DTM - DT Midstream: New Growth Projects And A High Yield

2023-08-29 08:09:16 ET

Summary

- DT Midstream is a natural gas-focused midstream company operating in the Marcellus and Utica Basins, well-positioned to take advantage of growing natural gas demand.

- The company's assets include pipelines and natural gas storage, which can supply the demand from liquefied natural gas export terminals.

- DT Midstream has projects under construction and is pursuing opportunities for growth, including a new gathering pipeline network in the Utica Shale.

- The company has further growth potential as LNG demand continues to grow, potentially positioning it for revenue and cash flow growth through 2030.

- DTM boasts a very strong balance sheet and a sustainable 5.16% dividend yield.

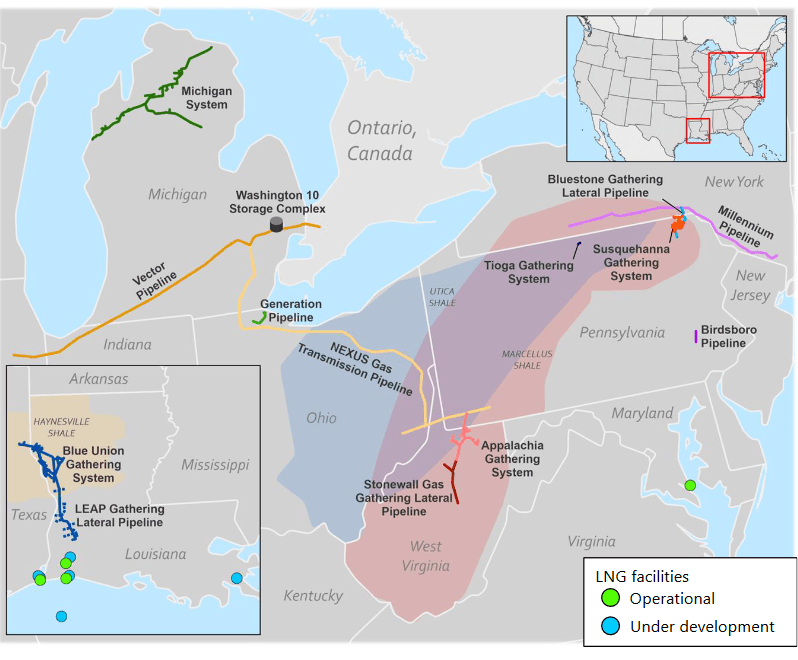

DT Midstream, Inc. ( DTM ) is a natural gas-focused midstream company that primarily operates in the Marcellus and Utica Basins of Appalachia, although it also has a small operation near the Haynesville Shale:

{kind=link}

These are two areas that are not commonly discussed in the mainstream financial media, but they are two of the richest hydrocarbon basins in the United States when it comes to natural gas. DT Midstream is one of the few midstream companies that is serving producers in these two regions, which positions it very well to take advantage of any growth in natural gas demand. As we have discussed in numerous previous articles, demand growth will almost certainly be coming over the next few years. For its part, DT Midstream has not been delivering the market performance that might be expected given its forward potential but that provides investors with a reasonably attractive way to get a 5.16% yield today. In my last article on this company, I also pointed out that DT Midstream has a very strong balance sheet and overall financial position. Several months have passed since then though, so it is worth revisiting our thesis and seeing how the company's story has played out over the past three quarters.

About DT Midstream

As stated in the introduction, DT Midstream is a natural gas-focused midstream company that operates in the Marcellus and Utica Basins in Appalachia, as well as in the Haynesville Shale. These regions are not as commonly discussed in the financial news media as oil-rich areas like the Permian Basin. However, Appalachia actually produces more natural gas than the Permian:

U.S. Energy Information Administration

The major factor that differentiates Appalachia and the Haynesville Shale from other hydrocarbon-rich basins is that they are targeted for the production of natural gas. The upstream companies that operate in most other American regions are interested in producing crude oil first and foremost, and the fact that their wells will also produce natural gas is something of an afterthought. As such, these basins will probably experience production growth as the demand for natural gas increases, which is likely to happen as electric utilities around the world utilize natural gas as a supplement to unreliable renewable generation technologies.

