DTM - DT Midstream: Overlooked With Attractive Yield And No Debt Maturities Until 2028

2023-10-10 15:02:06 ET

Summary

- DT Midstream is a small-cap natural gas infrastructure firm focused on the Marcellus/Utica and Haynesville dry gas fields.

- The company operates unregulated gathering pipelines and FERC- and state-regulated interstate and intrastate pipelines.

- DT Midstream offers a competitive yield for a non-MLP pipeline firm and has a conservative balance sheet with no upcoming meaningful senior notes maturities.

DT Midstream ( DTM ) is a small-cap natural gas infrastructure firm structured as a C-Corp., so no dreaded K-1s. DTM's focus is on the Marcellus/Utica and Haynesville dry gas fields, which combined account for approximately 50% of total US dry gas production. DTM operates both unregulated gathering pipelines and FERC- and state-regulated interstate and intrastate pipelines. FERC-regulated assets' fee structure includes an annual inflation adjustment, which is similar to its peers. DTM probably will not be a barn burner of capital gains but offers a competitive yield for a non-MLP pipeline firm, fitting nicely in an income portfolio.

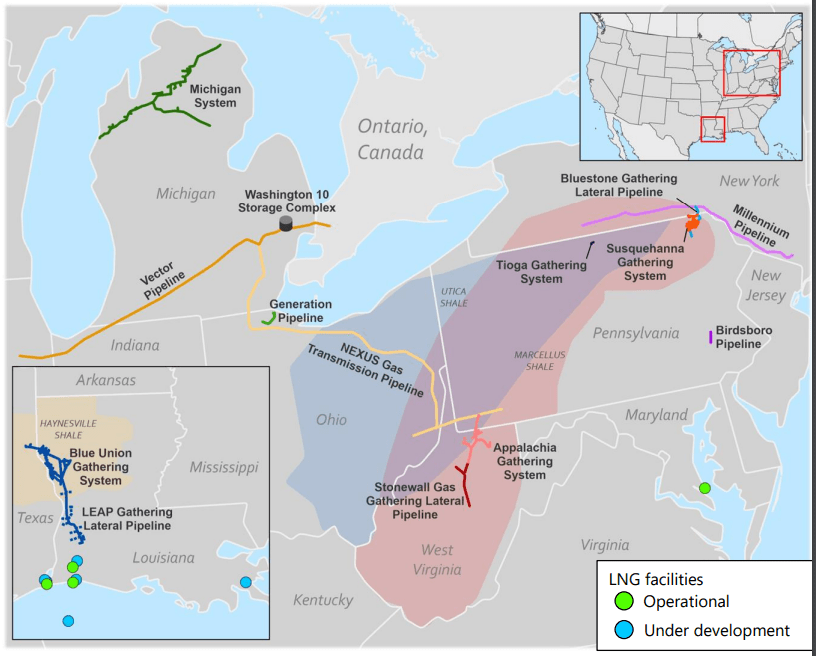

DT Midstream was spun out of Detroit-based utility DTE ( DTE ) in early 2021 and represented most of DTE's natural gas infrastructure business. Shedding of natural gas infrastructure by electric utilities has been a popular technique of utility restructuring over the past few years. The map below outlines the location of DT Midstream assets and is found in its latest investor presentation .

DTM Pipelines Assets (DTM Investor Presentation)

{kind=link}

DT Midstream is operated in two segments: Gathering and Pipelines. Gathering networks bring natural gas production from the wellhead to processing facilities. Lateral pipelines connect natural gas processing facilities with larger interstate gas transportation pipelines. Interstate pipelines are fed by multiple lateral pipelines which are fed by numerous gathering networks. Gathering networks are considered the most commodity and volume sensitive in the pipeline chain, while lateral and interstate pipelines are considered not as sensitive. As gas prices increase, so does drilling activity, increasing demand for gathering pipeline services. If drilling activity decreases, so does the volume of gathering pipelines. All three types of pipelines usually utilize minimum volume contracts, called "take or pay", where the customer guarantees a specific amount of volume regardless of their actual spot needs and production. However, take or pay is used less in gathering pipeline contracts and these are more susceptible to actual wellhead volumes produced - hence the higher exposure to commodity pricing and volumes. Lateral and interstate are usually lumped together as long haul natural gas transportation assets.

Gathering networks are not regulated by the government; intrastate lateral pipelines are state-regulated; interstate pipelines are FERC-regulated. From an investment vantage point, gathering networks are considered as higher risk due to its exposure to commodity pricing and volumes while interstate/intrastate are considered the least risky. DT Midstream focuses on two major dry gas fields, Appalachia and Haynesville, and offers both gathering and transport pipeline services to producers in these active basins.

Appalachia dry gas production is constrained by a lack of existing pipelines. To the north, New York state is a hostile regulatory environment for additional pipeline capacity, as shown by the multiple-year fight to build the National Fuel Gas' ( NFG ) Northern Access pipeline with 85% of capacity going to exports to Canada. Exiting capacity to the east is equally restrictive and is reflected in the cancellation of the Atlantic Coast pipeline and the uncertain fate of the Mountain Valley Pipeline. These factors lead to a potential preference to locate additional exiting capacity to the west through Ohio, and western exiting favors DTM's Nexus pipeline. There are both additional wells anticipated and added commercial and industrial use of natural gas along the Nexus corridor. It is noteworthy that DT Midstream operates the Nexus, Vector, and Millennium pipelines as joint ventures. DTM owns the following percentage of each: 50%, 40%, and 52.5%, respectively.

