DBX - Dropbox: Raising Price Target; The Runway Is Long

2023-08-06 23:33:27 ET

Summary

- Dropbox had a strong showing in Q2, with a 6% post-earnings pop that cheered better-than-expected revenue.

- The company continues to roll out new features, including those powered by AI to intelligently search and organize customers' content.

- Dropbox's FCF and operating margins in the ~30% are nearly unparalleled in the software industry.

- Trading at attractive multiples of FCF, Dropbox has plenty of steam to rally further.

Earnings season is in full swing and putting a strong test to tech stock rallies. As interest rate fears cool down and investors wade back into risk-taking, Q2 fundamental results (which are turning out more beats than misses across the board) are hoping to prove that the rebound is justified.

Dropbox ( DBX ) had a strong showing in Q2. The file sharing software company saw a 6% post-earnings pop, bringing its year-to-date gains above 20%. And though Dropbox is now trading at highs not seen since 2021, I'd argue the stock has long been undervalued and has plenty of runway left to rally further.

Dropbox's bull case rests on strong cash flows

I remain bullish on Dropbox and continue to hold onto the stock in my portfolio, and am raising my price target through the end of the year. I see Dropbox as a category leader in enterprise collaboration and file sharing, and a sturdy company that has found a way to balance consistent growth rates alongside healthy margin expansion. Though certainly no longer an exciting tech stock that is seeing explosive growth rates, Dropbox is making the transition to the later phase of a tech stock's lifecycle: growing profits, and justifying its valuation through earnings and cash flow.

It's worth noting as well that Dropbox has some product-driven catalysts for growth, including and especially in the applications of AI technology. New file preview technology helps users get quick summaries of content without having to parse through entire files. In addition, a new "Dropbox Dash" search function uses AI to point users toward recommended content and organize links into a single dashboard.

Here is my full long-term bull case for Dropbox:

- Sticky subscription business. In this macro environment, subscription revenue streams have become even more desirable due to the ease of planning cash flow and the reliability of low-churn customers. On top of high gross margins, Dropbox has a powerful formula for success.

- Dropbox isn't just trading on a pie-in-the-sky future projection, but on real free cash flow today, singling out from other SaaS stocks in this risk-averse environment. Growth and paying premiums for growth stocks are out; value is in. The fact that Dropbox has routinely dangled a target of hitting $1 billion in annual FCF by FY24 while continuously raising operating margins quarter after quarter is a big draw for investors. Note that in FY21, Dropbox already hit north of $700 million in free cash flow, so I think it's highly likely that this original $1 billion target gets replaced with something more aggressive.

- Consumer upsells. More and more freelancers have emerged from the pandemic, untethering themselves from a corporate lifestyle and building brands and businesses of their own. Tools like Dropbox have become necessary infrastructure, and one with very low barriers to entry and ease of setup. Accordingly, Dropbox has differentiated itself from Box by appealing to these professional solo acts and small businesses, which is reflected by Dropbox's greater upsells to premium paid plans.

- Enterprise market opportunity. Dropbox's traditional strength has always been in smaller/consumer users, though it has started ramping up its enterprise efforts lately (products like Capture add to the company's enterprise resume). There are still plenty of opportunities for Dropbox to take market share from Box here.

- E-signature opportunity. The addition of an enterprise tool like DocSend (acquired in 2021 and recently rebranded as Dropbox Sign) will further flex Dropbox's muscles in the enterprise space, helping it catch up to its rival Box (the latter of which has long touted superior security capabilities). Like the rest of Dropbox's product portfolio, Dropbox Sign has a range of plans and pricing for users of various budgets and levels of sophistication, giving it immediate cross-sell applicability to all segments of Dropbox's customer base.

Valuation for Dropbox also remains incredibly appealing. At current share prices just north of $27, Dropbox trades at a market cap of $9.61 billion. After we net off the $1.23 billion of cash and $1.37 billion of convertible debt on Dropbox's most recent balance sheet, the company's resulting enterprise value is $9.75 billion.

For FY24, Wall Street analysts are expecting Dropbox to generate $2.60 billion in revenue, representing 5% y/y growth (data from Yahoo Finance ). If we apply this year's expecting FCF margin of 33.3% on next year's revenue, estimated FY24 FCF assuming no further margin expansion would be $858 million, putting Dropbox's valuation at 11.4x EV/FY24 FCF.

I'm raising my year-end price target on Dropbox to $32, representing a 13x EV/FY24 FCF multiple and ~15% upside from current levels, up from a prior price target of $28.

Stay long here and keep riding Dropbox's upward momentum.

