BNDW - DSL: Nice International Exposure But This CEF Is Overpriced

2023-09-11 07:31:27 ET

Summary

- DoubleLine Income Solutions Fund offers a high level of current income with a 10.95% distribution yield.

- The fund's price has remained remarkably stable, in direct contradiction to the American bond market.

- The fund has significant exposure to non-American issuers, providing valuable international diversification for investors.

- The fund failed to cover its distribution in the most recent half-year period, heightening my concerns about a possible distribution cut.

- The fund is trading at a premium, which is above the 52-week average and makes no sense given the risks surrounding its distribution.

As the name of the fund implies, the DoubleLine Income Solutions Fund ( DSL ) is a closed-end fund that income-seeking investors can purchase in order to earn a high level of current income from their portfolios. This is evident in the fact that the fund currently boasts a 10.95% distribution yield, which is obviously significantly higher than most other things in the market. Unlike most other income-focused funds, this one has not exhibited a substantial year-over-year decline. In fact, the fund's shares have been almost totally flat over the past twelve months:

{kind=link}

The fact that the fund's performance does not appear to have been hampered by the broader weakness in both the stock and fixed-income markets is something that is undoubtedly going to be appealing to any risk-averse investor who is concerned with preserving the value of their principal. Another appealing characteristic is the fact that this fund has historically traded for a price that is slightly below its intrinsic value. That is not the case right now though, as the fund's recent performance has apparently renewed investor interest in it and seemingly pushed up the value of the fund's shares. As a result, the fund is trading at a slight premium to its net asset value. This implies that it may be best to wait for the fund's shares to decline a bit before purchasing its shares.

Another possible concern is the one that I pointed out in my last article on this fund. In short, the fund failed to cover its distribution during the most recent full-year period. However, that article was several months ago and the period in question is quite a bit in the past at this point. Despite failing to cover its distribution during that period, the fund did not cut the payout. As such, it is a good idea to revisit this fund using more recent data in order to determine just how sustainable its payout is likely to be. In addition, an update on the fund's portfolio could be helpful for current investors or those considering purchasing this fund. Let us investigate and see if purchasing this fund today makes any sense.

About The Fund

According to the fund's webpage , the DoubleLine Income Solutions Fund has the objective of providing its investors with a high level of current income. This certainly fits well with the fund's name, which strongly suggests that it invests in a portfolio of fixed-income securities. The portfolio itself confirms this assumption. As we can see here, 96.19% of the fund's assets are invested in bonds with the remainder invested in very small allocations to both cash and common stock:

CEF Connect

I explained why the fund's objective makes a great deal of sense considering the fixed-income portfolio in my previous article on this fund:

As such, it is not especially surprising that the fund's objective would center around current income. This is because bonds and other fixed-income securities provide the overwhelming majority of their investment return through direct payments made to investors, with only a limited potential for capital gains. That makes sense since bonds have no direct link with the growth and prosperity of the issuing company. After all, a company will not increase the amount of money that it pays to its bondholders simply because its income improved.

As I have pointed out in numerous previous articles, and as everyone reading this is likely well aware, the bond market has had a very challenging time since the start of 2022. This is due to the Federal Reserve reversing its longstanding policy of easy money and switching to a monetary tightening policy in an attempt to curtail the incredibly high inflation that has been prevalent throughout the American economy since the pandemic. As of the time of writing, the federal funds rate is at a higher level than we have seen since the popping of the Internet bubble back in 2001:

{kind=link}

The effective federal funds rate today is 5.33%, which is a level that has not been seen since February of 2001. This is obviously substantially higher than the 4.57% effective federal funds rate that was present the last time that we discussed this fund. Despite that, the fund's share price is actually up:

{kind=link}

This is the exact opposite of what we would expect from a bond fund in a rising-rate environment. After all, bond prices go down when interest rates go up. We can see this in the fact that the Bloomberg US Aggregate Bond Index ( AGG ) has actually declined since March 20, 2023, which was the last time that we discussed this fund:

{kind=link}

Part of the explanation for this comes from the fact that the DoubleLine Income Solutions Fund does not invest solely in American bonds. The fund's website explicitly states:

The fund will seek to achieve its investment objectives by investing in a portfolio of investments selected for their potential to provide high current income, growth of capital, or both. The fund may invest in debt securities and other income-producing investments anywhere in the world, including emerging markets.

