DSU - DSU: A CEF Opportunity For Income Investors To Diversify Their Fixed Income Portfolios

2023-10-02 05:06:04 ET

Summary

- BlackRock Debt Strategies Fund is a compelling choice for investors looking to diversify their fixed income portfolios.

- Rising rate environments favor low duration debt, and the Fed has signaled that rates may stay "higher for longer." This is a good headwind for bank loans.

- DSU's active management strategy allows for flexibility and responsiveness to markets and macroeconomic changes.

- Counterpoints include high fees, widening discounts, and variable payment structures.

Editor's note: Seeking Alpha is proud to welcome John Bowman as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Introduction

In the ongoing search for portfolio diversification and yield, we as investors may often overlook closed-end funds due to the industry's generally high fees, more opaque nature, and history of rogue funds misusing leverage. Sifting through the plurality of CEFs can be daunting, so many investors forgo it in their research for income opportunities.

The closed-end fund, BlackRock Debt Strategies Fund (DSU), stands out as a compelling choice for investors aiming to diversify their traditional fixed income portfolios. DSU fund primarily invests in bank loans, which have unique properties when compared to traditional fixed income products like corporate bonds.

Brief Overview

At a glance:

- Price: $10.26

- Distribution Rate: 10.64%

- Premium/Discount: (4.55)%

- Dividend Per Share: $0.9341

- Beta: 0.35

- Volatility (1Y): 11.05

- 30-Day Trading Volume: 1,287,948.06

- Market Cap: $478,221,801

Description: As per BlackRock -

BlackRock Debt Strategies Fund, Inc.'s (the 'Fund') primary investment objective is to provide current income by investing primarily in a diversified portfolio of US companies' debt instruments, including corporate loans, which are rated in the lower rating categories of the established rating services (BBB or lower by S&P's or Baa or lower by Moody's) or unrated debt instruments, which are in the judgment of the investment adviser of equivalent quality. The Fund's secondary objective is to provide capital appreciation. Corporate loans include senior and subordinated corporate loans, both secured and unsecured. The Fund may invest directly in such securities or synthetically through the use of derivatives.

DSU uses an opportunistic allocation strategy, allocating to bank loans that managers believe are mispriced by the market. The portfolio is managed by Mitchell Garfin, CFA; David Delbos, and Carly Wilson over at BlackRock. Wilson is an interesting manager in particular because she sits on the board of directors of the Loan Syndications & Trading Association.

With net assets at the $500 million mark, the fund is not small but doesn't make the list of top 100 CEFs by size by about 75 million. Don't be turned off by the high ER, an astounding 1.33%, because the managers justify it with excess returns via the use of leverage. The fund is leveraged at 22% of assets, but this may change over the course of the year, typically never exceeding 25%.

DSU distributes dividends monthly, with ex-dividend dates around the middle of the month, and payout dates toward the end of the month. Currently, the distribution rate is at 10.64% and has a yield to worst of 12.62%.

The fund trades at a discount of 4.55%, although it typically can get down further and often trades at an 8% discount to NAV.

Bank Loans As An Asset

If you're familiar with bank loans, skip down to the next bolded section.

Senior bank loans, also known as leveraged loans, are private debt instruments that hold a senior position in a company's capital structure. They offer investors higher yields with relatively low correlation to other fixed income assets. The interest rates on senior bank loans are typically variable, tied to a benchmark rate, providing a built-in hedge against rising interest rates. However, it's crucial for investors to consider the credit risk and liquidity concerns associated with senior bank loans as part of their overall investment strategy. Later in this analysis, we will take a look at the credit quality of the bank loans held by DSU.

Primary differences to corporate bonds include:

-

Higher Ranking in Capital Structure: In the event of a bankruptcy, the average recovery rate from 1987 to 2020 for senior secured loans was about 77%, whereas for senior unsecured bonds, it was only 48%. Investing in corporate debt carries risks, and credit risk is one of the most important risks for investors.

-

Lower Interest Rate and Duration Risk: The duration of bank loans is generally lower than that of corporate bonds, 0.64 years compared to 6.3 years respectively. This lessens the effect changes in interest rates will have on the value of the loans for resale in secondary markets, shielding investors from losses due to rising rates.

- Diversification and Risk Management: Allocating to bank loans can enhance diversification in traditional fixed income portfolios. The correlation between the Leveraged Loan Index and the U.S. Aggregate Bond Index was just 0.2, highlighting the potential for bank loans to offer meaningful portfolio diversification.

-

Comparable Yields with Lower Volatility: Despite their lower risk profile, bank loans have offered comparable yields to high-yield bonds in the last year and may continue to do so if we are to believe the Fed's "higher for longer" hawkish (big-"ish" here) turn.

