DSDVF - DSV A/S: Best-In-Class Player With Significant M&A Optionality

2023-08-01 08:12:32 ET

Summary

- DSV is a Danish freight forwarder with a strong track record of growth and high total shareholder returns.

- The company reported strong Q2 results, with upside potential to gross profit targets and an increased EBIT guidance.

- DSV has a history of successful M&A activity. We believe the market is currently underappreciating DSV's M&A optionality. The main potential target in the near term could be Schenker.

Drawn by a compelling structural outlook combined with an attractive valuation, we recently published our note with a Buy rating on Kuehne+Nagel , the world's leading freight forwarder. We now present our note on DSV ( DSDVF ), a Danish freight forwarder, and one of Europe's highest-quality businesses with an excellent track record of acquisitive growth and outstanding total shareholder returns.

Introduction to DSV

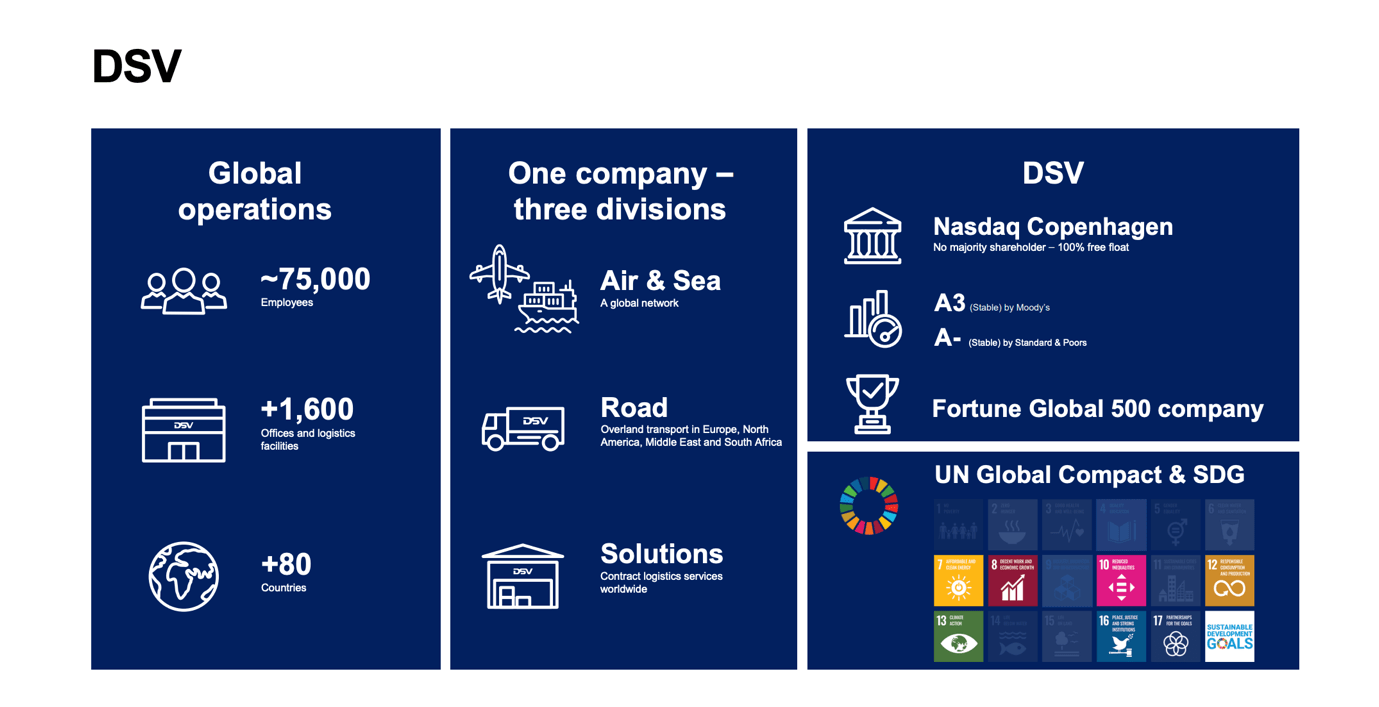

DSV is the world's 3rd largest freight forwarder by revenue, after Kuehne+Nagel and DHL Logistics , with a market share of around 4%. It consists of 3 divisions: Air & Sea; Road i.e., Overland Transportation; and Solutions i.e., Contract Logistics. The company employs 75k people across 1800+ offices and logistics facilities in more than 80 countries. It has a diversified and profitable client base of small and medium enterprises and leverages robust local teams combined with an efficient central system. DSV is listed on Nasdaq Copenhagen and has a market capitalization of DKK295 billion, or ca. $47 billion.

For a detailed explanation of the freight forwarding business, we would suggest our readers check out our article on Kuehne+Nagel .

{kind=link}

Q2 Results

DSV printed strong Q2 numbers. Gross profits declined 20% YoY in line with consensus expectations, and EBIT came in at DKK4705 million, also in line with company-compiled consensus. Yields fared better than expectations while volumes were slightly worse. Management is now talking about the upside to gross profit targets per unit, likely around DKK9000 in air and DKK4500 in sea vs. DKK8000+ and DKK4000+ respectively. The EBIT guidance was raised from DKK16-18 billion to DKK17-18.5. billion as a result of the strong operating performance. A share buyback program of DKK4 billion was announced, making the total buyback amount DKK12 billion or >4% of the current market capitalization. We have a positive view of the results.

