DUK - Duke Energy - A 4.5% Yield With Potential For 10% Annual Total Returns

2023-08-10 11:53:47 ET

Summary

- Duke Energy is a stable, low-volatility investment that adds balance and safety to a portfolio.

- The company's dividend growth is slow but steady, with a healthy payout ratio.

- Duke Energy has an ambitious growth plan, aiming for a 10% annual total return through EPS growth and a consistent dividend yield.

Introduction

The Duke Energy Corporation ( DUK ) was one of the first companies I bought when I started my dividend growth portfolio in 2020. I bought the stock because of its attractive yield, anti-cyclical business model, which comes with a wide moat, and the related fact that it would bring some balance to a portfolio that's currently overweight industrial and energy stocks.

It's also one of my most boring investments, and I rarely monitor it.

Currently, the stock yields 4.5% after its stock price lost 18% from its 52-week high.

Given that the company just reported its 2Q23 earnings, I thought the timing was perfect to dive into this utility giant and assess if it still serves the purpose which led me to buy it more than three years ago.

So, let's get to it!

Slow & Steady Wins The Race

I would be lying if I said I hadn't thought about selling Duke Energy a few times in the past three years.

Currently, I'm up 0.7% on my DUK investment, excluding dividends. That's not a lot. As I'm not at a stage where I depend on income from my investments, buying boring yield plays might be a waste of potential profits.

However, instead of selling, I decided to stick to DUK and limit future investments in boring high-yield stocks.

I believe that even younger investors benefit from adding low-volatility, high-yield stocks to their portfolios, as it adds some safety, which tends to improve the overall risk/reward of a portfolio.

The main reason why I stick to some boring investments is because I know that if I only buy stocks I'm passionate about, I'll end up creating a much more volatile portfolio. That was never my goal, so I'm refraining from it.

Also, going back to 2006, Duke Energy has slightly outperformed its utility peers ( XLU ) and the Vanguard High Dividend Yield ETF ( VYM ).

A big part of this outperformance was caused by a less severe sell-off during the Great Financial Crisis. In recent years, DUK has underperformed these two ETFs, albeit not by a wide margin.

To give you another example, a portfolio that consisted 100% of the Vanguard Dividend Growth ETF ( VIG ) has returned 9.24% per year since 2007. The standard deviation was 13.9%. A 90% VIG, 10% DUK portfolio has returned 9.15% per year during this period (9 basis points worse) but with a standard deviation that's almost 70 basis points lower, leading to a higher risk/adjusted return.

It also lowered the market correlation to 94%.

These aren't groundbreaking numbers by any means. However, even small adjustments make a difference on a long-term basis.

Additionally, as long as I pay a wealth tax instead of capital gains taxes, I have to buy some high-yield stocks.

So, while I am actively looking for stocks to replace DUK, I'm not willing to buy more high-yield in the energy sector or any stock that would result in me adding more volatility.

The Dividend

Having said that, the company pays a $4.10 per share per year (quarterly payments) dividend, which translates to a 4.5% yield. It also translates to a 73% payout ratio, which is very healthy in this industry.

However, dividend growth is slow. Over the past five years, the average annual dividend growth rate was 2.5%. The company hiked by 2.0% on July 13, 2023.

For now, it's essentially a high-yielding stock that protects its investors against inflation, assuming the Fed achieves its long-term target of 2.0% inflation, of course. Higher inflation is toxic.

The outlook of lower inflation is the perfect bull case, as it causes investors to rush for high-quality dividend stocks.

On a side note, please note that Duke Energy did not cut its dividend in 2007. Back then, it spun off its gas business, which resulted in a new company called Spectra Energy, which is now a part of Enbridge ( ENB ). Back in 2007, DUK Energy got shares in that company, which offset the lower DUK dividend.

With that in mind, the earnings payout ratio is expected to fall from 73% to 68% using 2024 numbers, as the company is consistently growing its earnings.

