DLTH - Duluth Holdings: Margin Expansion Likely In 2023

2023-04-07 02:04:47 ET

Summary

- The management saw its sales growth trend stabilize in 2023 and had growth drivers such as new product offerings, new market entries, and acquisitions.

- The management expected to see margin improvements in 2023, through gross margin expansion and advertising and selling expense leverage.

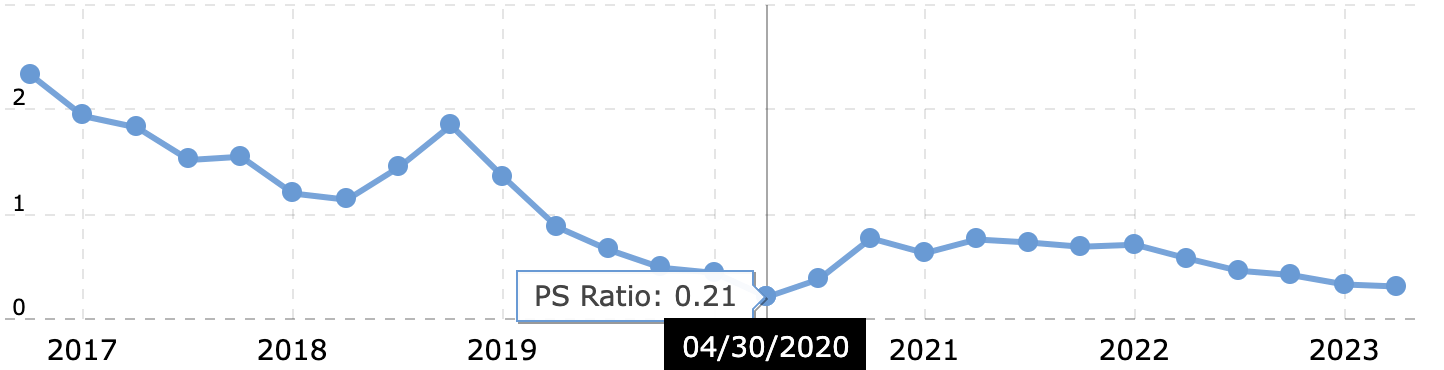

- The stock's P/S ratio of 0.32x is near the bottom of its historical low. This can provide comfort for investors, who would like to invest at this level.

- Catalysts for this company are likely margin expansion through its entry into the women's market. If its women's business continued to show sustained growth or accelerated growth in the coming quarters, we will be glad to convince ourselves of its comeback.

Investment Thesis

Duluth Holdings, Inc. ( DLTH ) saw its sales growth trend stabilize in 2023 and had growth drivers such as new product offerings and acquisitions. The management expected to see margin improvements in 2023, through gross margin expansion and advertising and selling expense leverage.

We think its gross margin of 52.5%, which is higher than many of its peers per Seeking Alpha, is a strong testament to its loyal customer base. If the company can leverage its strength to enter into new space, this can improve its profitability significantly.

If we look at its P/S ratio history, the stock is now trading near the bottom of its historical low of 0.21x. This can provide some comfort for investors, who would like to invest at this level.

Catalysts for this company are likely margin expansion through its entry into the women's market. If its women's business continued to show sustained growth or accelerated growth in the coming quarters, we will be glad to convince ourselves of its comeback. We rate this stock as neutral.

