DSU - DSU: Stable Assets Despite Recent Market Action In The Shares

2023-12-07 11:53:49 ET

Summary

- BlackRock Debt Strategies Fund Inc offers a high level of income with a current distribution yield of 11.32%.

- The DSU closed-end fund has delivered a strong total return of 7.77% since the last article was published, outperforming major stock and bond market indices.

- The fund's portfolio consists mainly of floating-rate debt securities, which may not benefit as much from price appreciation in a declining interest rate environment.

- The market might be very wrong about the direction of interest rates in 2024, so it is advisable to hedge your bets.

- The fund appears to be covering its distribution and is trading at a discount.

The BlackRock Debt Strategies Fund Inc ( DSU ) is a closed-end fund, or CEF, that can be employed by investors who are seeking to earn a very high level of income from the assets that are contained in their portfolios. The fund’s current distribution yield of 11.32% stands as a testament to its success at providing investors with a very high level of income. This yield is very much in line with the yields currently being offered by other junk bond and corporate loan funds, and it is certainly not a sign that the market expects that the fund will need to slash the distribution soon. After all, while it is certainly true that a few years ago a double-digit yield was a cause for concern, that is no longer the case considering that interest rates are much higher today than they were only two years ago.

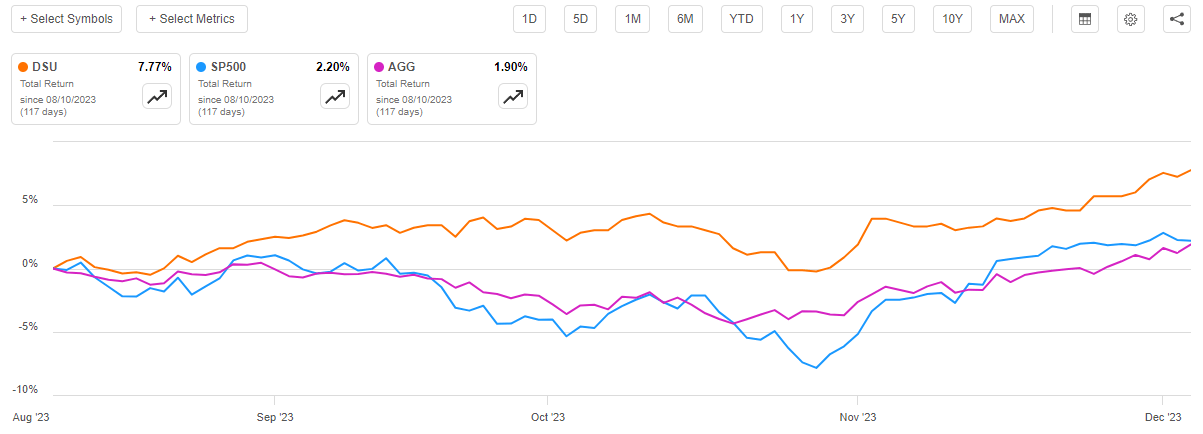

As regular readers may recall, we last discussed the BlackRock Debt Strategies Fund back in the middle of August. While only four months have passed since that time, it almost feels like much longer due to how much the mood in the market has changed. At the time that the previous article was published, investors were beginning to accept the Federal Reserve’s “higher for longer” mantra and were generally bidding down asset prices and allowing yields to rise. That is the exact opposite of what we have today, as financial conditions have been loosening for the past month or so and asset prices have been rising. This certainly shows up in the recent performance of this fund, which has delivered a 7.77% total return since the date that my prior article was published. This is a much better total return than either the S&P 500 Index ( SP500 ) or the Bloomberg U.S. Aggregate Bond Index ( AGG ) has delivered over the same period:

{kind=link}

As I have pointed out in previous articles, though, there could be some signs that the market is being wildly optimistic about the prospect of central bank rate cuts. In fact, as we will see in this article, there exists the possibility that the market’s current move to push rates down actually causes the Federal Reserve to hike again. As such, it would be prudent to maintain exposure to assets that will benefit from both rising and falling interest rates. The BlackRock Debt Strategies Fund invests in both fixed-rate and floating-rate debt, so it could be one way to achieve this goal.