DT Midstream's assets consist of approximately 600 miles of intrastate and lateral pipelines, approximately 900 miles of long-haul interstate pipelines, and 94 billion cubic feet of natural gas storage. These pipelines are well-positioned to supply the growing demand for natural gas that is coming from the liquefied natural gas export terminals that the energy industry is constructing to meet the growing demand for natural gas from the world's electric utilities. The company currently has the ability to supply up to two billion cubic feet of natural gas per day specifically to meet this demand. The company has not stated how much of the natural gas that currently moves through its pipelines is going to these facilities, but it does not really matter. After all, from the company's perspective, any natural gas that moves through its system generates revenue for it. This is due to the business model that DT Midstream employs. I have explained the way the company's business model works in various past articles:

Basically, the company enters into long-term contracts with its customers. Under these contracts, the company provides transportation and storage for the customer's natural gas and the customer compensates DT Midstream based on the volume of natural gas that is transported, not on its value. This provides the company with a great deal of insulation against fluctuations in resource prices. In addition to this, the contracts that the company has with its customers include minimum volume commitments that specify a certain quantity of resources that must be sent through the company's infrastructure or paid for anyway. As it is typical for upstream producers to cut production when resource prices decline, this provides DT Midstream with further protection against the inherent volatility of commodity prices.

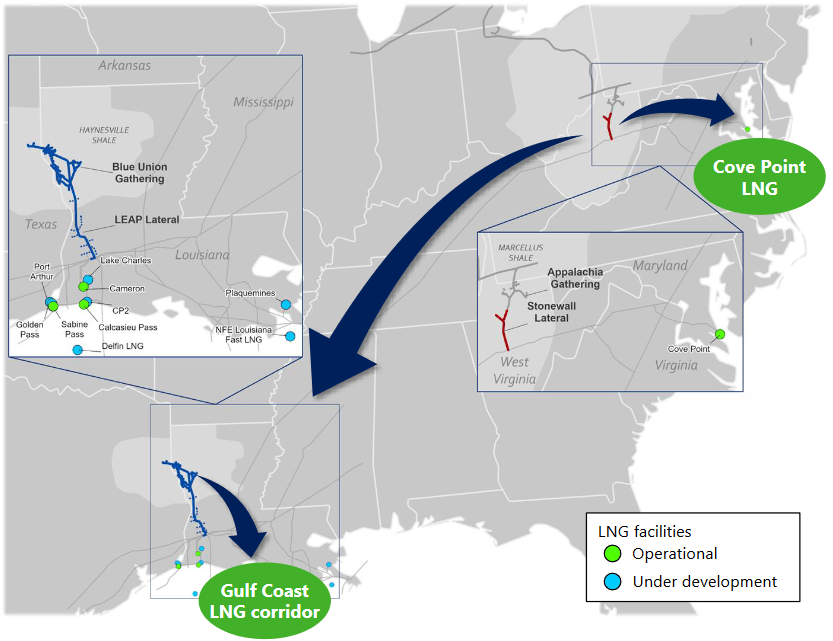

The major takeaway here is that DT Midstream's cash flows directly correlate to the volume of resources that it transports. Thus, when the company's volume of transported natural gas goes up, its cash flows should go up. There are two areas around which much of the construction of new liquefied natural gas plants has been centered. The first of these is around the Gulf Coast between Corpus Christi, Texas, and New Orleans, Louisiana. The second is south and east of Philadelphia, Pennsylvania. DT Midstream has significant operations in both of these areas:

{kind=link}

There are a number of new liquefaction plants under construction in these two areas, as can be clearly seen above. Once these are all operational, it will result in about twelve billion cubic feet of natural gas consumption in addition to the current consumption from the operational plants. This is all expected to happen by 2030. As should be immediately obvious, this could result in substantially more natural gas volumes flowing through DT Midstream's infrastructure.

Naturally, the demand growth will not benefit DT Midstream if it lacks sufficient capacity to actually transport the incremental resources to the new liquefaction plants. After all, a pipeline or other infrastructure is only capable of handling a limited amount of natural gas. Fortunately, the company has been pursuing various opportunities for growth. It is in discussions with customers in order to determine the amount of new transportation infrastructure that could be needed to meet their needs. It wants to have firm contracts in place before engaging in any construction, which is a good idea. After all, it costs a considerable amount of money to construct a new pipeline or other infrastructure and the company wants to make sure that it will be able to generate a positive return on any capital spending. This is a common practice in the industry, and it is one that we should be able to appreciate as investors.

