DSDVF - DSV A/S: Growth Through M&A

2023-10-16 12:47:34 ET

Summary

- DSV A/S is a Denmark-based transportation and logistics company that offers air and sea freight services, road freight services, and contract logistics services.

- The logistics market is experiencing a normalization of rates, impacting DSV A/S's revenues and earnings. However, the company has been able to offset some of the decline through share repurchases.

- DSV A/S is overvalued compared to the industry, but its history of successful M&A and value returned to shareholders through dividends and share repurchases make it an attractive investment.

I recently covered GXO Logistics (GXO), which has further deepened my interest in logistics providers as airplanes play a vital role in logistics and logistics play a vital role in manufacturing of aerospace products. In this report, I will be covering DSV A/S (DSDVF, DSDVY) and assess any upside potential for the stock.

What Does DSV A/S Do?

DSV A/S, formerly DSV Panalpina A/S, is a Denmark-based company engaged in the transportation and logistics services. The Company's operations are divided into three business segments: The Air and Sea service, which provides air and sea freight services across the globe; The Road, that provides road freight services across Europe, North America, and South Africa and The Solutions segment, which offers contract logistics services, including warehousing and inventory management, across the globe. So, we see that DSV offers its services in various geographical markets, and it provides a rather close solution set from warehousing to road, air and sea freight services.

