DUK - Duke Energy's Stock Valuation Is Not Attractive

2023-12-13 16:38:06 ET

Summary

- Duke Energy stock has underperformed and experienced deeper drawdowns compared to other investments.

- Investors may be holding onto Duke Energy stock due to assumptions about the safety of utilities and focus on dividend yield.

- The dividend time until payback analysis suggests it would take about 19-24 years to earn back the initial investment in Duke Energy stock through dividends.

Introduction

Investors have been very bullish on Duke Energy ( DUK ) stock for most of the past decade. In fact, there hasn't been a single "Sell" rated article on Seeking Alpha published since 2015. I found this very surprising since I see very little reason to own Duke Energy stock. Below is the total return performance of the stock since 2015 compared to inflation, the S&P 500 ETF ( SPY ), and Berkshire Hathaway ( BRK.B ):

There is no point during this period when Duke Energy stock was a good relative buy, and it has only produced a real annual return of +2.79% during this time. Not only has Duke underperformed, but it also hasn't been any more defensive during drawdowns as we see in the drawdown chart below:

So, Duke has been shown to produce poor average returns over this time frame while generally experiencing deeper drawdowns, yet after 100+ articles, nobody has considered selling it.

This begs the question, why not?

I think there are two answers to this question. One explanation is a confluence of investors simply not looking at the data and assuming utilities are "safer" when they aren't, along with investors focusing on the dividend yield rather than the likely future total return of the investment.

I think two potential arguments can be made against what I've shared so far. One is that while Duke might have been overvalued in the past, because of recent price declines, the valuation may be attractive now. The second argument is that while total returns for Duke have been poor, it is attractive because of its steady dividend payments and higher-than-average yield, currently about +4.32%.

I see no reason to think Duke Energy stock will produce more than the same 2% to 3% real CAGR long-term than it has been producing. I generally aim for double or triple that return for my equity investments. So, it's clear on its face without doing much additional work that Duke is too overvalued to own at today's prices for investors who want average or above-average total returns. But, it might not be quite as clear from strictly a dividend perspective, which is why I suspect the investors who do own Duke are long the stock to begin with. So, in this article, I will forgo the earnings-based total return valuation I usually share and instead focus on the dividend and dividend growth potential.

Dividend Time Until Payback Analysis

The idea behind the dividend time until payback analysis is very simple. We want to take the current dividend yield and the expected dividend growth and project them into the future to estimate how long it would take us to earn an amount equal to our initial investment in a stock via only collecting dividends. For example, if you pay $100 for a stock, you are estimating how long it will likely take to earn $100 in dividends back from that stock. To do that, I will look at the historical trend and extrapolate it out into the future rather than speculate on what the future dividend growth might be.