Q2 download

Let's now go through Dropbox's latest quarterly results in greater detail. The Q2 earnings summary is shown below:

{kind=link}

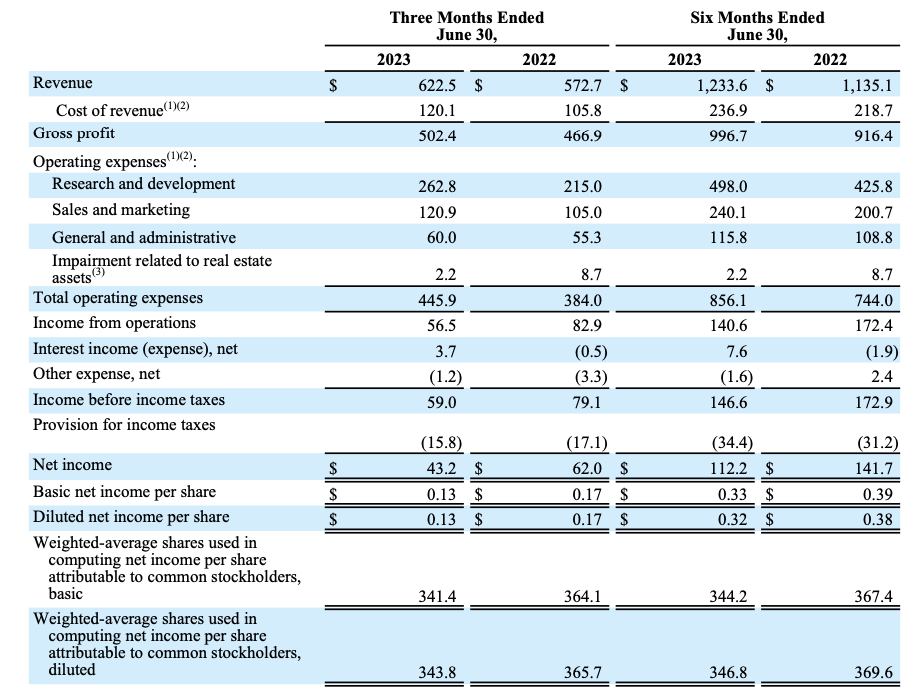

Revenue grew 9% y/y to $622.5 million, beating Wall Street's much more modest expectations of $613.2 million (+7% y/y) by a two-point margin. It's worth noting as well that revenue growth kept pace with Q1's growth rate of 9% y/y (which in turn had accelerated over 6% y/y growth in Q4).

And despite Dropbox's reputation as an older software company, the company has still identified a number of growth drivers to keep its revenue engine humming. Its primary strategy is still a "land and expand" sales approach, getting customers onto free or low-tier plans and eventually converting them to higher paid plans.

{kind=link}

The company is also continuously upgrading its tech stack to broaden its appeal and expand into workflow tools, which would help the company nab share from competitors like Asana ( ASAN ) and Atlassian ( TEAM ).

The slide below also shows some of the company's newest capabilities, including AI-assisted file organization and smart tagging/indexing for users to be able to find their content easier and faster:

{kind=link}

Here is some helpful context on the company's product strategy from CEO Drew Houston's remarks on the Q2 earnings call :

Over time, we plan to release more advanced use cases, such as Dash Answers, where users can ask any question or receive a specific answer about a piece of content instead of having to click through lots of search results or dig through specific files and folders. I'm looking forward to getting Dash in the hands of many more customers over the coming months.

Along with Dropbox Dash, in Q2, we also advanced our core product roadmap with the launch of Dropbox AI. Now, Dropbox Professional and Dropbox Teams users can leverage Dropbox AI on their file previews page to summarize their content with a single click, whether it's a 100-page document or even a long video. Users can also ask the question for Dropbox AI to answer based on content within a file, and over time we plan to apply this functionality to folders and eventually the user's entire Dropbox.

We're encouraged by the early engagement from the users who have tried Dropbox AI for their files. And as we increased discoverability for this new functionality for more users, we're excited to see how Dropbox AI can ultimately increase customers' productivity.

We'll continue to evaluate the performance on this new AI-powered product experiences as well as other in-house capabilities we're building within Dropbox. And we're not doing this alone. Last month, we were featured as a global partner for Meta's Llama 2 launch. And we also announced Dropbox Ventures to support the next generation of AI start-ups."

The company expects a more robust product portfolio to improve multi-product attach rates among its customer base. In Q2, overall ARR grew 11% y/y on a constant-currency basis to $2.5 billion, nearly the size of next year's consensus revenue expectations.