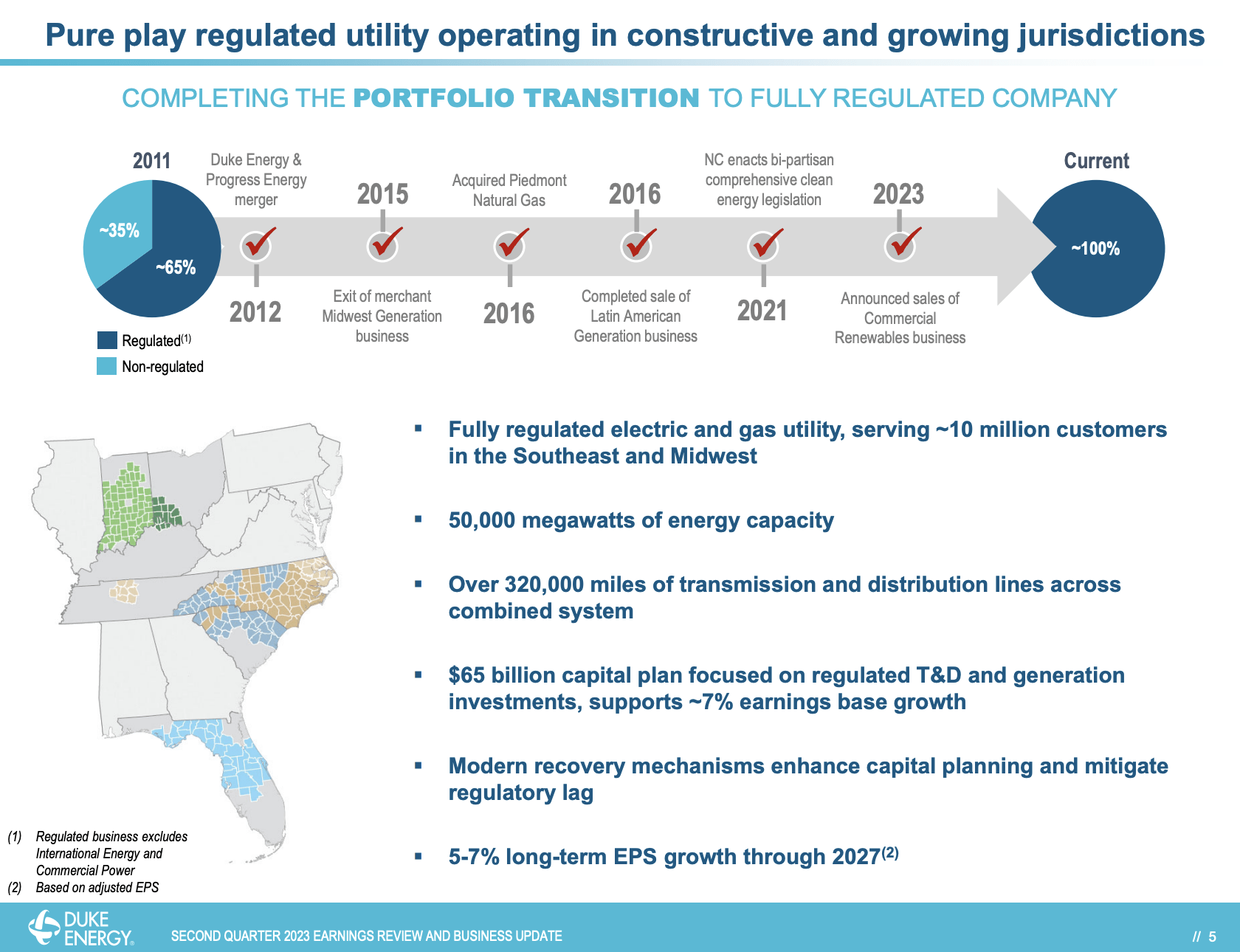

DUK Has An Ambitious Growth Plan

Duke Energy has turned its business into a fully-regulated utility company. As the overview below shows, in 2011, roughly 65% of its business was regulated. That number is now at 100% after the announced sale of its Commercial Renewables business.

{kind=link}

This deal is expected to close by the end of this year.

