DUK - Duke Energy: Watch This 4%-Yielding Dividend Stock

2024-01-17 07:30:00 ET

Summary

- Shares of Duke Energy have shed 6% of their value in the last 12 months.

- The electric utility's total operating revenue and adjusted EPS climbed higher in the third quarter.

- Duke Energy enjoys a BBB+ credit rating from S&P on a stable outlook.

- Shares of the utility appear to be fair valued.

- Duke Energy could be poised to modestly outperform the market in the coming 10 years.

The interest rate-hike cycle that has persisted for nearly two years now (except for the last several months) has had many implications throughout the stock market.

{kind=link}

Higher-yielding, risk-averse economic sectors have fallen by double-digits. When investors can attain equal or greater income from lower-risk options, this isn't a surprise.

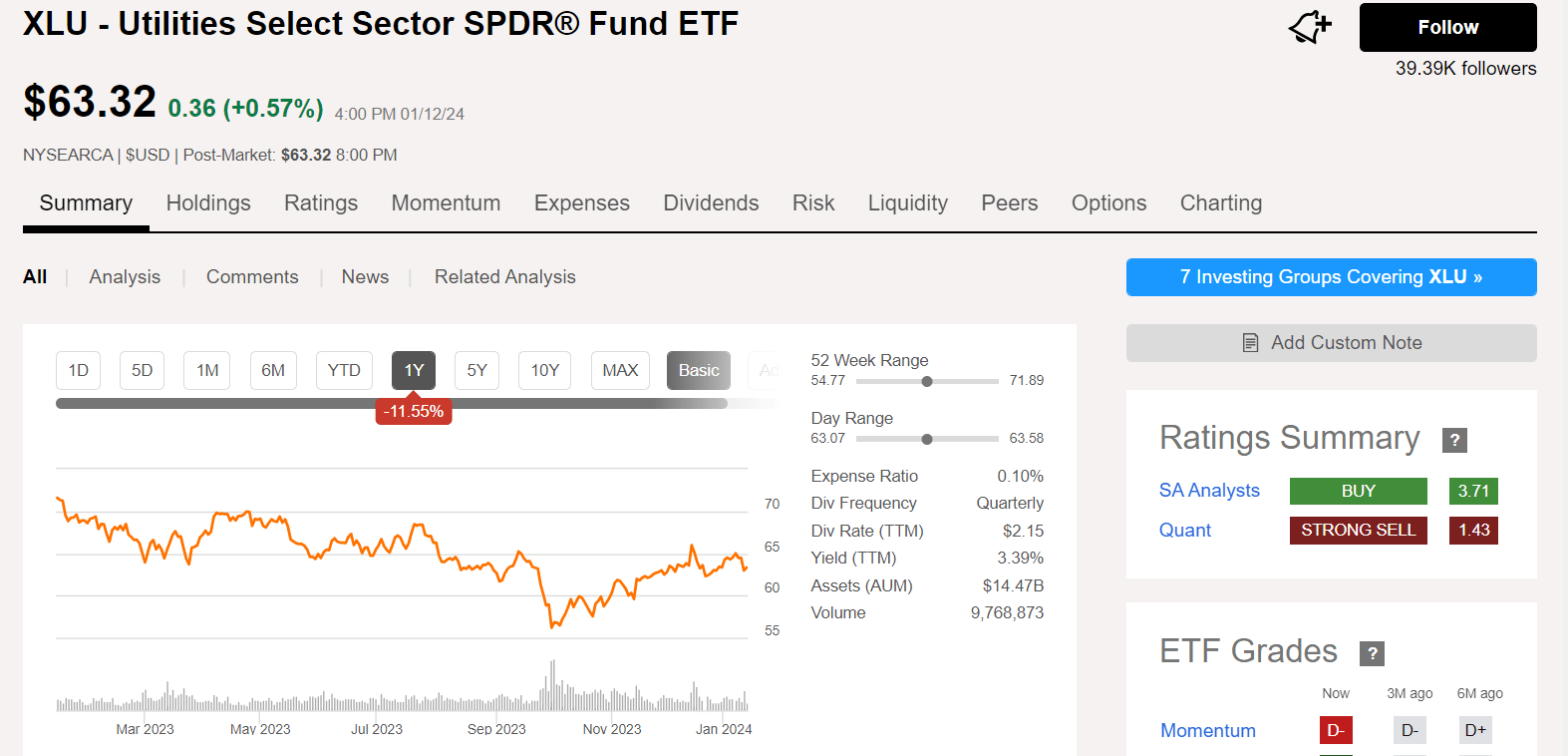

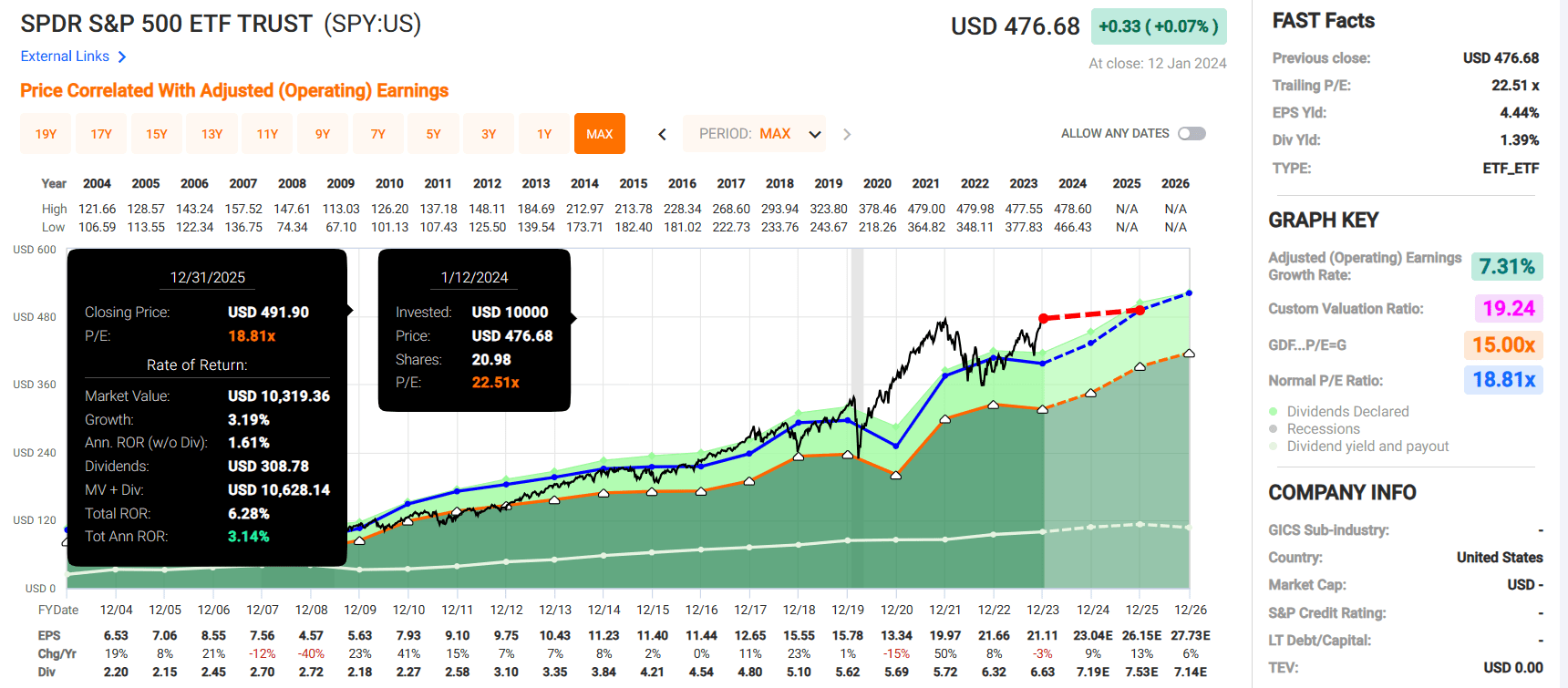

Predictably, the Utilities Select Sector SPDR Fund ETF ( XLU ) has dipped by 12% in the last year. Utilities have been negatively impacted by competition from higher-yielding investment vehicles that are perceived to be lower risk (e.g., treasuries and high-yield savings accounts) for one. Not to mention, higher interest rates have weighed on the profitability of the sector as utilities are more capex-heavy and leveraged relative to other sectors.

