LGDDF - Dufry: Cautiously Optimistic Prospects Likely Baked Into Stock

2023-06-26 21:43:54 ET

Summary

- Dufry AG reports strong Q1 2023 with organic sales up 51.5% YoY, driven by travel industry recovery.

- Near-term prospects are optimistic, but challenges include potential travel spending slowdown and uncertain outcome over AENA concessions.

- Long-term prospects are cautiously optimistic, but competitive risks are not insignificant.

Swiss duty-free retailer Dufry’s ( DUFRY ) near term and longer term prospects are cautiously optimistic. Prospects, however, are likely baked into the stock.

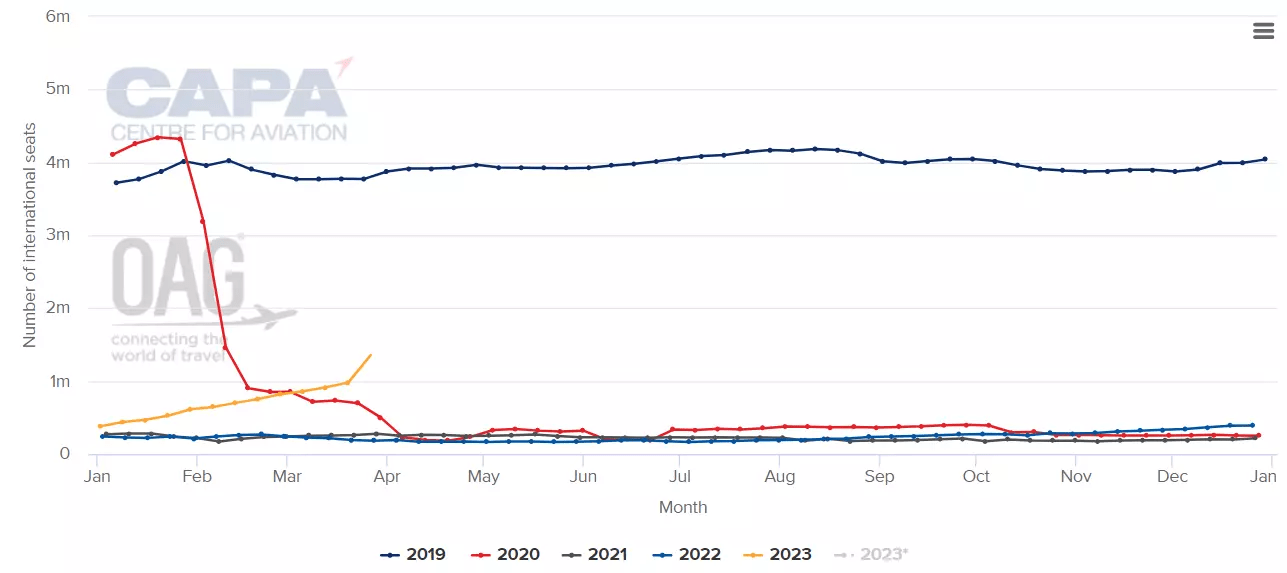

Q1 2023: strong start with organic sales up 51.5% YoY, all regions continue to recover

Dufry reported a solid Q1 2023 (quarter ended March 2023) with organic revenue growth of 51.5% driven by continued recovery in the travel industry. Reported revenues (which includes the revenue contribution from Autogrill, which Dufry acquired last year) rose 113.4% YoY on a constant currency basis to CHF2.4 billion for the quarter.

All regions reported solid growth (both organic and reported). Asia-Pacific was the fastest-growing, albeit from a low base, helped by China’s gradual re-opening.

Dufry AG Q1 2023 news release

Near term prospects are optimistic. Travel demand has already recovered to pre-pandemic levels as of April according to the International Air Travel Association (IATA), but there are still further tailwinds near term. Business travel recovery for instance has continued to lag leisure travel. Business travel may recover to pre-pandemic levels by late 2024 or early 2025 according to Deloitte.

Meanwhile, China, the most important source of international travelers, has yet to see international travel recover to pre-pandemic levels but recovery is underway; China’s international capacity has been rising steadily since January this year and there is plenty more runway for further recovery. Meanwhile, as of last month, international visa applications from China are just about 35% of pre-pandemic levels.

{kind=link}

Looking further ahead, prospects are cautiously optimistic.

Travel demand has tremendous room for growth

Travel demand prospects are positive as incomes rise, particularly in emerging markets like China, and India. Less than 10% of China’s population has passports but penetration is forecast to rise along with growing incomes (Morgan Stanley projects more than 35% of China’s population will achieve upper-middle and high income status by 2030. China is among the top 10 source markets for international travelers to Europe, which along with Middle East and Africa accounts for 45% of Dufry’s net sales.