Value Creation Through M&A

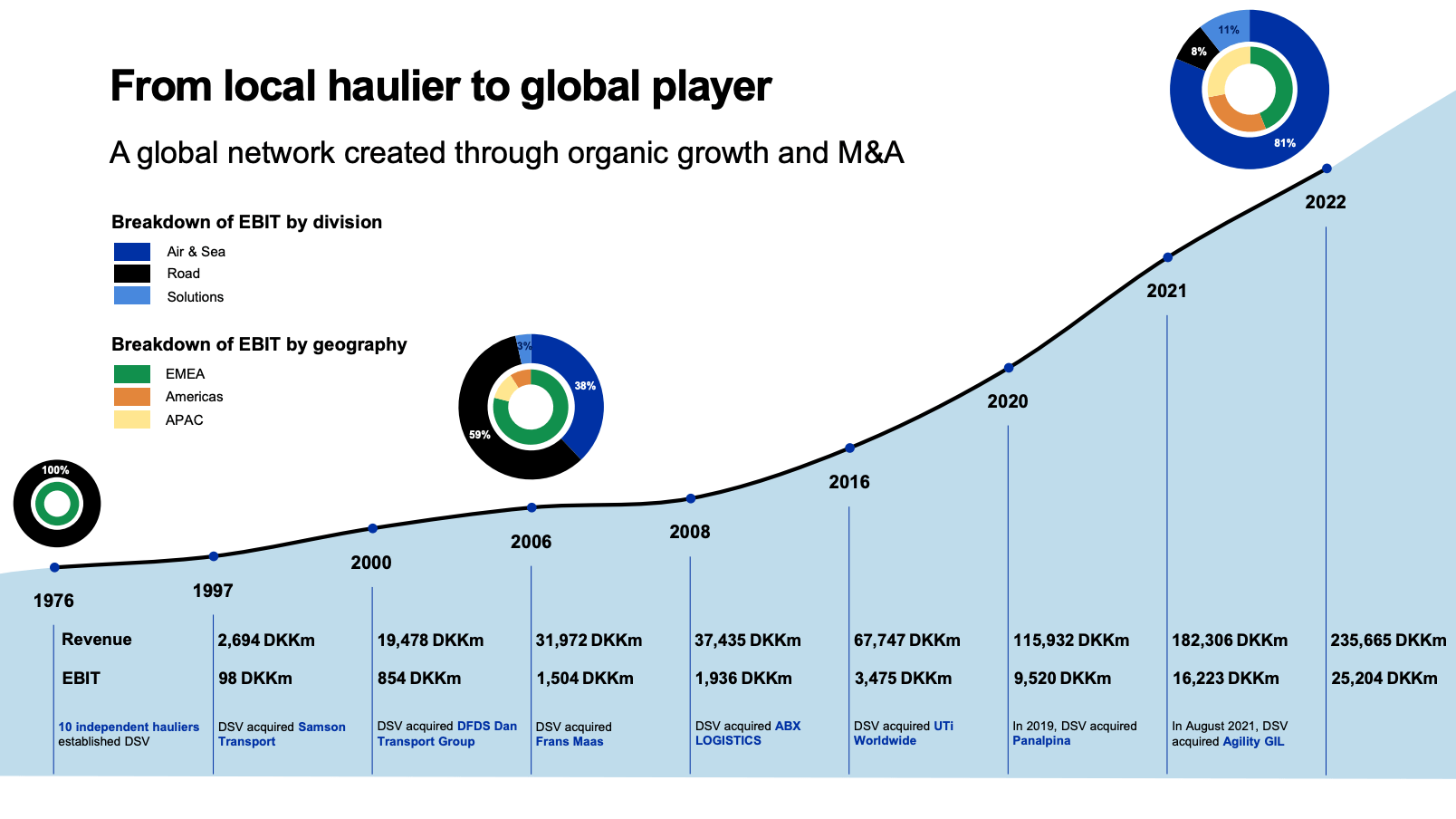

DSV has one of the most impressive long-term track records of growth and excellent capital allocation in Europe. Freight forwarding is a labor-intensive capital-light industry with effectively low barriers to entry, allowing hundreds of thousands or even millions of operators, often focused on a single vertical, to compete with little but an internet connection and a contact book. However, a wider set of capabilities and skills as well as significant scale is required to address higher volumes and higher complexity.

DSV has consolidated sea, air, and road freight forwarders as well as contract logistics networks in Europe and globally, achieving exceptionally high returns on capital, and delivering high teens to low twenties CAGR returns. It has consistently acquired underperforming asset bases, slashed costs, and re-leveraged excess cash flow through share buybacks. Large synergies and sustainable earnings accretion have been the norm. DSV's scale effectuates volume leverage, lower fixed costs per unit, and hence a pricing advantage, as well as a superior service.

The most notable acquisitions include Panalpina for $4.7 billion, GIL for $4.2 billion, and UTi for $1.4 billion. Acquisitions have been largely funded with equity and have been highly accretive with the targets acquired at high single digits PE multiples while DSV's stock was issued at 25x PE+.

There have been continuous rumors about the acquisition of the 4th largest freight forwarder: Schenker , a division of state-owned German rail operator Deutsche Bahn. DSV would potentially compete with Maersk as well as private equity funds for this asset. We believe DSV is better positioned as it can achieve relatively more synergies and is hence the most logical buyer. As per media reports, Schenker is worth up to €20 billion , effectively half the value of DSV. We have a positive view of the deal and view it as a valuable option. However, we believe any deal needs to be closed before the federal elections campaign in 2024, given the political sensitivity related to cost-cutting at a newly privatized company.

{kind=link}

Investment Case And Valuation

DSV's multiple has materially derated to the lower end of its historical range as freight rates and profitability have normalized. On a standalone basis, we see DSV as fairly valued, however, our investment case relies on the market's underappreciation of the multiple inorganic growth opportunities available to DSV. There is a significant runway for further inorganic market consolidation and value creation. In this context, we believe M&A option value should be reflected in the equity. Major M&A activity announcements should serve as a catalyst in combination with the realization of synergies and a resumption of market share gains. We are particularly paying close attention to the sale of Schenker. The acquisition of Schenker for an assumed value of €20 billion could add nearly 50% to DSV's earnings and meaningfully decrease forward multiples.