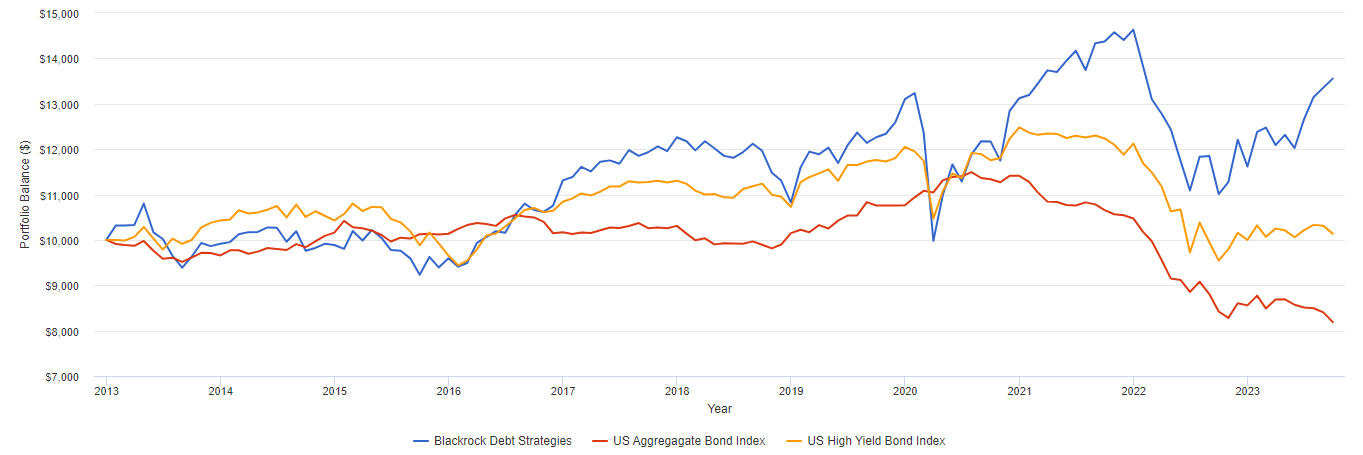

Even in a low-rate decade, bank loans (DSU, Blue) have outperformed on a risk-adjusted basis compared to both aggregate bonds (Red) and junk bonds (Yellow). Note: returns shown here are inflation-adjusted returns, assuming all dividends are re-invested at the time of distribution.

{kind=link}

Active Management

One of the most distinguishing features of DSU is its active management strategy. BlackRock's managers are not afraid of taking risks with this portfolio, but they have historically paid off well.

Compared to passive funds like BKLN, DSU's active management can add significant value. Passive funds, by design, lack the flexibility and responsiveness that DSU's management team brings to the table. The ability to assess and react to market changes enables DSU to optimize its portfolio continuously for the best possible return and risk balance. During the summer of 2020, DSU was able to access incredibly cheap leverage as rates went to zero . They used that leverage very effectively and loaded up on corporate debt at the lower end of the credit spectrum, primarily B rated bank loans.

DSU Credit Quality Breakdown (BlackRock, Inc.)

While the bank loan sector (and really most to all income securities) took a hit through 2022, DSU was able to temper some of it with their access to floating rate debt that commands a premium rate above the average rate due to lower creditworthiness.

Dynamic Credit Risk Reduction

The ability to screen for idiosyncratic credit risks and adjust to the changing market trends has proven to be a game-changer in the actively managed debt world. DSU is able to adjust the portfolio across multiple assets, including high-yield junk bonds, equities (preferred shares, etc.), and CLOs, as needed to react appropriately to macroeconomic events like rate changes and institutional defaults.

In the last ten years, we've seen a mostly steady rise in the total market for bank loans. As the market expands, DSU has been able to find more opportunities to hold quality debt from lower-credit borrowers. As more and more loans hit the market and more and more analysts are replaced by algorithms, there are bound to be more missed opportunities for clever fund managers to find.

Loans and Leases in Bank Credit, All Commercial Banks (Federal Reserve Bank of St. Louis)

{kind=link}

Debt being issued near par in this current environment may be as attractive as it will get for some time, as the Fed has made it clear that if we get more rate hikes, there may only be one or two more at the most. That may not hold out to be true, which is why old debt is becoming less and less attractive to hold on to. Passive indexes can't tactically position themselves or opportunistically screen for quality loans, leaving the managers only able to react to changing macroeconomic environments, never able to position their funds for headwinds.