Company Profile

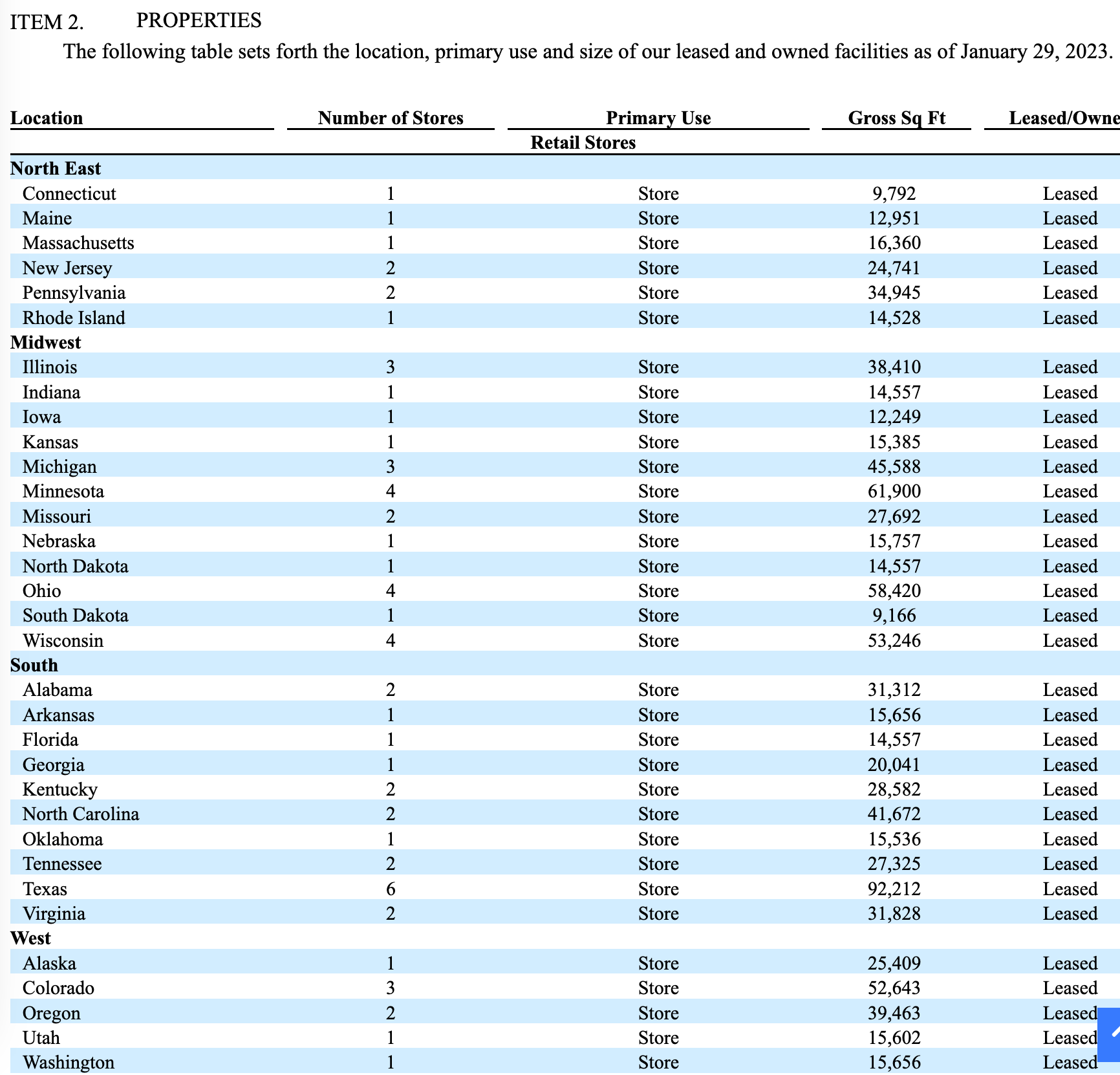

Duluth Holdings, Inc. is a lifestyle brand of men's and women's casual wear, workwear, and accessories primarily sold through its own omni-channel platform. As of January 29, 2023, it operated 62 retail stores and three outlet stores across 32 states with 4 fulfillment centers. The company employed 964 full-time and 1,582 part-time and flexible part-time employees.

Store locations (Company's filing)

{kind=link}

Key Takeaways from Q42022 Earnings:

- In Q42022, its sales decreased 10.7% to $241.8 million from $270.8 million. Retail store net sales decreased by 8.2% due to slower store traffic, partially offset by continued strong conversion rates. Direct-to-consumer net sales decreased by 12.0%. Women's apparel net sales increased by 1.7% due to continued strength in the AKHG collection.

- In Q42022, its gross margin decreased to 51.2% from 53.8% of net sales, due to a lower mix of full-price sales, coupled with deeper discounts as a response to the heavily promotional fourth quarter industry environment.

- In Q42022, its SG&A% increased to 46.8% from 44.9%.

- As of Dec 2022, its inventory increased 26% to $154.9 million, due to the planned pull forward of spring 2023 receipts in the fourth quarter to avoid any supply chain constraints.

The Company provided the following fiscal 2023 outlook:

- Its sales will remain flat and be in the range of $645 million to $660 million.

- Its adjusted EBITDA will increase by 10%and be in the range of $47 million to $49 million.

- Its CAPEX will increase to $55 million from $22 million.

We have the following comments:

- The management saw its sales growth trend stabilize in 2023. Though the company has no plan to open new stores in 2023, the management mentioned growth drivers such as new product offerings and acquisitions.

- The management expected to see margin improvements in 2023. This will be done through gross margin expansion and advertising and selling expense leverage, offset by G&A deleveraged due to increase investments.

