DBX - Dropbox: Proving Its Clout

2023-05-08 18:00:53 ET

Summary

- Dropbox rallied after the company released strong Q1 results.

- The company managed to accelerate revenue growth to 9% y/y, or 11% y/y on a constant-currency basis.

- It is also eliminating 16% of its workforce, which should boost profitability in the long run.

- The company also has ~$600 million left on its share buyback authorization, or roughly 8% of its outstanding market cap.

At this time when interest rates are soaring and not expected to fall until the end of the year, most investors have the same thing in mind: safety is best. Tech stocks with rich valuations have been dramatically pummeled since last year, but that doesn't mean the sector isn't worth looking into: but it's now about finding growth at a reasonable price.

Dropbox ( DBX ) fits the bill perfectly here. Now a household name for file sharing and storage, Dropbox has never really been a growth star - but that's almost what we're looking for in the market of 2023. Down ~6% year to date while most other mid-cap tech stocks have eked out a gain, Dropbox has begun to turn the tide with a small rally after its recent Q1 earnings print, and I think there is plenty of steam left to go.

I remain bullish on Dropbox (I entered the position first in the low $20s, and then doubled down when the stock briefly broke below $20). Of course, Dropbox no longer has the soaring growth potential of a newly minted tech startup. Even its buzzy initiatives to overhaul its product portfolio (namely implementing AI-driven features into its core products) are unlikely to spark substantial growth. But the key here is that for the largesse of its recurring-revenue base and the richness of its margin profile, Dropbox is quite severely undervalued.

And while it's unfortunate, I also find Dropbox's recent layoffs (500 heads, or roughly 16% of its workforce) to be an encouraging long-term signal that management is acting prudently for the future and taking advantage of the current recession to trim fat and focus on efficiency. It's worth noting that the company has hung on tight to its goal of generating $1 billion in free cash flow by 2024.

Here is the full long-term bull case for Dropbox:

- Dropbox isn't just trading on a pie-in-the-sky future projection, but on real free cash flow today, singling out from other SaaS stocks in this risk-averse environment. Growth and paying premiums for growth stocks are out; value is in. The fact that Dropbox has routinely dangled a target of hitting $1 billion in annual FCF by FY24 while continuously raising operating margins quarter after quarter is a big draw for investors. Note that in FY21, Dropbox already hit north of $700 million in free cash flow, so I think it's highly likely that this original $1 billion target gets replaced with something more aggressive.

- Consumer upsells- More and more freelancers have emerged from the pandemic, untethering themselves from a corporate lifestyle and building brands and businesses of their own. Tools like Dropbox have become necessary infrastructure, and one with very low barriers to entry and ease of setup. Accordingly, Dropbox has differentiated itself from Box by appealing to these professional solo acts and small businesses, which is reflected by Dropbox's greater upsells to premium paid plans.

- Enterprise market opportunity- Dropbox's traditional strength has always been in smaller/consumer users, though it has started ramping up its enterprise efforts lately (products like Capture add to the company's enterprise resume). There are still plenty of opportunities for Dropbox to take market share from Box here.

- E-signature opportunity- The addition of an enterprise tool like DocSend (acquired in 2021 and recently rebranded as Dropbox Sign) will further flex Dropbox's muscles in the enterprise space, helping it catch up to its rival Box (the latter of which has long touted superior security capabilities). Like the rest of Dropbox's product portfolio, Dropbox Sign has a range of plans and pricing for users of various budgets and levels of sophistication, giving it immediate cross-sell applicability to all segments of Dropbox's customer base.

And in spite of these longer-term strengths, Dropbox is still quite undervalued. At current share prices just north of $21, Dropbox trades at a market cap of $7.56 billion. After we net off the $1.25 billion of cash and $1.37 billion of convertible debt on Dropbox's most recent balance sheet, its resulting enterprise value is $7.68 billion.