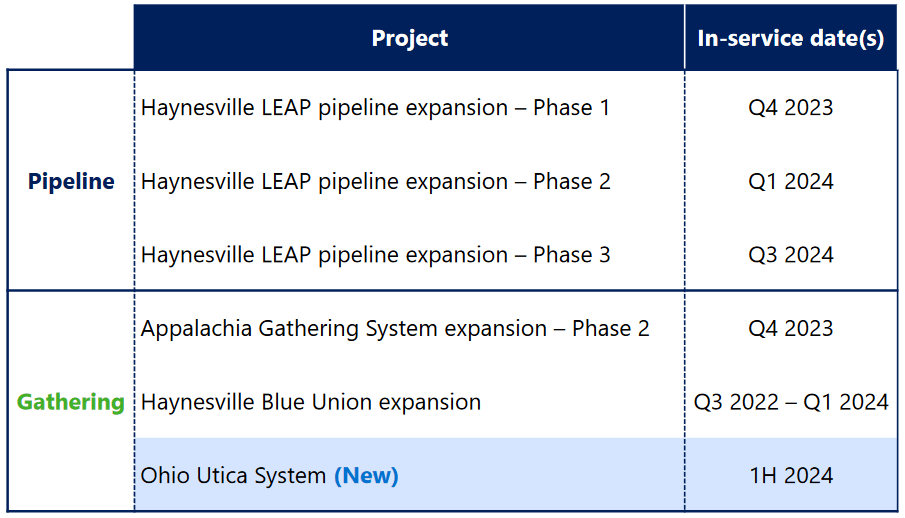

DT Midstream has a few projects that are currently under construction and are scheduled to come online between now and the middle of next year:

{kind=link}

The company already has firm contracts in place for the use of these new projects. As such, we can be reasonably sure that they will provide incremental revenue and cash flow to the company once they come online. This sets up the company well to deliver some growth to its investors while we wait for more projects to be approved (the company is trying to get projects in place to allow it to extend its growth through 2027).

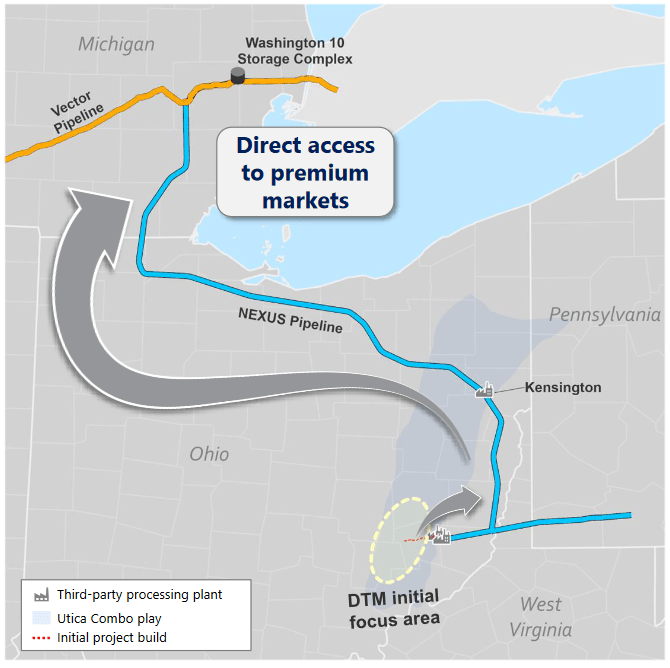

One of the projects shown above is new since our last discussion on DT Midstream. This project is the Ohio Utica System, which is expected to be completed sometime in the first half of this year. DT Midstream has not provided a lot of information about this project at this point, but it has stated that a large-cap investment-grade producer wants to conduct significant natural gas drilling activity in the western part of the Utica Shale. The drilling activity will be in the area identified by the yellow circle on this map:

{kind=link}

The producer has requested a system of gathering pipelines capable of handling at least 200 million cubic feet of natural gas per day, which will then be increased over the next eighteen to 24 months as the customer starts drilling activities. DT Midstream will connect this gathering system to its existing long-haul pipelines in the area to transport the natural gas to end-users in Michigan, Pennsylvania, and others.