{kind=link}

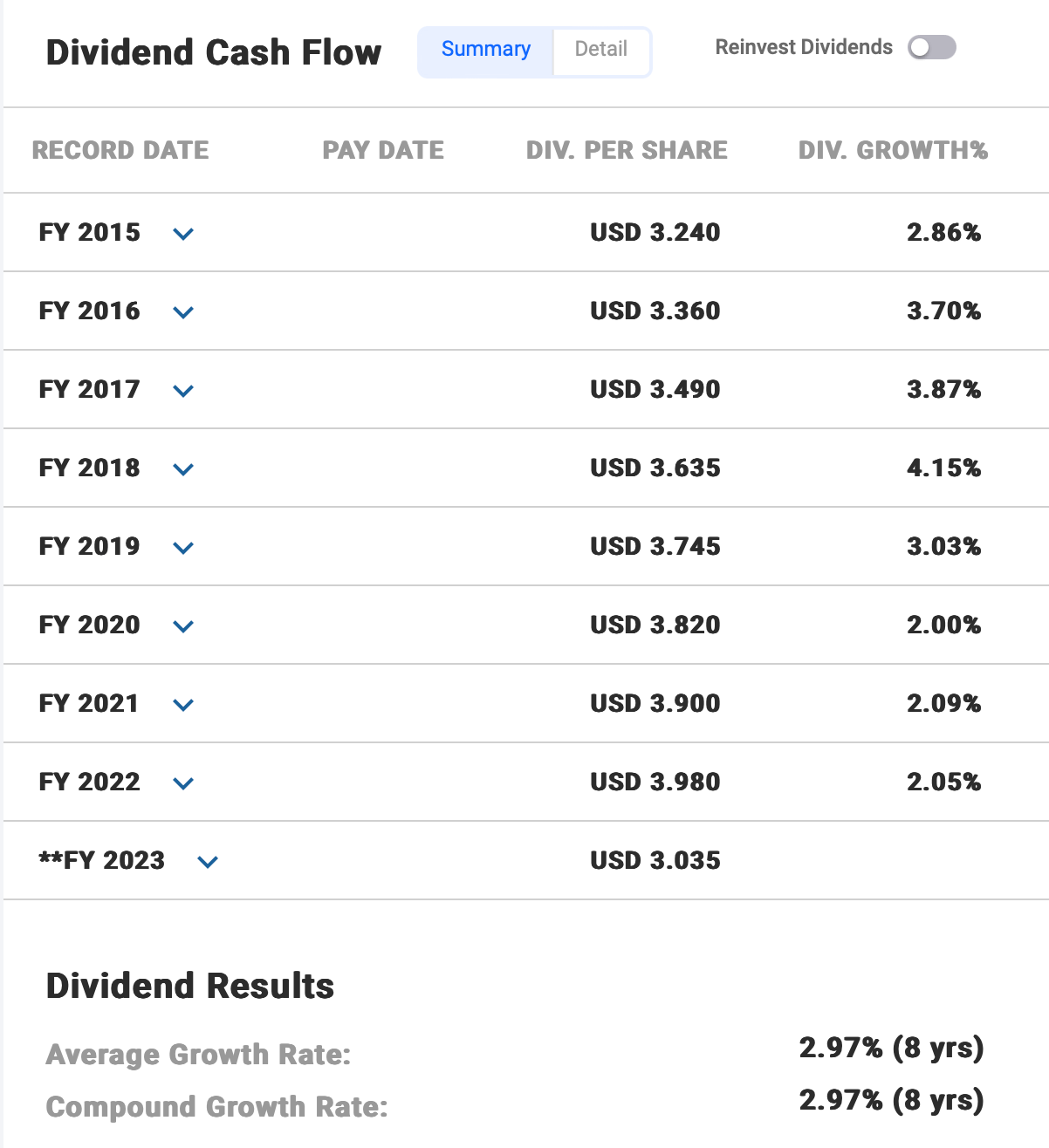

The FAST Graph data above shows Duke's dividend growth rate over this period has been about 2.97% per year. (About the same as the 3.03% inflation rate.) The payout ratio over this time has grown from 71% to about 75%, which means if this current trend continues over the long term the 2.97% growth rate is unsustainable. This is because the earnings growth rate during this time period has been about 2.09% annually. When I have a situation with a dividend stock that has a payout ratio over 50% and earnings growth is not keeping up with the dividend growth, I use the lower of the two growth rates to estimate the very long-term dividend growth rate. So, for this valuation, I will assume that DUK can grow its dividend at a 2.09% rate indefinitely.

The way I like to think about this is if I bought $100 in DUK stock with a 4.32% yield, the stock would pay me back $4.32 the first year without any growth, and if I pull that first year's growth forward it would pay me $4.41. I would collect that $4.41 and next year's payout would be $4.50. So after two years, I would have earned $8.91 via the dividend payouts. I want to know how many years it would take to collect $100, which is an amount equal to my initial $100 investment.

By my calculations, using this method, it would take about 19 years to earn my money back from dividends investing in DUK stock at today's prices. It's probably also worth keeping in mind that this does not include inflation. If the Fed meets its goal of a 2% long-term inflation rate, that is the same as DUK's earnings growth (and historically Duke's dividend growth has equaled inflation). This means in order to estimate how long it would take to earn one's money back via the dividend in real terms, we should assume the dividend rate does not grow. The 4.32% yield you get now is what you get each year in real terms. When I make that adjustment to the estimates, it will take about 24 years for an investor to earn an amount equal to their initial investment via the dividend.

I don't find this rate of payback attractive. However, I always try to examine a stock from as many angles as possible. On a relative basis, compared to a 60/40 style ETF like iShares Core Growth Allocation ETF ( AOR ) which only yields 2.17% right now, and has a 21-year time until payback without adjusting for inflation and a 24-year time until payback assuming 2% inflation, Duke's valuation looks similar. So, on a relative basis, if we assume a standard 60/40 is the best comparison, Duke is valued about the same in that regard.

Conclusion

I think what we see with Duke Energy is just another example of how overvalued reliable dividend-paying stocks are. Retirees would be much better off buying Berkshire Hathaway than Duke Energy and pulling the 4.32% from Berkshire at the beginning of each year. Here is how that strategy would have performed from 2015 through today, taking $432 each year inflation-adjusted from $10,000.

{kind=link}

An investor easily could have created their own dividend, which is equal to Duke's, with Berkshire and done very well. Usually, Berkshire grows about 8% per year on average plus inflation and it's a far safer investment than Duke Energy and a much better grower of wealth.

Sometimes when certain strategies become popular, as dividend investing is right now, investors have to use alternative strategies that are less popular, but more effective if they want to get good returns. Berkshire isn't super cheap right now, but it's also not super expensive like most utility stocks. It makes sense to sell Duke Energy and buy Berkshire and create your own dividend while growing your wealth over time. Berkshire's value should double in half the time Duke Energy does, even while selling enough shares each year to create an equal dividend.

For further details see:

Duke Energy's Stock Valuation Is Not Attractive