Moreover, as referred to in our note on Kuehne+Nagel, there is a wider market concern about the implications of declining global trade and nearshoring for freight forwarders. We would like to reiterate our positive structural outlook, highlighting that demand should depend mostly on complexity rather than other factors.

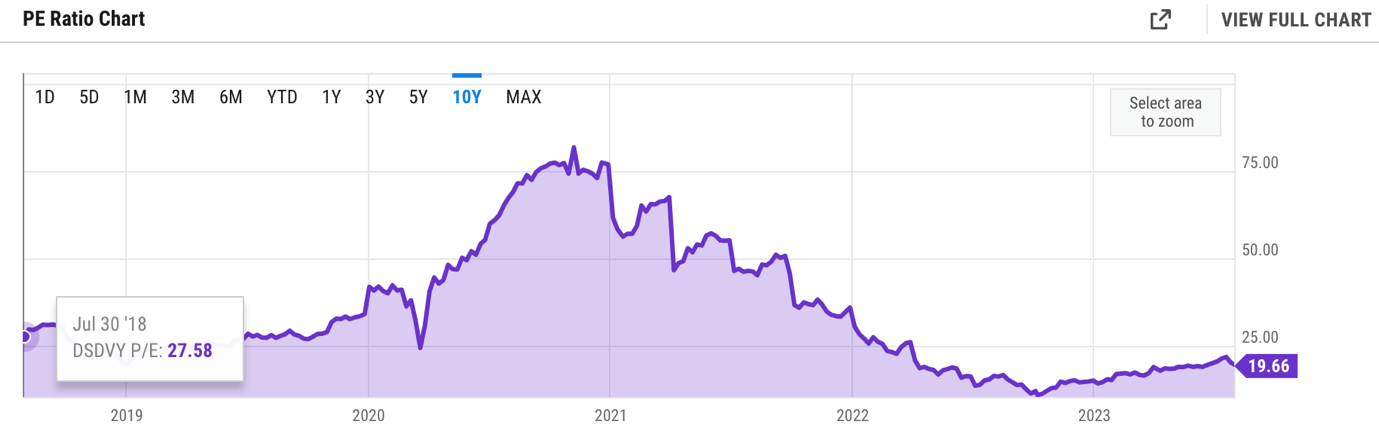

We forecast DKK165 billion of revenue, DKK17.5 billion of EBIT, and DKK12.5 billion of reported net profit in FY2024e, on the back of ca. 2% revenue decline vs our 2023 estimate, and consistent margins. This implies a 23.6x forward PE multiple. The buyback of >4% shares puts the multiple at around 22.5x forward EPS. This is lower than historical levels; as per YCharts PE multiples pre-pandemic have been consistently above 25x. As previously noted, our valuation fails to take into account the M&A option value. We do not make any assumptions about M&A deals in our model. We value DSV at 25x EPS2024e, at DKK1508/share or $223/share, implying 11% upside. We would like to emphasize that we see this as the lower end of the valuation range rather than our precise target price.

{kind=link}

Risks

Risks include but are not limited to a macroeconomic downturn, a decline in global trade, a decline in volumes, a decline in gross profit yields, a decline in freight rates, higher competition for deals from both industrial and financial buyers leading to increasing M&A target multiples, failure to integrate acquired companies, impairments, customer churn post deals, disintermediation through technological advancements, entry of lateral competitors such as carriers into the forwarding market, labor force unionization, etc.

Conclusion

Based on the robust structural outlook for freight forwarders, DSV's high-quality business model, strong track record, underappreciated M&A option value, robust operating performance, and a reasonable upside, we suggest building a small long position on DSV shares. In case of any major pullback, DSV would make for an excellent buy.

For further details see:

DSV A/S: Best-In-Class Player With Significant M&A Optionality