DUK - Duke Energy: Slow But Stable Growth

2023-09-20 13:44:07 ET

Summary

- Duke Energy's stock is undervalued compared to its peers and offers a 4.3% dividend yield, which is very healthy in the utility industry.

- Duke Energy’s debt-to-EBITDA in TTM is 5.4x, which is almost the highest among its peers.

- The company is operating in regions with a growing population thus higher customer demand is expected in the following years.

Introduction

Duke Energy ( DUK ) is a prominent energy provider headquartered in North Carolina and has turned towards becoming 100% regulated by the FERC and other regulatory agencies. The company includes two separate reportable segments: Electric Utilities and Infrastructure (EU&I) and Gas Utilities and Infrastructure (GU&I). The EU&I sector provides retail electricity services like generation, transmission, distribution, and sale of electricity to circa 8.2 million people in the Southeast and the Midwest of the U.S. In addition, GU&I is responsible for distributing natural gas to retail customers through North and South Carolina, Tennessee, Ohio, and Kentucky regions. In this thorough analysis, I investigate Duke Energy's financials and business outlooks to provide insights related to the company's growth path.

Duke Energy's business outlook

Duke Energy has one of the most diversified operating systems in this industry, which helps the company mitigate its operational risks while generating diversified profits. In doing so, they have plans to reduce 50% of their carbon emission by 2030, 80% by 2040, and net-zero emissions by 2050. Furthermore, the management set a goal to decline the portion of coal to less than 5% of their total generation by 2030 and a full exit by 2035. It is worth noting that they cannot achieve their carbon-free target without nuclear energy, which consists of approximately 80% of their generated carbon-free energy. Moreover, they made progress with the U.S. Department of Energy (DOE) to identify credit opportunities by their progression in renewable energy platforms. For instance, the company completed its $1 billion program to generate 700 megawatts of solar commitment in Florida in 2022, and it plans to spend more than $1 billion on the Clean Energy Connection program for another 750 megawatts by the end of 2024.

The management reaffirmed their guidance to a 5-7% earnings growth rate. Also, it is worth mentioning that Duke Energy has announced it will become a fully regulated company by the end of this year, thereby driving its growth during the coming years by investing in clean energy. In this regard, they have a long-term goal to become the largest energy transition company in this industry. What is clear about Duke Energy's pursuit path is that the company's transition to a fully regulated company coupled with its ambitious growth plan, provides a reliable and sustainable value in the future, notwithstanding being slow-paced. In this regard, the management commented :

"Later this year, we will begin the CPCN Process in North Carolina for replacement gas generation. At the same time, solar procurement will continue on an annual basis. In fact, our 2022 solar procurement was recently finalized, with nearly 1000 megawatts to be placed in service by 2027. And our 2023 Solar RFP targeting 1,400 megawatts was recently approved by the NCUC, with bids to be received later this year."

Duke Energy's financial outlook

The nature of utility companies is to have high net debt levels due to their high capital spending and infrastructure investments. Regarding Duke Energy's balance sheet strength, it is worth highlighting that the management is willing to recover circa $1.7 billion of deferred fuel costs by the end of 2023. Therefore, expect their deferred fuel balance to reach the historical average by the end of 2024. As a result, management predicts to see more strength in their balance sheet by next year. As it is demonstrated in Figure 1, Duke Energy's debt-to-EBITDA in TTM is 5.4x, which is almost the highest among its peers after Southern's ( SO ) 5.6x.

Figure 1 - DUK's debt-to-EBITDA vs. peers.