As of the time of writing, only 41.75% of the securities contained in the fund are American fixed-income issues:

CEF Connect

This could partially explain some of the fund's performance. After all, the Federal Reserve does not control interest rates in nations other than the United States. Those nations that did not increase interest rates would not have a corresponding decline in their bond values. With that said, the high inflation rates that we have been seeing are a global phenomenon and many central banks around the world have raised their benchmark rates over the past year. Out of the members of the Group of 20 nations, only Japan and China have not raised their rates, although the Bank of Japan did effectively raise its long-term rate. As we can see though, many of the countries whose securities this fund has exposure to are not in the Group of 20 nations.

The fact that the DoubleLine Income Solutions Fund has such significant exposure to non-American issuers could be a very valuable thing for many investors. As I mentioned in a recent article , one of the biggest problems that American investors have right now is overexposure to the United States. This is understandable, but it is also problematic because an event that has an adverse impact on the United States could have an outsized impact on an investor's portfolio. This risk is particularly high for Americans because most of their income would also come from the United States, whether from a job or from Social Security. A significant economic impact could result in a massive portfolio loss and a loss of income. The only realistic way to protect against such a risk is to ensure proper international diversification of your portfolio. This fund could help an investor achieve such international diversification.

One strategy that is frequently employed by fixed-income closed-end funds is purchasing assets that have less than stellar credit ratings. In other words, these funds will frequently purchase speculative-grade securities ("junk bonds") because the high yields on these assets allow the fund to generate a high level of income that can be paid out to their shareholders. This fund is no exception to this rule, which we can clearly see by looking at the aggregate credit scores of the securities in the portfolio. Here they are:

CEF Connect

As we can clearly see, only 9.20% of the securities in the portfolio have credit ratings of BBB or above, which is the threshold for an investment-grade bond. The remainder of the securities in the fund are junk bonds or things with similar risks to junk bonds. That is something that could be very concerning to those investors who are risk-averse and concerned with capital preservation. This category would probably include a lot of retirees and others who are dependent on their portfolios to provide the income that they need to pay their bills or finance their lifestyles. Fortunately, though, the fund currently has 478 unique issuers represented in its portfolio and the largest holding only accounts for 1.32% of the fund's total assets. As such, any default should only have a very limited impact on the fund itself. Overall, the biggest risk here is interest rate risk, not default-related losses.

Performance Comparison

As we have already seen, the DoubleLine Income Solutions Fund has generally been outperforming the Bloomberg U.S. Aggregate Bond Index. However, this is perhaps not the best index to use as a point of comparison because it only tracks the performance of U.S. bonds and the DoubleLine Income Solutions Fund only has 41.75% invested in U.S. bonds. As such, it would be a good idea to compare the fund's performance to the Bloomberg Global Aggregate Float Adjusted Composite Index ( BNDW ). It may also be a good idea to compare this fund to the JP Morgan EMBI Global Core Index ( EMB ) due to the substantial number of emerging markets whose issuers are represented in this fund's holdings.

Here is the fund's performance against each of these indices over the past year:

{kind=link}

As we can clearly see, the DoubleLine Income Solutions Fund managed to deliver a positive price return over the past twelve months, which easily beats any of the indices. However, there is another factor that we should consider. One of the defining characteristics of bonds and other fixed-income investments is that a significant proportion of their investment return is delivered in the form of direct payments to their investors. In some cases, these payments can be sufficient to offset a price decline. For example, if an asset declines in price by 1% during a year but pays a 3% interest rate over that same year, then the investor will still have more money than they started with after one year. As such, we should compare the total return of the fund against the three indices. Here is the total return chart for the past year:

{kind=link}

We can certainly see that the Federal Reserve has been much more aggressive about raising interest rates than the central banks of many other nations in the world. The Bloomberg U.S. Aggregate Bond Index handed investors a far worse performance than any of the other assets. In fact, both the DoubleLine Income Solutions Fund and the Emerging Markets Bond Index delivered positive total returns over the period.