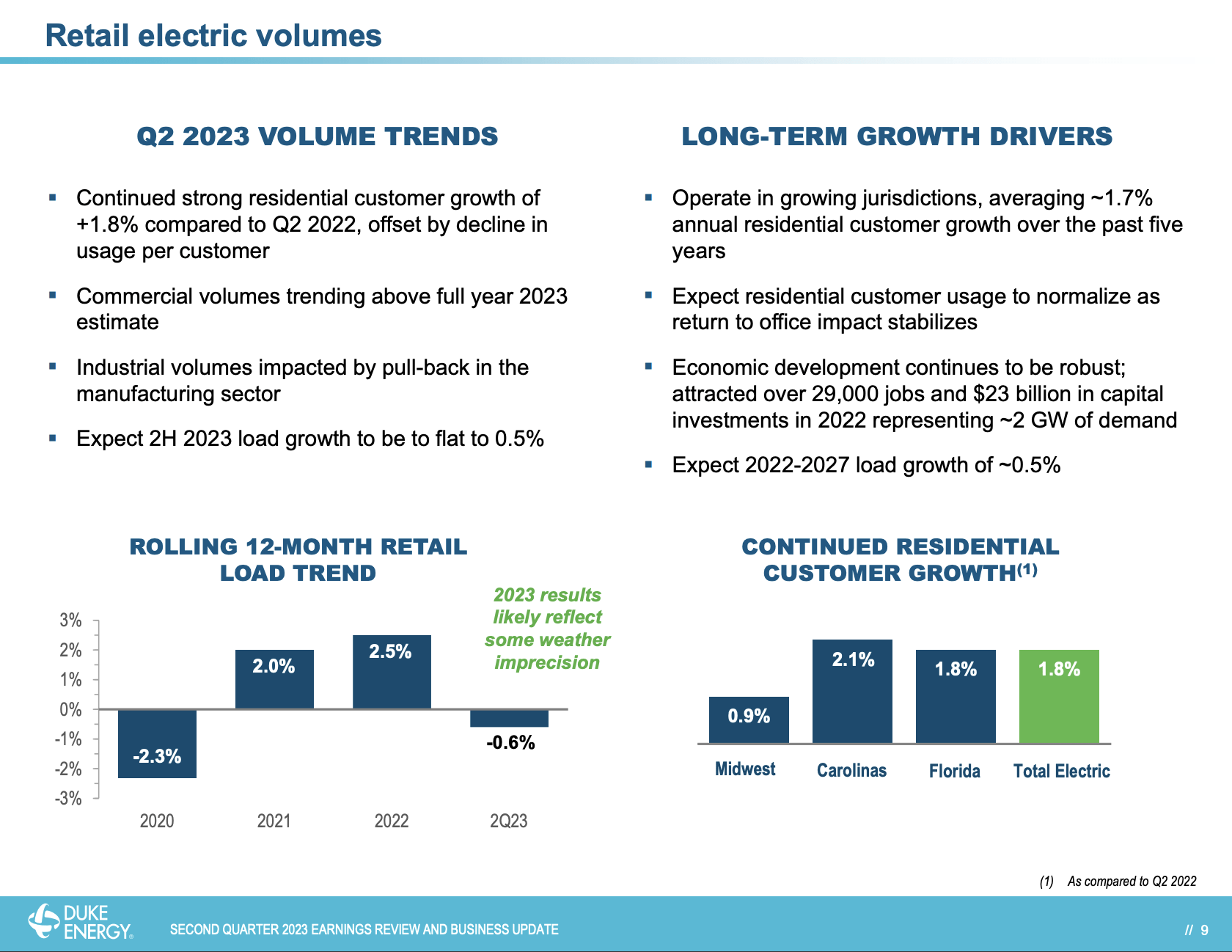

Furthermore, it's interesting that the company sees favorable long-term trends related to secular growth in electricity demand, supported by the energy transition and economic re-shoring.

In its 2Q23 earnings call, the company said that long-term residential growth maintains strength, averaging nearly 1% growth annually over the past five years, exceeding pre-pandemic levels by 4%.

Commercial class volumes also show promising trends above full-year estimates, driven by growth in data centers.