Over in India, passport penetration is roughly 5% but has enormous potential to increase as the country rises up the rankings as the world’s third biggest economy by 2030. India is among the top 10 most important source markets to the U.S., (currently ranked sixth behind France, Germany and the U.K. according to GlobalData) and their numbers have enormous potential for growth. North America accounts for about a third of Dufry’s net sales.

Dufry investor presentation, Q1 2023

As one of the world’s biggest travel retailers, Dufry AG is already positioned to benefit and the company’s continued expansion efforts should support market share gains. Notable wins and extensions lately include, the extension of three of its duty-free concessions in Spain (which covers most of Spain’s major airports), and new contract wins in Helsinki Airport in Finland, the Chongqing International Airport in China, and the joint venture with Kempegowda International Airport Bengaluru in India among others. Meanwhile, Dufry's Autogrill merger, which marks Dufry’s foray into travel F&B, will enhance Dufry’s economies of scale, and product offering.

Although competition is on the rise, Dufry has scale advantages (as the world’s top travel retailer) which could translate into cost advantages, and supplier relationships with key brands (enabling Dufry to offer travel exclusives, i.e., products exclusive to Dufry’s product catalog) which in turn could better allow Dufry to negotiate concessions and meet airport minimum annual guarantees ((MAG)) that smaller players may struggle to match in the foreseeable future.

Risks

Uncertain outcome over AENA’s remaining two concessions

Of the six concessions on offer by Spanish airport operator AENA, two did not receive any bids and will be rebid . These two are for Spain’s top two airports i.e., in Madrid and Catalonia and it is not clear what the outcome would be, but if Dufry, the current concession-holder fails to extend the contracts, the impact may not be insignificant. AENA (like most airport operators) is showing some resistance to Dufry's market leadership and is looking to break Dufry's near-monopoly position in their airports (the result of this effort seems to be French rival Lagardere winning one of the six AENA concessions, marking the time it enters the Spanish duty free market). Thus, winning the two prized concessions is not likely to be a cakewalk for incumbent Dufry.

Near-term travel slowdown or travel spending slowdown

Post-pandemic “revenge travel” tailwinds could recede , particularly with inflation and elevated interest rates cutting into consumer discretionary spending. Travelers may make adjustments such as opting for domestic travel, reducing international travel, or reducing travel-related spend (on duty-free shopping for instance). Surveys have already revealed softening travel enthusiasm among travelers in the U.S. and Europe . Inflation is particularly stubborn in these regions and any impact to travel demand could affect Dufry who collectively generates 78% of net sales from EMEA (Europe, Middle East & Africa), and North America. Four of the top 10 source countries of inbound travelers to the U.S are Western European countries ( namely UK, Germany, France, and Spain) where inflation is particularly high, while the U.S. is the leading source market for international tourists into Europe so any slowdown in travel from these two regions could impact Dufry.

Competitive risks

Competition is stiff in the travel retail space. In addition to retail operations owned and/or operated by airport operators themselves (such as KIX Duty Free shop which is owned by Kansai International Airport in Japan, or ATU Duty Free which is owned by TAV Airports), the market has no shortage of pure-play travel retailers, the biggest ones of which are well-established players like Dufry AG, French player Lagardere SA ( LGDDF ), and Hong Kong-based LVMH-owned DFS Group.

Competition, however, is increasing. A notable example of an increasingly formidable competitor is travel retail player Lotte Duty Free, owned by South Korean conglomerate (“chaebol”) Lotte Group. This year , Lotte Duty Free snagged the concession contract for Melbourne Airport from Dufry (who had managed the Melbourne Airport duty free shops for 30 years), as part of the former’s efforts to expand into the Oceania market. Lotte Duty Free likely has some competitive advantages over Dufry (for instance in terms of supplier relationships, and cost advantages in terms of logistics and marketing capabilities) thanks to parent company Lotte’s sprawling business empire which includes retailing, hospitality, and food.

Meanwhile in China, Shanghai International Airport (Group) Co., Ltd. announced that it would invest RMB1.7 billion (US$252.5 million) in two duty-free providers to develop its non-aeronautical business, cupping competition in the Chinese duty free space.

Conclusion

Dufry AG has an analysts consensus rating of moderate buy.

WSJ

Dufry is positioned to benefit from near term tailwinds from ongoing recovery in the travel industry and longer term growth prospects in travel demand. However near term growth prospects could be limited by macro challenges and competitive risks are increasing longer term from players with significant competitive advantages. With a GAAP TTM P/E of 64 , much of Dufry’s prospects are likely baked in and could be viewed as a hold.

For further details see:

Dufry: Cautiously Optimistic Prospects Likely Baked Into Stock