As we have just seen, the fund has delivered a very attractive total return that is far better than that of either of the major stock or bond market indices over the past four months. As such, it may be advisable to revisit this fund and attempt to determine if it still has room to run or if the fund’s strong recent rally has been overdone.

About The Fund

According to the fund’s webpage , the BlackRock Debt Strategies Fund has the primary objective of providing its investors with a high level of current income. This is not particularly surprising for a debt fund, as most of them have a similar objective. After all, debt securities are by their very nature income vehicles. As I explained in my previous article on this fund:

An investor purchases a bond at face value, receives a steady stream of coupon payments over the life of the bond, and receives face value back when the bond is redeemed at maturity. As such, the only return that the bond provides over its lifetime is the coupon payment made to the bondholder. There are no net capital gains due to the fact that bonds have no inherent link to the growth and prosperity of the issuing entity. A company certainly does not increase the payments that it makes to its creditors just because its profits go up and a government will not just pay its bondholders extra money because of an increase in tax revenue.

As such, bonds or debt securities have no net capital gains over their lifetimes. However, it is possible for an investor or a fund to earn some capital gains by trading a bond or similar security prior to maturity. This comes from the fact that bond prices increase when interest rates go down and vice versa. Unfortunately, this fund will not be able to benefit from that to the same degree as many other debt funds. In order to understand why, let us take a look at how the website describes the fund’s strategy:

BlackRock Debt Strategies Fund, Inc.’s primary investment objective is to provide current income by investing primarily in a diversified portfolio of US companies’ debt instruments, including corporate loans, which are rated in the lower rating categories of the established rating services (BBB or lower by S&P’s or Baa or lower by Moody’s) or unrated debt instruments, which are in the judgment of the investment adviser of equivalent quality. The Fund’s secondary objective is to provide capital appreciation. Corporate loans include senior and subordinated corporate loans, both secured and unsecured. The Fund may invest directly in such securities or synthetically through the use of derivatives.

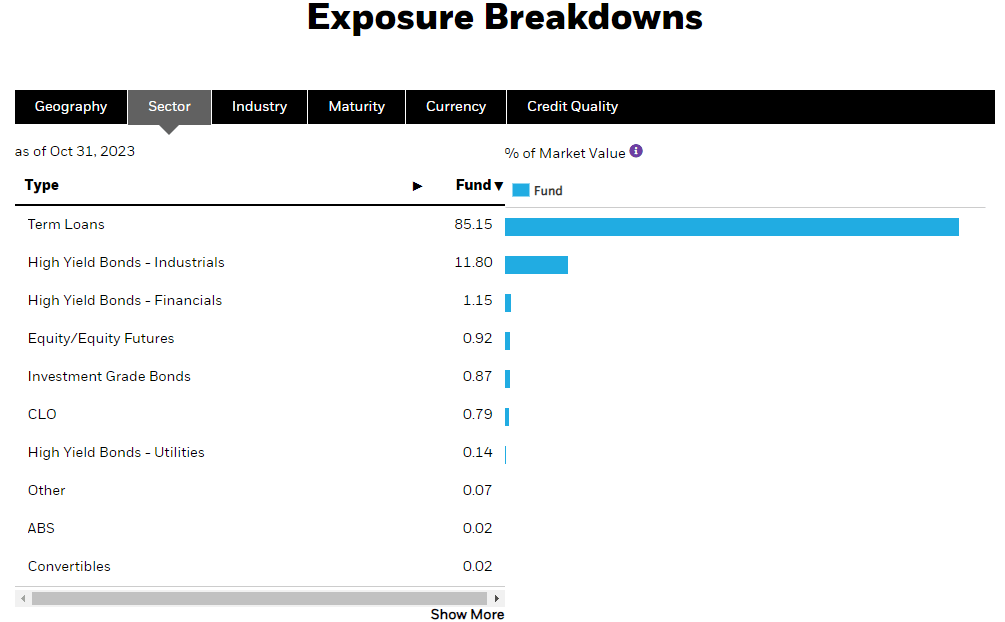

We notice how the fund’s description specifically states that it may invest in corporate loans. These securities are generally floating-rate loans that have their interest rates based on fluctuations in LIBOR, the ten-year U.S. Treasury (US10Y), or some other benchmark. As of the time of writing, 85.15% of the fund’s assets are invested in these securities:

{kind=link}

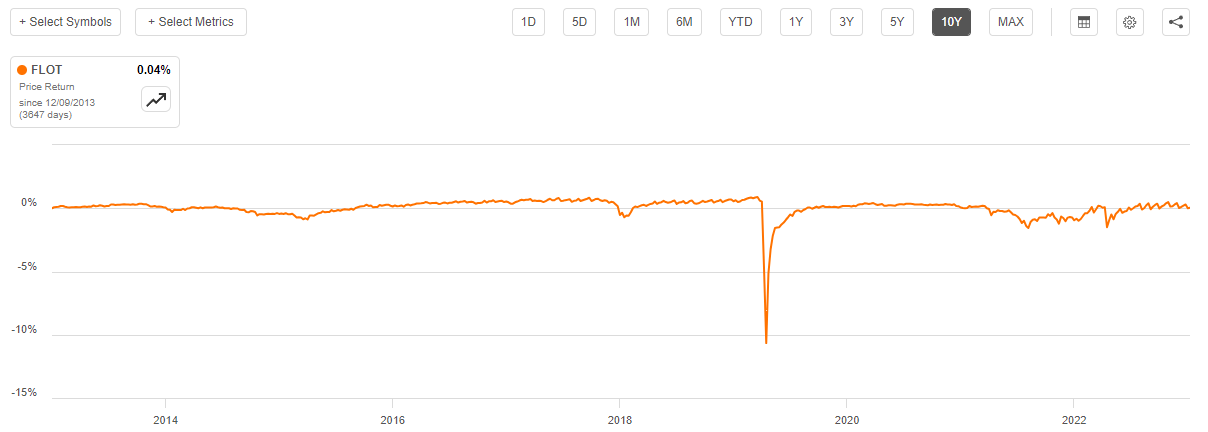

This is the thing that prevents this fund from fully benefiting from the price appreciation of debt securities that accompanies rising interest rates. As I pointed out in a previous article , floating-rate securities tend to maintain relatively level prices regardless of changes in interest rates. We can see this by looking at the BBG US Floating Rate Notes 5 Yrs. Or Less Index ( FLOT ). Here is the ten-year chart for this index:

{kind=link}

As we can see, neither the massive interest rate cuts of 2020 nor the interest rate hikes of 2022 and 2023 had any real impact on the price of the securities in this index. This is because, unlike traditional bonds, these securities always deliver an interest rate that is competitive with brand-new securities with otherwise identical characteristics. This will carry over to this fund’s portfolio. The floating-rate term loans held by the fund will probably not change very much if long-term interest rates continue to decline. As such, the fund’s net asset value will not appreciate as much as it would if the portfolio were entirely invested in junk bonds or other interest-rate-sensitive securities.

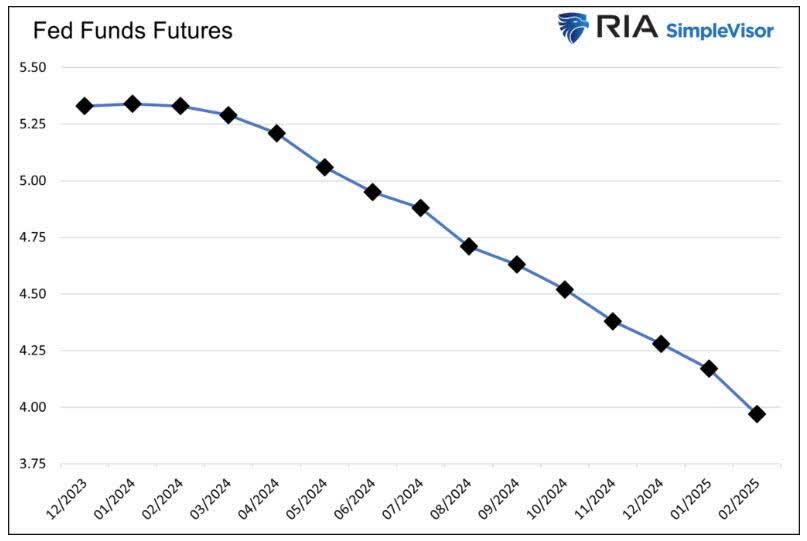

With that said, there is no guarantee that interest rates will continue to decline. As I have pointed out in a few recent articles, the market is currently anticipating that the Federal Reserve will start cutting the federal funds rate in March 2024 and will reduce rates by around 125 basis points by the end of the year.