Macroeconomic Opportunity

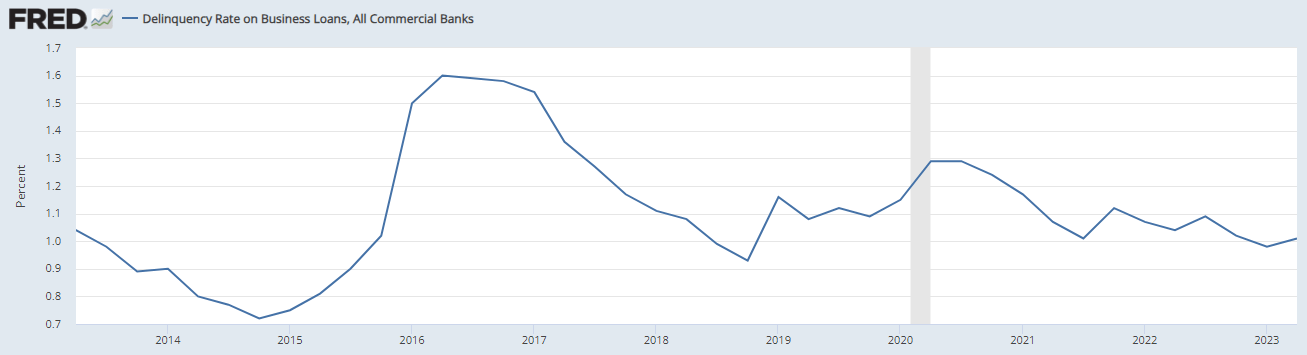

As rates climb, we should expect the market to contract. What we're seeing is that the market is able to withstand some pain, and may be able to tolerate much more than folks thought. When we compare this alongside the delinquency rate for business loans, we don't see the same pain that we should expect.

Delinquency Rate on Business Loans, All Commercial Banks (Federal Reserve Bank of St. Louis)

{kind=link}

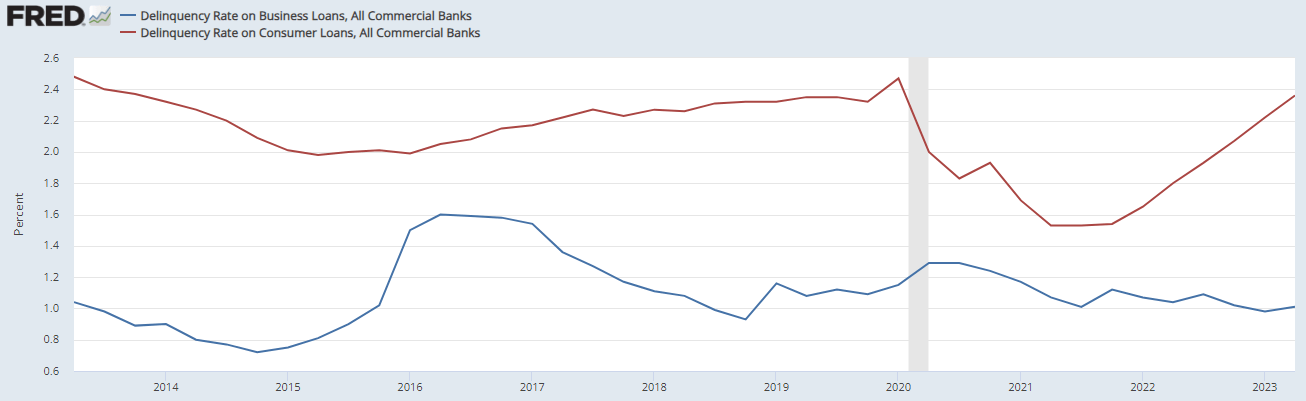

So where is that pain being felt? There may really be something to this "greedflation" narrative being sold in popular media . Consumers are not faring as well as businesses are. Credit card delinquencies are trending up quickly, despite a leveling out of business loans and commercial bank loans in general.

Delinquency Rate of Business Loans (Blue) vs. Consumer Loans (Red) (Federal Reserve Bank of St. Louis)

{kind=link}

Believing the Fed's current narrative means that we can expect these trends to continue for the next few years, hopefully leveling out as the hiking stops and rates are held. This unevenness in default rates gives me confidence in the coffers of businesses to pay back these loans moving forward, which also spells an opportunity for risk on income investors at large.

Counterpoints

It is important to highlight the downsides to any fund that I do positive analysis for. Here are several of the potential issues investors may have with DSU.

-

CEF market prices have no guarantee of returning to NAV, and there is no guarantee that any discount, currently discounted by 4.91%, will not widen after the purchase of shares. The 52-wk average discount is 9.37%.

-

Lower credit ratings present higher risk than investment grade bonds, and including leverage, DSU uses 22% leverage as of the time of writing; this may be above some income investor's risk tolerance and can lead to steep declines in periods of market turbulence (see above chart in 2020).

-

Floating interest rates create variability in payouts, which could pose a risk to investors requiring a more stable income stream.

-

The management fee comes out to 1.9% of net assets, requiring DSU to outperform the passive index by that amount just to break even. This is a risk as well and can potentially drag returns.

Conclusion

For investors looking to include bank loans in their income portfolios as a means of diversification, DSU appears as a good contender. In comparison to passively managed funds like BKLN, DSU's active management strategy enables it to adjust to market dynamics, pursue higher returns, and manage risk more effectively, which has historically justified its heavy fees. Investors should think about DSU as an alternative to a high-yield bond or passive index of bank loans.

For further details see:

DSU: A CEF Opportunity For Income Investors To Diversify Their Fixed Income Portfolios