DBX - Dropbox: Navigating The Crossroads Of Value Potential And Slowing Growth

2023-05-28 11:01:28 ET

Summary

- Dropbox displays strong free cash flow but faces slowing growth, evident from the 8.7% YoY revenue growth in Q1 2023.

- Positioned as a potential value stock, Dropbox grapples with maintaining growth amid fierce competition and a slowing core product.

- The company's survival strategy hinges on diversifying product offerings and continuing to innovate in the face of tech giants.

- Dropbox's future hinges on achieving ambitious targets including sustaining a ~7% p.a. growth rate and generating $1 billion in Free Cash Flow by 2024.

In the rapidly evolving world of technology, the story of Dropbox (DBX) represents an intriguing puzzle for investors, analysts, and industry watchers alike. A stalwart of the industry, Dropbox is known for generating robust free cash flow, a testament to its economic health and managerial efficiency. Yet, over the past year, the company's stock performance has lagged behind the broader tech market, setting the stage for a nuanced discussion about its present condition and future trajectory.

Indeed, the profitability of Dropbox is undeniable and reassuring. It speaks to a business model that delivers and can hold its own even in an intensely competitive landscape. However, the narrative takes a twist when considering the company's growth dynamics. In recent times, the growth rate has slowed down, creating a dichotomy between the company's strong value proposition and its diminished growth prospects.

As we delve deeper into the Dropbox puzzle, we are prompted to navigate a complex network of contributing factors. The questions are many: Can Dropbox continue to generate substantial free cash flows? How will it grapple with the deceleration in growth? Is it still a viable player amidst competition from tech behemoths? And ultimately, what should potential investors make of this scenario?

Revenue Deceleration: A Speed Bump

Dropbox's Q1 2023 results , while not bleak, signaled yet another potential sea change in its financial health. Despite robust free cash flow and strategic initiatives, revenue growth of 8.7% YoY—down from 9.9% YoY in Q1 2022—has shone a spotlight on the tech stalwart's financial trajectory.

This deceleration in revenue and Free Cash Flow growth, although not catastrophic, necessitates a reassessment of Dropbox's outlook. In a competitive tech landscape where innovation is relentless and market share is hard-fought, slowing revenue growth can raise questions about a company's strategy, its response to market dynamics, and the impact on customer retention.

The deceleration is particularly poignant for Dropbox, considering that most of its Q1 revenue growth has been derived from pricing strategies. The company witnessed an increase in average revenue per paying user by $4.44 from Q4 2022. Simultaneously, the influx of new paying users has continued to wane, with Q1 2023 witnessing a decline to a mere 130,000, a far cry from the nearly 300,000 new paying users per quarter in the preceding two years.

This underscores a fundamental shift in Dropbox's growth narrative. With a growing reliance on pricing rather than user expansion for revenue generation, Dropbox is at a crossroads in its tech stock journey. This development has crucial strategic implications, calling for a re-evaluation of its growth model and the underlying value proposition. Dropbox may need to reassess its strategies to stimulate user growth and diversify its revenue streams.

{kind=link}

Navigating the Growth-Value Paradox

The intriguing paradox of Dropbox's current state pertains not merely to whether it classifies as a value stock but to the extent to which it can preserve its growth narrative amidst the encroaching pressures of a decelerating core product and an aggressively competitive cloud storage market. Faced with a slowing core product and the external headwinds of competition, Dropbox finds itself at the intersection of growth and value investing. The company's ability to successfully navigate this juncture hinges upon its agility to devise strategies to counteract these challenges, innovate, and remain competitive in a saturated market.

