DUK - Duke's 4% Yield Is A Cornerstone Of My Portfolio

2023-05-11 09:44:10 ET

Summary

- Duke Energy is a low-volatility stock with a rock-solid business model and a 4% dividend yield.

- DUK has outperformed well-diversified ETFs with lower volatility, making it a great way to lower cyclical risks.

- DUK's dividend has a healthy payout ratio, is backed by solid fundamentals, and has grown in line with average inflation.

- With a $36 billion grid investment plan, Duke Energy is poised for sustainable earnings growth and continued dividend growth.

Introduction

Duke Energy ( DUK ) may be the most boring stock in my portfolio. However, that's a good thing, as it's doing exactly what it's supposed to do. In this article, I want to talk about this 4%-yielding stock, which comes with a rock-solid business model, dividend growth in line with average inflation, and the ability to outperform the market in times of turmoil.

FINVIZ

While DUK isn't a company that will make me rich, I have made it a cornerstone of the defensive exposure in my portfolio, thanks to its ability to deliver high and consistently-growing income without exposing investors to high volatility.

Low-Volatility Outperformance

While stocks, in general, are a great way to build wealth, I would make the case that some stocks are protectors of wealth while others are more suitable for growing wealth purposes (with slightly higher risks). Then, there are stocks in the middle that come with both wealth protection and growth.

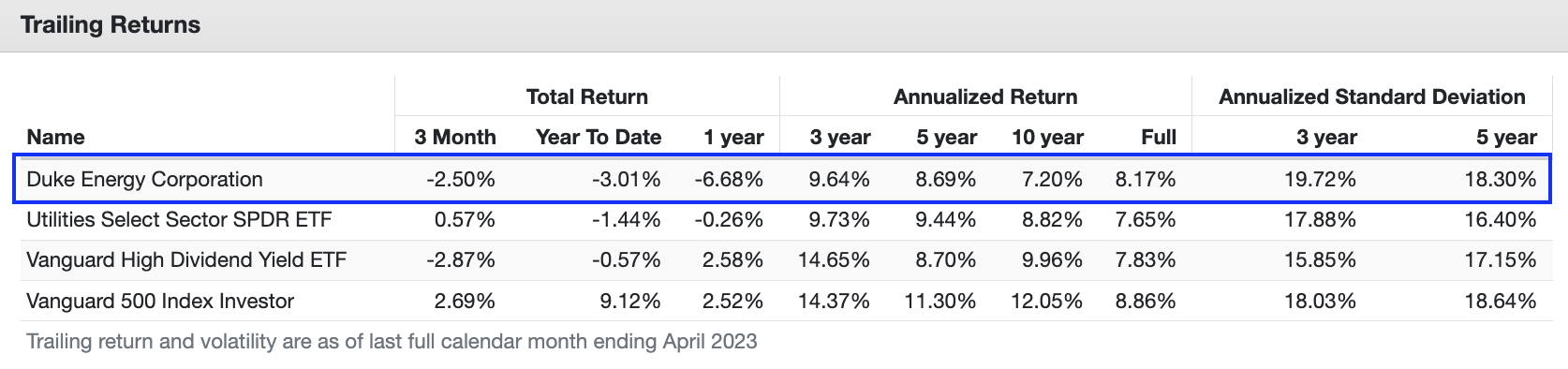

Going back to December 31, 2006, DUK has returned 8.2% per year. It slightly underperformed the S&P 500. However, it outperformed both the Utilities ETF ( XLU ) and the Vanguard High Yield ETF ( VYM ). It also came with low volatility. The standard deviation was 15.5%, which is below the S&P 500 standard deviation and barely higher than the standard deviations of the aforementioned ETFs. That is a mighty impressive result, as we're comparing a single company to well-diversified ETFs.

{kind=link}

With that said, it needs to be said that DUK failed to outperform its peers when excluding the Great Financial Crisis. Over the past ten years, DUK has underperformed its peers.

{kind=link}

That isn't necessarily a bad thing. However, it means investors need to make an important trade-off:

- The XLU ETF yields 3.0%

- DUK yields 4.1%

- DUK has a 7.6% weighting in the XLU ETF.

