so even if Dropbox records 0% growth in FY23, the valuation here will remain the same. In all, I believe the risk-reward profile of Dropbox is very attractive and more so given the uncertain investment climate today.

For further details see:

Dropbox: In Value Territory