- The company will increase investment in advertising on expanding brand awareness, acquiring new customers, and driving growth in both its men's and women's businesses. They also reformatted 20 stores to expand the women's assortment. We can see that Duluth has been working and deliberately transforming its brand image from a male-driven to a neutral stance. Although it could be too soon to see the initiatives in its financials, we think there is definitely some solid growth potential.

- The company will increase CAPEX to web platform upgrades, warehouse management systems, and fulfillment network expansion. Although the company has no immediate plans for opening new stores, we believe that investing in improving its online shopping experiences is crucial for the business to lift its margins. The advantages of omni-channel in lead generation and inventory clearance were also emphasized by the management.

This omni-channel functionality is critical for clearing through seasonal and clearance goods in the store's inventory, making room for the transition to the new season.

During 2023, we plan to continue refining and building on our omni-channel capabilities, focused heavily on delivering a frictionless experience while generating more reasons to visit the stores.

Supplier Concentration on Watch

The company does not own or operate any manufacturing facilities. Instead, the company arranges with third-party vendors for the manufacturing of its merchandise. The company has long-term relationships with its vendors. In 2022, 56% of its purchases came from an agent partner in Hong Kong who manages multiple factories across Asia and Latin America, including Vietnam, Indonesia, Cambodia, Bangladesh, Pakistan, China, Mexico, and Egypt. The company leverages the agents' purchasing power with multiple factories, as well as transportation and logistics capabilities.

We believe that the high concentration is undoubtedly a concern for investors. The company mentioned in this earnings the need to build up more inventories in advance in case of supply shortages. This indicates its weak bargaining power toward suppliers.

