DTM - DT Midstream: Strong Fundamentals Should Overpower Market Noise

2023-03-18 04:21:33 ET

Summary

- DT Midstream continues to post good results following the fourth quarter of 2022.

- When looking ahead into 2023, their guidance is now even higher than previously forecast, plus preliminary guidance for 2024 also points towards more strong growth.

- Admittedly, this is accompanied by high capital expenditure during 2023, but this does not endanger their dividends, as it is only temporary.

- Once this winds down in the future, they should see plenty of scope for more strong dividend growth, given the modest size of their payments at the moment.

- Despite the recent widespread sell-off, these strong fundamentals should overpower market noise, and thus, I believe that maintaining my buy rating is appropriate.

Introduction

When last discussing DT Midstream (DTM) earlier in 2023, it seemed that higher dividends were very likely coming soon, as my previous article flagged. Thankfully, it was not a long wait before shareholders were treated to a strong circa 8% dividend increase when their results for the fourth quarter of 2022 landed. Although positive, their share price is down around 10% since conducting my previous analysis as markets fret over banking stability concerns and recession risks, thereby causing a widespread sell-off. Whilst not necessarily ideal for existing shareholders, in the long-term their strong fundamentals should overpower market noise with plenty of scope for more strong dividend growth on the horizon.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

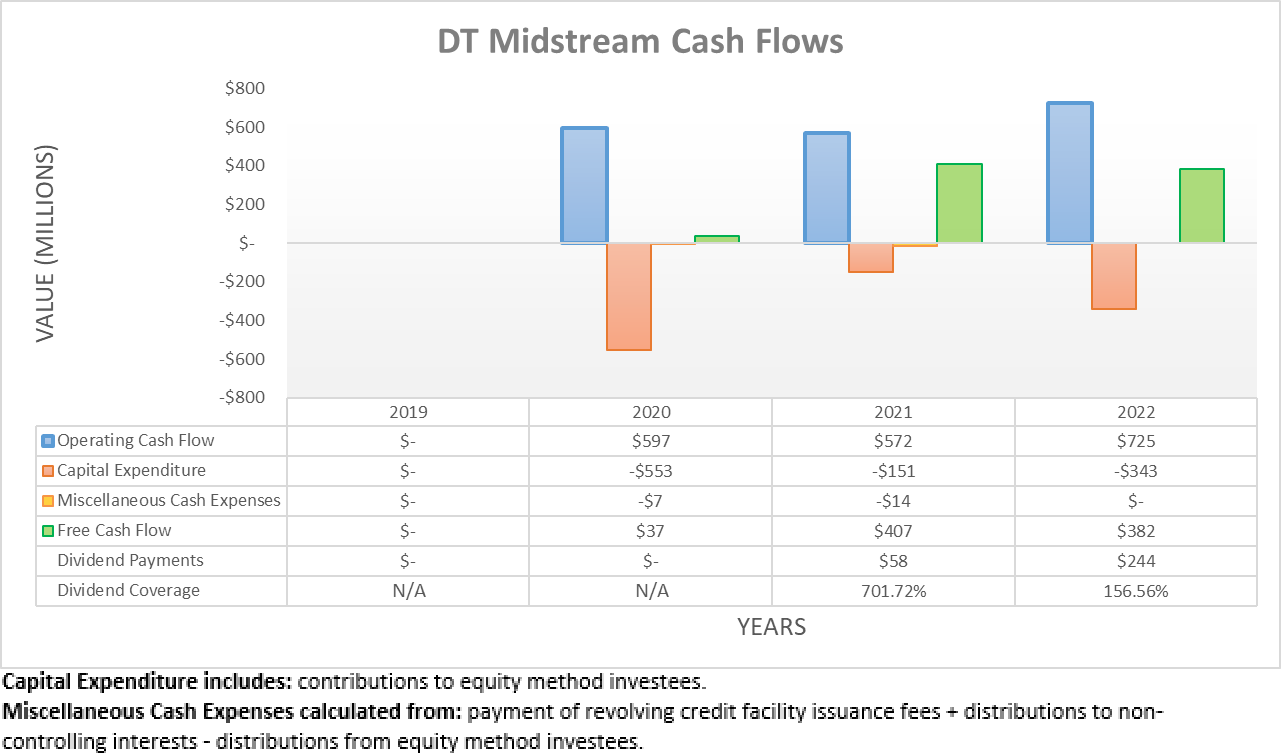

Following a good start to 2022 during the first nine months, it was positive to see this continue during the fourth quarter, thereby seeing the year ending with operating cash flow of $725m. Whilst they only have a short history of three years, this nevertheless sets a new record and easily surpasses their previous result of $572m during 2021.

