DTM - DT Midstream: Higher Dividends Are Very Likely Coming Soon (Rating Upgrade)

Summary

- DT Midstream continues to prove itself a desirable option in the midstream industry by executing its strategy well.

- That said, investors are not forgoing growth with their guidance for 2023 pointing to a significant year-on-year increase versus 2022.

- Management is clearly flagging that higher dividends are coming during 2023 as they scale accordingly with their earnings.

- Their solid financial position can also absorb their bolt-on Millennium Pipeline acquisition without creating new risks.

- Since they have performed strongly, I now believe that upgrading my hold rating to a buy rating is appropriate.

Introduction

It was almost exactly one year ago that I reviewed the newly listed DT Midstream (DTM) that as my previous article discussed, had years of dividend growth ahead whereby their 5% yield could turn into a very high 10%+ yield one day. Despite this positive outlook, they were unproven but thankfully after the last year, they are seemingly executing their strategy well and excitingly, it now seems higher dividends are very likely coming soon.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

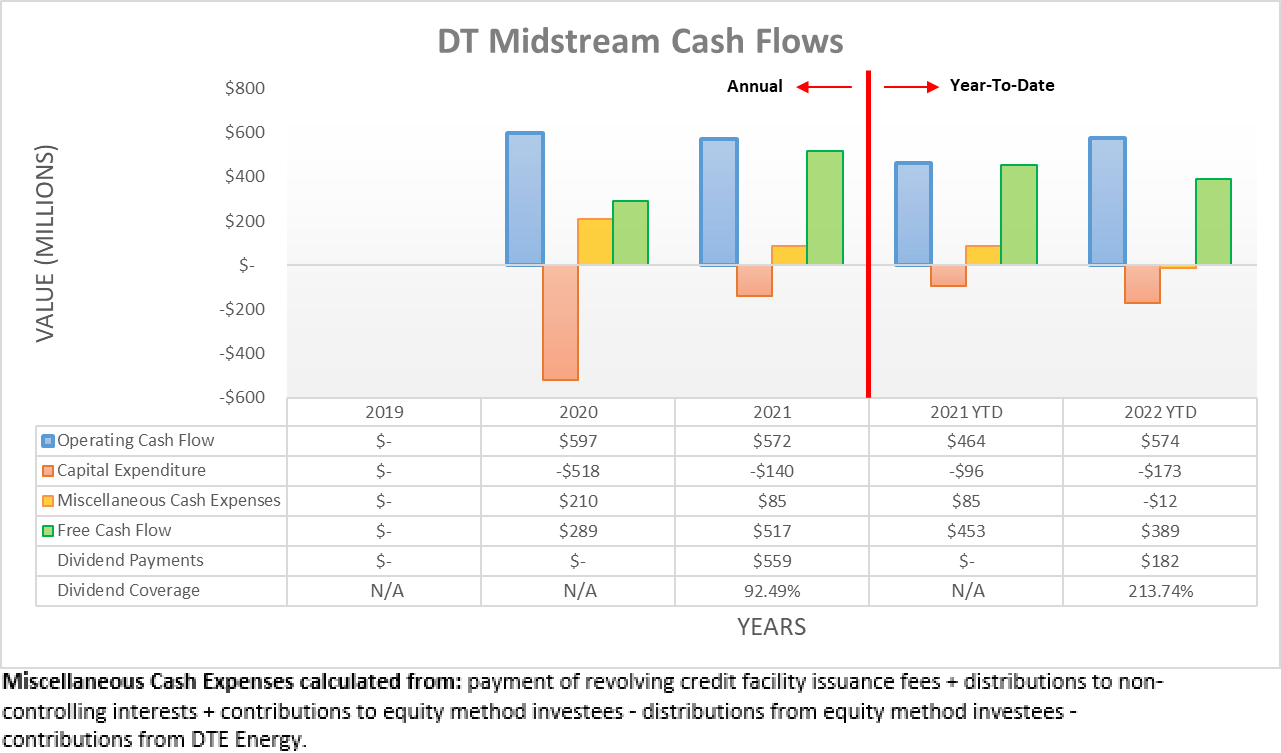

On the surface, their cash performance during the first nine months of 2022 was far stronger than seen during 2021. Most notably, their operating cash flow of $574m is actually $2m higher than their full-year result of $572m during 2021, despite being a one-quarter shorter length of time. Likewise, if comparing against the exact same period of time during 2021 that saw a result of $464m, their latest result is a very impressive nearly 24% higher year-on-year.