- The XLU ETF is overweight in NextEra Energy (NEE) with a 15.2% weighting, and it includes other utilities with lower yields and higher growth.

XLU benefited from the low-rate environment of the past ten years, which benefited fast-growing utilities more than DUK.

The chart below shows the ratio of the DUK total return and the XLU total return compared to the Russell 2000 Value total return versus the Russell 2000 Growth total return. While the two indicators do not move in lockstep, we can see that DUK started to seize underperforming XLU the moment the market shifted from growth stocks to value stocks roughly three years ago.

In other words, while I am consistently looking for opportunities that could provide me with a better risk/reward in the high-yield space, I feel that DUK is a great way for me to lower cyclical risks given my energy exposure of almost 20% and more than 40% industrial exposure.

What To Make Of DUK's Dividend

A high yield backed by solid fundamentals.

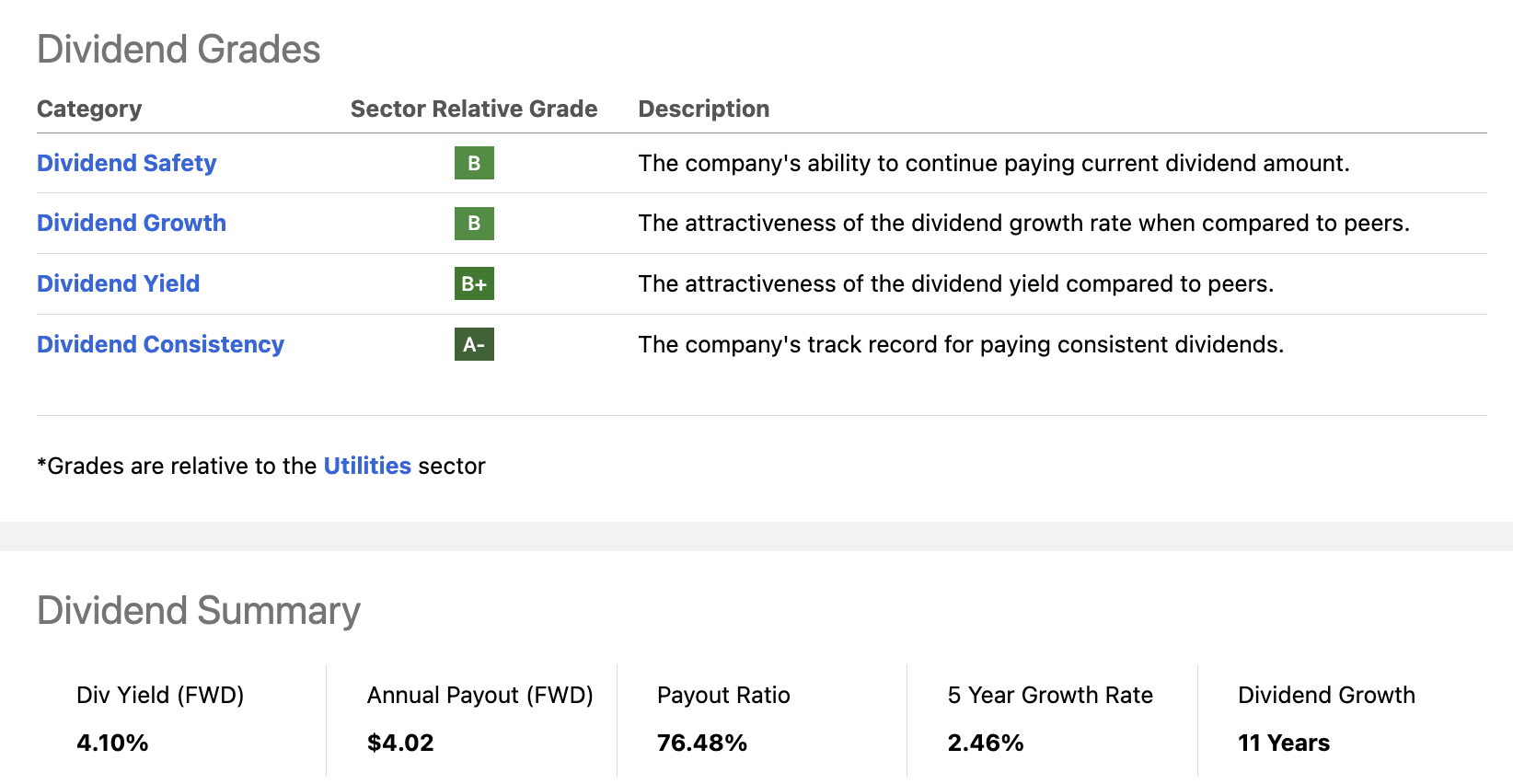

DUK has a 4.1% dividend yield. This is based on a $1.005 per share per quarter dividend.