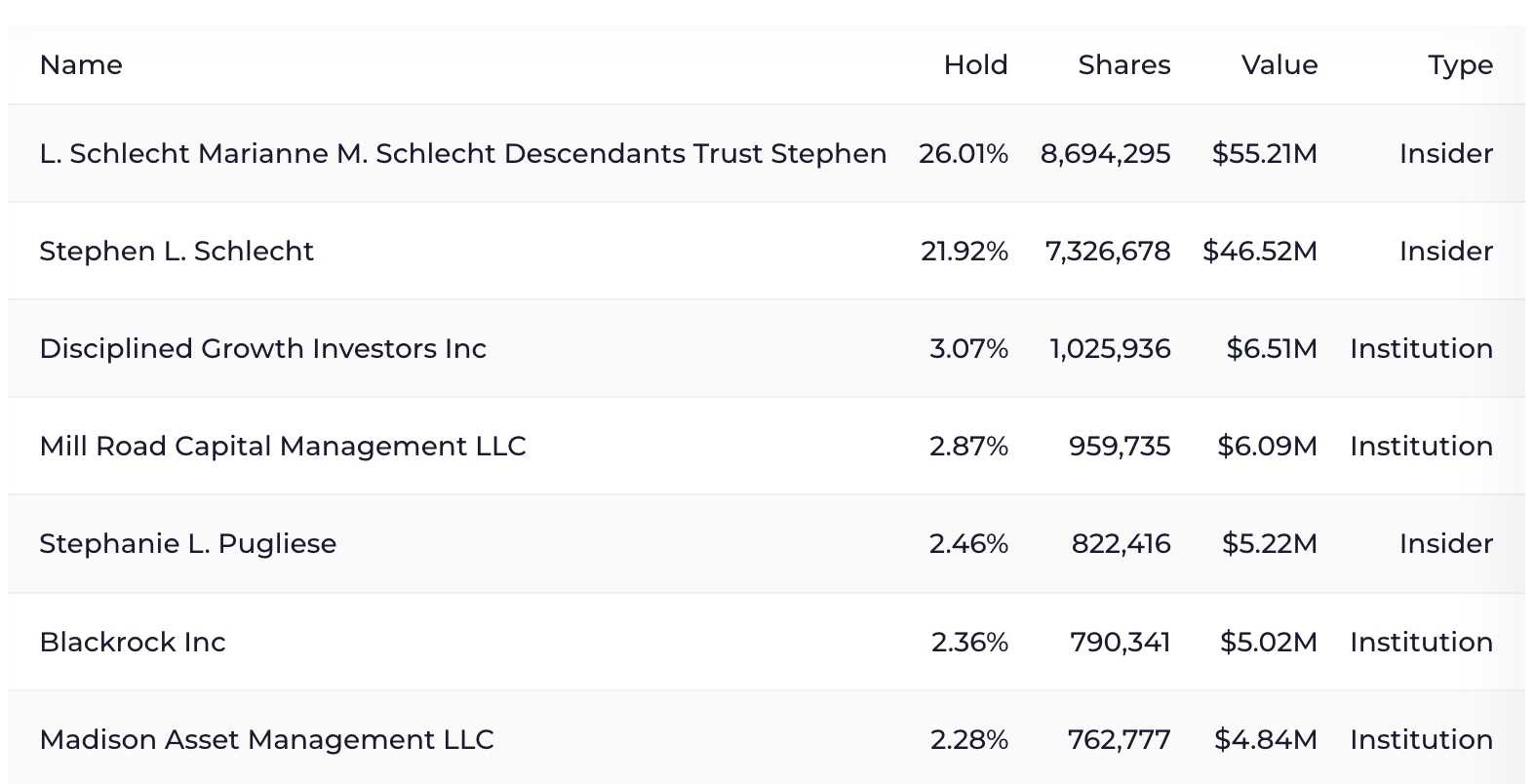

A Family-Owned Business with a Low Drive to Improve Minority Shareholder Returns

The company is owned by Stephen Schlecht. His son Richard Schlecht works as SVP of Product, Merchandise, and Inventory of the company.

{kind=link}

The company has no history of dividend issuance or has limited share buyback practice. The company's stock compensation expense as a percentage of its revenue was 0.4%. It is clear the team lacks the incentives to improve shareholder returns.

New Market Entry can Improve Its Profitability

Despite its gross margin of 52.5% in 2022, the company's operating margin was close to 0%. We think this is the result of an aggressive geography expansion strategy.

The company operated 62 retail stores and three outlet stores across 32 states with 4 fulfillment centers. Take a look at other peers for instance: Wolverine World Wide (WWW) operated 154 stores with 5 fulfillment centers and Buckle Inc. (BKE) operated 441 stores in 41 states with 1 fulfillment center. Duluth Holdings has a relatively lower store density than other companies but more fulfillment centers. The high occupancy and shipping costs as a percentage of sales explain its low operating margin. Its SG&A expenses %, and shipping and processing expenses % were 52% and 6.7%, respectively, in 2022.

The Good news is that the company has no plan to open new stores in 2023 and focuses to expand into the women's market. This can curb the occupancy expense to grow. The management mentioned the new product offerings and re-platform of its website in support of its women's business. The company also said there were early signs of success since its women's business grew faster than its men's business during the quarter.

Our women's business grew 1% overall led by improvements in our new product expansions, the launch of AKHG in the spring of 2022, and overall improvement in our inventory position. Our women's first layer category, which includes the No-Yank Tank collection, was up over 40% to last year. Our bra collection, including the recently introduced Line Tamer bonded bra, grew 10% in the quarter, driven by new innovations in fabric and design, featuring soft and seamless construction to prevent lines and bulk.

The launch of our spring swim collection for men and women is underway now and expands our AKHG Lost Lake collection with greater choice to mix and match tops and bottoms, all with the purpose of providing the necessary sun protection, fast-drying fabrications, and stylish patterns.

The company's gross margin of 52.5%, which is better than many of its peers according to Seeking Alpha, is in our opinion a clear indication of the company's engaged customer base. If the company can leverage its strength to enter into new space, this can improve its profitability significantly. Therefore, we will be watching and seeking more evidence of its sustained growth in its women's business.