Robust investment in Duke Energy's territories, particularly in batteries, EVs, and semiconductors, is expected to contribute around 2000 megawatts of demand as operations expand.

While some manufacturing customers experienced a slight pullback due to certain economic sectors' softened demand, underlying fundamentals support long-term growth of approximately 0.5% per year.

Again, that's a low number, but for utility companies, that's a very decent increase.

{kind=link}

Additionally, the company affirmed its full-year guidance after dealing with headwinds in its second quarter, including mild weather, which the company mitigated by reducing costs through measures that are expected to come with lasting benefits.

For the second quarter in a row, mild weather impacted results . For perspective in the Carolinas, January and February were the mildest in the last 30 years and May and June were in the top five. Through June, we're facing a weather headwind of nearly $0.30.

Agility measures have been put in place, which add to the $300 million O&M reduction that was targeted and in place coming into 2023 . Our cost initiatives are grounded in our culture of safety and serving our customers with excellence while maintaining our assets for the future. Brian will provide more on cost management in a moment.

We've had an early look at July, and as you would expect, July weather is positive and consistent with the trend across the U.S. and August and September are in front of us. With our largest quarter ahead, we are reaffirming our guidance range for 2023 [...] - DUK 2Q23 Earnings Call

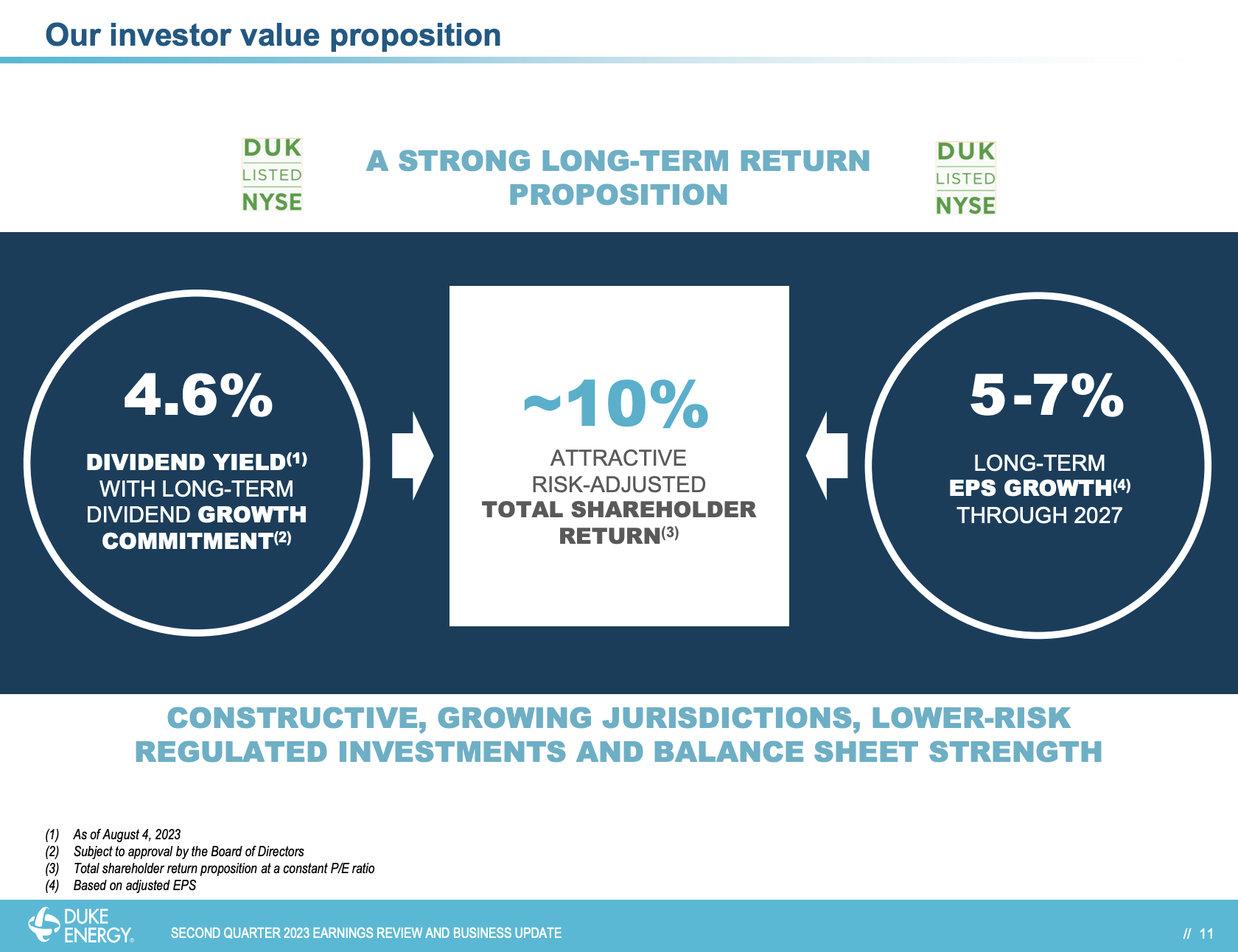

Even more important is that the company stuck to its longer-term outlook, which is a big part of its long-term total return proposition.

Essentially, DUK aims to let shareholders benefit from a 10% annual total return, consisting of its 4.6% yield and 5-7% annual EPS growth through 2027. Note that this excludes a higher valuation. If investors, for various reasons, would apply a higher multiple, the company could return more than 10% per year - assuming it achieves 5-7% annual EPS growth.

{kind=link}

According to the company:

With our portfolio repositioning complete , we offer an attractive fully regulated organic growth proposition. We have a clear strategy ahead of us as we invest to satisfy increasing demand for clean, affordable, and reliable energy across our growing regions. Our long-term fundamentals remain as strong as ever , and we're well-positioned to deliver sustainable value and 5% to 7% earnings growth over the next five years .

