DUK - Duke Energy Is A Solid Long-Term Investment

2023-06-25 08:16:17 ET

Summary

- Duke Energy is a solid utility company with steady EPS and sales growth, fueling a sustainable 3% dividend growth.

- The company has growth prospects around its investments, especially as the shift toward electric vehicles will be positive.

- Despite risks such as increased debt load and decimated free cash flow, the company is fairly valued and enjoys a monopolistic market position, making it a BUY for income and dividend growth investors.

Introduction

As a dividend growth investor, I constantly seek new ways to invest in income-generating assets. I frequently add to my existing positions if I believe they are undervalued. I also take advantage of market volatility by establishing new positions to diversify my portfolio and increase my dividend income with less capital.

The utility sector is becoming interesting due to rising rates. As interest rates increase, the value of dividend growth companies decreases as investors have other safer income-producing assets. Utilities are among the "bond-like" companies, and when risk-free interest is above 4%, they will eventually have to yield similarly. Therefore, investors can buy utilities and enjoy higher initial yield and future growth. Duke Energy ( DUK ) is an interesting utility stock because it has a strong track record of dividend growth.

I will analyze Duke Energy using my methodology for analyzing dividend growth stocks. I am using the same method to make it easier to compare researched companies. I will examine the company's fundamentals, valuation, growth opportunities, and risks. I will then try to determine if it's a good investment.

Seeking Alpha's company overview shows that:

Duke Energy Corporation operates as an energy company in the United States. It operates through two segments, Electric Utilities and Infrastructure (EU&I) and Gas Utilities and Infrastructure (GU&I). The EU&I segment generates, transmits, distributes, and sells electricity in the Carolinas, Florida, and the Midwest and uses coal, hydroelectric, natural gas, oil, solar and wind sources, renewables, and nuclear fuel to generate electricity. The GU&I segment distributes natural gas to residential, commercial, industrial, and power generation natural gas customers and invests in pipeline transmission projects, renewable natural gas projects, and natural gas storage facilities.

Fundamentals

The revenues of Duke Energy have increased by almost 30% over the last decade. It equates to roughly 2% annually. Utility companies tend to grow slowly as the regulators limit their tariffs. They grow sales as the demand for electricity and gas grows, and the population grows. The tariff increases allow the company to keep growing sales and invest in its infrastructure. In the future, as seen on Seeking Alpha, the analyst consensus expects Duke Energy to keep growing sales at an annual rate of ~2% in the medium term.

The EPS (earnings per share) grew by 12% over the last decade using GAAP earnings and 22% when using non-GAAP EPS. The slower EPS growth is due to higher costs that led to lower margins and the fact that the company is issuing shares to fund its growth. The company invests heavily in its infrastructure, and while it serves as an opportunity, it's a burden in the short term. The company aims to achieve an EPS growth of 5%-7% annually in the medium term, according to its Q1 2023 presentation . In the future, as seen on Seeking Alpha, the analyst consensus expects Duke Energy to keep growing EPS at an annual rate of ~6% in the medium term.

The company's dividend has been growing for the last fifteen years. The growth rate has been slow at 3% annually over the previous five years. The current dividend yield is 4.5%, yet the payout ratio is 125%, which seems risky. However, this is the payout based on the company's GAAP earnings. Using non-GAAP EPS, the company's payout ratio stands at 75%. This is a high figure but manageable for a utility company. As we advance, I believe 3% increases will likely increase as the company grows the EPS faster to slightly lower the payout ratio.

In addition to the dividends, companies tend to return capital to shareholders via buybacks. Buybacks support EPS growth as they decrease the number of shares outstanding. Duke Energy doesn't buy back its shares. It returns capital via a high dividend payout. Therefore, the number of shares increased by close to 10% in the past decade. Duke Energy issues shares to raise capital for projects and to compensate employees.