{kind=link}

In anticipation of this, investors have been aggressively buying long-term bonds, bidding up the price and forcing yields down. This has greatly loosened financial conditions, which is one of the most important metrics tracked by the Federal Reserve:

Zero Hedge/Data from Bloomberg

According to Simon White , Bloomberg’s macro strategist, this financial loosening is the exact opposite of what the Federal Reserve was attempting to accomplish with its rate hikes. He states that there is virtually no chance that the Federal Reserve will cut rates by anywhere close to the degree that the market is currently anticipating unless a severe recession occurs by March. In fact, Mr. White outright predicts that a rate hike is more likely than a cut given the market’s loosening efforts. When we consider that the Federal Government may use a variety of stimulative measures to avoid a recession during an election year, we can clearly see that there is still sufficient question with respect to the direction of interest rates that it probably smart to have both securities that will benefit from rising and falling interest rates. This fund certainly fulfills one of those objectives with the high allocation to term loans, although its junk bond allocation is too low to achieve the benefits from falling interest rates that could be desired. As such, it might make sense to hold this fund alongside a pure junk bond fund or a fund like the Ares Dynamic Credit Allocation Fund ( ARDC ) that will derive more benefits from a falling rate environment.

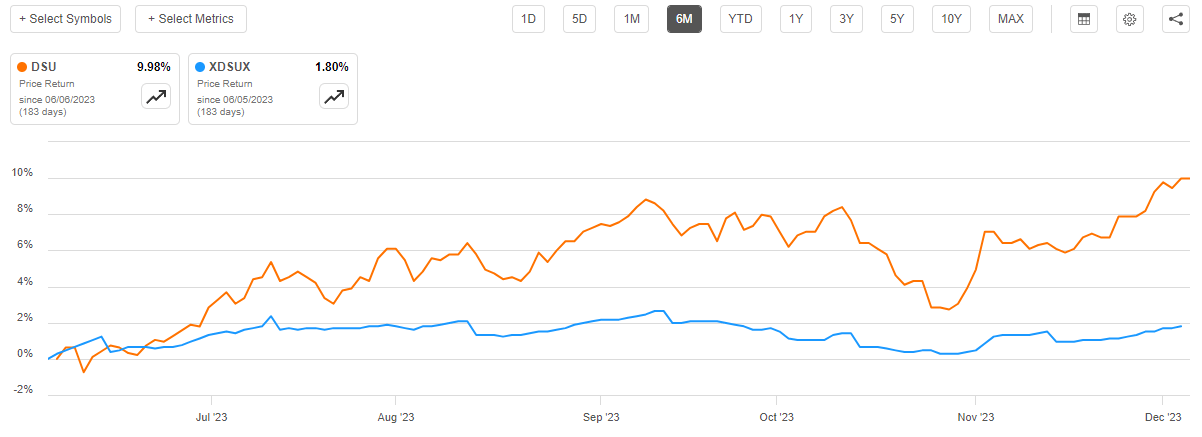

In the introduction, we saw that the market was bidding up shares of the BlackRock Debt Strategies Fund just like it is doing for ordinary bond funds. When we consider this fund’s high exposure to term loans and other floating-rate assets, this would seem to not make sense. In fact, the fund’s share price has been substantially outperforming its portfolio over the past six months. As we can see here, the fund’s shares are up 9.98% over the past six months. However, the fund’s net asset value per share is only up 1.80%:

{kind=link}

In short, the market appears to be far too exuberant here as it has been bidding up the shares of a fund that will not really benefit from falling interest rates. Indeed, this fund’s portfolio is largely interest-rate neutral right now. Its income will decline if rates go down, but the fixed-rate bond allocation is too low for it to earn capital gains sufficient to make up the difference. While it is possible that the fund could alter its portfolio towards junk bonds if those securities look more attractive, that is pure speculation and is not in line with how the fund claims to be invested today.

Leverage

As is the case with most debt-focused closed-end funds, the BlackRock Debt Strategies Fund employs leverage as a method of boosting the effective yield of the assets in its portfolio. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to buy various debt securities. As long as the yield that the fund receives from the purchased securities is higher than the interest rate that it pays on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio.