When looking at the dividend scorecard below, we see a lot of green. The company has satisfying scores in the safety, growth, and yield categories. It scores higher in the consistency category.

{kind=link}

Here are some factors that go with this scorecard.

- The company has a 76% payout ratio, which is above the sector median of 63%.

- The cash payout ratio is 40%. The sector median is 31%.

- The median sector yield is 3.5%.

- DUK's dividend has grown by 2.5% per year over the past five years. The 10-year average annual dividend growth rate is 2.8%. None of this is high. However, it protects investors against average inflation - not the inflation we're currently dealing with.

DUK has a terrific dividend track record. The only reason why the dividend imploded in 2006 is the Spectra Energy spin-off, which is now a part of Enbridge ( ENB ).

With that said, this dividend isn't just backed by a healthy payout ratio but also by a business that continues to do well in a high-rate environment. After all, DUK has close to $75 billion in net debt.

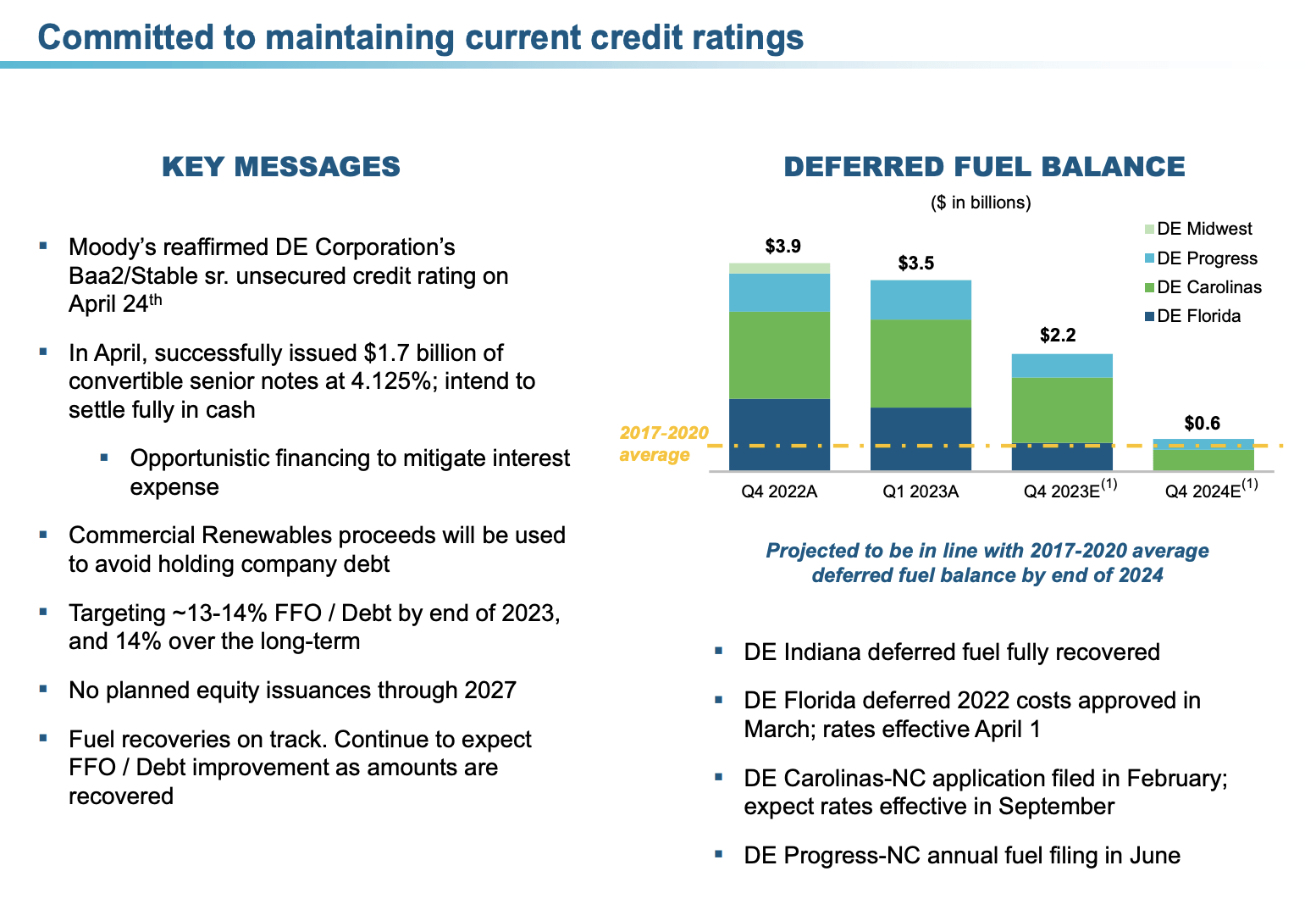

The good news is that the current debt ratio is at 5.9x EBITDA (BBB+ credit rating) and is not expected to increase in the years ahead, despite a high investment plan.