DT Midstream has not stated who this customer is, which may be concerning to some investors at first. However, this is a very normal practice in the industry, and it is nothing to be concerned about. I can certainly guess who this customer might be, but ultimately it does not matter as long as the customer is financially able to fulfill its end of the contract. Any large-cap energy company with an investment-grade credit rating should be able to do that, so everything is probably fine here. DT Midstream will earn roughly a 5x build multiple if it manages to hit its budget projections of $100 million for the initial build-out. That means that this new system should generate an adjusted EBITDA of about $20 million annually. DT Midstream had adjusted EBITDA of $225 million in the first quarter of 2023 and $224 million in the second quarter of 2023. This new system should thus boost the company's adjusted EBITDA by about 2.23% above its current level.

Financial Considerations

It is always important to investigate the way that a company finances itself before making an investment in it. I explained the reason for this here:

It is always important that we investigate the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is usually accomplished by issuing new debt and using the proceeds to repay the existing debt, as very few companies have sufficient cash to completely repay all of their debt as it matures. This process can cause a company's interest expenses to increase following the rollover, depending on the conditions in the market. In addition to interest-rate risk, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company's cash flow to decline could push it into financial distress if it has too much debt. While midstream companies tend to enjoy remarkably stable cash flows, this is still not a risk that we should ignore.

As I pointed out before, the most common way to evaluate a midstream company's ability to carry its debt is by looking at its leverage ratio. As of June 30, 2023, DT Midstream had a net debt of $3.163 billion. As already mentioned, the company had an adjusted EBITDA of $224 million in the second quarter, which was in line with the first quarter. Thus, we can annualize the company's adjusted EBITDA to $896 million for the purposes of our analysis. This gives the company a leverage ratio of 3.53x, which is reasonable. It is certainly better than the 5.0x that Wall Street analysts are usually happy with, and better than the 4.0x that I usually like to see. Thus, the company does not appear to be having any difficulty carrying its debt.

Dividend Analysis

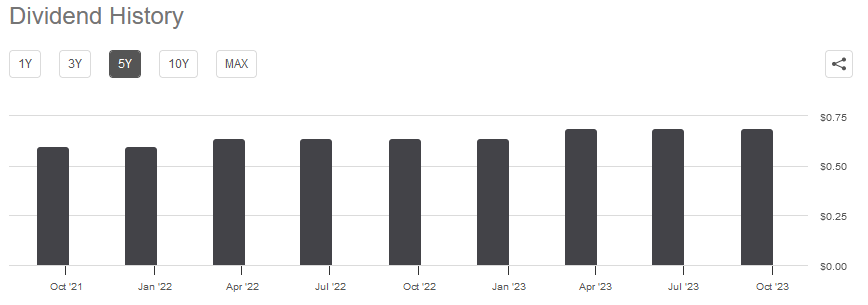

One of the biggest reasons why investors purchase shares of midstream companies like DT Midstream is the high yields that they normally possess. As of the time of writing, DT Midstream boasts a 5.16% yield, so it is certainly no slouch in this area. This is quite a bit lower than the 8.15% yield of the Alerian MLP Index ( AMLP ), however. Fortunately, DT Midstream does have a history of raising its dividend on an annual basis, which is nice to see during inflationary periods:

{kind=link}

As is always the case though, we want to ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut that reduces our incomes and almost certainly causes the company's stock price to decline.

The usual way that we judge a midstream company's ability to afford its dividend is by looking at its distributable cash flow, which is a non-GAAP metric that theoretically tells us the amount of cash that was generated by the company's ordinary operations and is available to be distributed to the common stockholders. In the second quarter of 2023, DT Midstream reported a distributable cash flow of $125 million, which represented a fairly steep decline over the $223 million that the company reported in the prior year quarter. However, it was still sufficient to cover the $67.0 million that the company paid out in dividends 1.87 times over. Generally, anything over 1.20 represents a dividend that is likely to be safe over the long term. As such, we should not really need to worry too much here. The dividend is quite safe overall.

Conclusion

In conclusion, DT Midstream is well positioned to profit from the growing demand for natural gas that is accompanying the world attempt to convert to "green energy." The company's assets are in basins that are somewhat untouched by other midstream companies but are very close to the numerous natural gas liquefaction plants that are being constructed. While that positions the company well in the long term, it will also benefit in the short term from the addition of a new gathering pipeline network in the Utica Shale. The company also boasts a very strong balance sheet and a sustainable dividend. The only real problem here is that the dividend yield is not as attractive as some other midstream companies possess.

For further details see:

DT Midstream: New Growth Projects And A High Yield