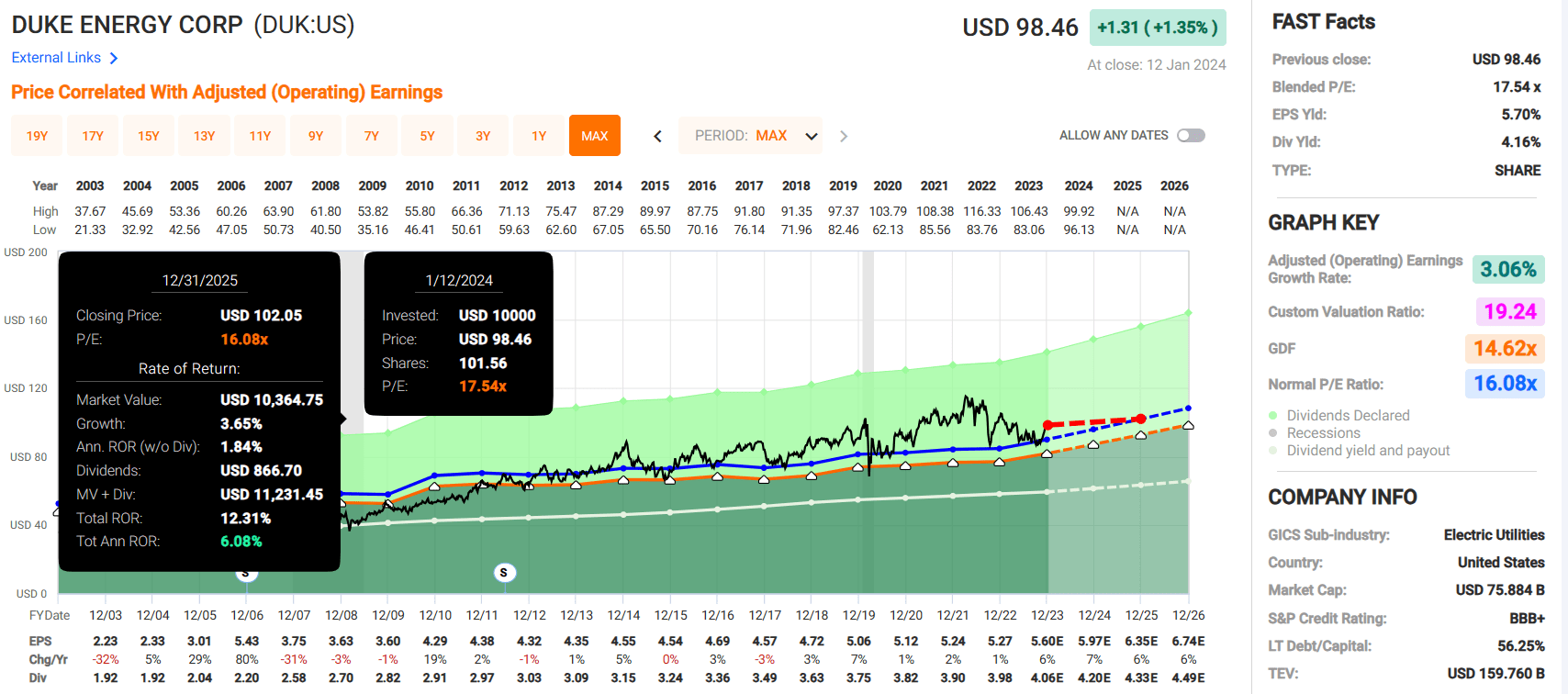

Duke Energy ( DUK ) is the third-biggest holding within XLU, comprising just over 8% of its total weighting. Shares of the electric utility have moved 6% lower in the past 12 months. Today, I will revisit Duke Energy's fundamentals and valuation for the first time since July 2019 to articulate why I'm maintaining my hold rating for now.