As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. However, this strategy does not work as well today with borrowing rates at 6% as when rates were basically 0% two years ago. This is because the difference between the interest rate that the fund pays on the borrowed money and the yield that it receives from the purchased securities is much smaller than it once was.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally want a fund’s leverage to be under a third as a percentage of its assets for this reason.

As of the time of writing, the BlackRock Debt Strategies Fund has leveraged assets comprising 21.44% of its portfolio. This is substantially less than the 24.61% leverage that the fund had the last time that we discussed it, which is a very good sign. It is, however, a bit surprising because the fund’s net asset value per share is actually down slightly since the last time that we discussed it. This suggests that the fund has taken some steps to actively reduce its debt and thus reduce its risk. Either way, the fund does have a reasonable balance between risk and reward with its current leverage so we should not need to worry about it very much.

Distribution Analysis

As mentioned earlier in this article, the BlackRock Debt Strategies Fund has the primary objective of providing its investors with a very high level of current income. In pursuance of this objective, the fund purchases a variety of both floating-rate and fixed-rate debt securities issued by companies with below-investment-grade credit ratings. As these are essentially junk debt securities, they tend to have much higher yields than typical investment-grade bonds or indeed many other things in the market. The fund collects all the money that it receives from these securities, then it borrows money to buy more income-producing securities. The leverage essentially boosts the yield that it receives based on its net assets. The fund combines this income with any capital gains that it manages to realize by exploiting changes in interest rates and bond prices. It then pays out all of the money that it manages to earn from these business operations to its shareholders, net of its own expenses.

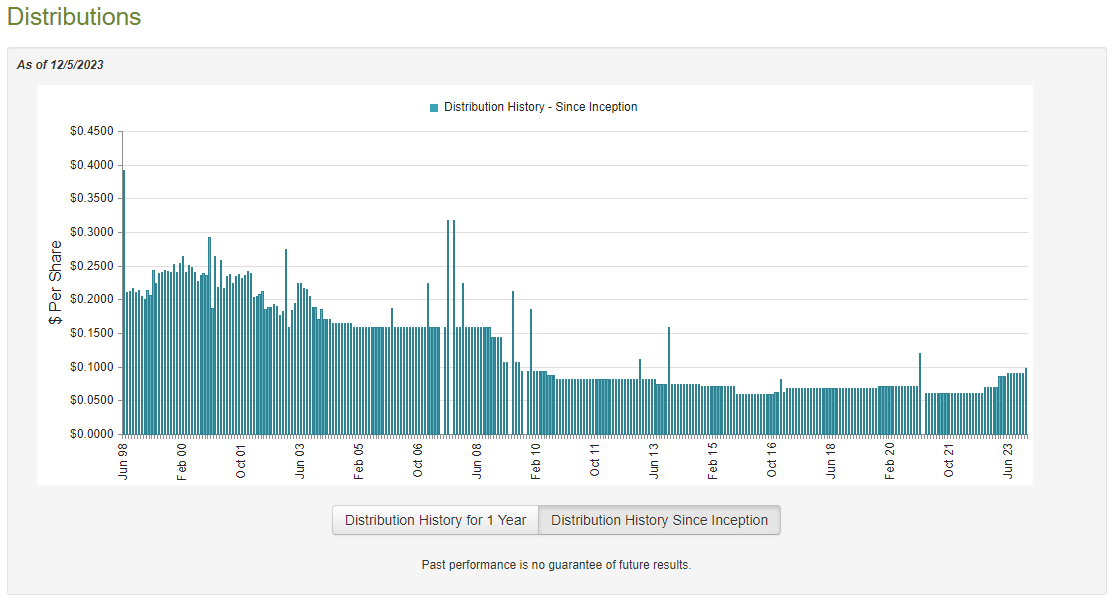

When we consider the nature of the securities that this fund invests in, and the beneficial effects of the fund’s leverage, we might assume that this business model would give the fund’s shares a very high distribution yield. This is certainly the case, as the BlackRock Debt Strategies Fund pays a monthly distribution of $0.0987 per share ($1.1844 per share annually), which gives it an 11.32% yield at the current price. That is in line with comparable hybrid bond funds right now so there is nothing to complain about with respect to the fund’s current yield. However, some investors might be turned off with the fact that the fund has altered its distribution numerous times over its history:

{kind=link}

This is certainly going to reduce the appeal of this fund in the eyes of those investors who are looking for a safe and consistent source of income to use to pay their bills or finance their lifestyles. However, it is not out of line with other debt funds, especially those that invest in floating-rate securities. This is simply because interest rates have a significant impact on the ability of these funds to generate income. When interest rates decline, the net investment income of this fund declines and it has to cut its distribution in order to avoid destroying its net asset value.