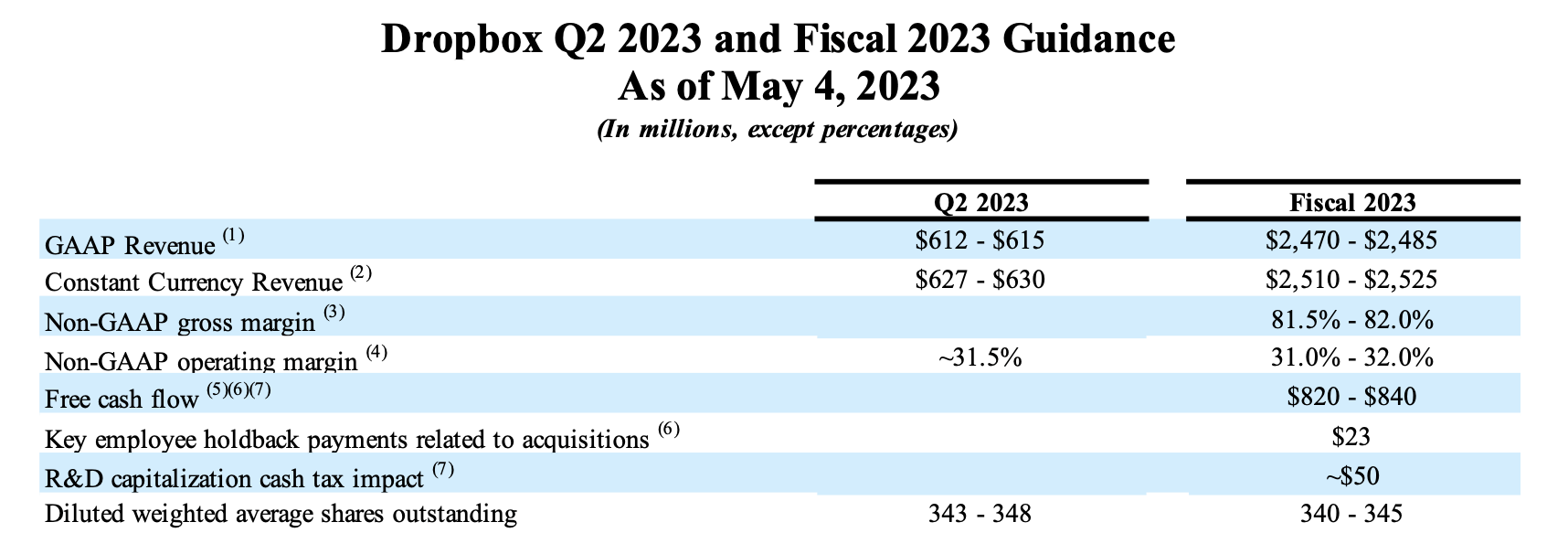

Meanwhile, for the current fiscal year Dropbox has roughly held its guidance of $2.470-$2.485 billion for the year (6-7% y/y growth), and free cash flow of $820-$840 million representing a 33-34% margin:

{kind=link}

Using the midpoint of these guidance ranges puts Dropbox's valuation multiples at:

- 3.2x EV/FY23 revenue

- 9.2x EV/FY23 FCF

Not only is the latter free cash flow multiple incredibly enticing, it's worth noting as well that Dropbox has been taking advantage of share price weakness to execute its buyback plan - of which there is still $573 million remaining as of the end of Q1, worth about 8% of the company's market cap. In my view, a "fair" multiple for Dropbox is at least 12x EV/FY23 FCF, representing a price target of $28 and ~30% upside from current levels - especially as Dropbox still intends to hit $1 billion in FCF (+19% y/y) next year, driven by continued margin expansion and opex reductions.

Stay long here.