{kind=link}

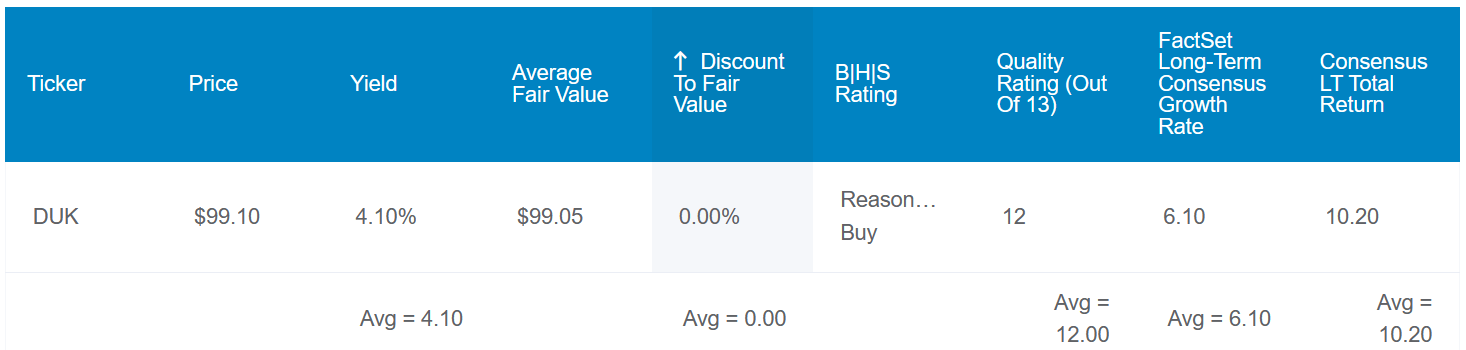

Duke Energy's 4.2% dividend yield is well above the 1.5% yield of the S&P 500 ( SP500 ). It's also a bit higher than the 4% yield of the 10-year U.S. Treasury. This payout also appears to be built on a firm foundation.

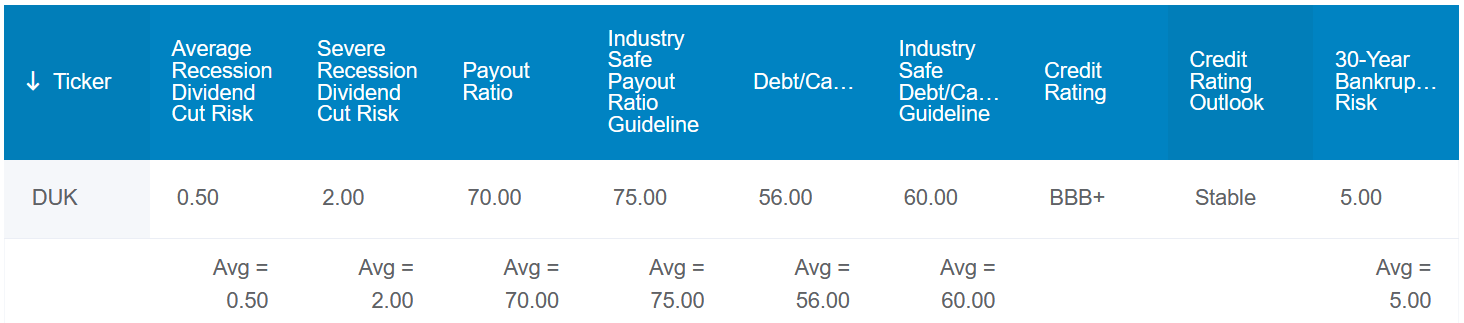

That is evidenced by a 70% EPS payout ratio, which is below the 75% EPS payout ratio that rating agencies consider safe for utilities. Duke Energy's 56% debt-to-capital ratio is also marginally lower than the 60% debt-to-capital ratio preferred by rating agencies. Thus, S&P awards a BBB+ credit rating to the electric utility on a stable outlook.