{kind=link}

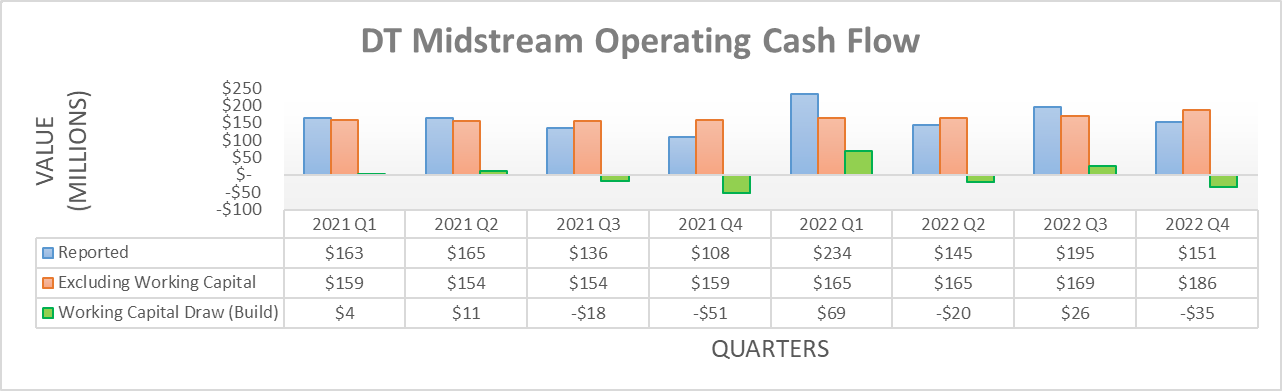

When looking at quarterly cash flow performance, it shows the fourth quarter of 2022 itself enjoyed a very strong result. Technically not their reported result of $151m that was weighed down by a $35m working capital build. Rather, it was their underlying result of $186m that easily surpassed anything in their history, at least since the beginning of 2021. If aggregating their working capital movements across 2022, they ultimately saw a working capital draw of $40m across the full year, thereby leaving their underlying result at $685m. If this same process were applied to their previous results during 2021, their equivalent result was $626m and thus, 2022 still represents a good improvement year-on-year, which builds momentum heading into 2023.

DT Midstream Fourth Quarter Of 2022 Results Presentation

As we move into the year ahead, their guidance for 2023 now forecasts a result of $900m at the midpoint, which is another $15m higher than was forecast within their preliminary guidance that my previous analysis discussed. This further adds to their growth which was already solid and thus now sees strong growth of around 8.50% year-on-year versus their result of $830m during 2022, as per their fourth quarter of 2022 results announcement. In theory, their underlying operating cash flow should scale higher year-on-year by a similar magnitude and thus climb from $685m to circa $740m during 2023. Even more excitingly, management also provided preliminary guidance for 2024 that sees their strong growth continuing with their adjusted EBITDA forecast to reach $945m at the midpoint that represents another increase of 5% year-on-year versus their forecast for 2023.

The last week was a tough one as markets fret over banking stability and the risks of a recession but thankfully, their financial performance should be largely unaffected given their minimum volume commitments cover circa 90% of their revenue. Not to mention, similar to most in the midstream industry, they have no direct commodity exposure and thus the recent sell-off in oil and gas prices is nothing more than market noise.

DT Midstream Fourth Quarter Of 2022 Results Presentation

Whilst undoubtedly very positive, to be fair their strong growth does not necessarily come cheap per se. In fact, this means their guidance for 2023 forecasts capital expenditure will reach $647.5m at the midpoint, which is quite a large increase year-on-year versus their capital expenditure of $343m during 2022.

DT Midstream Fourth Quarter Of 2022 Results Presentation

After lifting their quarterly dividends higher to $0.69 per share, their cost is now $267.4m per annum given their latest outstanding share count of 96,888,357. When combined, this leaves estimated cash outflows for 2023 at circa $915m, which sees a net cash outflow of circa $175m once considering the cash inflow from their estimated operating cash flow of $740m, give or take a little depending upon working capital movements.