{kind=link}

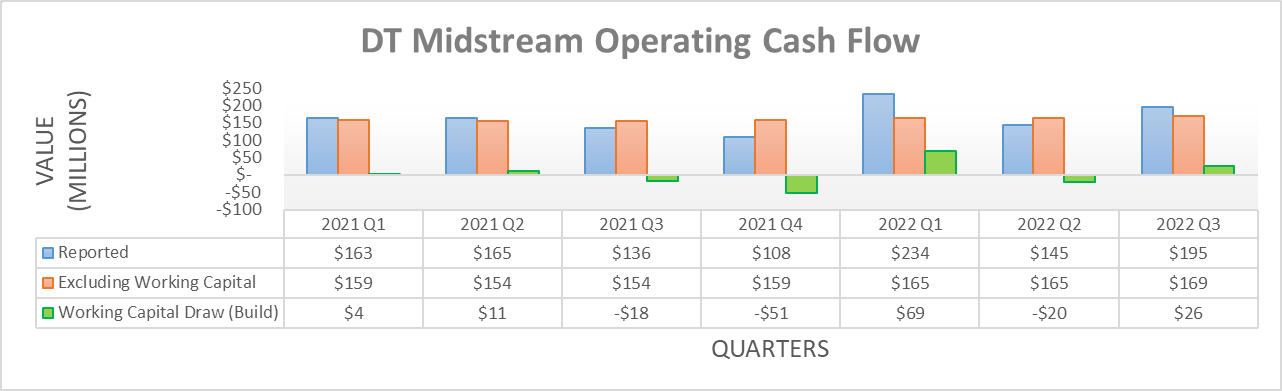

Whilst their reported operating cash flow is very positive, underneath the surface, the comparison is still good but not quite to the same extent. If viewed quarterly, it is easier to see their working capital movements that unlike during the first nine months of 2021, played a sizeable role during the first nine months of 2022. In the case of the former, they only saw an immaterial build of $3m, whereas in the case of the latter, they saw a sizeable draw of $75m, which aided their reported results. If excluding these working capital movements, their underlying results were $467m and $499m respectively, thereby still representing a modest increase of almost 7% year-on-year. When everything is said and done, the more important aspect right now is their outlook for the year ahead.

DT Midstream November 2022 Investor Presentation

Whilst they were already forecasting a strong performance during 2023, this was increased even further with management now forecasting adjusted EBITDA of $885m at the midpoint. If this comes to pass, it represents an increase of slightly more than 8% year-on-year versus their forecast of $817.5m at the midpoint for 2021. In theory, this should broadly translate into their operating cash flow given their positive correlation, plus just as importantly, higher dividends given their approach to their shareholder returns, as per the commentary from management included below.

"So our --you're right, and we're going to continue with our guidance that we will continue to grow our dividend in line. We believe that's part of the total shareholder return and investment thesis for us. We'll grow it in line with our cash flows."

-DT Midstream Q3 2022 Conference Call.

Since they tether their dividends to their earnings growth, in my eyes this effectively means that higher dividends are very likely coming soon, which means they are executing their strategy well, as hoped when conducting the previous analysis one year ago. The only remaining downside right now is the temporary lack of clarity on their capital expenditure going forwards into 2023 and beyond, as per the commentary from management included below.

"We look forward to providing a complete update of our 2023 guidance on our year-end call, which will include a refreshed view for our base business and our long-term growth capital plan."

-DT Midstream Q3 2022 Conference Call (previously linked) .

Whilst technically unknown and thereby leaving their dividend coverage uncertain, the remainder of their third quarter of 2022 conference call did not make it sound like dramatically higher capital expenditure would be forthcoming in 2023 and beyond. Furthermore, as they have consistently generated free cash flow during 2020, 2021 and now 2022, it stands to reason this will continue into 2023 and beyond.