For these reasons, the probability of Duke Energy cutting its dividend in the next average recession is only 0.5%. Even in the next severe recession, that risk rises to merely 2%.

{kind=link}

Since I last covered Duke Energy four and a half years ago, it has grown into its valuation. Using historical dividend yield and P/E ratio, the electric utility is worth $99 a share. Relative to the $98 share price (as of January 15, 2024), Duke Energy could be nearly 1% undervalued.

If the company grows as anticipated and reverts to fair value, here are the total returns that it could generate for shareholders in the coming 10 years:

- 4.2% yield + 6.1% FactSet Research annual growth consensus + 0.1% annual valuation multiple expansion (rounded up to the nearest tenth of a percent) = 10.4% annual total return potential or a 169% 10-year cumulative total return versus the 8.6% annual total return potential of the S&P or a 128% 10-year cumulative total return

Solid Third-Quarter Operating Results

{kind=link}

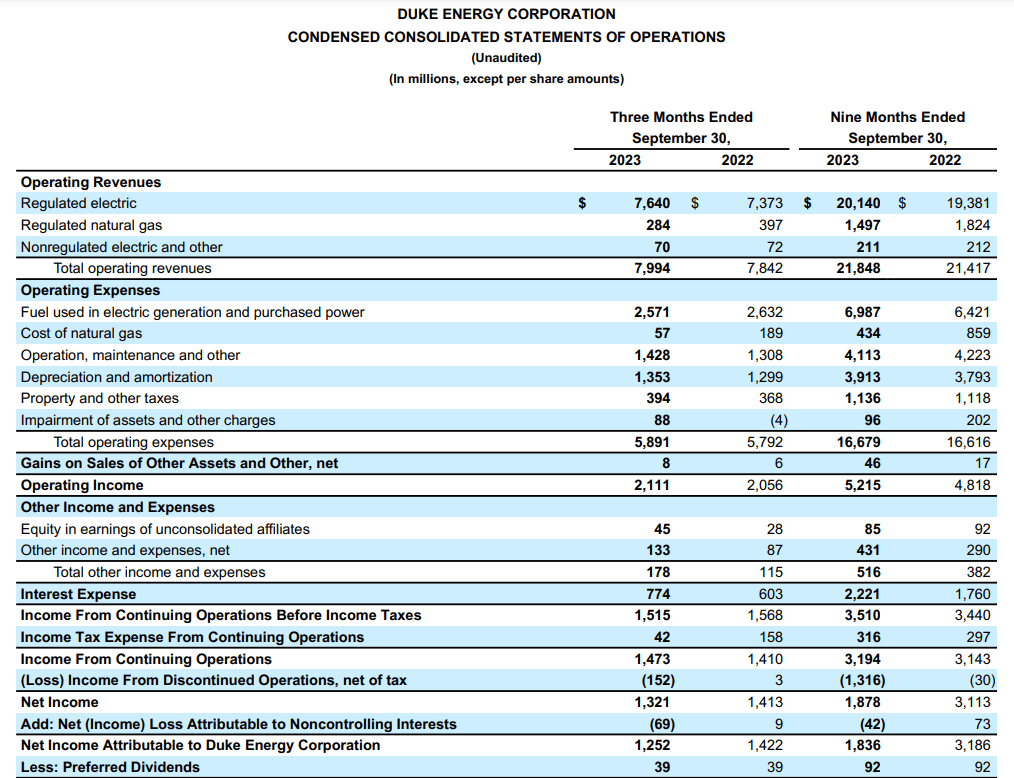

Duke Energy's results for the third quarter ended September 30 weren't flashy, but they were just fine. The company's total operating revenue edged 1.9% higher year-over-year to $8 billion in the quarter, which missed the analyst consensus by $150 million .

Duke Energy's slight revenue growth was driven by 3.6% growth over the year-ago period in the regulated electric segment operating revenue to $7.6 billion. This was led by $155 million in additional fuel revenues stemming from higher fuel cost recovery. Equally as important, the company benefited from a $146 million increase in storm revenues by Duke Energy Florida due to collections related to Hurricanes Ian and Nicole. Favorable rate case activity in South Carolina and North Carolina, as well as base rate adjustments in Florida, were other catalysts.