{kind=link}

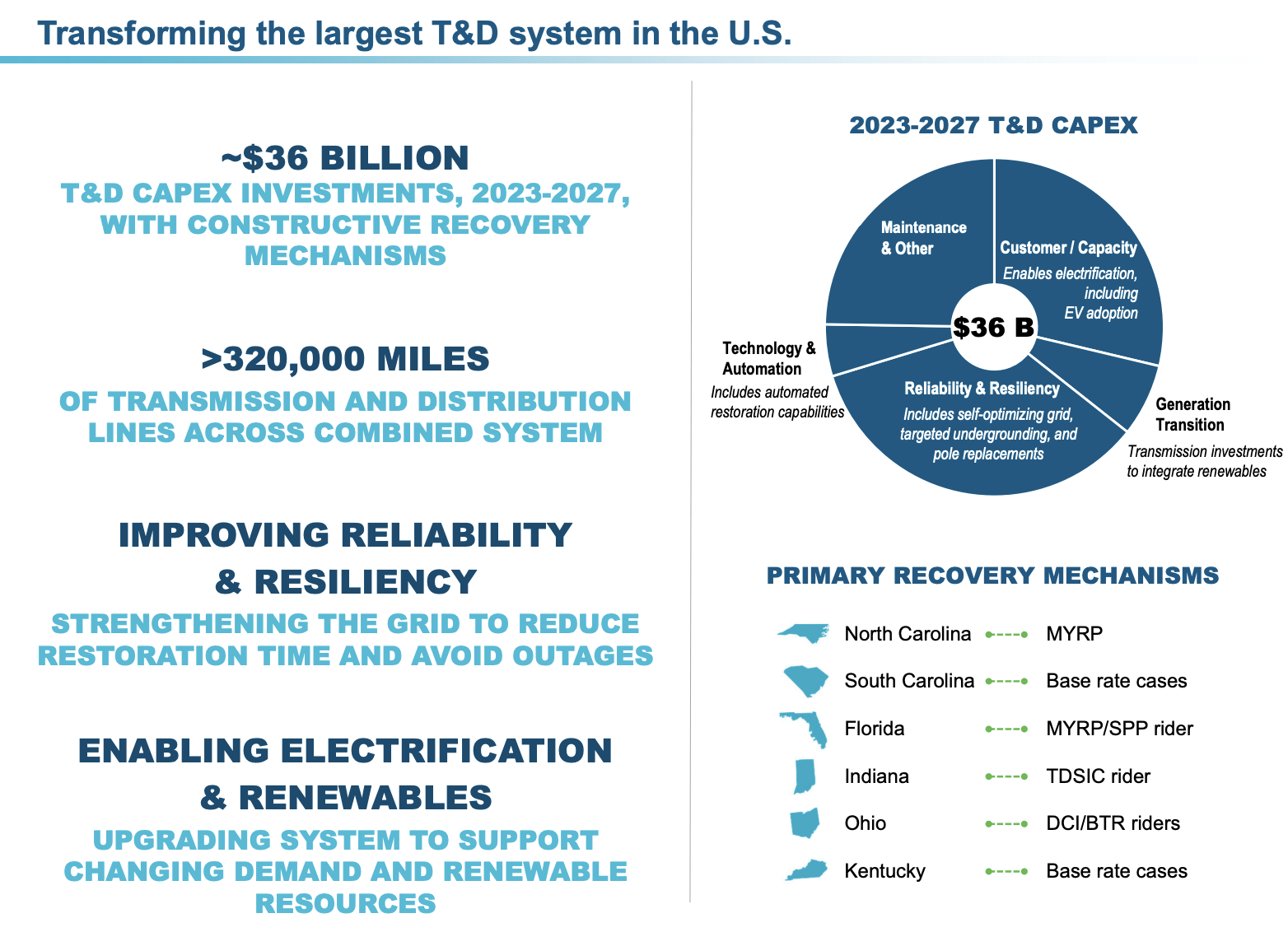

A big part of the company's investments is its grid investment plan, which is $36 billion and accounts for over half of its five-year capital plan and is critical to the company's energy transition. With more than 320,000 line miles, Duke Energy operates the largest transmission and distribution system in the nation.

{kind=link}

According to the company , these investments are expected to support steady earnings growth that supports its balance sheet and - as a result - continuing dividend growth.

From grid improvements to installing renewables to advancing policy, we're taking collective action to transform and ready the system for the future. We have a clear path forward and are confident our investment plan will deliver sustainable value and 5% to 7% earnings growth.

Furthermore, with regard to its financing operations, Duke Energy completed around 60% of its planned 2023 issuances and took advantage of market dynamics, which made convertible notes an attractive option.

Duke issued $1.7 billion of these notes in April to reduce its commercial paper balance and lower interest expenses. Duke Energy received approval for a full recovery of the 2022 deferred fuel balance in Florida and filed for recovery of approximately $1 billion of deferred fuel in DEC North Carolina.

The company also continues to expect proceeds from the sale of commercial renewables in the second half of this year, which will be used for debt avoidance at the holding company.

Based on this context and according to the company (emphasis added):

I know the balance sheet is top of mind for investors, and credit is at the forefront of our planning as well. In fact, our efforts and commitment to the balance sheet were recently recognized by Moody’s. In April following their Annual Meeting, Moody’s reaffirmed our current credit ratings and stable outlook at the holding company. This is further evidence that we have the right plan in place and are taking appropriate steps to maintain our strong balance sheet as we advance our energy transition and execute our capital plan .