Since their forecast capital expenditure for 2023 consumes most of their estimated operating cash flow, it means their dividend coverage will be very weak given the reliance on external capital from debt markets. Thankfully, this is not necessarily a problem because it results from large growth investments, which consume the vast majority of their forecast capital expenditure guidance. Once they pass this era, they should have zero problems funding their dividend payments with free cash flow given they represent only a modest size compared to their operating cash flow, which in turn should see plenty of scope for strong dividend growth.

{kind=link}

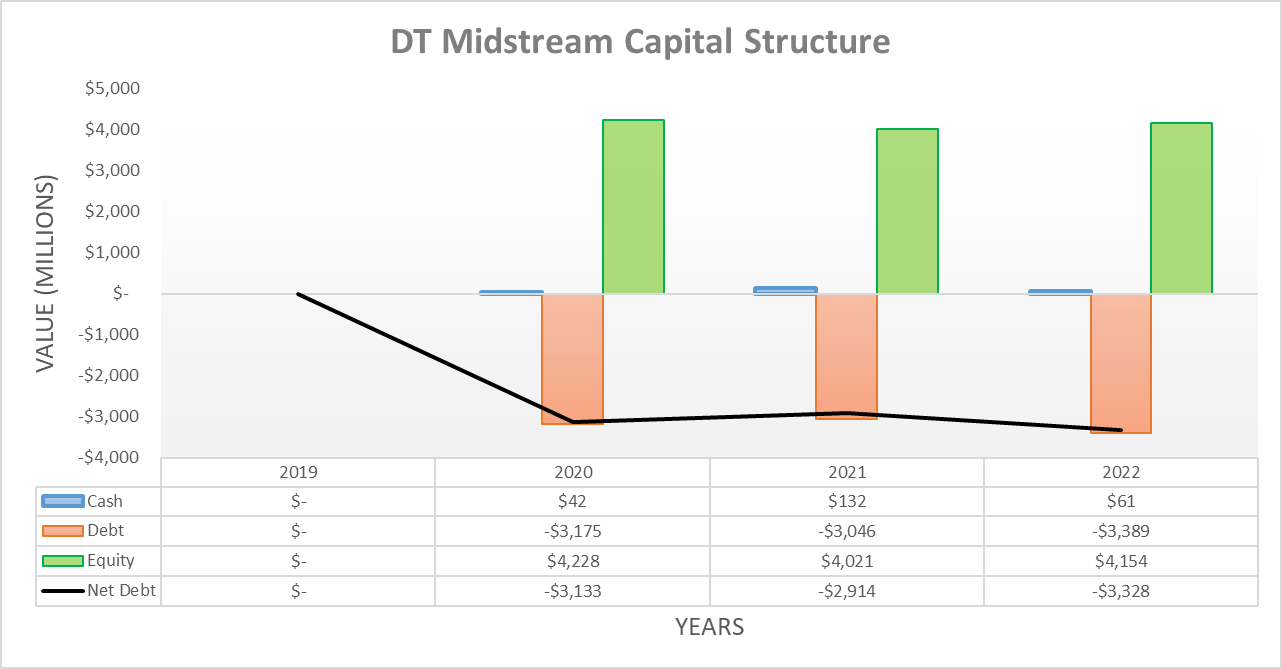

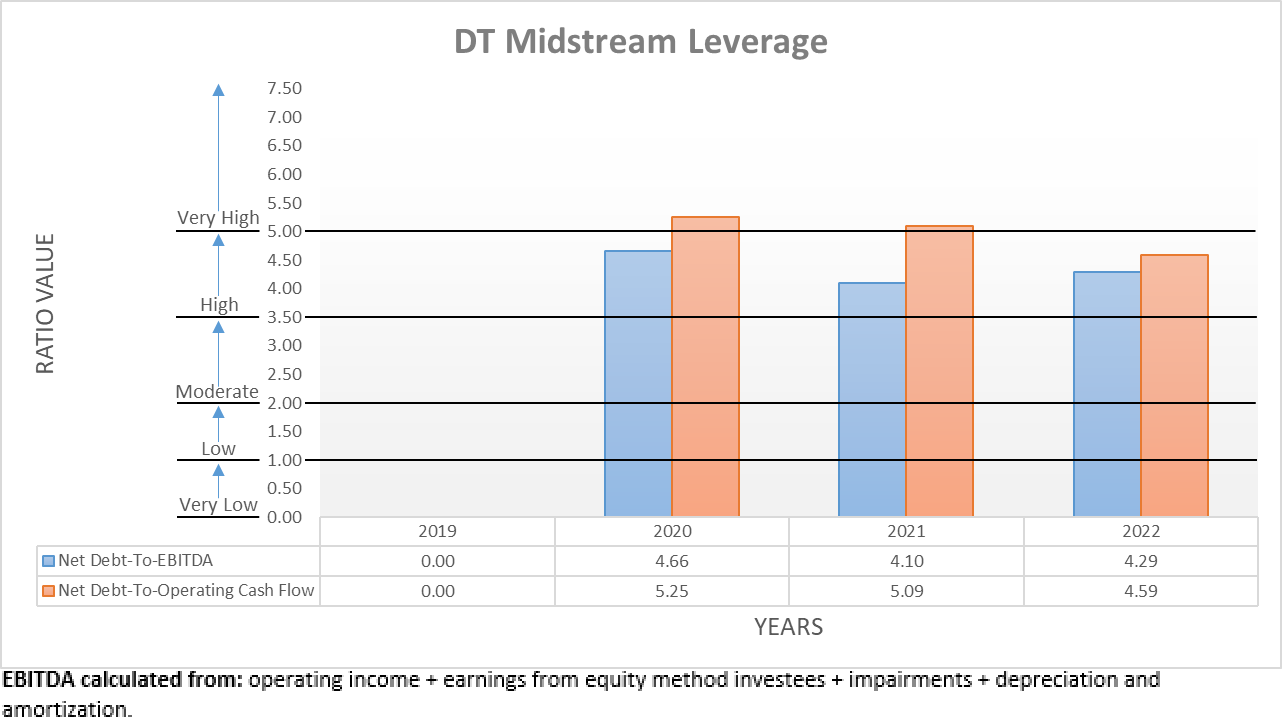

The fourth quarter of 2022 saw their net debt spike to $3.328b versus its previous level of $2.703b following the third quarter, as was expected when conducting the previous analysis given their bolt-on Millennium Pipeline acquisition . Whilst their net debt should continue increasing going forwards into 2023 given their aforementioned estimated net cash outflow of $175m, this should largely be offset by their guidance for higher earnings. As a result, it would be redundant to reassess their leverage and debt serviceability once again, especially because their updated guidance for 2023 and the resulting implications for their cash flow performance were the primary focus of this follow-up analysis.