However, one year is not really a good point of comparison. After all, any fund manager will occasionally have periods in which they manage to beat an index for a short period of time. Let us compare this fund's performance to the indices over a longer period of time. Here is the ten-year total return chart for the DoubleLine Income Solutions Fund against each of the three indices:

{kind=link}

There is no real comparison here. We can easily see that the DoubleLine Income Solutions Fund and emerging markets bonds were really the only things in the bond market that were really worth investing in over the long term. This is the problem with the ultra-low interest rate policy that was pursued in the developed world. Emerging markets did not follow such a policy and their bonds generally had a much higher yield. Indeed, even today the emerging markets bond index has a 5.00% yield. The higher yield resulted in a much higher total return over time. The DoubleLine Income Solutions Fund has an even higher yield than any of the indices and so benefited from it even more.

As should always be mentioned, past performance is no guarantee of future results. However, the fact that this fund did manage to significantly outperform all of the bond indices during the past year speaks incredibly well for the skill of its management team. After all, the past year was the most challenging market for bonds in more than ten years. Thus, we can have some confidence that it will probably continue to outperform going forward.

Leverage

The DoubleLine Income Solutions Fund employs leverage as a method to increase the effective yield of its portfolio. I explained how this works in my last article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase bonds or other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund needs to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage since that would expose us to too much risk. I do not generally like to see a fund's leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the DoubleLine Income Solutions Fund has leveraged assets comprising 23.87% of its portfolio. This is quite a bit less than the leverage that the fund had the last time that we discussed it, which is a very good sign. This implies that the value of the fund's assets is increasing more rapidly than its leverage, or that it is taking advantage of recent capital gains to reduce its leverage. Either option reduces the risks that we have as investors with respect to this fund. Overall, it appears that this fund is continuing to maintain a very reasonable balance between risk and reward.