{kind=link}

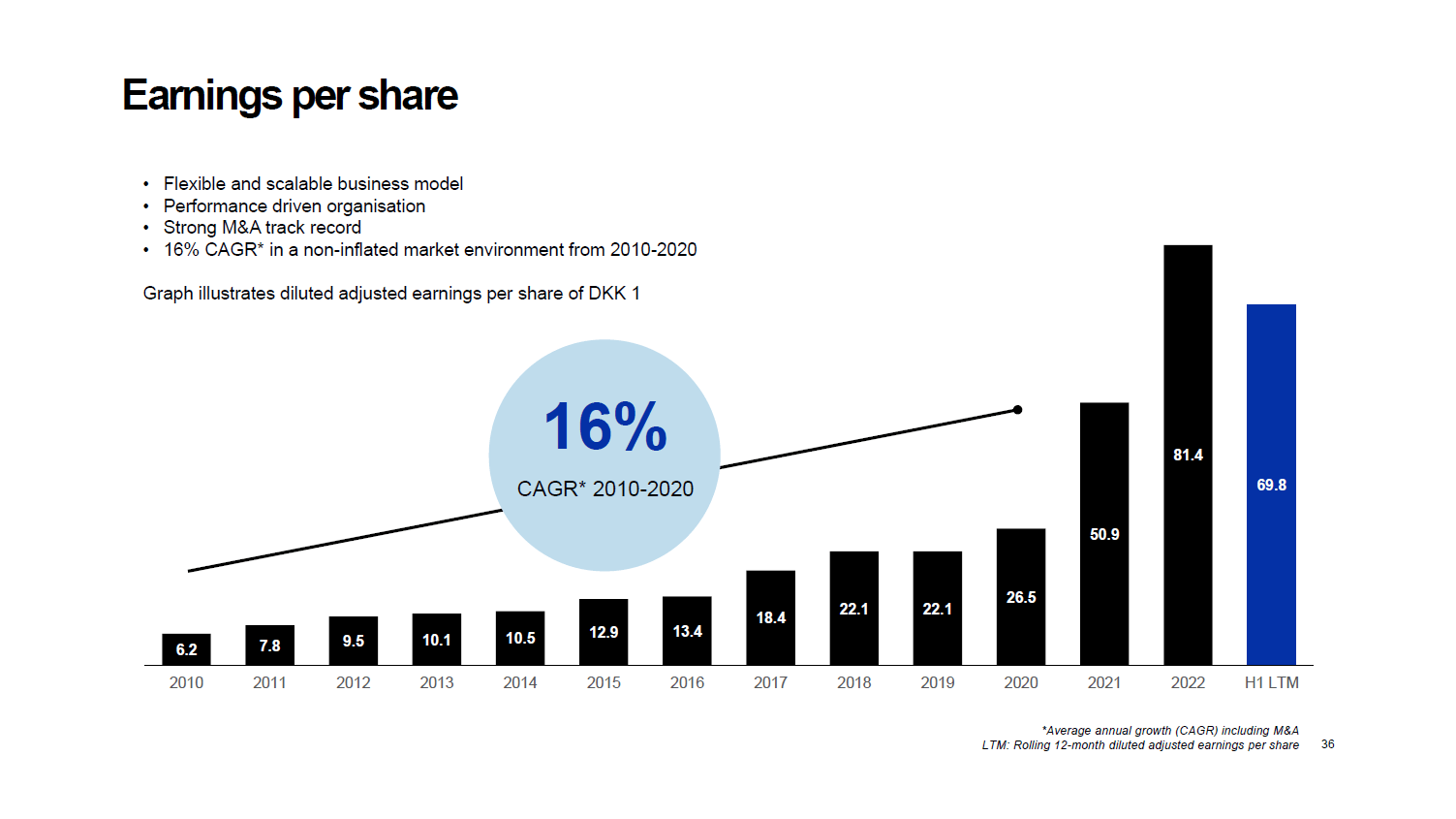

Earnings per share for DSV A/S boast a 16% CAGR, which has been largely enabled by a successful M&A track record, which turned the company from a local carrier to a global logistics player.

Normalization In The Logistics Market

The logistics market is going through a round of normalization of rates and that is also visible in the H1 2023 results. I don't want to provide a full analysis of the most recent results announced months ago, but there are some things to highlight. Revenues have declined 36.5% with a 34.8% decline in adjusted EBIT. However, driven by share repurchases the decline in earnings per share was only 3%. Air & Sea results were impacted by a 21% reduction in air freight volumes as well as a 9% reduction in sea freight volumes and a weakening in yields as freight capacity constraints are easing significantly. To some extent, the market is now seeing a normalization and many airlines that were quick to establish freight divisions during the pandemic are now going to face a normalized market that likely provides a challenging background to turn a profit for these airlines.

Road revenues declined by 4.5% but saw a reduction of "just" 2.8% in EBIT, while the solutions segment including warehousing solutions saw a nearly 5% decline in revenues but was hit by a 23.4% lower EBIT due to inflation and capacity expansion.

For DSV A/S, there is no extremely positive scenario when looking at the year-over-year changes, but we should just keep in mind that rates are normalizing across air and freight shipping and excluding the solutions business, we did see operating margins improve. So, DSV can't show anything close to growth but that is just the reality of the industry now. What DSV, however, is doing is using the value created during high growth years to repurchase share which offsets a significant portion of the decline in earnings per share.

Is DSV A/S Stock A Buy?