{kind=link}

Valuation and Catalysts

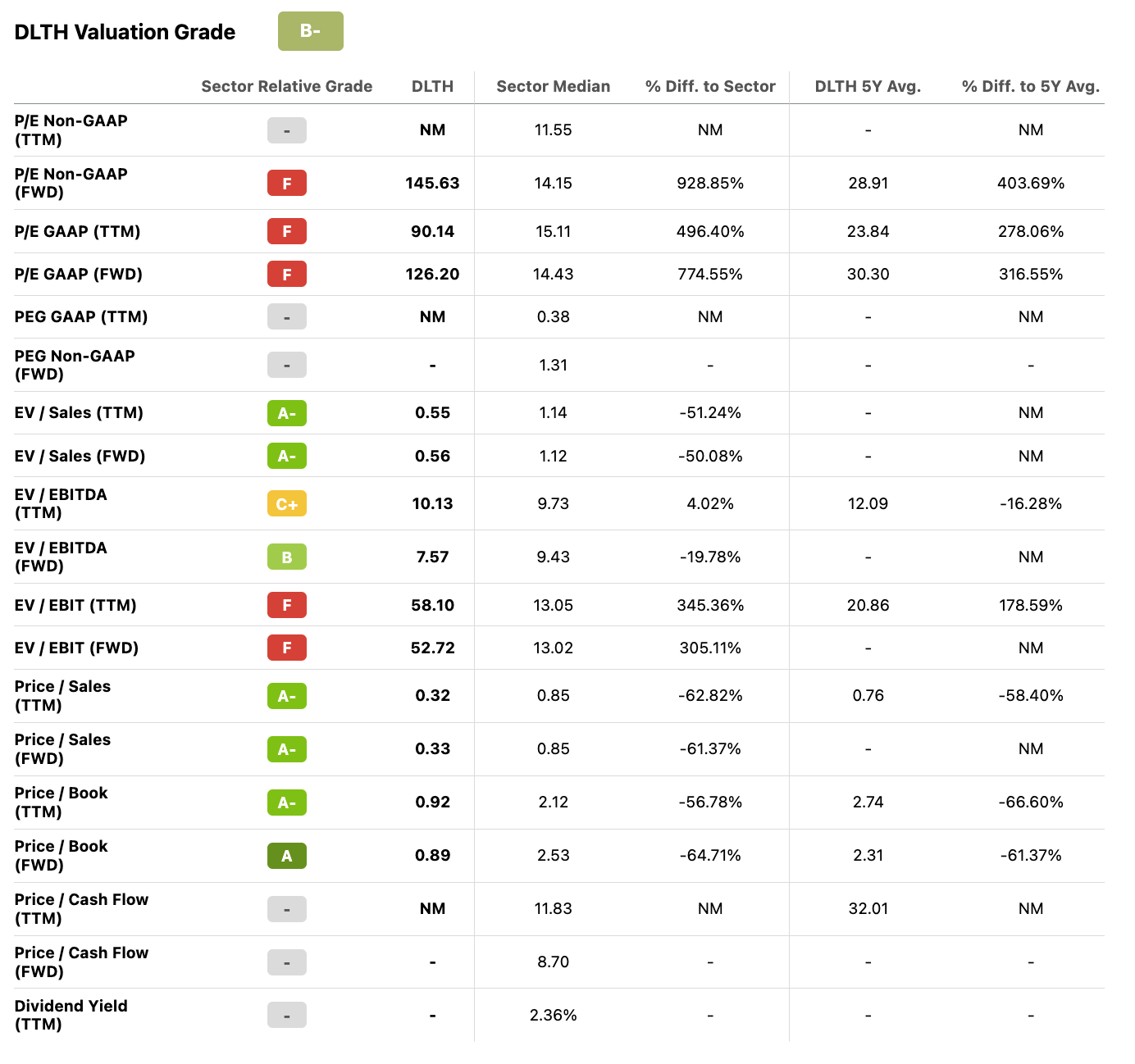

The valuation multiples on EV/S or P/S are definitely cheap. We think this can be the result of its low earnings.

From an M&A standpoint, the company could be an ideal acquisition target for larger conglomerates in the consumer space. However, we think the acquisition premium is limited. Given that the company's widespread stores are mostly located away from malls or traffic centers, this creates extra costs for the acquirer to integrate into its portfolio. We do not see the M&A opportunity as attractive.

{kind=link}

The company was aggressive in expanding its geography presence and thus resulting in low earnings due to high occupancy costs. Its P/E ratio is not meaningful for investors at the moment. However, if we look at its P/S ratio history, it is now trading near the bottom of its historical low of 0.21x. Thus, this can provide some comfort for investors, who would like to invest at this level.

{kind=link}

Catalysts for this company are likely margin expansion through its entry into the women's market. If its women's business continued to show sustained growth or accelerated growth in the coming quarters, we will be glad to convince ourselves of its comeback.

However, we think the lack of a mechanism to align the interests of minority shareholders with management is negative.

Risks

Liquidity risk

The company maintained very low cash on hand. Its cash conversion cycle was 107 days in 2022 but its quick ratio was only 0.6x as of the end of 2022. The management mentioned the company had 0 bank debt and thus had the flexibility when needed.

Summary

The management saw its sales growth trend stabilize and margin expansion in 2023.

The company's gross margin of 52.5%, which is better than many of its peers according to Seeking Alpha, is in our opinion a clear indication of the company's engaged customer base. If the company can leverage its strength to enter into new space, this can improve its profitability significantly.

If we look at its P/S ratio history, the stock is now trading near the bottom of its historical low of 0.21x. This can provide some comfort for investors, who would like to invest at this level.

Catalysts for this company are likely margin expansion through its entry into the women's market. If its women's business continued to show sustained growth or accelerated growth in the coming quarters, we will be glad to convince ourselves of its comeback.

For further details see:

Duluth Holdings: Margin Expansion Likely In 2023