PEG - DTE Energy: Valuation Has Improved Compared To Peers Presenting Opportunity

2023-10-13 10:56:22 ET

Summary

- DTE Energy Company, a regulated electric and natural gas utility, offers a dividend yield of 3.89% and a history of growing dividends over time.

- The stock has underperformed the S&P 500 Index and the U.S. Utilities Index over the past two months, but its recent decline in price makes it more attractively valued.

- DTE Energy's customer base has remained stable, although the population of Detroit, its primary service area, is declining.

- The company enjoys remarkably stable revenue and operating income regardless of economic conditions, which should position it well to weather whatever comes.

- The company formerly benefited from ESG interest, but that seems to have declined. DTE Energy stock now appears to offer a very attractive valuation.

DTE Energy Company ( DTE ) is a regulated electric and natural gas utility that primarily serves the Greater Detroit, Michigan metropolitan area. The utility sector has long been among the favorite investments for more conservative investors who do not want to take on much risk, which has led to them sometimes being referred to as “widows and orphans” stocks.

There are some good reasons for this, as most utilities have fairly low growth rates and tend to pay high dividend yields. For its part, DTE Energy yields 3.89% at the recent price. This is not especially impressive considering that anyone can get a 5% yield in an ordinary money market fund or high-yield bank savings account right now, but the fact that DTE Energy has a history of growing its dividend over time helps to make up for this. After all, if the company continues along this trajectory, it will have a much higher yield in only a few years. In that way, it could provide a source of income that grows with time, which helps to offset inflation. That is always very nice to see.

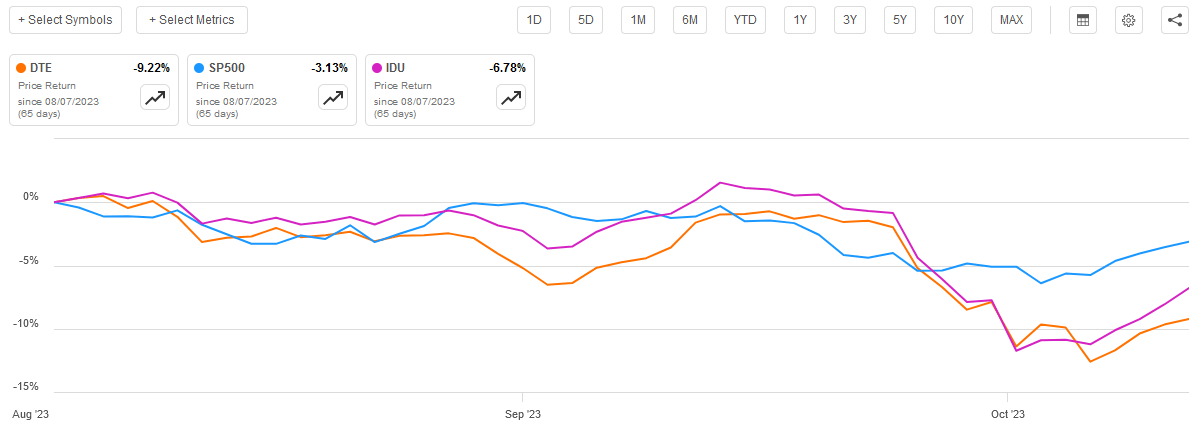

As regular readers likely recall, we last discussed DTE Energy Company in early August. It pretty much goes without saying that the market has changed significantly since that time, as the market has gradually begun to believe the “higher for longer” mantra coming out of the Federal Reserve and has adjusted the price that it pays for various assets as a result. DTE Energy was certainly not immune to this as the stock is down 9.22% since the time that the previous article was published. That is worse than either the S&P 500 Index ( SP500 ) or the U.S. Utilities Index ( IDU ):

{kind=link}

This underperformance is disappointing, but it is not entirely surprising. After all, as I pointed out in various previous articles on DTE Energy, the stock has generally been fairly expensive relative to the rest of the sector. This was due to the company’s very aggressive rhetoric with respect to its renewable energy ambitions. Renewable energy was a popular theme in the aftermath of the pandemic, but it has started to lose its shine over the past several months as the market began demanding more immediate profits and returns.