With that said, 5-7% average annual EPS growth also shows that the balance sheet is in a good spot, despite rising net debt.

Balance Sheet & Valuation

Because of aggressive investments in renewables and existing infrastructure, the company is not generating positive free cash flow. In 2021, the company had $67 billion in net debt. That number is expected to rise to $86 billion in 2025.

However, thanks to solid long-term growth and the related fact that debt is spent on value-adding projects, the net leverage ratio has declined from 6.2x EBITDA in 2021 to 5.8x 2023E EBITDA.

This company's credit rating is BBB+, which is one step below the A-range.

With regard to its valuation, DUK is trading at 11.4x 2024E EBITDA. This is based on a $155.3 billion enterprise value, consisting of its $71.5 billion market cap, $80.3 billion in expected net debt, $2.7 billion in minority interest, and $800 million in pension liabilities.

This valuation is fair but not a no-brainer, as potentially sticky inflation and prolonged elevated rates are toxic for companies with high gross debt loads - even if the balance sheet in itself is healthy.

Hence, when markets started to price in a more hawkish outlook for Fed Funds rates, the stock quickly fell from $95 to $90.

FINVIZ

The current target price is $104, which is 12% above the current price.

I agree with that target and will maintain a buy rating.

However, I do not expect significant stock price potential above that target, at least not until we get more certainty that inflation is likely to remain subdued.

Hence, I would only add on weakness, as the company's yield is the core of the bull case.

The 10% annual total return is still possible, but I believe it will be unlocked in a more favorable interest rate environment, which means it may take 1-2 years until DUK is able to take off.

Takeaway

So far, my journey with Duke Energy has been a lesson in patience. Despite its somewhat boring business, DUK's stable performance and reliable dividends have played a crucial role in diversifying my portfolio.

DUK's transition to a fully-regulated utility business aligns with long-term trends, and its ambitious growth plan reflects a commitment to sustainable value.

The company's growth plan and projected 5-7% EPS growth through 2027 further solidify its position. A fair valuation and a robust credit rating add to its appeal.

So, I'll hold onto this steady earner, capitalizing on its core strength: a consistent dividend yield.

For further details see:

Duke Energy - A 4.5% Yield With Potential For 10% Annual Total Returns