{kind=link}

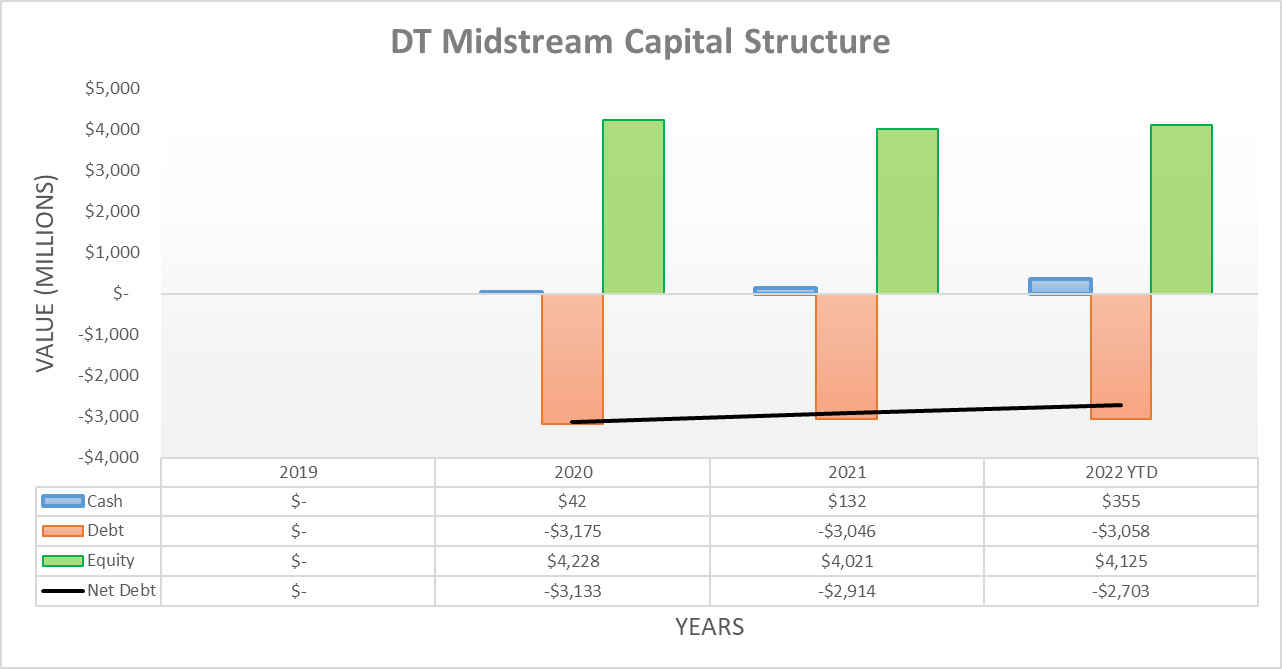

Thanks to their consistent and steady free cash flow, their net debt continued trending lower, as was the case throughout 2021 and certainly bodes well for higher dividends. This pushed their net debt down to $2.703b following the third quarter of 2022 versus $2.914b at the end of 2021 and $3.133b at the end of 2020. Although, the recently ended fourth quarter of 2022 results will see this spike higher on the back of their bolt-on Millennium Pipeline acquisition for $552m, which is funded via cash on hand and debt from their credit facility. At least their net debt should resume its downward trajectory during 2023 and beyond, despite pushing it back around its highest point ever at circa $3.1b to $3.2b, depending upon their accompanying free cash flow during the fourth quarter.