The stock price decline may have worked in the favor of new investors in DTE Energy, though. The stock currently looks to be trading at a more attractive valuation than we have seen in a long time, but none of the fundamentals about the company have worsened. Thus, it may be a good time to revisit this Michigan-based utility giant.

About DTE Energy

As stated in the introduction, DTE Energy is a regulated electric utility that primarily operates in the city of Detroit, Michigan, and the surrounding suburbs.

DTE Energy

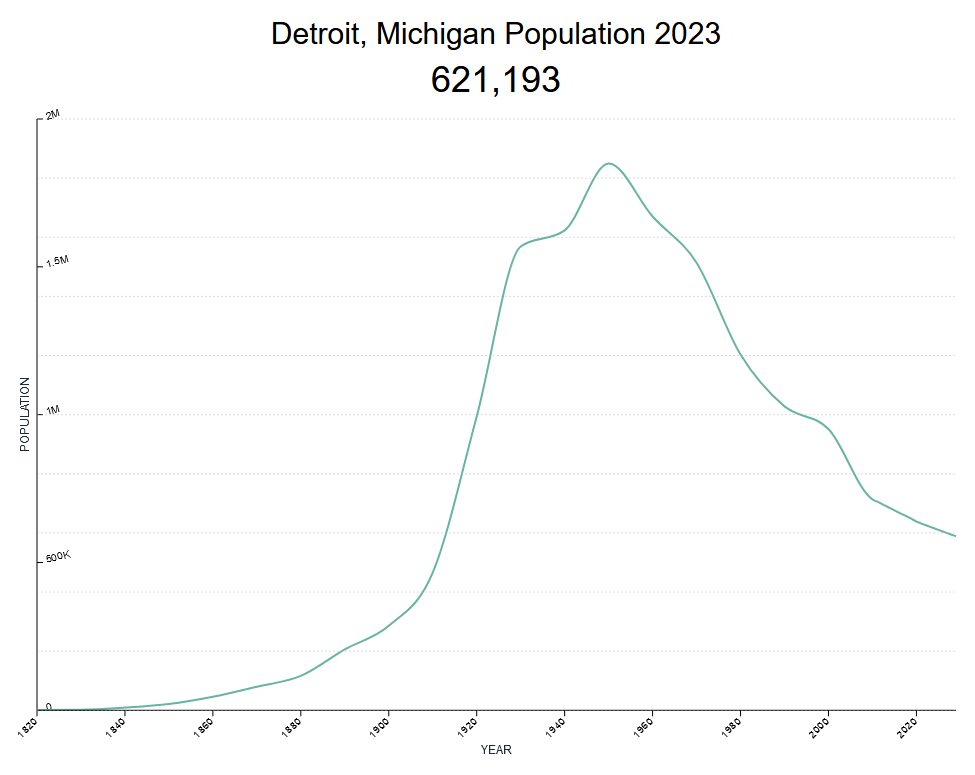

Detroit is the largest city on the border between the United States and Canada, but it is only 27th in the United States with an estimated population of 621,193. Unfortunately, the population of the city is declining at a fairly rapid rate:

{kind=link}

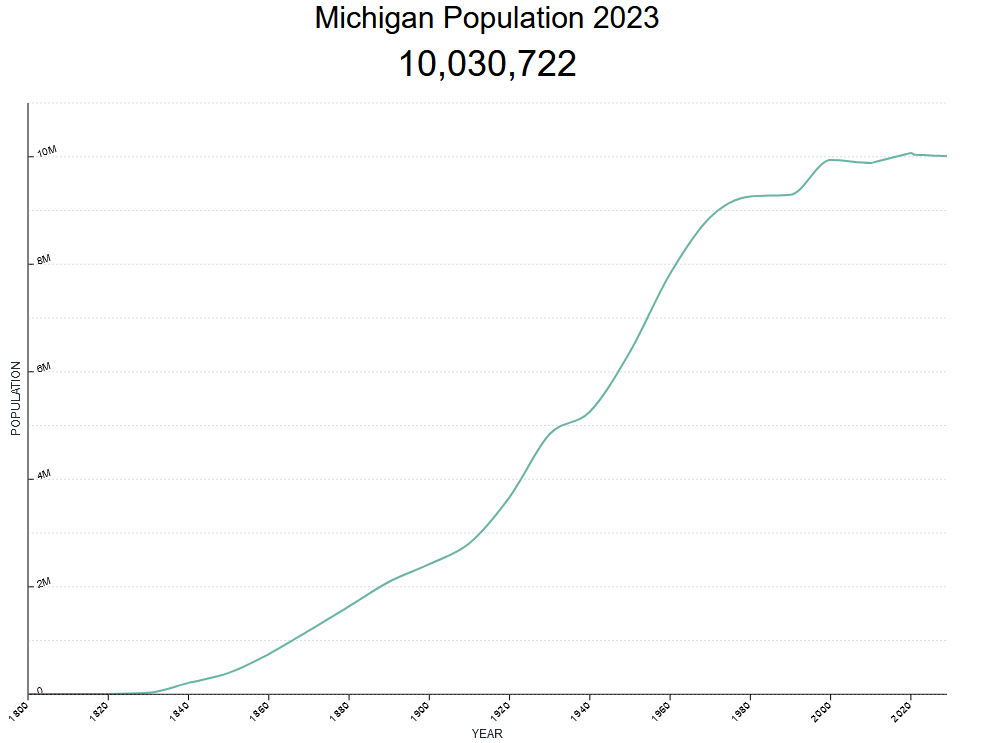

This is not a particularly good situation for DTE Energy Company, because it means that its customer base, at least in that area, is declining. Fortunately for DTE Energy, the population of Michigan itself remains relatively stable:

{kind=link}

Thus, it appears that people who can afford to leave the city itself are doing so, but they may simply be relocating to the suburbs. As long as they are not leaving the company’s service territory, this is probably not a very big deal. Unfortunately, DTE Energy does not specifically provide a chart on its website or in its investor materials showing its customer count as some other utilities do. This is a possible sign that the trend is not particularly favorable. In its second-quarter 2023 earnings report , the company stated the following:

DTE Energy is a Detroit-based diversified energy company involved in the development and management of energy-related businesses and services nationwide. Its operating units include an electric Company serving 2.3 million customers in Southeast Michigan and a natural gas company serving 1.3 million customers in Michigan.

The company’s customer count stood at 2.3 million electric and 1.3 million natural gas customers at the end of 2021 . Thus, it does not appear that the company is experiencing much growth in terms of its customer base. However, it is also not losing customers, which is a good sign.

The reason that the company’s customer base is important is that increasing the number of customers that it serves is one of two ways through which a regulated utility can grow. After all, the more people that the company supplies with electricity or natural gas, the more people that it has paying their monthly bills and thus providing it with revenue. All else being equal, this should give the company more profits since it has more money available to pay its regular expenses. This is something that is completely out of a utility’s control, but there are enough other utilities throughout the United States that are growing their customer counts that we do not need to be satisfied with one that is static.

With that said, DTE Energy Company has generally delivered revenue growth over the years, but it has not been perfect in this respect. This chart shows the company’s revenues over the past ten full-year periods, as well as over the twelve-month period ending June 30, 2023:

{kind=link}

We can see strong growth here, although it has not been stable. In particular, the company’s revenues declined significantly in both 2019 and 2020 before returning to growth in 2021. The company also experienced a revenue decline in 2015 and 2016, but the company did have much more exposure to natural gas prices than it does today and that corresponds to one of the most challenging periods of time that the energy industry experienced in the 21st century.

The company’s operating income shows much the same trend, as it generally grew over the past ten years, too:

{kind=link}

Granted, neither of these are perfect trends, as there were some periods in which DTE Energy’s revenue and operating income declined. However, we can still see that the company’s financial performance is generally far more stable than we see in companies in most other sectors. That is part of the appeal of the utility sector in general, which I pointed out in the introduction.

I explained the reason for this incredible stability over time in my last article on the company:

The reason for this stability should be fairly obvious. DTE Energy provides a product that is generally considered to be a necessity for our modern way of life. After all, how many people do not have electricity in their homes? Natural gas service is likewise a necessity for people whose residences use a natural gas heating system. As these things are considered to be necessities (and may even be required by habitation laws), people will generally prioritize paying their utility bills ahead of discretionary expenses. This is only natural as it makes no sense to buy a new smartphone or spend your money on a fancy restaurant dinner when you do not even have electric or heat at home.

