DCT - Duck Creek Could Offer Stable And Profitable Growth

Summary

- DCT is the second largest provider with strong SaaS capabilities and low-code configurability.

- The business is still growing at double digits during the economic downturn without debt and share dilution.

- The operational efficiency and profitability are improving year after year.

- Huge opportunity for new customer adoption and migration as the industry is at an inflection point towards digitalization.

Duck Creek Technologies, Inc. ( DCT ) offers software platforms with services and products that support insurers in the P&C industry. Similar to Guidewire Software ( GWRE ), DCT has complete insurance product lines covering definitions, distribution, underwriting, policies, and claims. The stock has been crushed since its IPO in 2020. I think DCT has lots of potentials to expand its business and offer profitable growth. As the insurance industry is very resilient to economic downturns, DCT may offer opportunities for long-term returns.

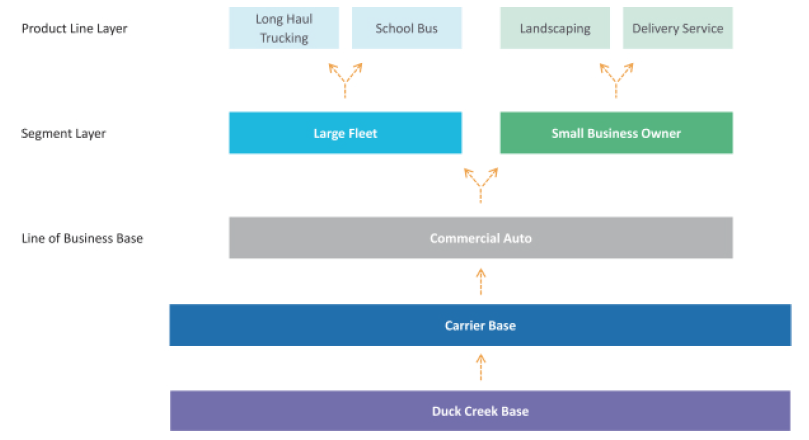

Business and product lines

DCT follows GWRE as the second-largest player and is considered another leader dominating the market. After GWRE and DCT, no real competitors could match their positions given the technology materials and ecosystems built for their insurer customers.

DCT, however, wants to differentiate itself as a provider with stronger SaaS capabilities and low-code configurability. They are the first company to provide cloud solutions. They believe their modern technology architecture is more cohesive, agile, and affordable, as the CEO stated in the fiscal 2022 Q4 conference call :

We're confident that our delivered combination of better business performance and lower operating costs will resonate with customers in all market conditions.

Their inheritance-based development model (as image below) should allow for more consistent and efficient software development and create new product lines and features without reworking. This enables faster innovation cycles.

Duck Creek's inheritance model (Duck Creek 10k)

{kind=link}

Duck Creek's recent business development

For the full fiscal year 2022 , DCT has some headwinds from the slowdown of deal-making during the macro recession. However, the company still manages to grow 16% YOY on total revenue (302.9M) and 23% YOY for subscription revenue only (153M). The percentage of Subscription revenue to total software revenue grew to 78% from 71% in 2020. ARR reaches 169.3M growing 25% YoY while adjusted EBITDA stays positive with 24.2M (43% YOY growth). The management also guided the full-year fiscal 2023 with a total revenue of 328M to 336M.

The CEO has highlighted some significant wins such as Secura, Tokyo Marine, Hollard Insurance, Star insurance, California Fair plan, Franklin Mutual Insurance, Catholic Church Insurance, AXIS Insurance, and Co-action Specialty Insurance. He is also pleased with the Effisoft acquisition in July, which provides world-class product and customer relations in the reinsurance category. It is a very reasonable addition to DCT given lots of immediate cross-sell opportunities.

DCT's growth track record is very stable with lots of hidden strength

Although DCT's IPO is in 2020, the company actually has a long history, founded in 2000. It has been acquired by Accenture in 2011 then Accenture sold its majority stake in DCT to a private equity firm, Apax Partners in 2016. I think this return to independence gives DCT new opportunities for growth. Accenture is also an important partner of DCT moving forward. Now, it has over 150 insurance customers with some of the largest global companies including Progressive, Liberty Mutual, AIG, The Hartford, Berkshire Hathaway Specialty Insurance, GEICO and Munich Re Specialty Insurance while a large portion of carriers both in North America and globally unexploited.

In the last 4 years, DCT management seems to have a very strong focus on profitable and quality growth. It has doubled its sales to 300M+ without significant long-term debt, asset expansions, and share dilutions. Compared to Guidewire, DCT shows strong profitability efficiencies with improving gross margins and decreasing SG&A to Revenue ratio (below). Even after the acquisition of Effisoft, 32.5% of assets are still cash, indicating a strong financial position of the company.

Furthermore, DCT proved its capabilities to build a partner ecosystem with over 80 different companies and 23 SIs (e.g. Accenture). The number of professionals practicing in Duck Creek platforms grew significantly from 700 to 6000 right now since 2016. In other words, DCT is quickly building a network and business scale in recent years.

DCT products are extremely critical for insurers who have to make long-term commitments for adoption, with long sale cycles of 12 to 15 months. Implementing or migrating an IT platform also takes another multi-year process. Therefore, DCT will likely keep its market position for a while given the stickiness of its products.

Market potential and growth opportunities

The P&C and general insurance industry are large, fragmented, and highly regulated with about 2.7T gross written premiums ((DWP)) spanning thousands of carriers globally. DCT's revenue is directly linked or negotiated with DWP. As the industry grows at a CAGR rate of 4.9% , DCT will likely gain along with it. According to the company's estimate , DCT's total addressable market could be 6B in the US and 15B globally, specifically for core system software spending. With only 300M sales, there is still lots of space for DCT to penetrate in. Currently, DCT only has about 30M international sales maximum. Given Guidewire has almost 300M of its sales outside the US, DCT could expand faster in this area after their Effisoft acquisition. In the US, DCT's business is about half the size of Guidewire. I think both companies will continue to penetrate and get most of the shares of the market in the next 10 years because heightened end-user expectations and increased complexities will drive more carriers to outsource their IT solutions.

Valuation

DCT's price/sale ratio is currently at 5.13 which is similar to GWRE (5.93). However, both stocks are at historical lows in terms of valuation. As the future business prospects should clearly be better than right now, I think these evaluation ratios will be elevated once the bull market comes.

Assuming DCT continues its previous growth momentum with a CAGR of 15% for the next five years and 10% CAGR thereafter, we could expect a conservative 1B revenue 10 years from now. If DCT could achieve a 10%-15% profit margin which is similar to other mature IT platform companies (e.g., Accenture), we can expect 0.1B to 0.15B earnings at year 10, which is a PE level of 10 to 15 from the current market cap of 1.5B. For a good scenario, if DCT can grow at 20% for the first five years, then 15% thereafter, and achieve a 20% profit margin, we can expect 0.33B earnings at year 10, in which the current market cap is only valued at 5x PE. It seems that the current DCT price is not ridiculously cheap, while it is not expensive either. Considering the sticky business model, debt-free balance sheet, and buyback potential, it is normal to trade at premiums more than others. I think DCT is a quality company with a long runway ahead, it is worth keeping an eye on it or cumulating a position during the market pessimism.

For further details see:

Duck Creek Could Offer Stable And Profitable Growth