{kind=link}

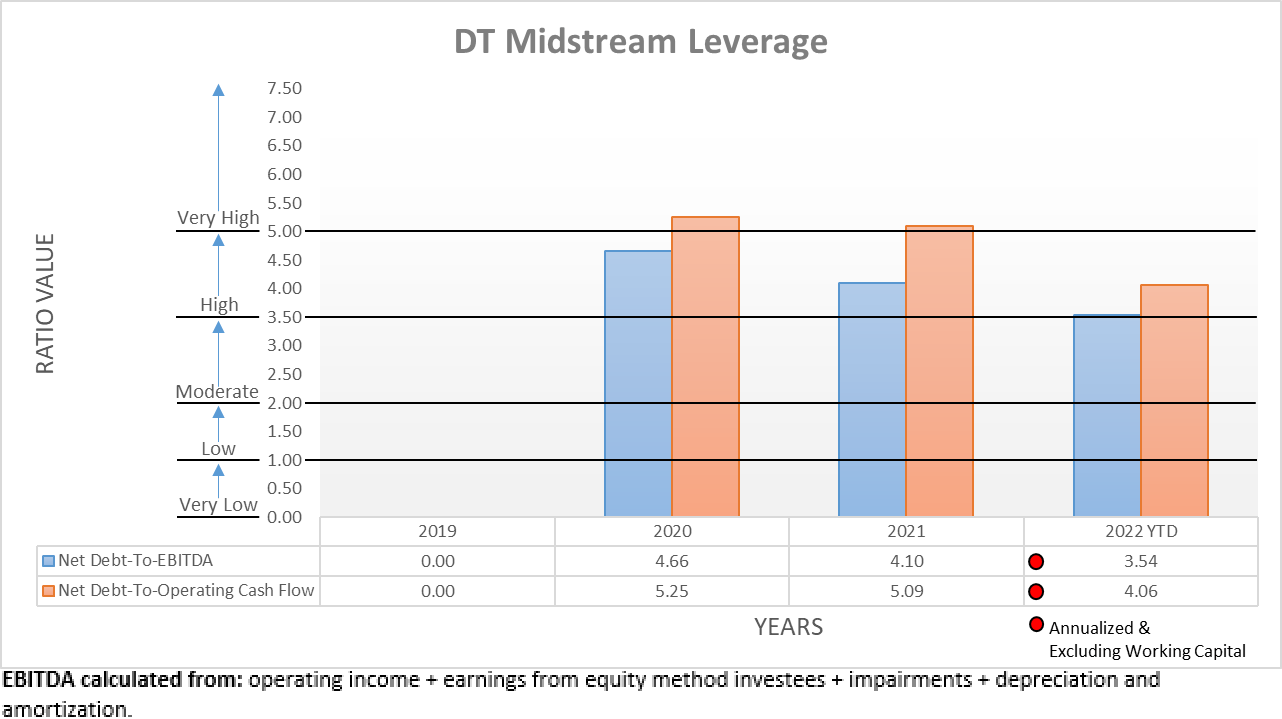

Unlike many in the midstream industry, they are not plagued with troublesome leverage with their net debt-to-EBITDA falling to 3.54 following the third quarter of 2022, thereby down from 4.10 at the end of 2021. Concurrently, their net debt-to-operating cash flow also saw an even larger decrease to 4.06 versus 5.09 across these same two points in time. Whilst both of their results are still technically within the high territory, they sit within the bottom half of the range of 3.51 to 5.00, especially in the case of their net debt-to-EBITDA, thereby making for a solid base going forwards.

That said, their upcoming Millennium Pipeline acquisition will obviously see these spike higher in conjunction with their net debt. Thankfully, as their financial performance is stronger than back during 2020 when their net debt was last around circa $3.1b to $3.2b, their leverage should not be pushed as high. Plus, as 2023 progresses and their net debt most likely resumes its downward trajectory alongside even stronger financial performance, their leverage should see more sizeable decreases that in turn, helps support higher dividends.