Q1 download

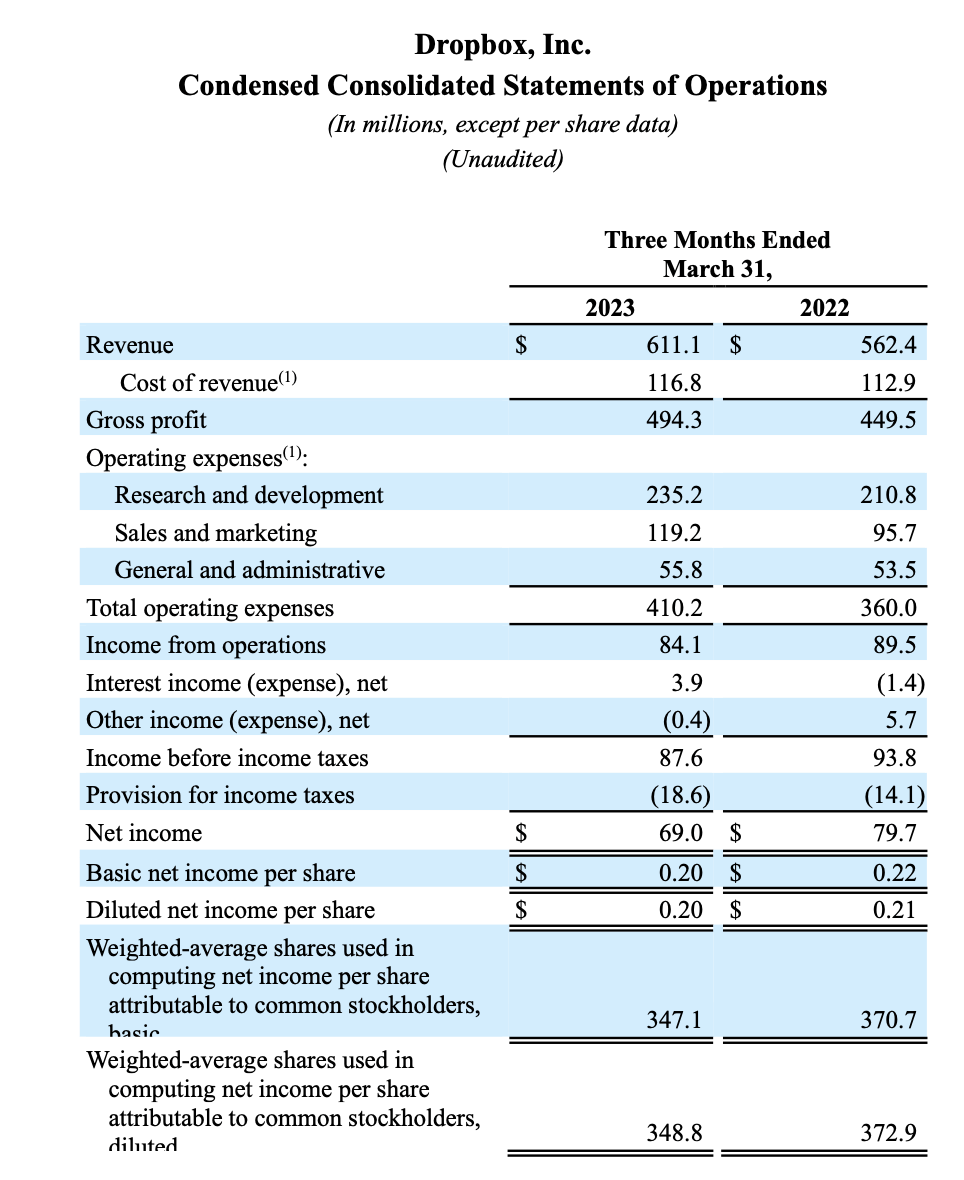

Dropbox's Q1 print, released in early May, was an upside surprise for most investors. Take a look at the earnings summary below:

{kind=link}

Revenue grew 9% y/y to $611.1 million, squarely beating Wall Street's much more modest expectations of $601.2 million (+7% y/y) in a quarter where earnings beats have become very rare for tech stocks. Note as well that Dropbox achieved substantial re-acceleration in growth with over 6% y/y growth in Q4, which the company attributed to better performance and retention within its core products as well as overachievement in FormSwift, a recent Dropbox acquisition that helps clients create legal documents. Note as well that growth on a constant-currency basis at 11% y/y would have been much stronger, as foreign exchange continues to be a headwind for Dropbox.

Dropbox management noted that it isn't immune to the weakening macro environment. Per founder and CEO Drew Houston's remarks on the Q1 earnings call:

Overall, I'm pleased with how we performed in Q1 during a challenging environment. We beat our guidance across all metrics, led by revenue outperformance in FormSwift, which we acquired in late Q4 and some better performance around individual sign-ups exiting the quarter.

On the flip side, we saw continued weakness across our team's plans as our customers face pressure in their own businesses. And we also saw a continued moderation in our DocSend and Dropbox Sign businesses due to ongoing softness in their respective markets.

Over the last several months, we've noted that we're not immune to the increasing macro headwinds that our customers are also facing. And during this period, we've carefully evaluated our different business units and recognize that some investments which showed promise before the downturn have less potential today."

In spite of these headwinds, the company added 120k net-new customers to its base to end the quarter at 17.9 million paid users, up 5% y/y.

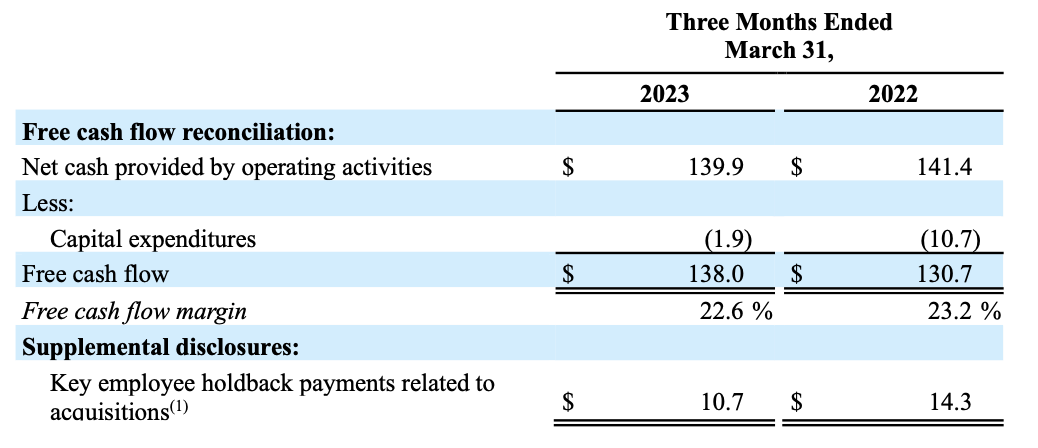

From a margin perspective, Dropbox also inched up pro forma gross margins by 110bps y/y to 82.4%, while free cash flow grew 6% y/y to $138 million:

{kind=link}

Key takeaways

In my view, with Dropbox we don't really need the company to hit many home runs in order for the stock to re-rate to a fairer multiple of free cash flow. A steady stream of earnings beats in which Dropbox continues to show revenue hitting targets and free cash flow growth should help the company nudge its stock back upward.

For further details see:

Dropbox: Proving Its Clout