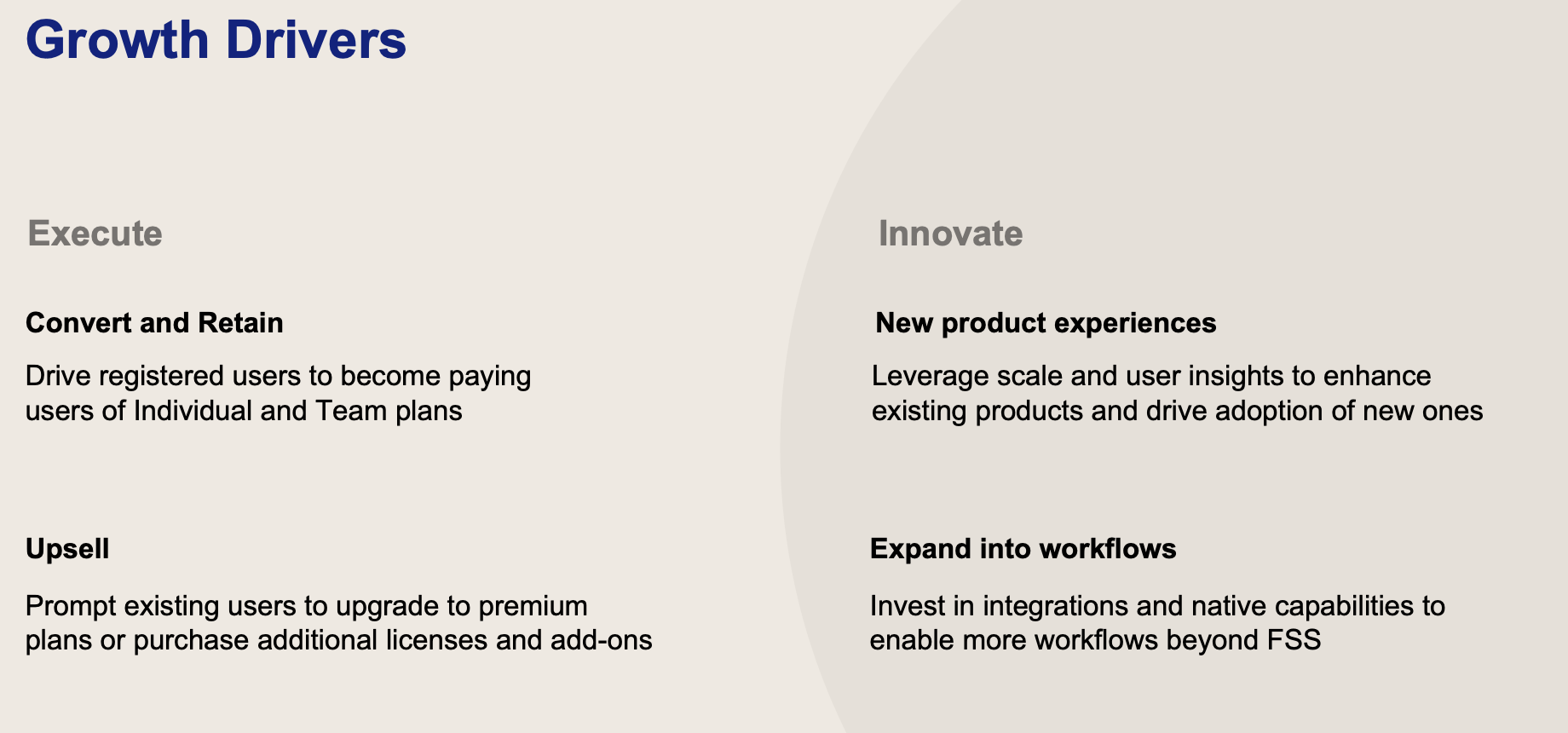

The company's continued strong free cash flow generation gives it a significant competitive advantage. Yet, in the face of a decelerating core product, Dropbox must diversify its product offerings and capitalize on its current assets to sustain growth. This might involve a more aggressive push into new growth segments like e-Signature and document analytics, which have shown promise. The stronger push for profitability and uncertainties also become visible in Dropbox's recent layoff of about 16% of its workforce .

Equally, navigating the competitive landscape will require fortifying its value proposition against the backdrop of tech giants such as Google ( GOOG ) (GOOGL), Microsoft ( MSFT ), and Apple ( AAPL ). Although Dropbox has remained among market leaders despite these competitors' presence, an ongoing assessment of competitive threats and strategic responses is crucial for survival.

In essence, Dropbox's ability to uphold its growth trajectory and maintain its stature as a value stock largely hinges on its ability to balance these dual challenges of maintaining momentum amidst a slowdown in its core product and sustaining its ground amidst fierce competition. This balancing act, thus, emerges as a critical component of Dropbox's strategic roadmap.