{kind=link}

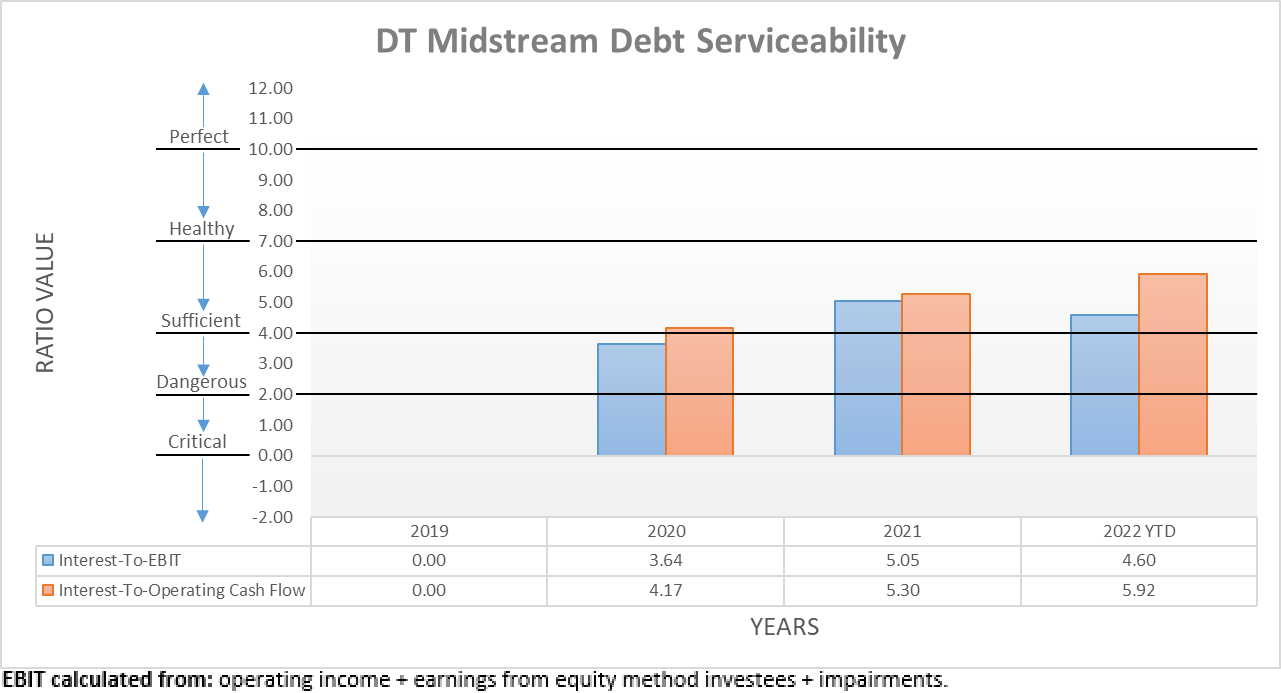

Following their lower leverage, it would have normally been expected to see their debt serviceability following in tandem. Although, this was not necessarily forthcoming as their interest expense compared against their EBIT sees coverage of 4.60 following the third quarter of 2022, which is actually down versus their previous result of 5.05 at the end of 2021. Whilst the accompanying comparison against their operating cash flow sees a result of 5.92 versus 5.30 across these respective points in time, it was aided by their aforementioned working capital draw.

This increase was driven by their interest expense climbing slightly more than 22% year-on-year during the first nine months of 2022 to $99m versus $81m, obviously on the back of the rapidly tightening monetary policy. At least on both accounts, their interest coverage is still healthy and thus poses no hindrance to higher dividends, especially because they should improve further into 2023. As for their Millennium Pipeline acquisition, the debt-funded portion will obviously add to their interest expense but at the same time, it will also add to their financial performance, therefore broadly netting out.

{kind=link}

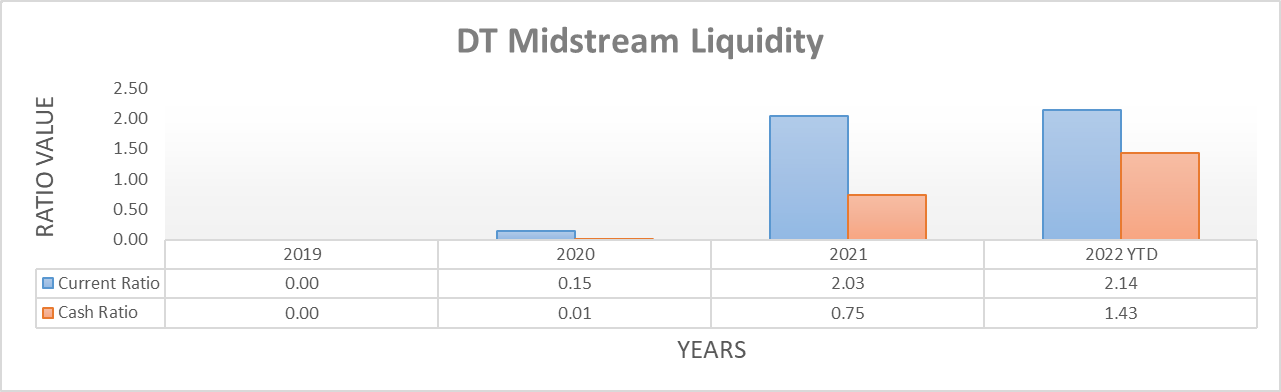

Not only did their free cash flow facilitate deleveraging, it also improved their already strong liquidity to now see a current ratio of 2.14 following the third quarter of 2022. Most notably, they now sport a cash ratio of 1.43, which is almost twice its previous result of 0.75 following the end of 2021, which was already strong. That said, funding the cash portion of their Millennium Pipeline acquisition will see these drop lower following the fourth quarter of 2022.

When the third quarter of 2022 ended, their cash balance was $355m, whilst their credit facility held $750m of availability that did not mature until June 2026, thereby making for a combined total of $1.105b and thus essentially double what is required to fund this acquisition. It currently remains unknown exactly how they split the cost between these two pools of funding but regardless, a lower cash balance will equal lower current and cash ratios. Thankfully, they are starting from a strong base that can easily support such a move, especially as their free cash flow in 2023 stands to help replenish their cash balance, plus they do not see any other debt maturities until as late as June 2028.

DT Midstream November 2022 Investor Presentation

Conclusion

There are very few things that are certain in life, especially when it comes to investing but in this situation, it seems that higher dividends are very likely coming soon given their guidance for both shareholder returns and their earnings in 2023. Since they are seemingly executing their strategy well as hoped one year ago when conducting the previous analysis, I now believe that upgrading my hold rating to a buy rating is appropriate, as previously promised

Notes: Unless specified otherwise, all figures in this article were taken from DT Midstream's SEC Filings , all calculated figures were performed by the author.

For further details see:

DT Midstream: Higher Dividends Are Very Likely Coming Soon (Rating Upgrade)