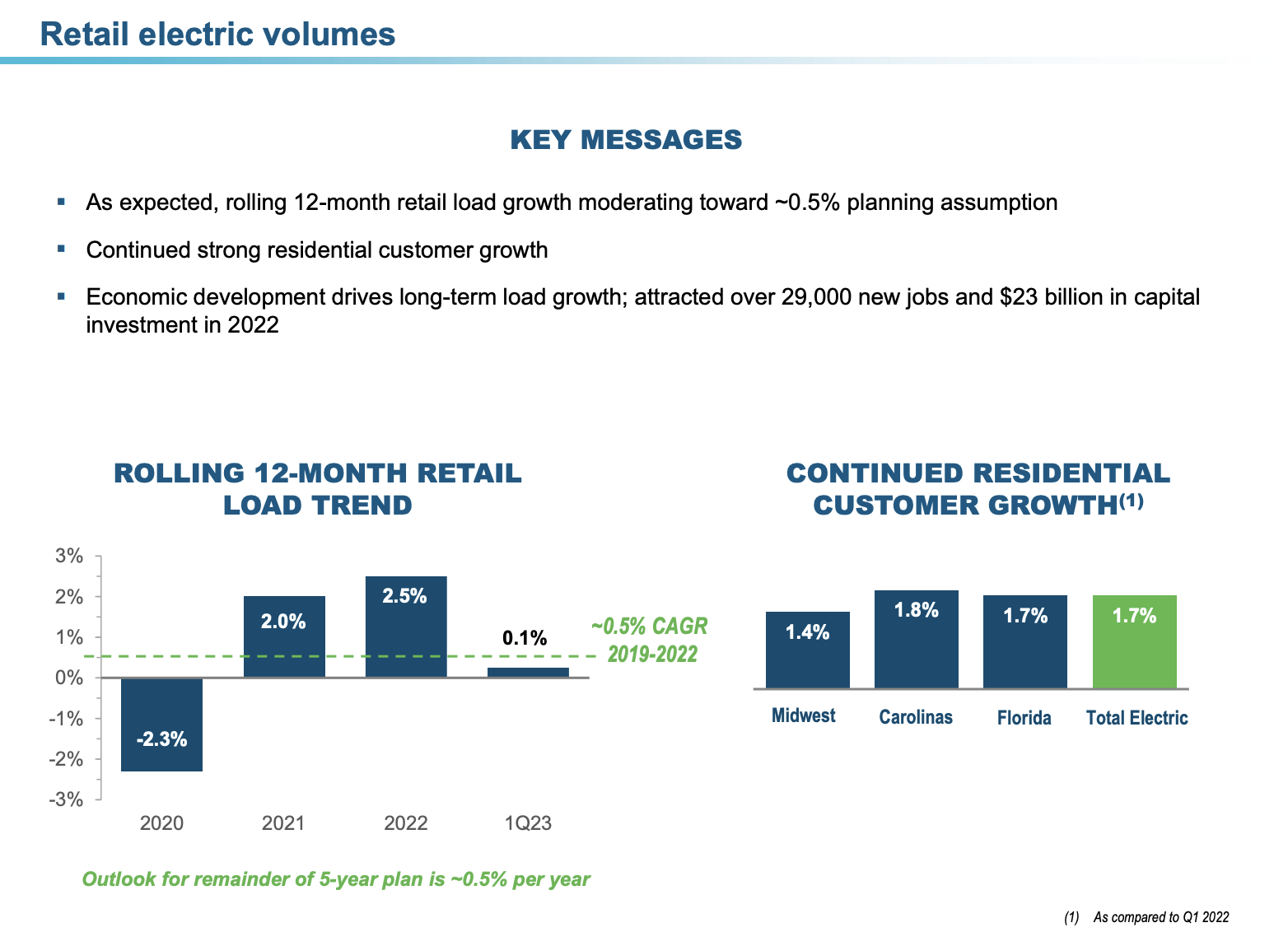

It also helps that demand trends are favorable. On a rolling 12-month basis, load growth has moderated closer to pre-COVID trends. The Q1 weakness this year was seen in January and February when the weather was extreme. In March and April, when the weather was closer to normal, volume trends were more consistent with expectations, giving the company confidence that the full-year 2023 load growth could be in the neighborhood of 0.5%.

{kind=link}

Strong continued customer growth in the residential class also supports confidence in the company's outlook.

Valuation

DUK's valuation is fair. Not too expensive and not anywhere close to deep value. DUK shares are trading at 12.3x 2023E EBITDA, which is well below the pandemic peak but above the longer-term median.

The same applies to the price-to-earnings or price/earnings ratio. Using 2023 expectations, the ratio is in line with the long-term median.

Sell-side price targets reflect this. The average price target is $109, which is roughly 10% above the current price ($99).

I think this is a fair price.

While waiting for weakness could always end up giving investors a better entry, I believe that current prices offer good value for investors looking to buy high-quality defensive income.

Takeaway

Duke Energy is a low-risk, low-volatility stock that offers a 4% yield with a strong business model dividend growth in line with inflation. While DUK's returns have underperformed its peers over the last ten years, it has outperformed the S&P 500 and other diversified ETFs in the past.

Investors must balance the higher yield of DUK compared to ETFs, which have lower yields and higher growth. Duke Energy's dividend is backed by a healthy payout ratio and a business that continues to do well in a high-rate environment.

Duke Energy's $36 billion grid investment plan is a critical part of its energy transition, which is expected to support steady earnings growth and continuing dividend growth.

The valuation is fair.

All things considered, I believe DUK is a great tool to add low-risk high yield to both dividend growth and high-yield portfolios.

For further details see:

Duke's 4% Yield Is A Cornerstone Of My Portfolio