{kind=link}

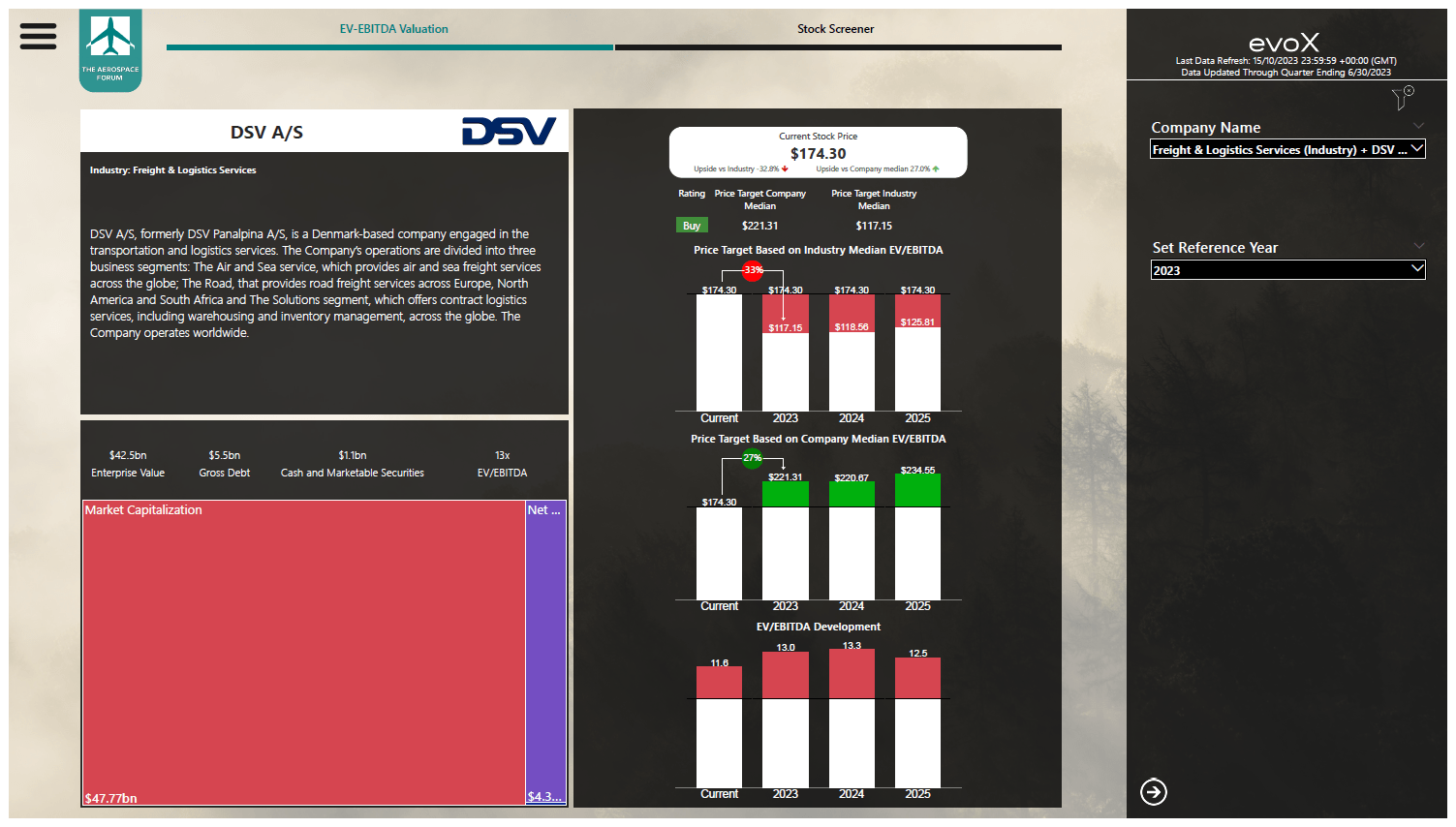

After filling in the balance sheet data and forward projections for DSV A/S into the evoX Financial Analytics tool available to subscribers of The Aerospace Forum, we get a bit of a mixed picture. Against the EV/EBITDA for the industry, the company is significantly overvalued. However, in case of DSV A/S, there seems to be a good reason for that. The company has a history of share repurchases and dividends that warrant a premium against the industry median. Moreover, the company's M&A path is what allows it to grow significantly, and the company has had quite a good track record acquiring and integrating businesses. That M&A is important to the business growth also shows in the price targets for the 2023-2025 period in which the year-over-year upside based on current projections is rather low which shows that continued business acquisition is what really boosts upside for the stock.

Conclusion: DSV A/S Returning Value To Shareholders Through Strong M&A Strategy

The current market is a tricky one for freight forwards as volumes are decreasing and unit freight rates are normalizing while inflation is still having an impact on the cost side of the warehousing business. However, DSV A/S seems to be a somewhat compelling play as the company has a good track record of growing its business through acquisitions and returning value to shareholders in the form of dividends and share repurchases.

For further details see:

DSV A/S: Growth Through M&A