{kind=link}

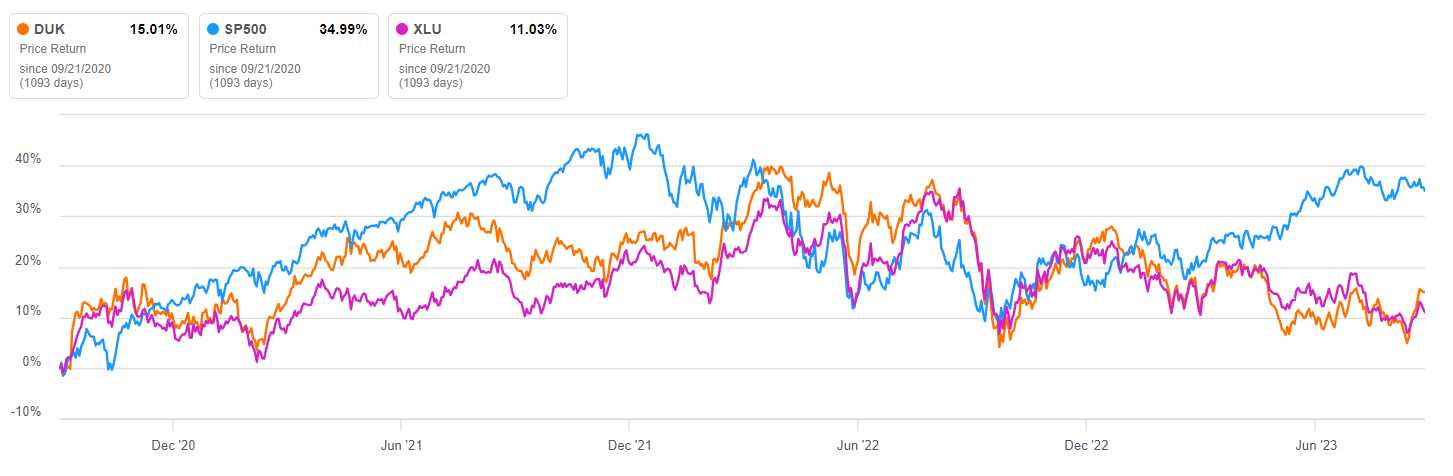

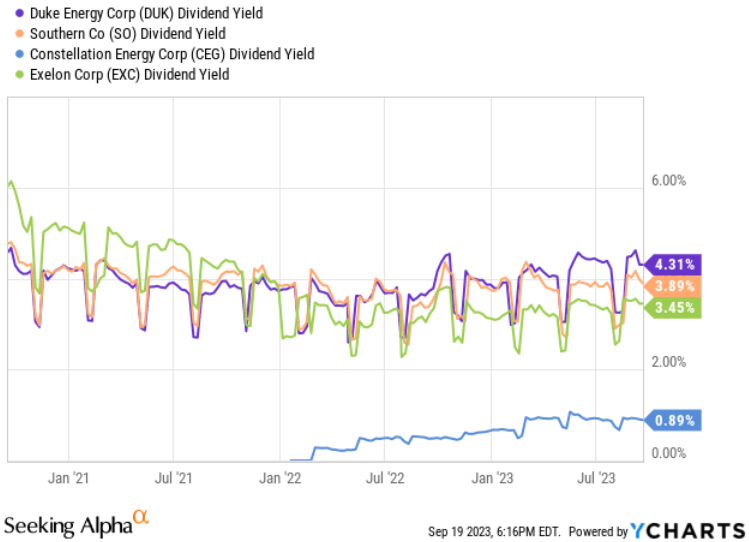

Also, comparing Duke Energy's return during the recent years with the S&P 500 index and its utility peers ( XLU ) indicates that the company has underperformed the S&P 500 while being almost on the same line as its utility peers (Figure 2). In addition, it is worth mentioning that DUK provides a very healthy level of 4.3% dividend yield, which is the highest level among its peers (see Figure 3).

Figure 2-

{kind=link}

Figure 3 -

{kind=link}

Duke Energy's stock valuation

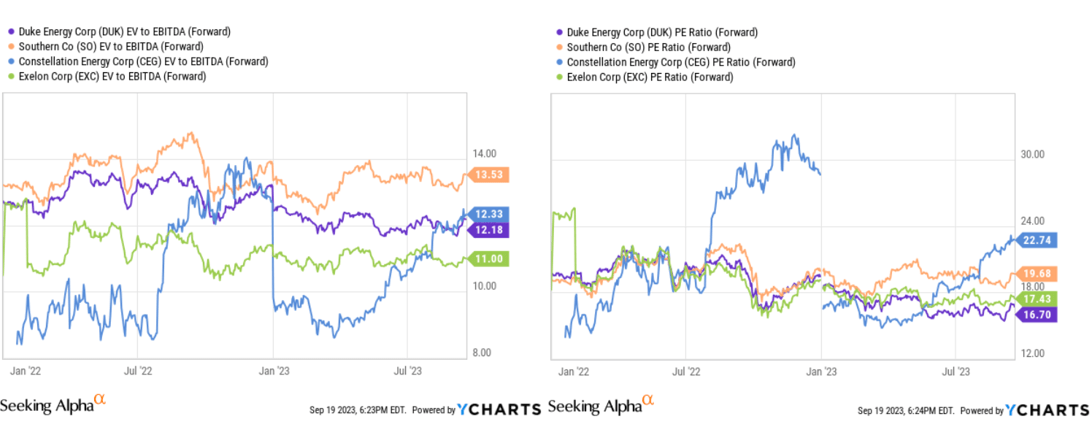

DUK's forward valuation metrics indicate that the company's performance is healthy and undervalued versus its peers. In minutiae, after Exelon's ( EXC ) forwarded EV-to-EBITDA of 11x, DUK has the lowest record of 12x. Moreover, the company's forwarded PE ratio is at the lowest level of 16.7x in comparison with its peers, while Constellation Energy ( CEG ) hit the highest level of 22.7x (see Figure 4). Overall, although Duke Energy is a company with small dividend growth and thus is not an investment to protect us in the current high inflation era, its valuation metrics indicate that the company is undervalued in comparison with its peers.

Figure 4 - DUK's valuation metrics vs. its peers

{kind=link}

Conclusion

Duke Energy is operating in regions with a growing population thus, the management expects higher customer demand in the following years. Moreover, taking advantage of IRA tax credits has empowered the company to provide lower costs for customers, and additional federal funding will cater to opportunities to advance new resources and stimulate economic development. Overall, in comparison to its peers, DUK is providing the highest dividend yield of 4.3%, which is very healthy in the utility industry, while it has been undervalued versus its peers. When all is said and done, I believe a buy rating is appropriate for DUK stock.

For further details see:

Duke Energy: Slow But Stable Growth