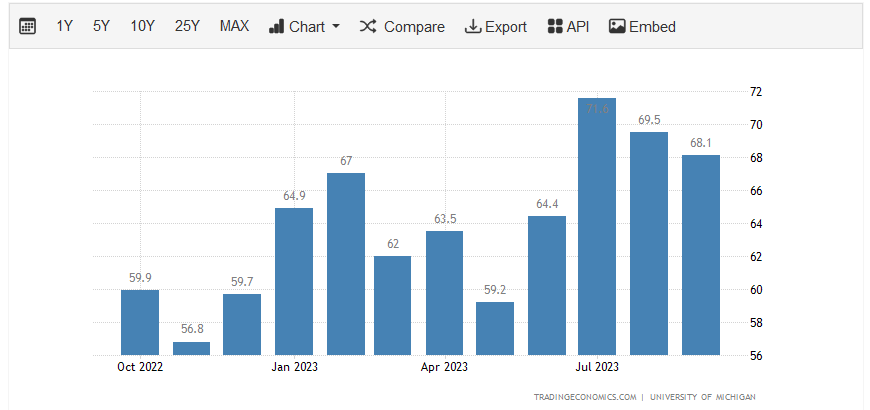

Over the past three months, consumer confidence has been declining:

{kind=link}

While it still remains higher than it did near the start of the year, this is still a sign that consumers may slow down somewhat on their spending. After all, when people are less confident about the future, they tend to slash their unnecessary spending, pay down debt, and prepare for challenges ahead. This is one reason why consumer and business confidence are often leading indicators of a recession. In a few recent articles, I pointed out that an overwhelming majority of corporate chief executive officers expect a recession next year, and they are likely to base their companies’ investment decisions on that belief. Thus, we could very well see a recession settle in. DTE Energy should be much more resistant to recessions than many other companies due to the nature of its business. After all, during a recession, consumers may opt to stay home and watch television instead of going out to a show. They are still likely to pay their electric bill, though, so DTE Energy should be able to weather through just fine.

DTE Energy And Environmental, Social, And Governance Initiatives

In the introduction to this article, I suggested that DTE Energy had a certain amount of following from those investors who are interested in environmental, social, and governance as an investment movement. This is a concept that grew in popularity around the time of the pandemic that espouses that a company’s stance on climate change, employee diversity, executive pay, and various other issues has an effect on its financial performance. This is one of the reasons why so many companies over the last few years have started to involve themselves in politics or create employee diversity programs. They even frequently promote these initiatives in industry or analyst presentations and events.

There is a good reason for doing this as numerous fund houses set up environmental, social, and governance funds for the stated purpose of only buying equities issued by companies that managed to espouse certain principles. A 2020 report from the US SIF Foundation found that investors had $17.1 trillion invested in assets chosen specifically because the issuing companies met certain criteria under these principles. American mutual funds and exchange-traded funds that invested only in companies with a sufficiently high rating under these principles had $400 billion under management in 2021. This is a substantial amount of money, and easily sufficient to have an impact on the stock performance of any company. Thus, it becomes fairly obvious why companies would attempt to court the people investing based on these principles.

DTE Energy was a fairly popular company among investors following these principles. This is partly because of the company’s ambitious goals to achieve net-zero emissions across both its electric and natural gas utilities. The company was also fairly aggressive at promoting its qualifications in investor presentations. For example, the company has an investor update on its webpage right now that devotes eight full pages to discussing its various environmental, social, and governance initiatives.