Distribution Analysis

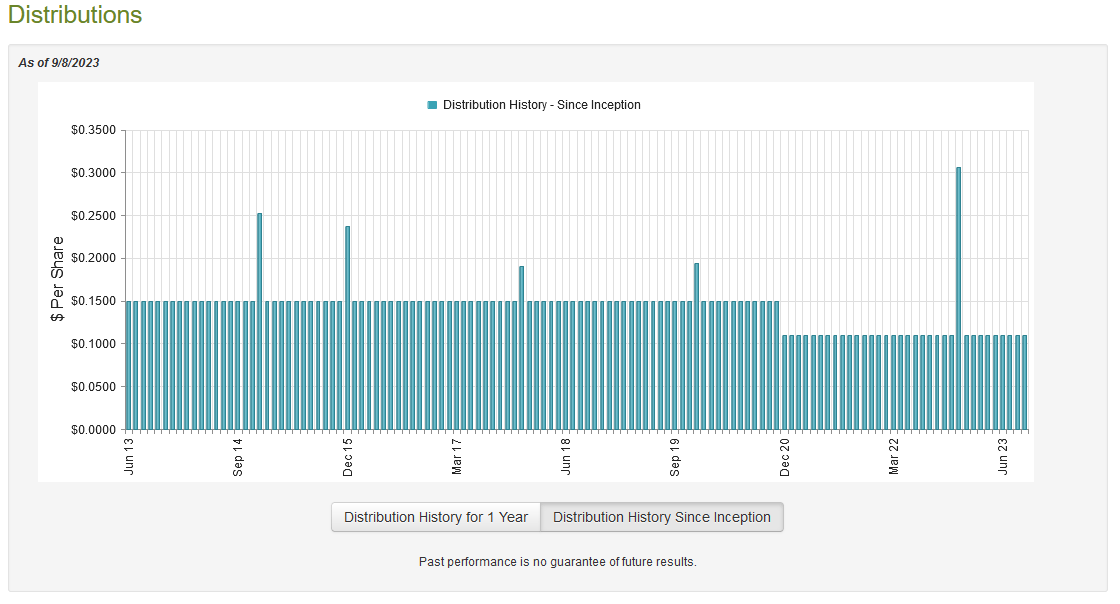

As mentioned earlier in this article, the primary objective of the DoubleLine Income Solutions Fund is to provide its investors with a very high level of current income. In order to achieve that goal, the fund invests in a portfolio of bonds, including emerging markets and junk bonds, that frequently have very high yields. The fund then applies a layer of leverage to boost the effective yield of its portfolio beyond that possessed by the bonds in it. As such, we might assume that the fund is able to boast a very high yield itself. That is indeed the case as the DoubleLine Income Solutions Fund pays a monthly distribution of $0.11 per share ($1.32 per share annually), which gives it a 10.95% yield at the current price. Unfortunately, the fund has not been particularly consistent with its distribution over the years, as it cut the payout back in December of 2020 and has kept it at a lower level since that time:

{kind=link}

With that said, this fund has definitely done a much better job of keeping its distribution consistent and reliable than most other fixed-income funds. As we have seen in numerous funds that are covered in this column, fixed-income funds have a tendency to vary their distribution significantly as interest rates vary. The fact that this one has only changed once during its life will increase its appeal to anyone who is seeking a safe and secure source of income to use to pay their bills or finance their lifestyles.

As is always the case though, it is important that we ensure that the fund can actually afford its distribution. The market is currently suggesting that it cannot, as most things with a double-digit yield are expected to have to cut their payouts at some point. In addition, the fund failed to cover its distribution during its most recent fiscal year, which I pointed out the last time that we discussed it. Thus, we do want to pay special attention to its finances.

Fortunately, we do have a fairly recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on March 31, 2023. This is a much newer report than the one that we had available to us the last time that we discussed this fund, which is nice as it should give us a good idea of whether or not the fund managed to turn its fortunes around during the rebound in the bond market around the start of this year.

During the six-month period, the DoubleLine Income Solutions Fund received $76,349,106 in interest and $1,094,798 in dividends from the assets in its portfolio. This gives the fund a total investment income of $77,443,904 during the period. The fund paid its expenses out of this amount, which left it with $57,906,823 available for shareholders. That was, unfortunately, not nearly enough to cover the $87,363,079 that the fund paid out in distributions. At first glance, this is likely to be very concerning since we typically like fixed-income funds to be able to cover their distributions entirely out of net investment income.

However, this fund does have other methods that can be employed to obtain the money that it needs to cover the distribution. For example, it might have been able to earn capital gains that can be paid out. The fund had mixed results at this during the period. It reported net realized losses of $125,488,623 but these were offset by $137,688,303 net unrealized gains. That was a reasonable performance, but it was still insufficient to cover the distribution. The fund's net assets declined by $13,970,093 after accounting for all inflows and outflows during the period, which included the issuance of $3,286,483 of new common stock. Unfortunately, it appears that this fund continued to fail to cover its distribution. This is a real concern as it is uncertain how much longer it can continue to bleed assets like this.

Valuation

As of September 7, 2023 (the most recent date for which data is available as of the time of writing), the DoubleLine Income Solutions Fund has a net asset value of $11.93 per share but the shares currently trade for $12.05 each. That gives the fund's shares a 1.01% premium on net asset value at the current price. That is perfectly in line with the 1.01% premium that the shares have averaged over the past month. However, the fund's average price over the past 52 weeks has been a 2.02% discount on net asset value. As such, the current price looks very expensive. In addition, I cannot justify paying a premium for any fund that appears unable to cover its distribution. It would be advisable to wait until the price comes down before buying shares.

Conclusion

In conclusion, there are definitely some things to like about the DoubleLine Income Solutions Fund. In particular, the fund's substantial allocation to emerging markets and foreign bonds is nice from a diversification perspective. This is particularly true for American investors who tend to have an outsized financial exposure to the United States. In addition, the fund has a solid performance history as it has beaten comparable index funds over both the short-term and the long-term. Unfortunately, it appears unable to sustain its distribution and its shares are trading at a price that is above their intrinsic value. I might be able to justify buying this fund at a discount, as then a distribution cut would be priced in. However, I cannot justify paying a premium for this fund.

For further details see:

DSL: Nice International Exposure, But This CEF Is Overpriced