{kind=link}

Future Prospects: Balancing Valuation and Growth

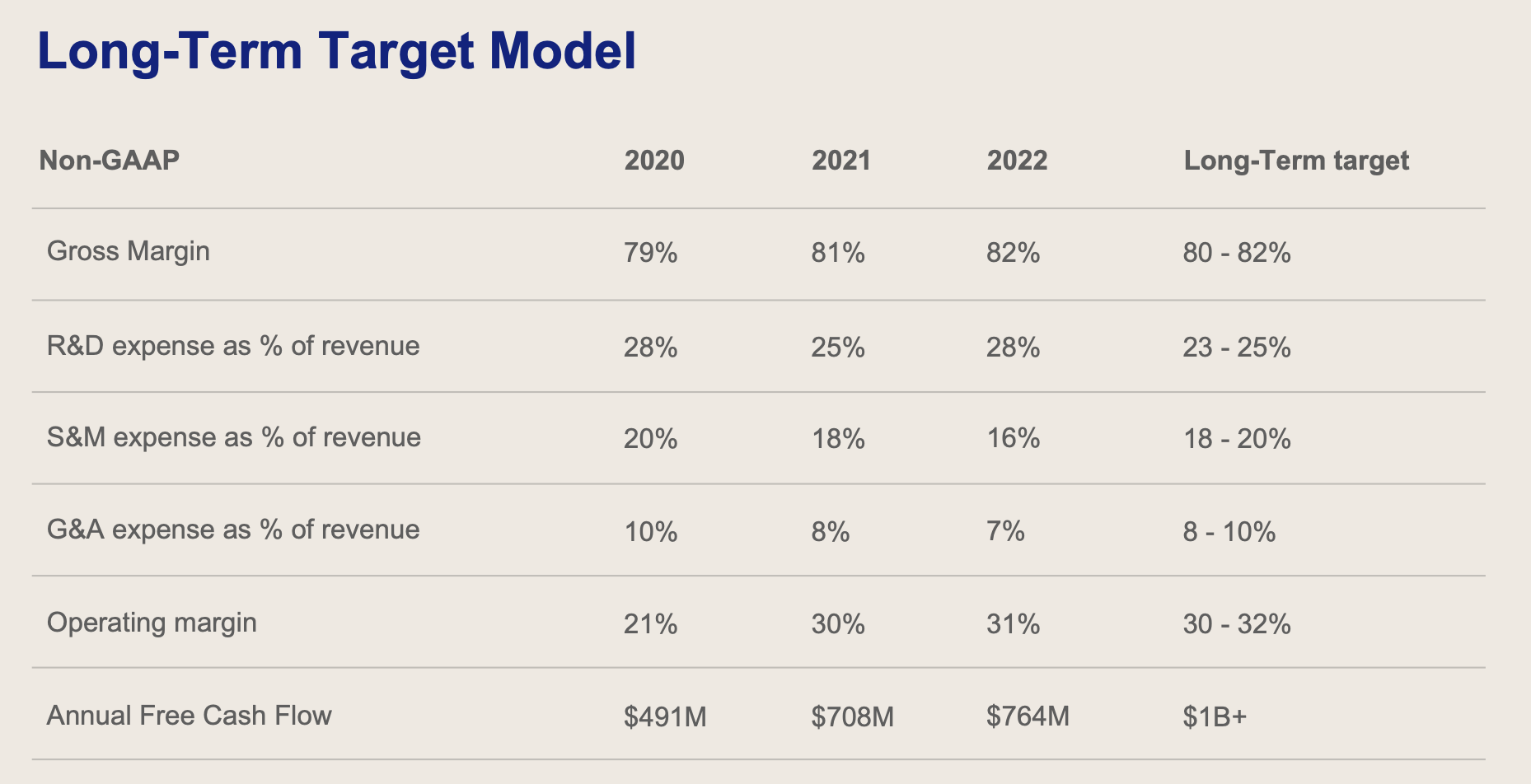

Despite the hurdles, there are reasons for cautious optimism regarding Dropbox. A compelling aspect lies in its forward P/E multiple of a modest 12.11, well below industry norms, hinting at the potential undervaluation of the stock. Furthermore, the ambitious target set forth by Dropbox's management team, aiming to generate $1 billion in Free Cash Flow by 2024, also lends weight to the bullish outlook.

Nevertheless, the realisation of these targets is anything but guaranteed. It rests precariously on the company's ability to strike a careful balance between valuation and growth. The key benchmark set by management — sustaining a growth rate of ~7% per annum — is an ambitious one. Even more so, considering the downward pressure on Dropbox's revenue growth and the mounting competition it faces in the cloud storage market.

In addition, the company's objective to maintain an operating margin of 30-32% necessitates a rigorous focus on cost efficiencies and operational excellence. Achieving this will require not just sustaining its core business but also ensuring the profitability of new ventures like e-Signature and document analytics offerings.

In essence, while Dropbox's future prospects may appear promising at a glance, they hinge on its ability to navigate an array of challenges and to strike an optimal balance between growth and value. The road ahead for Dropbox is strewn with potential and pitfalls alike, making it a company to watch in the coming years.

Conclusion: A Balanced Outlook

The narrative around Dropbox is a complex tapestry of robust free cash flow, ambitious management targets, decelerating core product growth, and intense competition. The interplay of these factors creates a compelling but cautious investment story.

The company's track record of free cash flow generation and its potential for undervaluation make a persuasive argument for considering Dropbox as a value investment. However, there are caveats to this optimism. The ambitious growth targets and the required operating margins hinge on the company's ability to counteract the decelerating growth of its core product and to navigate the highly competitive landscape.

As Dropbox strides into the future, the need for striking the right balance between preserving value and pursuing growth will be more pressing than ever. The company's journey ahead promises to be an interesting spectacle, not just for its stakeholders but also for those keenly observing the dynamics of the cloud storage market.

While Dropbox's future is not without challenges, it remains a company with substantial potential — if it can successfully meet the demands of its shifting landscape. It is a company that merits close observation as it endeavours to chart a course through its unique blend of opportunities and obstacles.

For further details see:

Dropbox: Navigating The Crossroads Of Value Potential And Slowing Growth