These catalysts were partially offset by a $141 million decrease in revenue due to lower demand at Duke Energy Florida and a $72 million revenue decline from unfavorable weather.

Moving to the regulated natural gas segment, operating revenue plunged by 28.5% year-over-year to $284 million during the third quarter. Substantially lower natural gas rates and lower volumes contributed to these headwinds (details in the previous three paragraphs sourced from pages 95-97 of 146 of Duke Energy's 10-Q filing ).

Duke Energy's adjusted EPS surged 9% higher over the year-ago period to $1.94 for the third quarter. A higher operating revenue base and a 120 basis point expansion in non-GAAP net profit margin to 18.6% were the contributing factors. That explains how adjusted EPS growth exceeded operating revenue growth in the quarter.

Additionally, CFO Brian Savoy reiterated the company's 5% to 7% annual earnings growth rate guidance through 2027 in his opening remarks during Duke Energy's Q3 2023 earnings call . That's because the electric utility appears to have the cash flow necessary to support its $65 billion five-year capital spending plan through 2027.

Additionally, Duke Energy's balance sheet is on sound footing. Even in this environment of elevated interest rates, the company's interest coverage ratio was 2.6 through the first nine months of 2023. For most other industries, this interest coverage ratio would be cause for concern. But the nature of the regulated utility industry makes this metric of Duke Energy's acceptable.

Dividend Growth Should Continue

Duke Energy's quarterly dividend per share has grown by 10.6% cumulatively in the last five years to the current rate of $1.025 . This probably isn't going to impress anybody.

However, the company's adjusted EPS payout ratio is continuing to improve. In 2018, the payout ratio was 77% ($3.634 in dividends per share paid versus $4.72 in adjusted EPS). Using the midpoint adjusted EPS guidance of $5.60 for 2023, the payout ratio in 2023 will be a more manageable 72.5%. As the company expects to keep heavily investing in capital spending, I wouldn't expect dividend growth to materially accelerate anytime soon. However, Duke Energy's modest dividend growth is offset by a higher starting yield and improved overall growth prospects in my opinion.

Risks To Consider

Duke Energy is a leading utility, but that doesn't make it immune to risks.

As is the case with most publicly traded utilities, the company is focused on achieving net-zero carbon emissions from electricity generation by 2050. This objective exposes the company to risk.

Duke Energy could be too aggressive in investing to meet this goal. There is the potential that the company could invest simply for the sake of meeting this objective and get complacent about the returns that these investments generate for investors.

Another risk to Duke Energy is its nuclear fleet which is being utilized to meet these goals. The company has 11 reactors in operation at six nuclear stations that it is seeking to renew the licenses of for an additional 20 years. If any of these reactors experienced incidents, that could result in legal liability for the company and harm its good standing with regulators (page 25 of 330 of Duke Energy's 10-K filing ).

Regulatory risk is also another risk that Duke Energy faces moving forward. If the company experiences adverse outcomes with rate cases in any major markets, that could weigh on growth potential. The good news is that the company is relatively diversified across numerous markets, so one bad rate outcome won't completely torpedo its growth prospects.

Summary: I'd Prefer A Margin Of Safety Before Upgrading To A Buy

{kind=link}

{kind=link}

To be clear, Duke Energy has the potential to deliver 10% annual total returns in the years ahead. My only issue with the company is that the current valuation doesn't offer an adequate margin of safety. Duke Energy's 17.5 blended P/E ratio is slightly beyond its normal P/E ratio of 16.1. Thanks to improving growth prospects, I would argue that this premium over its historical average can be justified.

However, if Duke Energy falls short of analyst growth expectations, the likelihood of double-digit annual total returns drops drastically. This is why until the utility falls back into the low-$90s or becomes more valuable over time, I am maintaining a hold rating.

For further details see:

Duke Energy: Watch This 4%-Yielding Dividend Stock