Haynesville basin in NW Louisiana and NE Texas was commercialized in 2008 and was one of the popular dry shale gas plays in the southern US. However, over the years, drilling activity declined as more secondary/by-product natural gas was produced in oil-rich areas like the Permian. However, with increased LNG export activity along the TX/LA coast, Haynesville is the closest supplier to this new demand. Haynesville is undergoing a rebirth and recently produced a record level of natural gas. As shown in the above graphic, there are three operational LNG facilities close to Haynesville, with five more in development. DT Midstream offers both gathering and lateral pipeline services for companies looking to develop long-term LNG supply contracts from the Haynesville basin.

From an operational perspective, ~75% of DT Midstream revenues are generated from fixed fees, with many contracts utilizing "take or pay" commitments. DTM's average weighted contract has 9 years remaining. This revenue profile creates consistency in cash flow. In 2022, approximately 65% of EBITDA was generated from Appalachia, 30% from Haynesville, and 5% from other regions. 2022 adjusted EBITDA exceeded $800 million with 43% generated from the gathering segment and 57% from the pipeline segment, of which 40% was cash distributions from pipeline joint ventures.

In addition, DTM has a very conservative balance sheet with plenty of breathing room to fund capital expansion projects from operating cash flow. There are no debt maturities until 2028 and 77% of debt is fixed rate with a coupon of 4.35% and less. According to the second quarter 10-Q , DTM has three senior notes outstanding and a revolving Line of Credit: 2029 $1.1 billion at 4.125%; 2031 $1.0 billion at 4.375%; 2032 $600 million at 4.30%; and a 2028 $400 million Term Loan at SOFR + 2.11%. Having no meaningful senior notes maturities until 2029 provides management the ability to expand cash flow through internally funded growth capital and gives management the option to pay down debt from operating cash flow prior to maturity. This financial advantage is not going unnoticed by analysts, with several commenting that DTM should be free cash flow positive by the end of next year.

Last August, Fitch offered an unusually in-depth review of DT Midstream during its re-confirmation of DTM's BBB- senior secured ratings, along with an upgrade to a Positive outlook from Stable. Interestingly, Fitch believes DTM has a high exposure to counterparty risk. Southwestern Energy Company ( SWN ) generated ~65% of DTM 2022 revenues with a significant portion of the contracts containing "take or pay" volume commitment. Fitch offered this overall DTM comment:

Given the acquisition of additional interest in Millennium Pipeline, success in signing demand-pull contracts, and an expansion of the Louisiana Energy Access Pipeline LEAP, Fitch anticipates the pipeline segment, including the JVs, will grow faster than the gathering segment in the near term and contribute approximately 60% of adjusted EBITDA in 2023. The increasing weight of the pipeline business adds additional stability to the cash flow as this segment is generally less volatile than the gathering business.

FERC-regulated pipelines employ an approved formula as a maximum fee for rate setting. Most pipeline operators utilize this formula in their contracts, and the FERC formula includes an annual inflationary adjustment. For instance, the FERC announced a 2023 formula index rate increase of 13%, based on adjustments of its inflation input as reported by the Producer Price Index for Finished Goods (PPI-FG). Pipelines using the FERC Pipeline Index in their rate contracts were given permission to raise rates in 2023. This annual inflation rider is an underappreciated attribute of FERC-regulated assets.

DT Midstream is currently analyzing an opportunity for its first carbon capture and storage project, which could reach a final investment decision in the first half of next year. It seems Louisiana is becoming the carbon-sequestering capital of the US, and with DTM's current Haynesville footprint, the opportunity to expand into this field seems ripe. About 30 carbon-capture projects have been proposed in Louisiana, all spurred by federal subsidies and supercharged by increased incentives in the Inflation Reduction Act. A total of 170 projects have been announced nationwide, with only Texas having more projects than Louisiana. In early August, the DOE announced $1.2 billion in investments in carbon capture projects in Louisiana and Texas. If approved by DTM's BOD, carbon sequestering should be an addition to its investment thesis and future cash flows.

DTM currently yields 5.1% and trades at $54. Earnings are expected to grow by 6% to 8% annually, which will allow for similar growth in the dividend. While many MLPs with K-1s offer a higher yield, as a smaller C-Corp pipeline operator, DTM is a nice balance to higher-yielding pipeline MLPs, such as Enterprise Product Partner ( EPD ), which I have also owned for over 20 years.

I first bought DT Midstream in the mid-$40s upon separation in 2021, based on its western Appalachian exit footprint and the rebirth of the Haynesville basin. Last month, I made another buy of DTM as it dropped below $51, after missing the mid-$40s last May. I plan on buying more on additional drops below $50. Investors looking for a non-K-1 natural gas pipeline company with a conservative balance sheet, with positive free cash flow in 2024, and with several growth drivers should conduct a deep dive into DT Midstream. Over the medium term, DTM is well positioned for growth opportunities in western exiting Appalachian pipelines along with the rebirth of Haynesville to supply new LNG export facilities.

For further details see:

DT Midstream: Overlooked With Attractive Yield And No Debt Maturities Until 2028