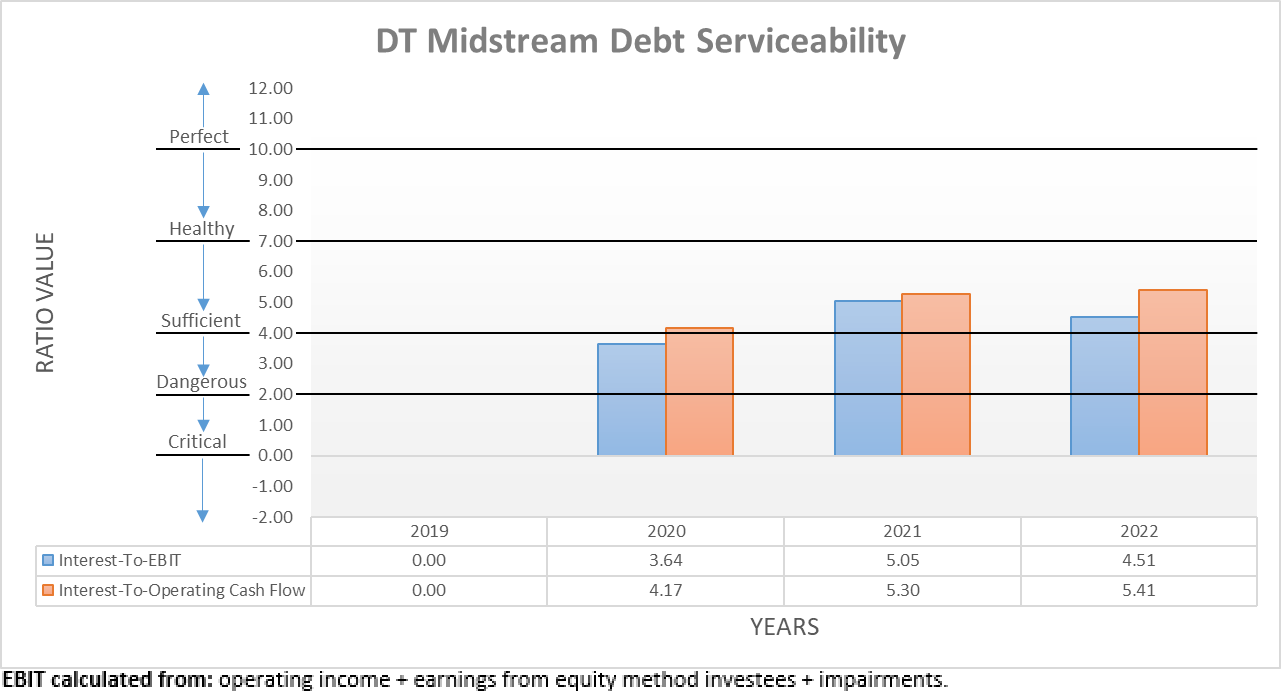

The two relevant graphs are still included below to provide context for any new readers, which shows they have a net debt-to-EBITDA of 4.29 and a net debt-to-operating cash flow of 4.59. These are both around the middle of the high territory of between 3.51 and 5.00, which is not concerning for a midstream company that sports strong growth prospects. Likewise, their debt serviceability remains healthy with interest coverage of 4.51 and 5.41 when compared against their EBIT and operating cash flow, respectively. If interested in further details regarding these topics, please refer to my previously linked article.

{kind=link}

{kind=link}

{kind=link}

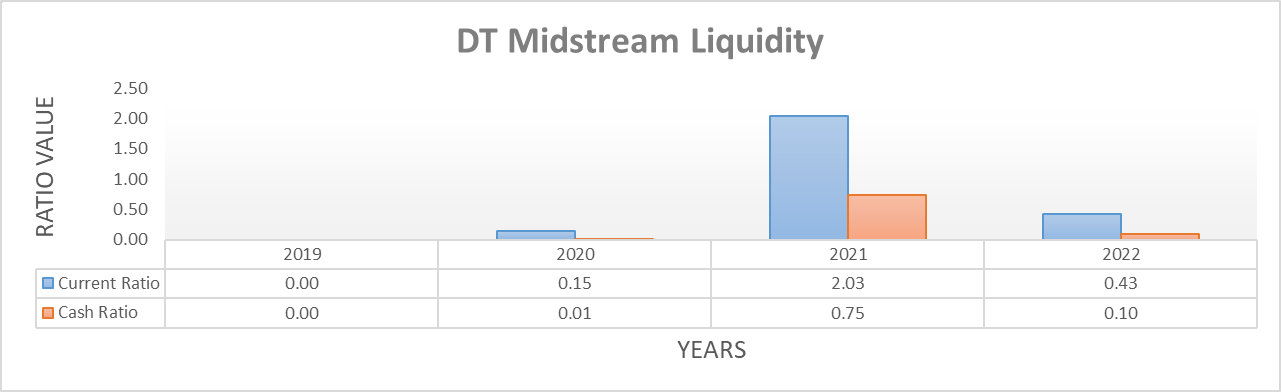

Whilst there was nothing new to discuss regarding their leverage and debt serviceability, there were some developments within their liquidity worth than explanation, especially because on the surface they may seem more concerning than actually the case. When looking at their current ratio following the fourth quarter of 2022, it plunged to what seemingly is a worryingly low 0.43 versus its previous result of 2.41 following the third quarter. Likewise, their cash ratio also followed in tandem by plunging to 0.10 versus 1.43 across these same two points in time, respectively.

This was largely driven by their aforementioned Millennium Pipeline acquisition, which drained most of their previous cash balance of $355m following the third quarter of 2022 to only $61m following the fourth quarter. Additionally, they also borrowed $330m from their credit facility, which was accounted for as short-term borrowings, despite it not actually maturing until October 2027 and as such, this saw it listed as a current liability on their balance sheet. If excluding the latter variable, it more aptly shows their current and cash ratios would have otherwise been 0.92 and 0.21.

They still retain a further $631m of availability within their credit facility, which should be plenty to see them through 2023 without accessing debt markets given their aforementioned estimated net cash outflow of $175m. Equally as importantly, they see no other debt maturities until after 2027, as per their 2022 10-K and thus, when wrapped together it means their liquidity is still strong.

Conclusion

Even though the last week was a tough one for shareholders with their share price sliding alongside almost everything as markets fret over banking stability and recession risks, this is merely market noise for this stable midstream company that is forecasting strong growth in the years ahead. As such, I see no reasons to expect their strong dividend growth to stall anytime soon and with their yield now pushing towards a high near-6%, I believe that maintaining my buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from DT Midstream's SEC Filings , all calculated figures were performed by the author.

For further details see:

DT Midstream: Strong Fundamentals Should Overpower Market Noise