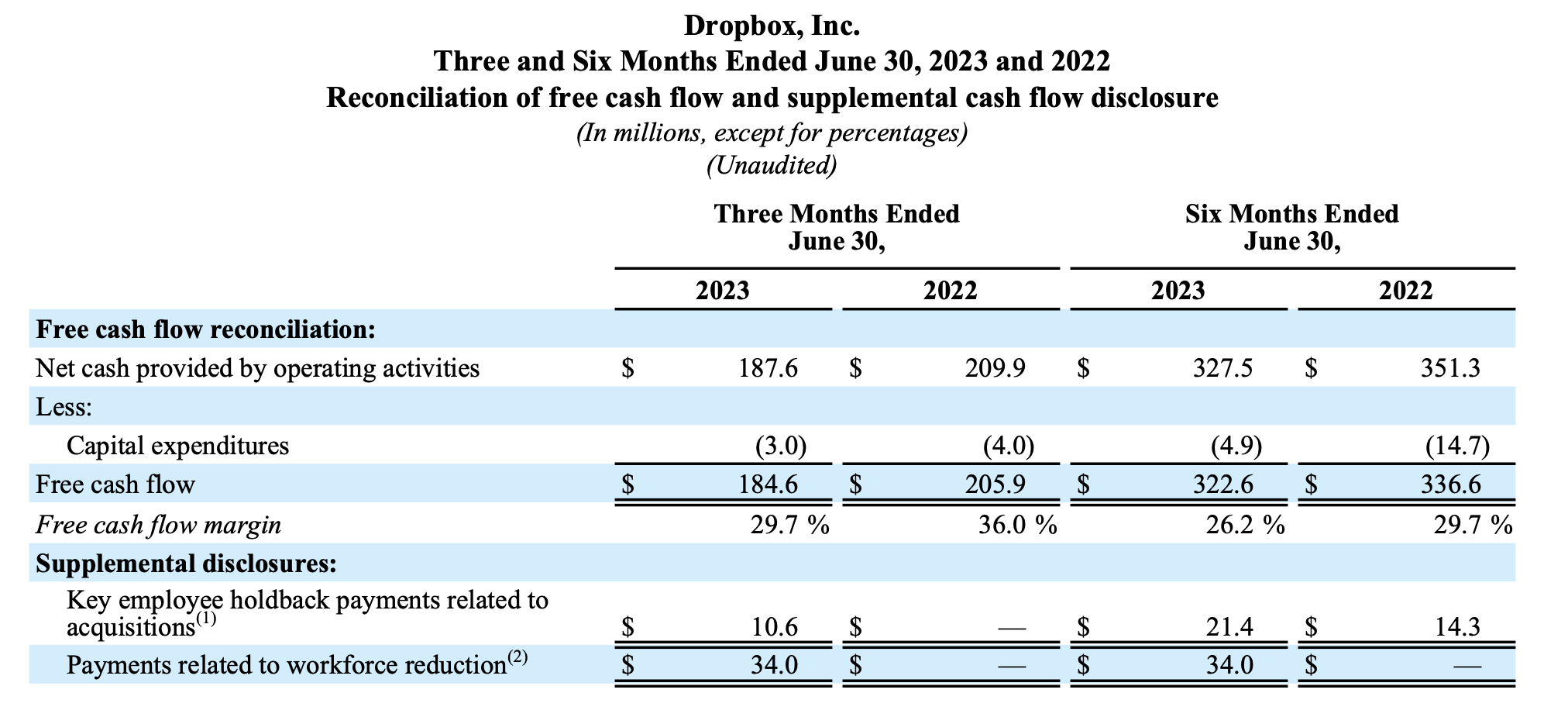

And from a margin perspective, the company notched a 34.2% pro forma operating margin in Q2, 230bps better than 31.9% in the year-ago quarter. This was driven by strong gross margins (83% on a pro forma basis) and lower cost associated with the layoffs that the company enacted in April. Free cash flow, however, declined slightly to $184.6 million, or a 29.7% margin.

{kind=link}

It's worth noting that after adjusting for $34 million in severance-related payoffs from the headcount reductions that helped boost margins, Dropbox's FCF would have grown to $218.6 million or a 35% FCF margin more in line with last year.

Key takeaways

Strong cash flows, continuous product innovation, a massive ARR base and a sticky subscription customer pool - there's a lot to like about Dropbox especially at a low-teens FCF multiple. Stay long here.

For further details see:

Dropbox: Raising Price Target; The Runway Is Long