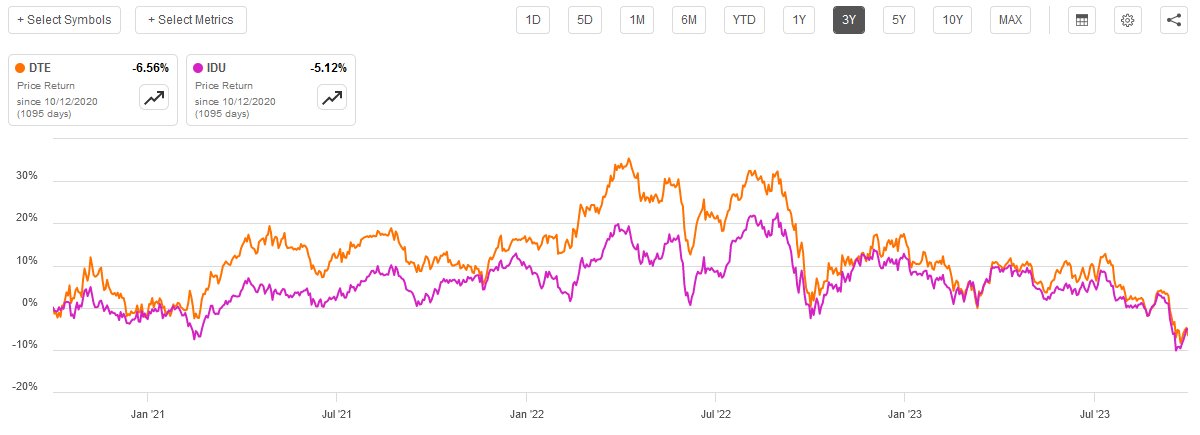

Regardless of your individual stance on this concept, there is a lot of money involved and it does seem likely that the company managed to attract some of it for its renewable energy initiatives if nothing else. Indeed, in prior articles on the company, I suggested that DTE Energy could see some benefit from it as investors bought it up for its credentials. We certainly saw that reflected in the stock’s performance. As we can see here, DTE Energy’s stock outperformed the U.S. Utilities Index for two of the past three years:

{kind=link}

However, we see the company’s share price crash during the latter part of 2022 and underperform the index overall. This actually corresponds to the rapid pull away from environmental, social, and governance principles as an investment thesis.

24/7 Wall Street has a great summary of this, which can be found here . The article specifically mentions that more than twenty environmental, social, and governance funds have shuttered this year due to poor performance and investor interest. The article suggests that more closings could be coming.

This has, unfortunately, worked against DTE Energy over the past year or so. However, it could work to investors’ advantage going forward. As I pointed out in my articles on DTE Energy over the past two years or so, the company has been somewhat expensive compared to its peers. That appears to be changing now.

Valuation

According to Zacks Investment Research , DTE Energy will grow its earnings at a 6.00% rate over the next three to five years. This is at the low end of management’s 6% to 8% guidance, but it is certainly a very reasonable estimate of the company’s earnings per share growth prospects. It is also the same figure that Zacks has been projecting since at least the end of 2021, which can be clearly seen by looking back at the articles that I published on this company from that time.

That growth rate gives the company a price-to-earnings growth ratio of 2.63 at the current stock price. This compares to the 3.33 ratio that the company had at the end of 2021 and the 2.91 ratio that the company had back in August. Thus, we can clearly see that the price is getting cheaper. Here is how DTE Energy compares to its peers:

| Company |

| PEG Ratio |

| DTE Energy |

| 2.63 |

| CMS Energy ( CMS ) |

| 2.24 |

| Exelon Corporation ( EXC ) |

| 2.70 |

| Eversource Energy ( ES ) |

| 2.71 |

| Public Service Enterprise Group ( PEG ) |

| 3.23 |

These are the same peer companies that were used in the valuation comparison back in August. As we can see, Exelon and Eversource Energy have not really gotten any cheaper. DTE Energy, CMS Energy, and Public Service Enterprise Group have all gotten substantially cheaper than the price that they previously traded at. Most importantly, DTE Energy now compares much more favorably to its peers. Previously, only Public Service Enterprise Group had a less attractive price-to-earnings growth ratio. Today, CMS Energy is the only company that appears to be somewhat cheaper, and CMS Energy is actually a bit more leveraged.

Thus, DTE Energy appears to be offering a better entry price now than it used to, but its fundamentals have not really changed.

Conclusion

In conclusion, DTE Energy Company is looking much more attractive as an investment than it has in a long while. The company’s valuation has fallen a lot compared to its peers, which may be partly because investors have started to focus more on actual financial performance than on other things. It still retains the characteristics that we appreciate, though, such as a very respectable dividend yield and acceptable earnings growth for a utility. Now may be an opportunity to begin accumulating shares prior to the onset of a recession or other economic turbulence, since DTE Energy appears to be well-positioned to weather such a scenario.

For further details see:

DTE Energy: Valuation Has Improved Compared To Peers, Presenting Opportunity