DBX - Dropbox: Investment Thesis Update

2024-01-09 07:28:33 ET

Summary

- Dropbox's financial performance has exceeded expectations, with revenue expected to increase by 7.4% in 2023.

- The integration of acquired companies and the addition of new services have improved Dropbox's offerings.

- The main investment thesis remains the same, focusing on Dropbox's ability to generate cash flow and use it for buybacks.

Introduction

More than a year has passed since my first article on this platform and the topic was precisely Dropbox (DBX). Re-reading it I see many critical issues and I am much more proud of the last analysis I did, so the purpose of this article is to build on the previous one to see if the proposed investment thesis is still valid and to assess whether the conditions that made me invest in Dropbox have changed over this year.

You can find the original article here .

Initial Hypotheses

The main arguments behind the old analysis concerned Dropbox's ability to generate large amounts of cash on a consistent and sustained basis and given the low level of CapEx, use this excess cash to buy back its own shares.

Risk factors were mainly related to the extreme competition in the cloud sector, and pessimism toward the company was fueled by the reduction in revenue growth rates. In the previous article, I had focused on giving price targets based on management's goal of reaching a FCF of $1 billion in 2024 and the hypothetical reduction of outstanding shares through buybacks. I consider it a mistake from the perspective of the long-term investor to consider such short-term price targets; in fact, these can easily be rendered meaningless by short-term market conditions that do not affect the company's ability to generate satisfactory returns over the long term. Therefore, this time I will focus only on estimating the intrinsic value of Dropbox using the DCF model.

Financial Results

Beats & Misses (tikr.com)

In the previous five quarters Dropbox has managed to consistently perform better than analysts' expectations, and taking into account estimates for Q4, overall in 2023 revenue is expected to increase by 7.4 percent over 2022 to nearly $2.5 billion and an estimate by management of FCF of between $820-$840 million. This growth was boosted by higher prices and a slight increase in paying users. Reduced operations in the Private Equity and Venture Capital sector were a slowing factor for revenue growth, given the extensive use in this sector of services offered by Dropbox, such as HelloSign and DocSend (renamed Dropbox Sign and Dropbox DocSend). Positive, on the other hand, was the growth of FormSwift, above management's expectations. Finally, diluted weighted average shares outstanding are expected to be in the range of 345 to 350 million.

I believe that the past year has been good for Dropbox, not only because of its financial performance, but also because the integration of previously acquired companies and the addition of new services and enhancement of existing products have made Dropbox's offerings better than 2022. What I appreciate about co-founder and CEO Drew Houston is the obvious long-term vision and M&A policy. Indeed, in 2021 in particular we have seen a lot of M&A by many companies, acquisitions of enormous size and in most cases completed through extensive use of debt with the ultimate goal of showing the market significant revenue growth. On the other hand, analyzing the acquisitions completed by Dropbox, we can see a desire to integrate technologies and services that can improve the products and services offered to customers and not done simply to show major growth over the previous year.

New Hypotheses

Today the main arguments behind a potential investment in Dropbox in my opinion do not differ from those of a year ago. In fact, the most important variables to consider are Dropbox's ability to continue to generate large and growing cash flows (albeit less than a few years ago) and to use this excess cash to remunerate shareholders through buybacks. The old target of 1 billion FCF in 2024 has been lowered slightly to $964 million because of $36 million they expect to have to pay due to R&D tax legislation. The current market capitalization is about $10 billion, the impact of the continuation of the share buyback policy is still considerable (even if dilution due to share-based compensations is taken into account).

Operationally, the company has improved since last year, and a future lowering of interest rates could lead the private equity and venture capital sectors back to growth in terms of deals closed and could be a positive catalyst for Dropbox.

{kind=link}

Analysts' growth estimates for the next 3 years have been lowered from last year, and only 3.1% revenue growth is expected for 2024. In my opinion Dropbox can easily beat these expectations (barring any nasty surprises for the economy in 2024).

{kind=link}

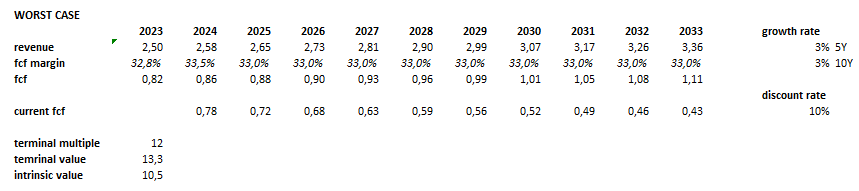

Assuming a pessimistic scenario of constant revenue growth for 10 years of 3 percent, a FCF below both analysts' and management's expectations, and a distribution of this FCF to shareholders of 100%, the company to date seems correctly valued to offer an average return of 10 percent per year. If the terminal multiple is lowered from 12 to 8 the intrinsic value is reduced to $9 billion.

{kind=link}

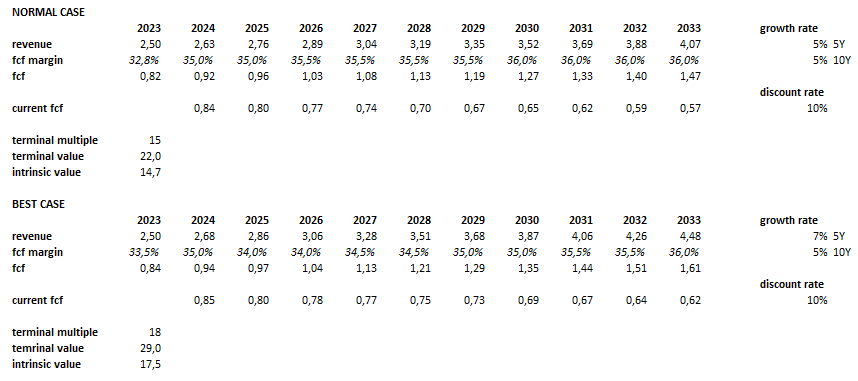

If we take into account estimates that are more optimistic than the previous one and more in line with analysts' and management's expectations, Dropbox would currently appear to be undervalued and could offer a significant margin of safety for the long-term investor.

Conclusion

Dropbox's stock price when I wrote the previous article was about $23, I personally bought the shares at an average price of $20 and although to date the price is between $29 and $30 I see no fundamentally sound reason to sell my shares. At current valuations, I still consider Dropbox to be an investment with an excellent risk/return ratio that could offer satisfactory returns.

In conclusion, as you have read in the preceding paragraphs, the crucial factor in this investment thesis is Dropbox's ability to continue to consistently buy back its own stock. The case of Apple provides us with a good example of how a consistent and continuous share buyback policy can bring exceptional results, even if the growth of the underlying business is modest.

For further details see:

Dropbox: Investment Thesis Update