However, as I have pointed out numerous times, a fund’s history is not necessarily the most important thing for brand-new investors to consider. This is because anyone who purchases the fund today will receive it as it is right now and will not be adversely affected by events that have occurred in the past. As such, the most important thing for our purposes right now is to determine how well it can sustain its current distribution.

Fortunately, we have a relatively recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2023. That means that this is a more recent report than the one that we had the last time that we discussed this fund, which is nice to see. After all, the first half of this year was an interesting one as the market was widely expecting that the Federal Reserve would cut interest rates during the second half of 2023. As a result, it was bidding up asset prices and driving long-term interest rates down. While this belief was proven to be incorrect, as the current belief very well might be, there still could have been the opportunity for this fund to earn some capital gains by selling appreciated bonds in a very energetic market. This report will give us a good idea of how well it managed to take advantage of that potential opportunity.

During the six-month period, the BlackRock Debt Strategies Fund received $107,384 in dividends and $27,684,364 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, the fund had a total investment income of $28,054,503 during the period. It paid its expenses out of this amount, which left it with $22,283,433 available for shareholders. This was, unfortunately, not enough to cover the $22,953,248 that the fund paid out in distributions during the period, but it obviously did manage to get very close. At first glance, this might be concerning because we would normally like a fixed-income fund to completely cover its distribution out of net investment income and while this one did manage to get close; it did not quite make it.

However, the fund does have other methods through which it can obtain the money that is needed to obtain the money that it needs to cover the distribution. As mentioned earlier, the fund might have been able to obtain some money by selling bonds into the strong market during the period and realizing capital gains. However, the fund actually reported mixed results in this task. During the six-month period, it reported net realized losses of $6,422,360 but these were more than offset by $20,276,402 net unrealized gains. Overall, the fund’s net assets increased by $13,184,227 over the period after accounting for all inflows and outflows. Thus, the fund did technically manage to fully cover its distributions during the period, although it had to rely on unrealized capital gains to accomplish the task.

As a general rule, we do not want a fund to rely on unrealized capital gains to cover a distribution. This is because unrealized capital gains can disappear during a market correction. This fund did manage to get pretty close to full coverage simply with net investment income though, and as we can see here, the fund’s net asset value per share increased by 0.37% since July 1:

{kind=link}

This suggests that the fund has managed to fully cover its distribution since the date that this report was released. This happened despite the fact that the fund has been increasing its distribution over the past few months. As such, we can probably conclude that the fund can continue to keep its distribution at the current level as long as its net investment income remains relatively stable. That will probably be the case until the Federal Reserve cuts interest rates.

Valuation

As of December 5, 2023 (the most recent date for which data is currently available), the BlackRock Debt Strategies Fund has a net asset value of $10.77 per share but the shares currently trade for $10.46 each. This gives the fund’s shares a 2.88% discount on net asset value at the current price. That is a very small discount that is a bit worse than the 3.17% discount that the shares have had on average over the past month. It might be possible to get a better price by waiting a bit, but a discount is still an acceptable entry price for most funds.

Conclusion

In conclusion, the BlackRock Debt Strategies Fund probably does not deserve the market volatility that it has been seeing with its share price. The fund’s assets consist mostly of floating-rate securities that do not see their price vary much with interest rates. With that said, this fund does look reasonably decent as a way to hedge exposure to interest rates. Despite the market’s current belief, the Federal Reserve will probably not cut interest rates by 125 basis points next year and traditional bonds could very easily get punished when that happens. This fund should hold up much better though because it is mostly invested in floating-rate securities.

For further details see:

DSU: Stable Assets Despite Recent Market Action In The Shares