Valuation

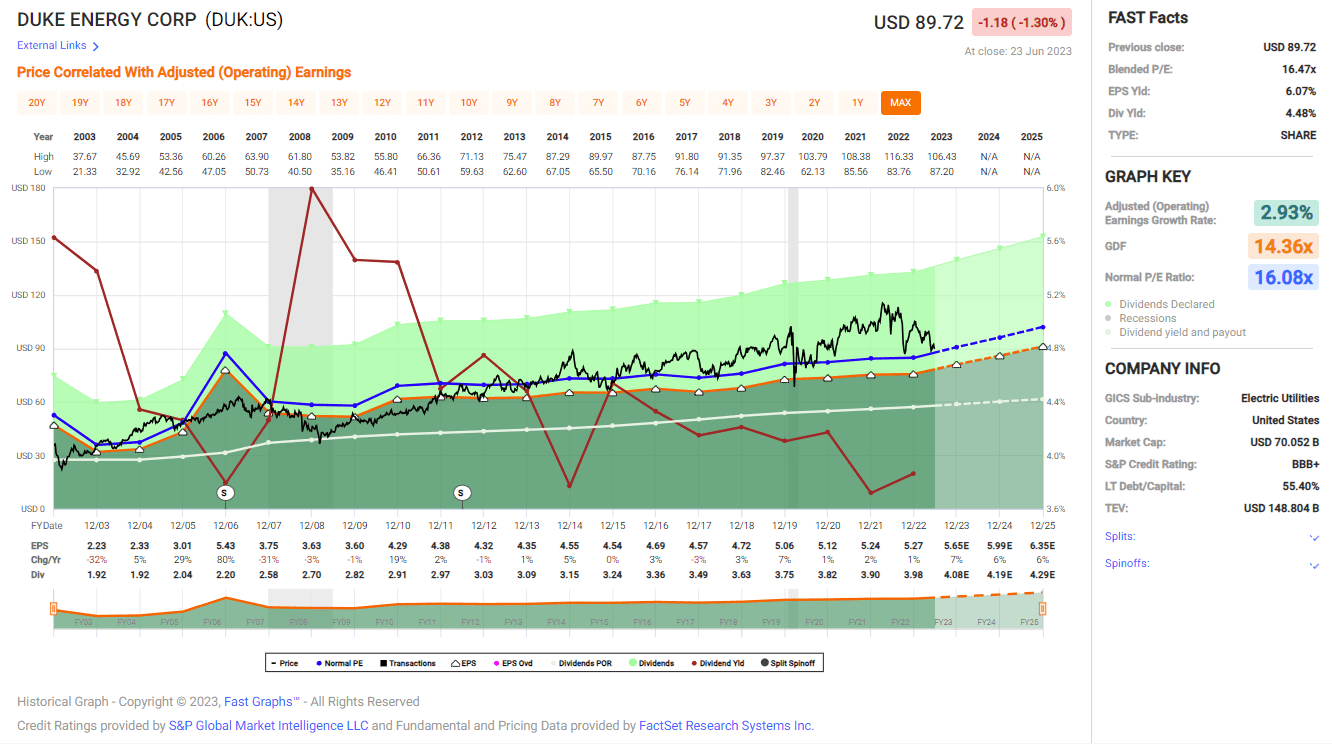

The P/E (price to earnings) ratio of Duke Energy stands at 16 when using the 2023 EPS forecast. This is the lowest valuation we have seen over the last twelve months, as the P/E ratio was over 20 ten months ago. The current valuation seems fair as the company intends to grow its EPS by roughly 6% annually, and its sales and income are relatively predictable due to the fact that it is a regulated regional monopoly.

The graph below from Fast Graphs shows that the company is fairly valued. The EPS grew at a CAGR of 3% over the last two decades, while the P/E ratio was 16. Today we see a similar valuation and a forecast for an even greater growth rate. Yet, skepticism is in place since it is a forecasted growth rate that is double the historical growth rate. Therefore, I believe that shares are reasonably valued, with room for capital appreciation as the company grows according to its plan.

{kind=link}

Opportunities

The demographics are a broad growth opportunity for the company. Even if people do not consume more electricity and natural gas, having more people in your service area will profoundly impact your growth. The company expects the number of consumers to grow at an annual pace of 1.7%. This is the result of the service area, as seen below. The company is mainly active in southern markets, which enjoy a growth in immigration within the United States.

Duke Energy

Transformation of the energy mix is another growth opportunity. The demand for clean and reliable energy requires utility companies to build new power plants. These plants will use natural gas and renewable energy such as solar, hydro, and wind. These are massive investments that Duke Energy will make to achieve its 2030 goal, as outlined below. The regulator compensates Duke for its investments, and therefore, this change is a positive long-term event, as it will lower pollution and support the company's sales growth.

Duke Energy

Another important opportunity is the company's transmission and distribution network investment. The company will invest $36B in that system in four years. It will allow the company to improve the automation of the system, thus saving capital. More importantly, it will increase the capacity of the network. It is crucial as vehicles shift to electricity, increasing demand for Duke Energy. The company is improving its network to support the growing demand for electricity instead of gas.

Duke Energy

Risks

The first risk for the company is that it lacks free cash flow. Yes, it is profitable and invests in its future in electricity generation, transmission, and distribution. Yet this investment will only come to fruition in the future. In the meantime, the company is burning as it awaits its projects to go online. Delays in these projects and lower-than-anticipated demand might hurt the company's EPS and FCF while it will still have to pay for these investments.

The debt burden is another risk for Duke Energy. The company's debt to EBITDA ratio is above 5 and has two negative effects. It decreases the company's EPS as the interest expense grows, especially with higher rates. in addition, it also limits the company's ability to keep investing as the debt burden is high, and its only other option is raising capital by share issuance, which dilutes shareholders and thus decreases the EPS.

The combination of inflation and a regulated utility is also a short- and medium-term risk. Inflation increases the costs for Duke Energy by raising wages and the price of materials needed, such as coal and natural gas. The company has to get regulators to approve price increases, and as inflation hurts the public, regulators are reluctant to increase prices. Therefore, they may try to delay price increases for as long as they can, which will hurt the margins of Duke Energy and its peers.

Conclusions

To conclude, Duke Energy is a solid utility company making a massive investment in its infrastructure to grow its business into a more robust and clean utility. The EPS and sales are growing steadily, fueling a 3% dividend growth that looks sustainable. The company has several growth prospects around its investments, as the shift toward electric vehicles will be positive.

The company is dealing with the risks around its investments as they increased the debt load and decimated the free cash flow. Still, the company is trading for a fair value and enjoys a monopolistic market position. Therefore, I believe it can handle the risks. Investors should expect a 4.5% dividend yield with roughly a 6% EPS increase for a total return of ~10%. Therefore, I rate the company a BUY for income and dividend growth investors.

For further details see:

Duke Energy Is A Solid Long-Term Investment